- Peru: New Central bank projections for 2022: cautious forecasting with some unknowns ahead

PERU: NEW CENTRAL BANK PROJECTIONS FOR 2022: CAUTIOUS FORECASTING WITH SOME UNKNOWNS AHEAD

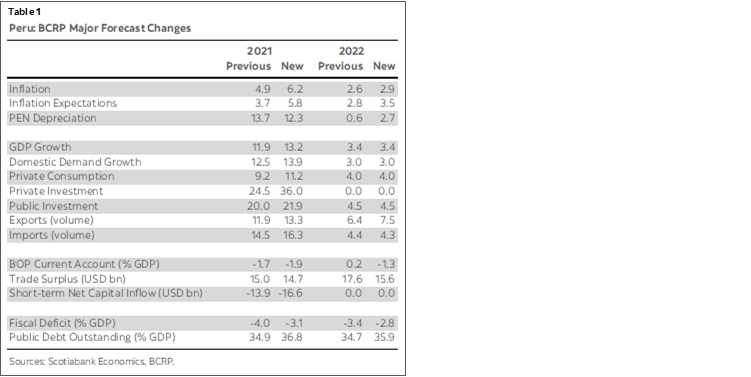

The BCRP released its quarterly Inflation Report on Friday, December 17. The BCRP updates its forecasts on a quarterly basis in this publication and provides its view on the economic and monetary outlook going forward (see table 1 for all updated forecasts).

One of the key modifications in Friday’s report was a substantial increase in the BCRP inflation forecast for 2021, from 4.9% to 6.2%. More importantly, the BCRP raised its forecast for 2022 only very mildly, from 2.6% to 2.9%. One gets the impression that the BCRP is not quite ready to signal that inflation could remain outside of its 3% target range ceiling next year. We, on the other hand, expect yearly inflation to end 2022 at 4.5%.

BCRP guidance states that monetary policy would continue to be expansionary for a prolonged period of time, during which there will be a gradual withdrawal of monetary stimulus. What this means, in our view, is that the BCRP will continue raising the reference rate, but not so aggressively as to surpass inflation expectations. In other words, it would seek to maintain a negative real reference rate throughout the foreseeable future, with the rate becoming less and less negative over time. The key here is inflation expectations, which the BCRP has just raised for 2022 from 2.8% to 3.5%. The assumption behind our forecast that the BCRP will raise the reference rate in 2022 to 4.0% is that inflation will surpass 7% early in the year, and that inflation expectations will be higher than the 3.5% that the BCRP is foreseeing.

Overall, and aside from inflation, growth forecasts for 2022 appear to reflect a sense of uncertainty that many market analysts entertain. The fact that the BCRP has not modified its GDP or domestic demand forecasts in this report may well reflect a stance that future growth is just too much of an open question to be making changes, at least until initial figures start to appear. Note, for the record, that the BCRP forecast of 3.4% GDP growth in 2022 compares with our expectation of 2.6%. The general story is the same as ours, growth that is relatively mediocre if you consider today’s metal prices. Where we are in closer agreement is in low private investment, nil growth according to the BCRP and marginal 1% growth for us. The BCRP is one percentage point greater in its consumption forecast: 4.0%, to our 3.0%.

Also of note is that, whereas the BCRP expects domestic demand growth to surpass aggregate GDP growth in 2021, in 2022 the BCRP expects domestic demand, with 3.0% growth, to underperform GDP growth (3.4%). Thus, net exports will have a greater weight in growth. This is in part due to 2022 being the first full year of operation of the new Minas Justa mine. The risk, of course, is that social conflicts affect mining output significantly. Social conflicts have already shut down the Las Bambas mine indefinitely. The recent closure, the duration of which is hard to pre-determine, may not be sufficiently reflected in the BCRP forecasts.

The other issue where uncertainty appears evident is in the BCRP forecast of nil net short-term capital outflow. This seems optimistic, after an all-time high of over USD16 bn in 2021. Assuming nil net anything can sometimes be an easy way out when you’re unsure of what to expect.

Where the BCRP concern over political stability does filter through is in the change in forecast for the PEN depreciation in 2022 from 0.6% previously, to 2.7% currently. In other words, despite strong and improving macro accounts, the BCRP expects the PEN to continue to be under pressure, albeit of a milder magnitude compared to 2021.

The BCRP is much more sure-footed regarding its fiscal forecasts, where they have made major changes. With Peru’s 12-month fiscal deficit to November at 3.3% of GDP, the BCRP is keeping on trend in forecasting 3.1% for full-year 2021 (down from 4.0%) and 2.8% of GDP for 2022 (down from 3.4%, previously). Although the changes are large, they are believable, given the current trend in fiscal accounts.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.