- The government’s latest Medium-Term Fiscal Framework balances poverty reduction and economic recovery with the need for fiscal sustainability.

- The plan rests on assumptions that may prove optimistic and fiscal reforms that have yet to be fully articulated.

Minister of Finance José Manuel Restrepo released Colombia’s Medium-Term Fiscal Framework 2021 (MTFF) on Tuesday, June 15 that balances near-term fiscal support for the economy with medium-term fiscal sustainability. The MTFF has become the government’s key fiscal policy document, providing insights on the country’s economic and fiscal results and perspective on factors influencing the main fiscal goals and fiscal sustainability over the next ten years.

The MTFF highlights bigger deficits and continuing support for the economy but reaffirms the government’s commitment to fiscal sustainability. The deficit increased to 7.8% of GDP in 2020 from 2.5% of GDP in 2019 as tax collections fell (accounting for 0.9% of GDP of increase in the deficit), indirect effects from the COVID-19 shock (2.6% of GDP), and extra-spending programs to address the COVID-19 emergency (1.8% of GDP). The higher deficit lead to a sharp increase in Gross Central Government debt as a share of GDP from 50.3% to 64.7%.

Minister Restrepo underscored the importance of measures to provide social support and outlined three interrelated objectives for the MTFF—poverty reduction, economic recovery, and fiscal sustainability. The MTFF defines these objectives as:

1. An expansive fiscal policy in the short term to maintain social programs and to reduce poverty to pre-pandemic levels;

2. A strong medium-term fiscal anchor (fiscal rule), to gradually return to fiscal sustainability; and

3. A strategy to increase fiscal income, which is a direct reference to the Fiscal Reform to be presented in July 2021.

MACRO FUNDAMENTALS AND FISCAL TARGETS

- GDP is projected to grow by 6.0% y/y in 2021 factoring in the negative effects of the nationwide strike in Q2-2021, supported by international trade and investment. For 2022, economic growth of 4.3% y/y is expected. Over a 10-year horizon, economic growth averages 3.7% y/y, with above-potential GDP growth GDP until 2026 (chart 1).

- The MTFF envisions further fiscal deterioration this year, followed by gradual but steady improvement. The 2021 fiscal deficit target is -8.6% of GDP, consistent with the Financial Law passed in the beginning of the year. Meeting the target will require budgetary reallocations to finance key social programs. A deficit of 7.0% of GDP is expected in 2022, which assumes a reduction in social expenditures of 0.4% of GDP, an increase of 0.2% of GDP in fiscal revenues, greater tax collection efficiency (contributing 0.4% of GDP), government expenditure reductions (1.3% of GDP) and higher oil sector-related revenues (0.7% of GDP).

- The government expects to run primary surpluses after 2023 (chart 2), fueled by additional fiscal reforms. Minister Restrepo said that fiscal reforms already announced are expected to raise the equivalent of two-thirds of what is needed to achieve fiscal sustainability, implying that a new reform package would be needed before 2024.

- The trajectory for the fiscal deficit in 2022 and following years is mapped out under a new definition of the fiscal rule. The Minister of Finance emphasized that a new structure for the fiscal rule will be fully articulated in the Fiscal Reform bill but that a key change would include the use of the total debt as an anchor. The gross debt-to-GDP ratio is expected increase to 66.8% of GDP in 2021 and up to 69.1% of GDP in 2023 (chart 3). Starting in 2024, a convergence to lower levels through primary surpluses is expected.

- Other assumptions. Minister Restrepo said that Brent prices are expected to average USD 63 per barrel in 2021 and 2022, while the exchange rate is expected to average 3,667 for 2021 and 3,744 in 2022. We consider these optimistic assumptions. It is worth noting that for 2022 oil revenues would be significant source of revenues (0.7% of GDP) amid current favourable price conditions.

FUNDING FOR 2021

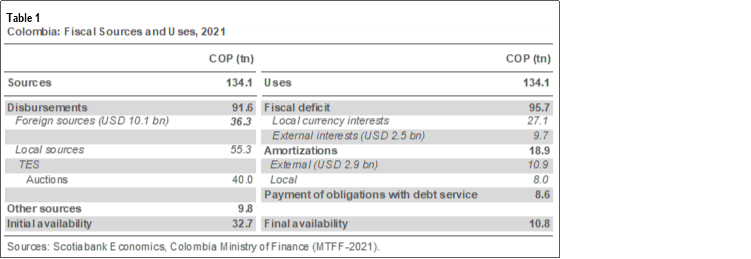

In 2021, uses and sources of funds remained broadly unchanged from the Financing Law presentation (table 1). This is a credit positive in our opinion. 2022 financing needs will remain elevated, suggesting that auctions of local debt will continue at a similar amount to those observed in 2021. Assets sales, primarily ISA (state-owned electrical company) transactions, remain in the fiscal plan for 2021 and 2022.

- External sources of funds are projected to provide USD 10.1 bn. Treasury Head, Cesar Arias, said that financing is expected 50%/50% between multilateral credits and bond issuances. Up to May, around USD 4.6 bn has already been done through external debt issuance. External debt would continue to be an important source of funding for the current account deficit, which is expected to hit 4.0% of GDP in 2021.

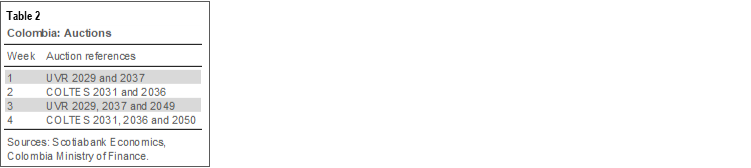

- Local debt markets are expected to finance COP 55.5 tn. TES (Treasury bond) issuances would remain at COP 40 tn. However, auctions will change (table 2):

- Colombia will launch a new 10-year benchmark (COLTES 2031) auctioned on June 23 and July 24, with each auction offering COP 700 bn.

- Additionally, starting on July 28, the longest tenor (COLTES 2050 and COLTES UVR 2049) will be auctioned only once a month in accordance with previous strategies to reduce supply pressures at the long end of the curve.

FUNDING FOR 2022

- By 2022, the fiscal deficit is expected to be 7% of GDP, resulting in continuing large borrowing demands (table 3).

- External sources will remain a key source of funds (USD 10.5 bn), again under a 50/50 split between multilateral and external debt. Monetization would remain high since amortizations, and interest payments of external debt are relatively low (approximately USD 4.0 bn).

- Local sources of funds are expected to provide COP 62.8 bn, an increase of 13% versus 2021. However, auctions would remain around COP 40 tn. Other sources of local funding would come from other instruments such as pension bonds, green bonds and ETFs.

- In 2022 the COLTES May 2022 matures with about COP 22 tn outstanding; however, the Treasury would be encouraged to continue making debt swaps.

OUR TAKE

The MTFF stakes out a commitment to medium-term fiscal sustainability, but one based on favourable assumptions. The MTFF is based on a conservative assumption regarding economic recovery in 2021, with GDP growth of 6% y/y. The macro assumptions in the following years, in contrast, will be more challenging to achieve. In this respect, the debt-to-GDP ratio is not expected to trend down until 2024, even with the assumption of additional fiscal reform to the current potential bill to be discussed in the H2-2021. Moreover, fiscal consolidation will prove challenging since social programs to reduce poverty to pre-pandemic levels will remain in place. Additional revenue would come from traditional sources (high-income individuals and corporate taxes) and efficiency in tax expenditure (also a strong assumption). In other words, the government is betting on significantly higher economic activity growth to ensure fiscal sustainability. On the financing side, for the moment, the Treasury is not anticipating further supply pressures; instead, it is reducing auctions in the longest tenors, given the steepening of the curve. In the meantime, funding needs will remain high, with a large share coming from external debt.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.