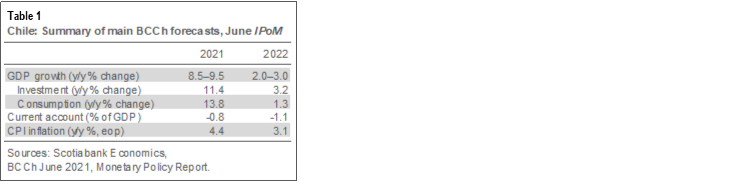

- Chile: Quarterly Monetary Policy Report, GDP forecast up (to 8.5%–9.5% y/y) and policy rate holds at 0.5%

- Mexico: AMLO shuffles finance minister; May y/y inflation down, but still well above Banxico target

- Peru: Elections—it’s not over until it’s over

CHILE: QUARTERLY MONETARY POLICY REPORT, GDP FORECAST UP (TO 8.5%–9.5% Y/Y) AND POLICY RATE HOLDS AT 0.5%

On Wednesday June 9, the central bank (BCCh) released its Quarterly Monetary Policy Report (IPoM), whose main takeaway is the economy’s remarkable performance so far this year. This outcome is notable as quarantines effected a softer-than-anticipated impact despite a decline in activity in March and April.

In view of this solid performance, a much greater fiscal impulse, and favourable external conditions, the BCCh has raised its range of forecasted GDP growth to 8.5%–9.5% y/y from a 6.0–7.0% y/y in March (table 1). This follows April’s upward revision from an earlier 5.5–6.5% y/y projection. The new forecast goes beyond our expected range of 7%–8% y/y, per our June 4 Latam Weekly.

The neutral monetary policy interest rate (neutral MPR, or the tasa de politica monetaria neutral in Spanish, TPMN) represents the long-term equilibrium level of the MPR in the absence of transitory shocks. To the extent that it anchors the long-term value to which the MPR should converge in the absence of future shocks, when the economy has normalized, the difference between the neutral MPR and the existing MPR is a key input in the calibration of the expansiveness of monetary policy. The update of the estimate of the neutral MPR shows that its level is around 0.5% in real terms. Adding the inflation target and considering the uncertainty regarding the estimates, the Board considers that the nominal neutral MPR is in a range between 3.25% and 3.75%, with a midpoint at 3.5%. This is 50 basis points lower than in the last update provided by the BCCh in June 2019.

The Board also updated its estimate of the trend growth of non-mining GDP (potential GDP) for the period 2021–30 to between 2.4% y/y and 3.4% y/y, with a midpoint at 2.9% y/y. This represents a decrease of 0.6 percentage points with respect to the range estimated in 2019 (3.25%–3.75%).

The economy’s solid performance is attributed to various factors, notably the boost from much greater fiscal spending, recently approved income support programmes for small businesses and households, and pension withdrawals. It is worth noting that the combination of various expanded fiscal supports has significantly pushed up fiscal spending, bringing it close to a nominal 25% y/y, compared to the 5% y/y considered in the March IPoM.

The report also highlighted greater dynamism in consumption and private spending. And, while the labour market continues to improve, it is happening unevenly. More than half of the jobs lost following the onset of the pandemic have now recovered, but segments lag behind such as the self-employed, informal salaried workers, low-skilled workers and women.

With respect to monetary policy, the BCCh considers that economic recovery is still being impacted by the pandemic and the lag in the labour market. However, the economic dynamism poses important changes for the macroeconomic scenario over the next few months. As we noted in yesterday’s Latam Daily, the BCCh is holding onto a 0.5% policy rate, but has strongly signaled a hike later this year. Our view is that inflation will temper over the short term, leading the central bank to hike at the October 13 meeting.

—Jorge Selaive

MEXICO: AMLO SHUFFLES FINANCE MINISTER; MAY Y/Y INFLATION DOWN, BUT STILL WELL ABOVE BANXICO TARGET

I. Mexico’s AMLO shuffles finance minister, nominating Mr. Herrera as new central bank governor

President López Obrador shuffled his finance minister of the last two years, Arturo Herrera, announcing Rogelio Ramírez de la O as his new minister. The shuffle was motivated in order to nominate Mr. Herrera, a close ally of the president, as new governor of the central bank, Banxico. Incumbent Alejandro Díaz de León will conclude his term on December 31.

The nomination was widely expected, as the president had previously said he would not propose a second term for Gov. Díaz de León. Market reaction to the changes was muted.

Mr. Ramírez de la O has been close to the president since his 2006 presidential campaign. In the current administration, he has served as one of the president’s main economic advisors and had previously been considered a possible successor to Carlos Urzúa, AMLO’s first finance minister. Ramirez de la O holds a Cambridge PhD in economics and a BSc in economics from Mexico’s UNAM. His nomination will be sent to the Senate for ratification towards the end of the year.

—Eduardo Suárez & Miguel Saldaña

II. Inflation slows in May, but stays well above central bank target

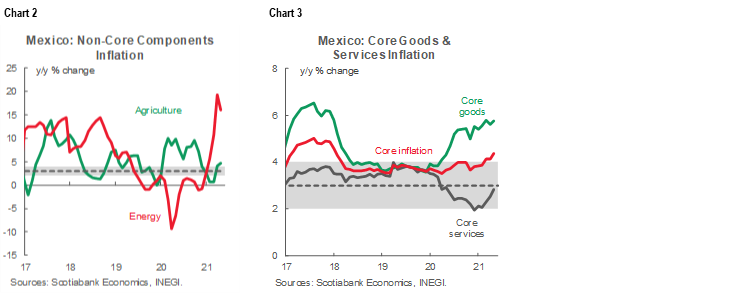

According to data released by Statistical Agency, INEGI, on June 9, CPI declined in May to 5.89% y/y, from 6.08% y/y the previous month (chart 1), slightly above the Bloomberg consensus (5.86% y/y) and materially above the high end of Banxico’s target range. This was the third consecutive month surpassing the 4.00% y/y upper limit of Banxico’s target band. We maintain our view that the central bank will keep its key target rate on hold at 4.00% y/y through the remainder of 2021.

The moderating inflation components were non-core items that softened their sub-index inflation from 12.34% y/y to 10.76% y/y (chart 1 again). Pressures in energy prices slowed from 19.30% y/y to 15.97% y/y, which was partly offset by agricultural prices where inflation rose from 4.08% y/y to 4.67% y/y (chart 2). Core inflation maintained an upwards trend as it moved from 4.13% y/y to 4.37% y/y (chart 1 again), with pressure from both goods prices (5.76% y/y from a previous 5.59% y/y) and services (up from 2.53% y/y to 2.84% y/y) (chart 3).

On a monthly basis, headline inflation moderated from 0.33% m/m to 0.20% m/m, above the 0.16% m/m consensus in the Citi Survey. Non-core inflation was in fact negative, coming in at -0.75% m/m (0.21% m/m previous), owing to lower electricity prices at the beginning of the seasonal energy tariff subsidy programme. The core component rose from 0.37% m/m to 0.53% m/m, above the 0.46% m/m consensus. Pressure again came from surges in goods prices (0.62% m/m), and in services prices (0.42% m/m). All told, inflation materially above Banxico’s target range should keep the Board cautious, but the sequential inflation trend gives it some maneuvering room for now.

In its June Quarterly Report, Banxico revised up inflation estimates for 2021, but still sees it converging to 3.00% in Q2-2022, suggesting that the Board considers the recent spike in inflation as a transitory event mainly driven by base effects. The Board also considered the balance of risk for inflation skewed at the upside.

—Miguel Saldaña

PERU: ELECTIONS—IT’S NOT OVER UNTIL IT’S OVER

Vote count has virtually been completed. With 99.998% voting booths processed, Pedro Castillo has a narrow but clear lead of about 70,000 votes. Despite this, the election is not yet over, as processed votes do not yet include the approximately 280,000 votes submitted for validation to the elections authority, JNE.

Keiko Fujimori’s party, Fuerza Popular, believes that a large portion of these votes, if validated, would go to Fujimori, using the argument of excessive challenges by the opposite party’s booth representatives. If that were the case, these votes by the JNE could conceivably alter the final results. Compared to the previous election,1,395 both results are currently under review by the JNE, against just over 1,200 in 2016. These had no impact on the final outcome.

Fujimori’s FP is further requesting the annulment of another 200,000–230,000 votes from more than 800 booths, citing evidence of unusual behaviour or results. As an example, the FP cites booths that reported having no votes, in stark contrast to neighbouring areas. It is unclear whether the JNE will accept these claims, and such annulments are allowed by law, but it is yet to be seen how the law will be interpreted on votes already counted. There is no precedent for JNE rulings on challenged votes overturning elections results in the past. The current environment could leave lasting challenges in the country beyond the election if half of the country questions its legitimacy.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.