- Banxico’s Governing Board cut the benchmark interest rate by 25 basis points to 7.50%, in line with the market consensus, in a split vote.

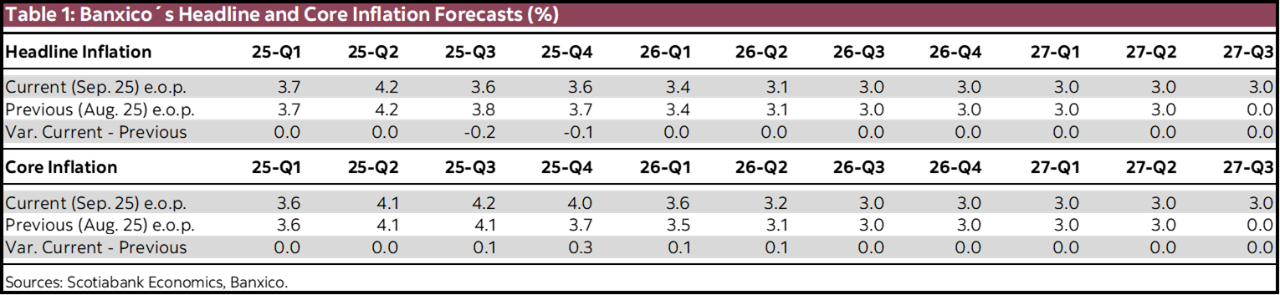

- Headline inflation forecasts were revised downward, while core inflation projections were adjusted upward in the short term again, owing to rising prices in goods and services. Inflation is expected to converge to the 3.0% target by Q3 2026.

- Monetary conditions are now very close to the upper bound of the neutral interest rate, despite persistent inflationary pressures, mainly from the core component.

- We maintain our year-end target rate forecast at 7.00%, subject to the inflation trajectory and the interest rate differential between Mexico and the United States.

The Governing Board of Banco de México decided to cut the benchmark interest rate by 25 basis points to 7.50%, in line with consensus expectations. This marks the third consecutive meeting with a split vote, with Deputy Governor Jonathan Heath once again dissenting. This brings the total to ten consecutive rate cuts: four cuts of 25 bps last year, four cuts of 50 bps earlier in 2025, and two cuts of 25 bps since.

Notably, the Board revised upward its core inflation expectations from Q3 2025 to Q2 2026, while headline inflation estimates for Q3 and Q4 2025 were revised downward. The Board maintained its expectation that inflation will converge to the 3.0% target by Q3 2026 (table 1).

The communiqué reiterated that global economic activity likely slowed during Q3 2025 compared to the previous quarter. It also anticipates continued moderation in both the global and U.S. economies through the remainder of 2025 and into 2026. The Federal Reserve reduced its benchmark rate by 25 basis points and signaled further cuts, leading to lower interest rates—especially at shorter maturities—and a moderate depreciation of the dollar. Inflation in major advanced economies showed mixed behaviour. Key global risks include rising trade tensions and geopolitical conflicts, which could impact inflation, growth, and financial volatility.

Domestically, the Board noted that economic activity showed weakness at the beginning of Q3 2025 amid uncertainty and trade tensions, which pose significant downside risks. It also highlighted that Mexican government bond yields declined, particularly at longer maturities, while the peso appreciated.

Regarding inflation, the Board reported that between July and the first half of September, headline inflation in Mexico rose from 3.51% to 3.74%, while core inflation remained stagnant between 4.23% and 4.26%. Headline inflation expectations were revised downward for year-end, with convergence to the target expected in Q3 2026. However, core inflation forecasts were revised upward. Upside risks include peso depreciation, geopolitical conflicts, persistent core inflation, cost pressures, and climate-related events. Downside risks include weaker economic activity, lower cost pass-through, and peso appreciation. The balance of risks remains tilted to the upside, albeit less than in previous years. Uncertainty surrounding changes in U.S. economic policy could affect inflation in both directions.

We consider that the monetary policy decision reflects a less restrictive stance compared to previous meetings, as evidenced by the new rate cut. However, monetary conditions remain close to the upper bound of the neutral rate, despite ongoing inflationary pressures, particularly from the core component. The statement highlights the dissenting vote of Deputy Governor Jonathan Heath, who favoured maintaining the rate at 7.75% for the third consecutive meeting. The possibility of further rate cuts remains open, as noted in the statement: “Going forward, the Governing Board will assess additional reductions to the reference rate.”

In this context, it will be crucial to monitor not only upside inflation risks and the impact of domestic economic weakness on price dynamics, but also labour market developments and inflation trends in the U.S. These factors could significantly influence the Federal Reserve’s next rate decision, potentially creating more room for Banxico to continue its easing cycle. We expect Banxico to proceed with another rate cut in the November decision, in line with the Fed’s moves. However, the decision is likely to be split again, given ongoing differences among Board members regarding inflation risks and the monetary stance, both in absolute and relative terms.

We maintain our forecast for a 7.00% interest rate at year-end 2025, assuming the rate differential between Mexico and the U.S. does not fall below 325 basis points. To better understand each Board member’s position, it will be especially important to review the minutes of this decision, scheduled for release on October 9th, 2025.

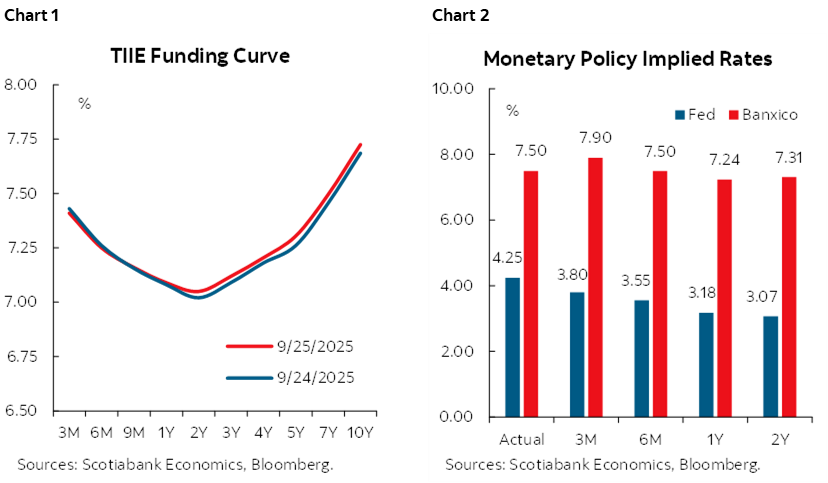

Regarding market reaction, the exchange rate experienced slight depreciation during the day, fluctuating between $18.40 and $18.56, with a modest appreciation to $18.52 following the monetary policy decision. Meanwhile, the TIIE funding curve moved lower, with an average decline of 2 basis points compared to the previous day (chart 1). The three-month implied curve stood at 7.41%, while the one-year curve settled at 7.08% (chart 2). Analysts participating in expectations surveys forecast the benchmark rate to end 2025 at 7.00%, with responses ranging from 7.00% to 7.50%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.