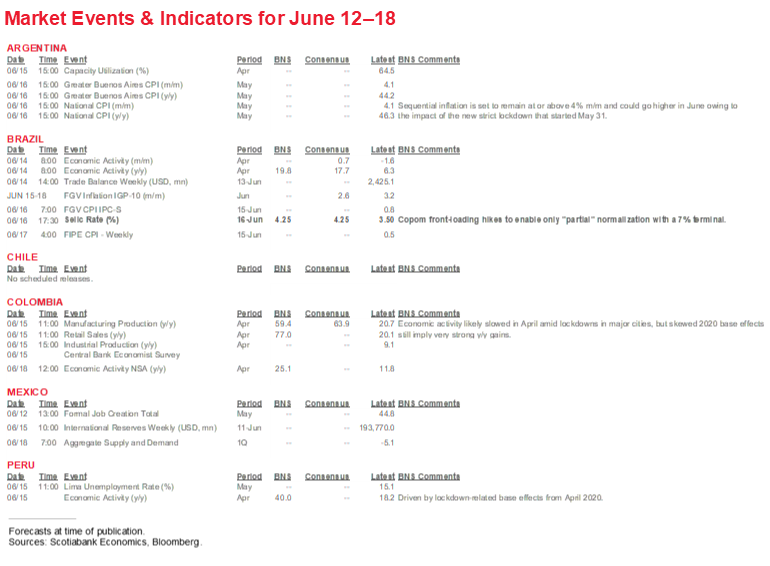

- Indicators point to economic recovery in the Latam region, but sustained growth depends on the progress made in containing the pandemic.

- The pandemic also creates uncertainty in the interpretation of monthly indicators of growth and inflation, as base effects create large year-over-year swings.

- Meanwhile, political developments have generated uncertainties that financial markets have priced-in.

KEY ECONOMICS CHARTS

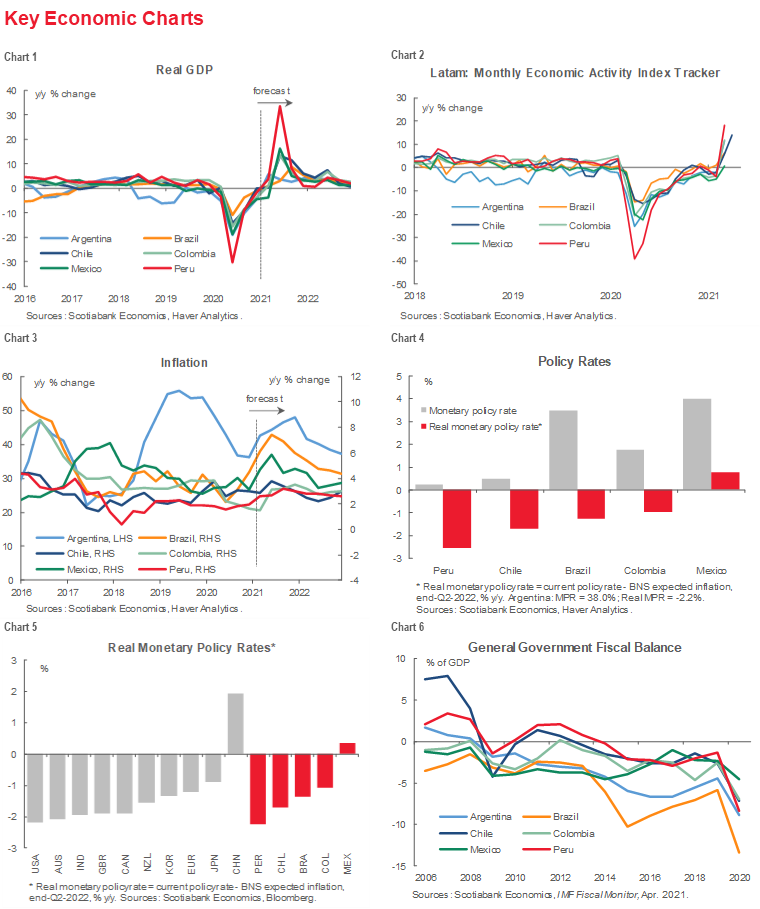

- Monitoring of key economic variables continues to be clouded by the effects of the pandemic.

- In this respect, while projections for real GDP (chart 1) are broadly consistent with the Monthly Economic Activity Index Tracker (chart 2), which is signalling economic recovery, large rebounds in year-over-year numbers include base effects and must be interpreted with caution. There are, however, undeniable signs of strength. Chile stands out. The central bank’s latest Monetary Policy Report released on June 9 raised the range of expected GDP growth to 8.5%–9.5% y/y (see yesterday’s Latam daily). Containing COVID-19 is a key factor behind restoring growth, and the projection of strong growth reflects Chile’s remarkably successful vaccine campaign (see discussion below). Yet, uncertainties remain, as illustrated by the decision of Chilean health authorities to re-impose a lockdown in Santiago.

- Inflation numbers are also subject to base effects. And while inflation measured on a year-over-year basis is projected to increase across the region, inflation is expected to moderate over the course of 2021 and 2022 as base effects coinciding with the early months of the pandemic tail off (chart 3).

- A key element of the outlook for inflation is the extent to which inflation expectations have remained anchored by central banks’ inflation targets. Real policy rates, defined as the current policy rate minus Scotiabank’s expected inflation, rate one year ahead, remain negative in most countries to provide support for economic recovery (chart 4). This setting is broadly appropriate; going forward, central banks will have to remain vigilant to price pressures that could become embedded in inflation expectations.

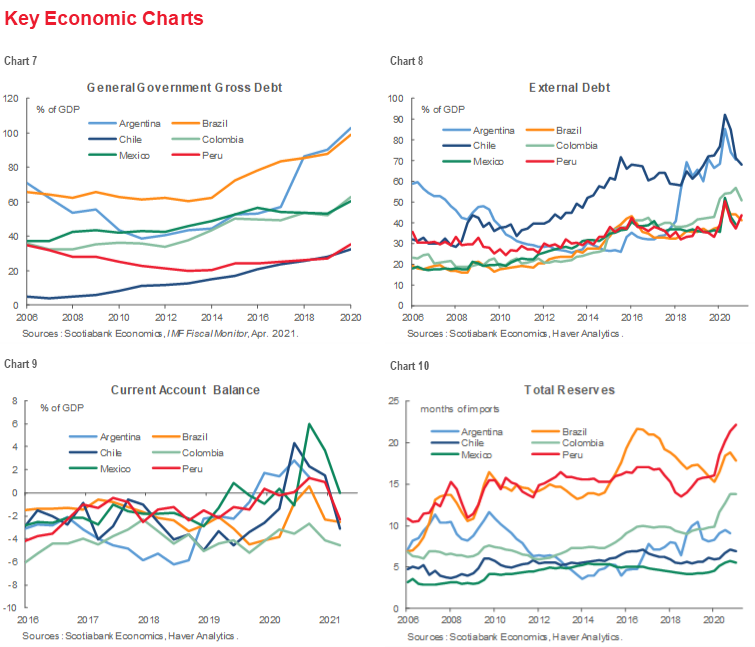

- Likewise, fiscal policy, which has provided support to individuals and the economy through large fiscal deficits (chart 6), will have to be calibrated to ensure long-term sustainability. In most countries of the region, General Government Debt as a share of GDP (chart 7) and External Debt as a share of GDP (chart 8) remain manageable despite higher deficits, though increases in Argentina’s debt loads are significant.

- Meanwhile, improved current account balances (chart 9) have contributed to total reserves (chart 10), and mitigate foreign exchange risks.

FINANCIAL MARKET CHARTS

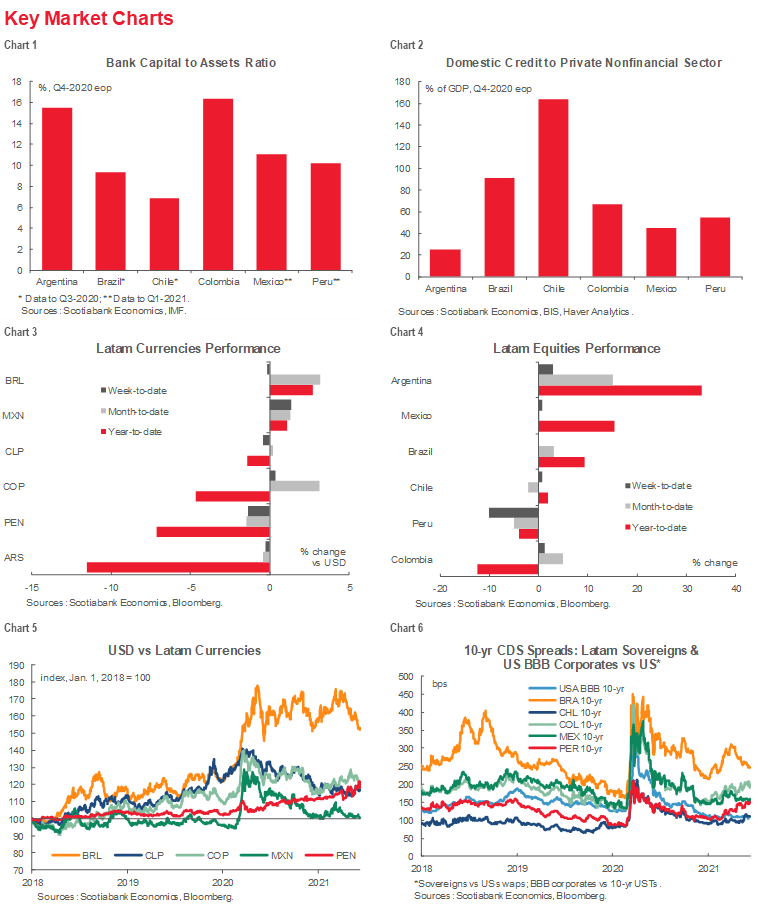

- Financial markets have reflected recent political development.

- In Peru, capital outflows prior to the June 6 run-off presidential election led to a sharp drop in the currency. The PEN recovered some ground after the vote, as officials of leftist candidate Castillo’s party signalled that his administration would pursue a moderate approach to economic policy, including respecting central bank independence. On balance, however, the PEN was down on the week (chart 3). The stock market responded negatively to the prospect of a left-of-centre government that promises to raise corporate taxes (chart 4). Political uncertainty from a disputed election is likely to weigh on financial markets in the weeks ahead, possibly leading to continued widening of credit default spread (CDS) spreads, which began to widen in late-2020 (chart 6).

- Large, sustained political protests in Colombia may likewise account for the rise in the 10-year CDS spread (chart 6).

- In Mexico, in contrast, equity markets responded positively to its June 6 mid-term election results, which reduced the ruling party’s super-majority in Congress’ Lower House to a simple majority and, going forward, will limit President AMLO’s capacity to initiate far-reaching reforms contingent on constitutional changes. Investors may view the resulting constraint on policy making as limiting one source of possible policy uncertainty.

YIELD CURVES CHARTS

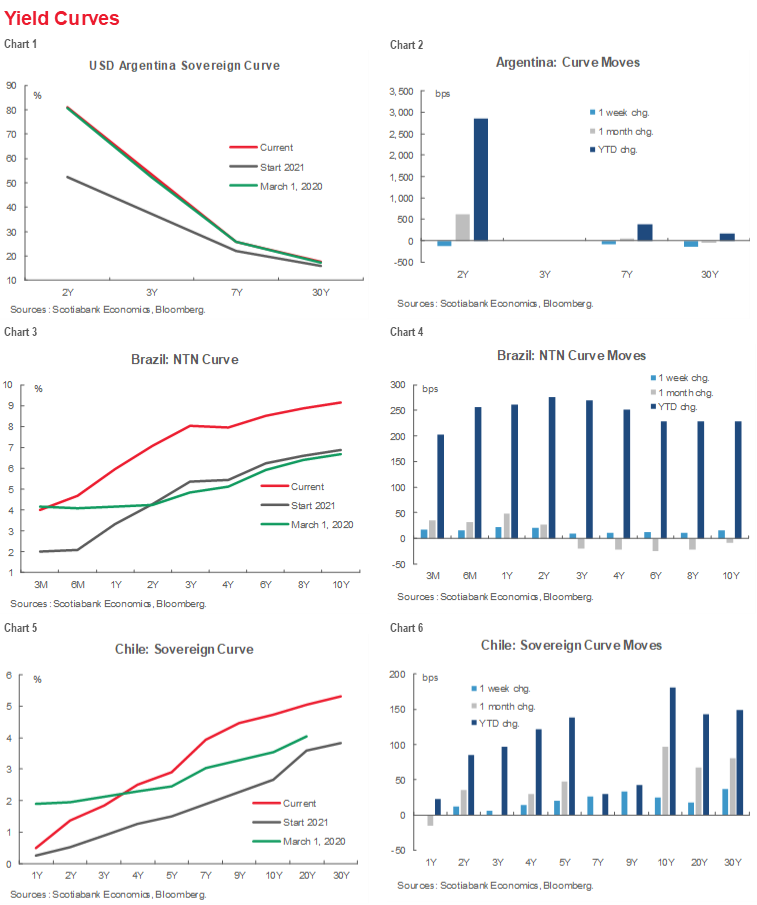

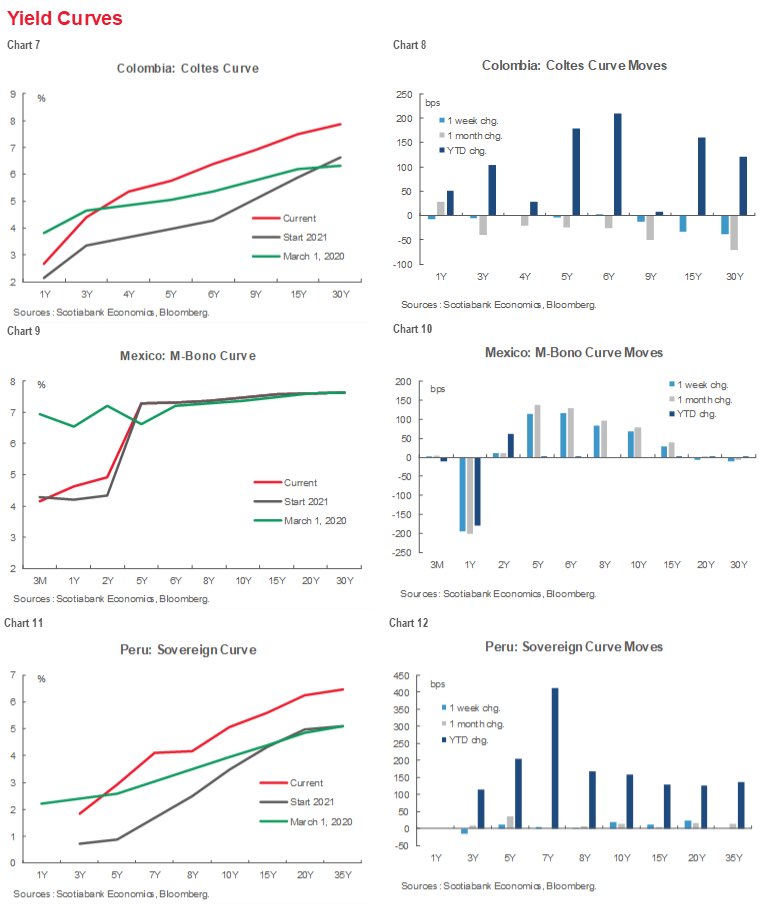

- For the most part, yield curves across the region have been remarkably stable over the past month.

- The Argentina Sovereign Curve remains deeply inverted following a sharp rise of over 3,000 basis points at the short end of the curve earlier in the year (charts 1 and 2).

- Elsewhere in the region, sovereign curves that shifted up in line with global rates in early-2021 remain largely unchanged from a month ago, though the sovereign curves of Brazil (chart 3) and Chile (chart 5) moved slightly higher.

- Mexico is the exception, with the short-end of the curve (one-year M-Bono rates) returning to levels seen at the start of year and medium-term rates moving higher (charts 9 and 10). With these changes across the maturity spectrum, the Mexican sovereign curve is now back to where it was at the start of year.

KEY COVID-19 CHARTS

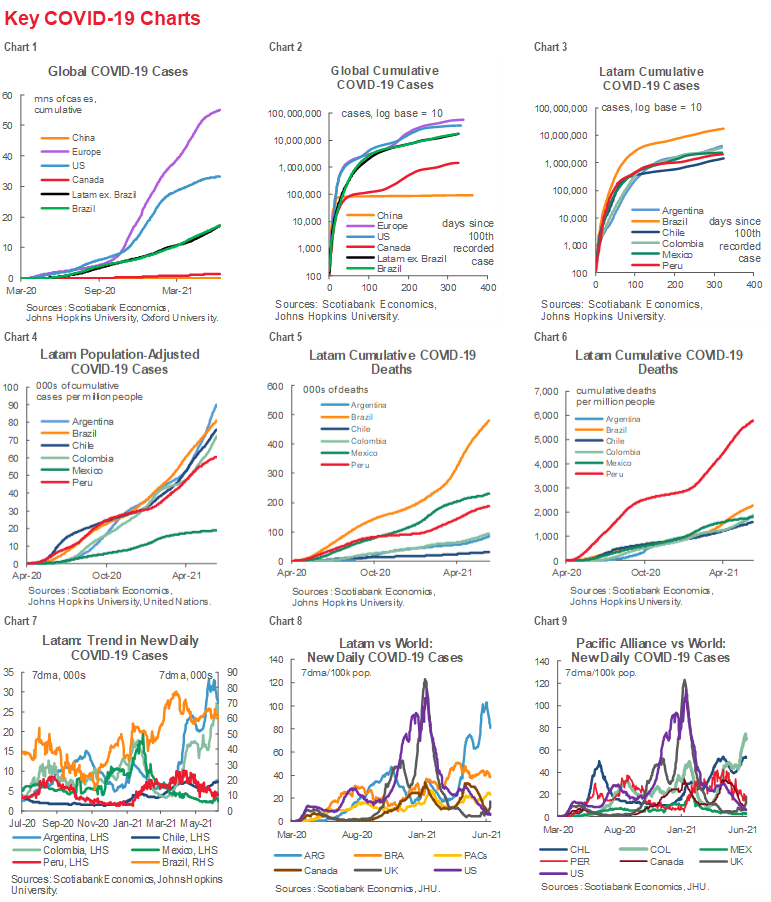

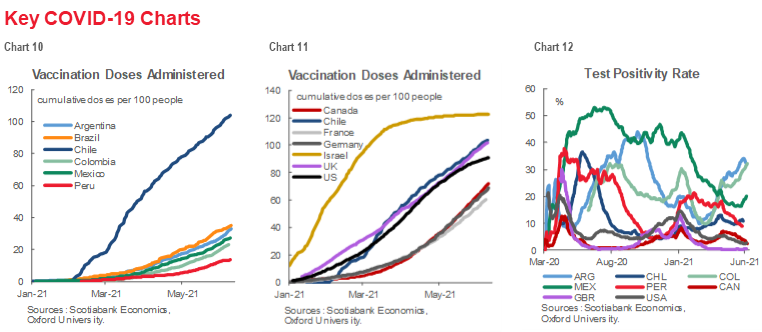

- As noted above, the critical takeaway from our COVID-19 monitoring charts remains Chile’s success in administering vaccine doses. It not only leads the region in terms of does administered per 100 people (chart 10) but is also outperforming most other countries (chart 11). This outstanding performance creates the basis for sustained economic recovery and underscores the importance for other countries in the region to accelerate vaccine rollouts.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.