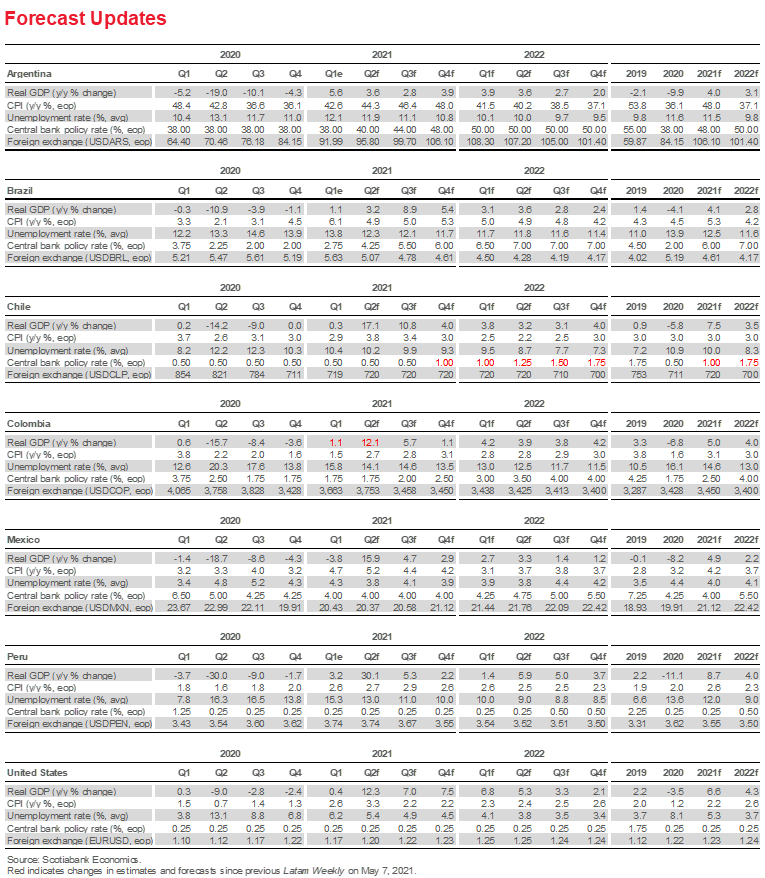

FORECAST UPDATES

- A hawkish hold by Chile’s BCCh on May 13 based on an improved economic outlook prompted our team in Santiago to bring forward its forecast for a first rate hike from January 2022 to October 2021.

ECONOMIC OVERVIEW

- Moves by some G10 central banks to taper—or talk of tapering—asset purchases and make monetary policy less accommodative in the face of rising inflation and rebounding economies raises questions about whether EM central banks will also have to accelerate their normalization processes. We look at the implications for our Latam rates forecasts.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

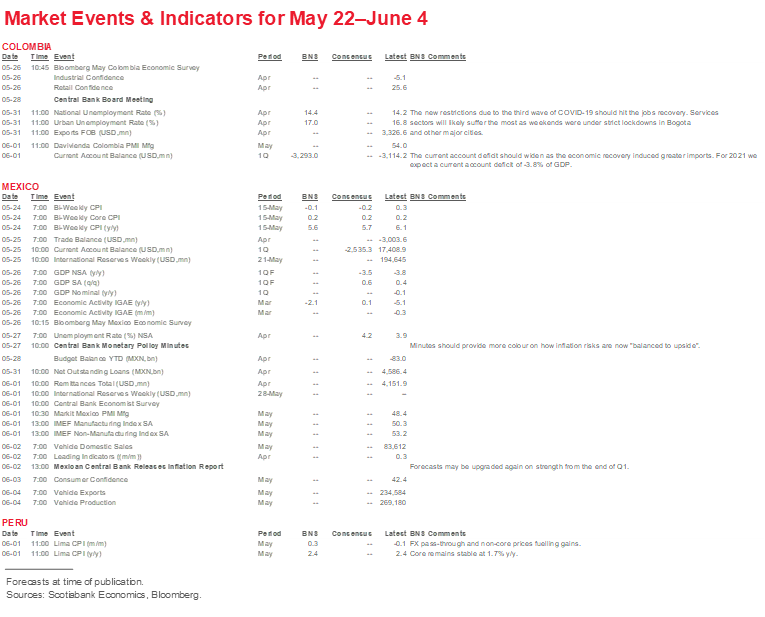

MARKET EVENTS & INDICATORS

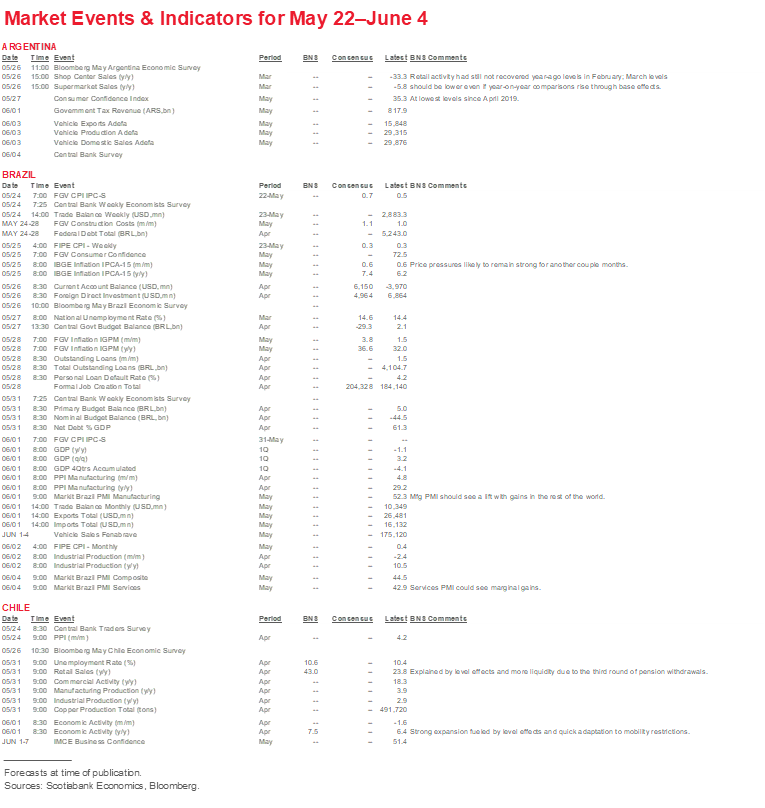

- A comprehensive risk calendar with selected highlights for the period May 22–June 4 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Steady as It Goes

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

- Moves by some G10 central banks to taper—or talk of tapering—asset purchases and make monetary policy less accommodative in the face of rising inflation and rebounding economies raises questions about whether EM central banks will also have to accelerate their normalization processes.

- Our forecasts continue to see Pacific Alliance central banks lifting rates in late-2021 or 2022.

CENTRAL BANKS: REBOUNDS, TAPER TALK, AND POLITICS

Our forecasts remain broadly stable as we watch sequential month-on-month developments in March and April data and look through skewed year-on-year comparisons with the beginning of 2020’s pandemic induced lockdowns (see Forecast Updates on pp. 2 and 3). Macro data are broadly tracking continued recoveries across Latam, with some generalized strengthening in growth across sectors and activities even in the face of the latest restrictions that were imposed in response to COVID-19’s latest wave. Households, businesses, and governments in the Pacific Alliance countries have all become progressively more effective at operating under a range of public-health protocols. With vaccination roll-outs accelerating across Latam and COVID-19 infection and hospitalization numbers starting to ebb from recent peaks, risks to our outlook are tipped to the upside in most cases.

The recent moves by central banks in the United Kingdom and Canada to begin tapering asset purchases—and the Fed’s shift to initiate talking about tapering—have raised questions about the extent to which emerging-market central banks will follow with accelerated normalization of very accommodative monetary policies. Recent moves in Latam equities and currencies have, however, been dominated lately by domestic political developments rather than “taper tantrum” concerns (tables 1 and 2); similarly, some of the region’s most pronounced yield-curve steepening has followed the delays in Colombia’s fiscal reform and the outcome of Peru’s first round of presidential voting (charts 1 and 2, respectively), rather than new from the Fed.

Latam central banks are currently showing some mixed performance against their inflation targets and relative to G10 monetary authorities (chart 3). While headline inflation in Chile, Colombia, and Peru remains well-behaved—even with the onset of base effects from 2020’s shutdowns—recent readings in Brazil and Mexico have landed well above their target bands. Brazil’s BCB has already started a quick hiking cycle in the hope that it may need to normalize policy rates only “partially” to bring inflation under control. In Mexico, a member of Banxico’s Board has taken the prospect of any further easing entirely off the table.

Real policy rates remain very accommodative across Latam (chart 4) and even with hikes expected across the region by mid-2022, monetary policy should still be supportive of further recovery. Looking across the forecast horizon in the Pacific Alliance countries (charts 5–8), real rates are set to turn more restrictive in Mexico in response to the present spike in prices, with Colombia joining it in positive territory in the coming months. With inflation still reasonably contained in both Chile and Peru, real rates could stay in negative territory into 2022 to ensure that output gaps continue to close. As such, we maintain our forecast that policy hikes will come first in Colombia (Q3-2021), followed by Chile (Q4-2021), Mexico (Q1-2022), and Peru (mid-2022).

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—New Political Cycle Begins as Constitutional Assembly Members are Elected

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

The May 15 and 16 elections marked the beginning of a new political cycle in Chile. Members of the Constitutional Assembly, regional governors, mayors, and members of the municipal council were elected in the most important vote in decades.

The composition of the Constitutional Assembly bespeaks the shift in the political forces that will write the new constitution. Among the winners, the independent lists and the far-left coalition stand out, with the Communist Party and Frente Amplio securing 28 of the 155 seats in the Assembly. On the other hand, the government’s coalition, Chile Vamos, suffered a big disappointment as it couldn’t secure one-third of the seats, which would have given them a blocking position on proposed articles for the new constitution; instead, they won only 37 seats. Furthermore, the Ex-Concertación—the left-of-centre coalition that governed the country from 1990 to 2010—also got a poor result, securing only 25 seats. The market reacted negatively to this political news: on Monday, May 17, the IPSA declined almost 10%, the CLP depreciated around 2% against the USD, and long-term interest rates increased about 15 basis points.

With no coalition reaching the two-thirds majority needed to approve each article in the new constitution, negotiations between and concessions from each group will be key to reaching agreements. Our preliminarily assessment suggests that the independence and autonomy of the central bank will not be modified. Other topics, such as the rules on fiscal responsibility and the existence of a private pension system may be altered in the new constitution.

Meanwhile, public-health measures continue to improve, albeit heterogeneously among age groups. ICU bed occupancy has continued to decline for older groups, but has seen a small increase for people younger than 49 years old (chart). This age group started its vaccination process some weeks ago, but its vaccination rates have been lower than that of older groups, which may explain why we haven’t observed the same improvement in ICU bed occupancy for this cohort. On the other hand, new infections have continued to decrease, but not as fast as the authorities would like, and the country is averaging more than 4,500 new cases per day.

On the monetary front, the BCCh had its third meeting of the year on May 13, which concluded with a decision to keep the key policy rate at its technical minimum of 0.5% and to maintain unchanged the central bank’s unconventional measures to support liquidity and credit. On the basis of the Board’s assessment of new and forthcoming liquidity injections to the Chilean economy, we brought forward our projection for the BCCh’s first 25 bps rate hike from January 2022 to October 2021.

Along with more developments and information regarding the views of Constitutional Assembly members, the next fortnight will be packed with the publication of tier-1 indicators. On May 31, we will know the sectoral and employment data for the month of April. We expect an increase of 43% y/y in retail sales in April, explained by the boost in consumption coming from the third withdrawal of pension funds and base effects from last year’s shutdowns. The unemployment rate should increase from 10.4% at end-March to 10.6% in the February–April moving quarter, as mobility restrictions were in place throughout March and April and the job recovery has been slower than expected.

On June 1 monthly GDP data for April will also be published. We expect an expansion of 7.5% y/y. Even though Chile experienced strict confinement measures during April 2021, the economy adapted well to these new restrictions, and there are favourable level effects, as April 2020 was the first month with full restrictions in the country.

Colombia—A Very Good Start to 2021 Could Be Offset by Recent Political Unrest

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

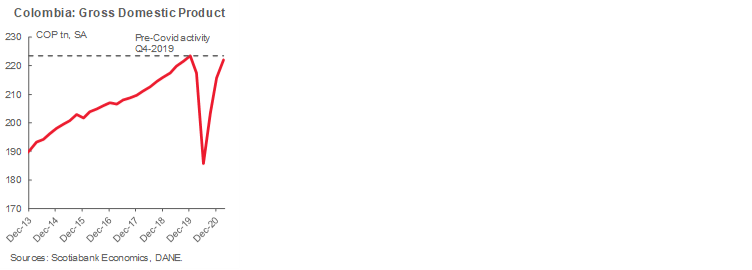

Colombian Q1-2021 GDP showed that economic activity started 2021 on the right foot: in seasonally adjusted terms, GDP grew by 2.6% q/q (1.1% y/y). In levels (COP trillions), Q1-2021 GDP was at 99% of what the country produced in Q4-2019 (chart), which represented a very positive surprise for markets and analysts and showed that the Colombian economy had gained resilience to the COVID-19 crisis. It is worth noting that, despite the economy broadly reaching pre-pandemic levels, sectors continue to exhibit a mixed picture: agriculture, industry, and financial activities outperformed in Q1 at 3.9%, 3.4%, and 4.3%, respectively, above pre-pandemic levels (Q4-2019), while mining and construction lagged in the recovery, with production levels 15.1% and 12.1% below pre-pandemic norms. Either way, the Colombian economy has consistently surprised to the upside, showing that the recovery has adapted to changing rules in terms of lockdowns in its major cities.

At the end of April, not only did Colombia face a third wave of the pandemic, but it also had to face nationwide protests that produced road blockades that lasted more than ten days, which raises the question of how much of the good production news from Q1-2021 will be netted-off by a strong contraction in May. Let’s look at how the protests have affected economic activity.

During the first ten days of the social unrest, major cities suffered from significant violence that negatively impacted commercial activities and manufacturing employees’ mobility. In fact, in Cali (9% of GDP) and Bogota (26% of GDP), between April 28 and May 8, most major activities were restricted to functioning on half days owing to the violent outbreaks and traffic problems during the protests.

Additionally, after the first three days of protests, people started to blockade the country’s principal inter-city roads, which produced significant goods shortages in major cities and impaired some supply chains owing to difficulties in bringing inputs to factories. According to Ministry of Finance data, the gross effect of the social unrest, so far, has been equivalent to -0.7 ppts of GDP, implying that the excellent news of Q1-2021’s gains will be partially offset by a much weaker Q2-2021 than previously expected. As a result, our counsel on the release of the Q1 numbers that our 5% y/y growth forecast for all of 2021 would likely have to be revised upward may not be realized. Still, our bias on this year’s growth outlook remains positive.

In terms of the long run, beyond 2021, our concerns are focused on potential output: if protests continue and cause FDI to hold back and domestic companies to postpone capex, we may need to lower our 4% y/y growth forecast for 2022 and shave our long-run average GDP growth forecast of 3.6% y/y for years farther out. As of now, we haven't yet seen any real impact from recent events on the investment plans of companies; however, we will keep an eye on projects to see if there are early signs of change.

Once the current political impasse is resolved, civil works should accelerate, focused on the reconstruction of infrastructure damaged by the protests. The economy has shown progressively more resilience to public-health restrictions. This, combined with accelerating vaccination deliveries to more Colombians should boost growth in H2-2021 and make up for recent losses. As a result, we have no trouble maintaining our 5% y/y forecast for 2021, with a continued upside bias—but we’ll wait for greater clarity on the next steps on fiscal reform before we revise our outlook.

Mexico—Growth and Inflation Expected to Move in the Right Direction as Elections Near

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

On May 24, we are scheduled to get bi-weekly CPI data for the first half of May. Consensus calls for a deceleration in inflation driven by non-core prices (Bloomberg’s consensus calls for headline -0.14% 2w/2w, and core 0.17% 2w/2w), which we agree with, although we see a slightly milder deceleration in headline prices than consensus (i.e., -0.11% 2w/2w). However, despite this temporary reprieve, we expect that price shocks will keep inflation highly volatile and above the 4% y/y top end of Banxico’s target range for 2021 (4.2% for year-end). A record drought hitting the country should push agricultural prices higher over the course of the North American summer. Similar events in Brazil are affecting global prices of certain agricultural commodities alongside beef export restrictions in Argentina. We also expect base effects combined with a rapid re-opening in the services sector to drive a services price spike into H2-2021: about half the country is already in “green traffic light” mode, and schools are expected to open briefly in June, and to be fully open at the start of the next school year in late-August. The TIIE curve is already pricing in 80% odds of a 25 bps rate increase over the coming 3 months, and over 50 bps of hikes by November. Our house call is for more patience from Banxico, with our view being that rate increases will kick off with the first meeting of 2022 through a 25 bps move.

Monthly GDP proxy data to be released on May 26 (INEGI’s IGAE index) is expected to show a decline of around -2.1% y/y in March based on INEGI’s nowcast of monthly economic activity (the IOAE), with the services sector dragging down stronger performance in secondary activities. INEGI’s nowcast already covers April, when annual comparisons will be heavily distorted by pandemic-related base effects. If we take 2019 as a reference point to gauge where activity stands compared to pre-pandemic times, the nowcast implies that by April, activity will be around 3% below the same month of 2019.

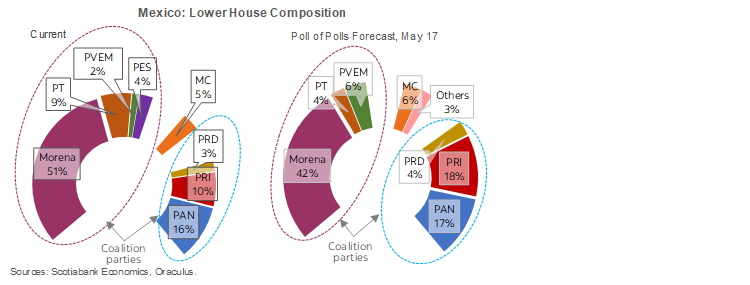

On the political front, we’re now two weeks away from mid-term elections where among many other public officials, Mexicans will elect all the members of the Lower House of Congress and 15 Governors. The most recent poll-of-polls elaborated by Oraculus.mx implies that the likelihood of the government’s coalition securing a qualified majority in the Lower House of Congress (i.e., the two-thirds majority needed to amend the constitution) is decreasing (chart). As we have highlighted in the past, control of the Lower House will be critical for some of the Lopez Obrador Administration’s pending legislative agenda, including: fiscal reform, pension reform, oil and power sector reforms (which may require constitutional amendments), and changes to the electoral system that President Lopez Obrador has discussed.

Peru—Election Uncertainty Continues to Overshadow an Improving Economy

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head of Economic Research

51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

COVID-19 vaccinations are accelerating, albeit less than 6% of the population has been inoculated. At the same time, both infections and hospitalizations are clearly declining. The combination is triggering a dawning sensation that maybe the worst is behind us and soon things will be back to normal in the country. But, then, just as you start to settle into a sense of relief, you remember: the elections!

Polls are pointing to a very contested finale, for June 6. The gap has narrowed between Pedro Castillo and Keiko Fujimori to between no more than five and, in some polls, as little as two percentage points of voting intention shares. A two-point gap is within the statistical margin of error. However, lest one become tempted to argue that the race is now a draw, note that all polls are aligned in showing Castillo in the lead. What one can say, however, is that the elections are now in a territory in which the results could conceivably be determined by the relative bias of absentee voters. If more voters leaning towards Castillo decide not to trouble themselves to vote, this would favour Fujimori. Of course, the reverse is also true. Meanwhile, both candidates have introduced new members to their respective government planning teams. Castillo apparently has had trouble recruiting people of note and prominence in their fields, and the names released do not really help in dispelling uncertainty around his candidacy. The new members of Fujimori’s team are better known, but it isn’t clear how much they may contribute to attracting undecided voters.

Leaving the elections and health issues aside, the economy continues to outperform. GDP growth in March was 18.2% y/y (first chart), versus our expectation of 16% y/y. Of course, this was off a low base as Peru’s lockdown began in mid-March 2020. To put this in perspective, GDP in March 2021 was 1.6% lower than in March 2019. This is not bad, considering that March was a month in which mobility restrictions were again in place and COVID-19 was nearing the zenith of its recent wave. Note that a number of sectors are trending above pre-COVID-19 levels, including fishing, manufacturing, electricity, construction, telecoms, government, and the financial system. The sectors that are lagging 2019 levels include agriculture, mining, commerce, transportation, and hospitality.

March GDP was more than enough to reverse the declines in January–February, and GDP for the Q1-2021 ended up 3.8% y/y. The most outstanding performer for the period was construction GDP, up 41.9% y/y in Q1-2021. Early indicators for April are even stronger. Electricity demand was up nearly 40% y/y (second chart), and domestic sales tax revenue increased 70.8% y/y (third chart). To put this in perspective, electricity demand is actually more or less on par with 2019 levels. Overall, the economy seems to be reasonably close to 2019 GDP levels, but not really better.

Another positive sign of improving macro accounts is the rather sharp decline in the fiscal deficit to -7.2% of GDP in April, down from 8-.9% of GDP at the end of 2020. This is broadly in line with our expectations that the fiscal deficit will continue falling towards our forecast of -5.4% of GDP at the end of 2021. The huge 92% y/y increase in tax revenue in April had two sides to it. One is that it compares with a low base due to COVID-19-related tax deferrals in 2020. At the same time, however, high metal prices surely fed the 111% y/y rise in income tax payments by businesses during April, which was the height of the tax season. Sales tax revenue also continued strong, up nearly 75% y/y, in line with our view that digitalization is leading to a greater formalization of previously informal sales.

Unlike macro balances, socio-economic indicators have deteriorated noticeably. The National Statistics Institute released figures showing that poverty soared from 20.2% in 2019, to 30.1% in 2020, as a result of the impact of COVID-19 and the mandatory lockdown. Meanwhile, unemployment remains stuck at high levels, registering 15.1% in the three-month period ending in April. This was an only marginal improvement from 15.3% in the rolling quarter to March. It is somewhat disappointing that employment continues to lag so significantly behind the rest of the economy during the recovery.

The BCRP surprised no one when it left its reference rate stable at 0.25% this month. Headline inflation in April came in at 2.4% y/y and core inflation at 1.7% y/y, both comfortably within the BCRP target range. Inflationary pressures are still mild in Peru, but the risk is to the upside. The BCRP has been more focused on the FX rate, which has whiplashed up and down, in sync with the changing polling numbers on the presidential race; the steady improvement in Peru’s terms of trade over the last year (fourth chart) hasn’t been sufficient to insulate the sol from political uncertainty. After reaching a record USDPEN 3.90 when Castillo showed a commanding lead in the first half of May, the exchange rate then plunged to 3.66 as the gap narrowed, and is currently sauntering around the 3.70–3.75 range. The future of the PEN hinges rather dramatically on the June 6 run-off presidential election results.

Peru has a lot going for it, but little of that matters until the political outlook is clearer. Metal prices are at multi-year highs, macro accounts are improving, and the economy is rebounding nicely, with COVID-19 starting to abate. And yet, the future will remain uncertain until it becomes clear what type of profile the next government will have.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.