- Economic indicators continue to point to strong growth in the Latam region, reducing the uncertainty that had prevailed with respect to the resilience of the recovery. Strong growth will soon restore output to its pre-pandemic level—or has already done so.

- The big questions now concern the level and persistence of inflation, and what it will take in terms of central bank tightening to contain price pressures. Latam central banks have begun tightening, with additional policy rates hikes on the way.

- At the same time, continued growth remains hostage to possible adverse developments in the pandemic that could, for example, exacerbate existing supply chain disruptions or propagate new bottlenecks.

KEY ECONOMIC CHARTS

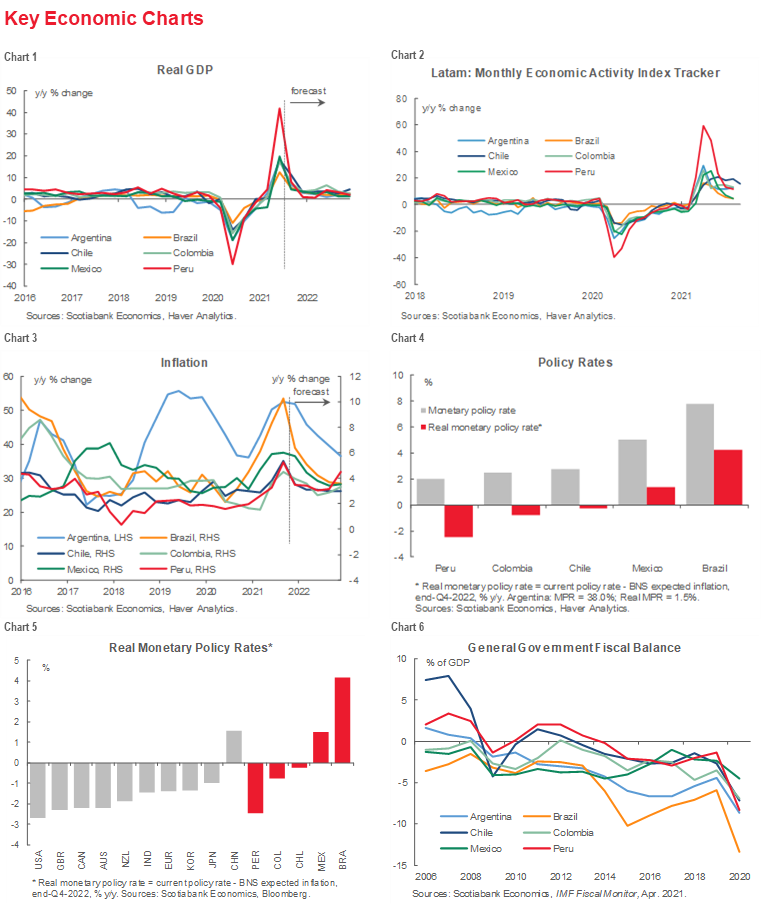

Only a few months ago, uncertainty regarding the resiliency and the pace of economic recovery hung over the Latam region. While Latam economies experienced a rebound from the pandemic-induced contractions in 2020 (chart 1), questions remained as to whether the recovery would be maintained. These doubts reflected several factors; not surprisingly, the most important unknowns related to the transmission and virulence of COVID-19.

Much of that uncertainty has dissipated. As additional data points on economic activity have come in (chart 2), projected growth rates have been raised, and there is growing confidence that output will soon return to pre-COVID-19 levels and, indeed, has likely already done so in Colombia, where September indicators provide a strong close to Q3.

Growth rates across the region are expected to moderate, however, as base effects, which reflect the contraction in output early in the pandemic, wane. Over 2022, growth is projected to broadly return to pre-pandemic levels. In this regard, raising long-run potential output growth remains an important policy challenge in terms of addressing long-standing development issues. And boosting potential output would also have a salutary effect on inflationary pressures.

The Latam region, like the rest of the global economy, has experienced a sharp rise in inflation as economies have recovered (chart 3). For the most part, recent data releases underscore this trend: October numbers for Chile and Mexico show inflation at 6% y/y, above the upper range of inflation targets, while in Peru the most recent survey of 12-month inflation expectations by the BCRP revealed expected inflation at 3.6%, above the upper limit of the central bank’s target range for the third consecutive month. In Colombia, in contrast, October CPI came in at 0.1% m/m, with a VAT holiday offsetting other price rises. While that temporary measure may provide short-term benefits by containing year-end indexation effects, our team in Bogota do not expect it to affect the central bank’s tightening plans.

Price pressures are expected to be transitory, with inflation rates projected to gradually decline in 2022 as temporary supply-side bottlenecks and supply chain disruptions are corrected. But this forecast is contingent on Latam central banks following through on price stability commitments to firmly anchor inflation expectations.

Central banks across the region have reacted by embarking on a tightening cycle to unwind the extraordinarily stimulative monetary conditions introduced in the pandemic. Key policy rates have been raised across the region; the latest increases coming in Mexico, where Banxico raised its policy rate 25 bps on November 11, and Peru, with the BCRP hiking its policy rate 50 bps, also on November 11. Despite recent increases, however, policy rates remain negative in real terms (adjusted for inflation) in Chile, Colombia, and Peru (chart 4). Central banks in Brazil and Mexico have been more aggressive in hiking rates, setting them apart from their peers in the region and around the globe (chart 5).

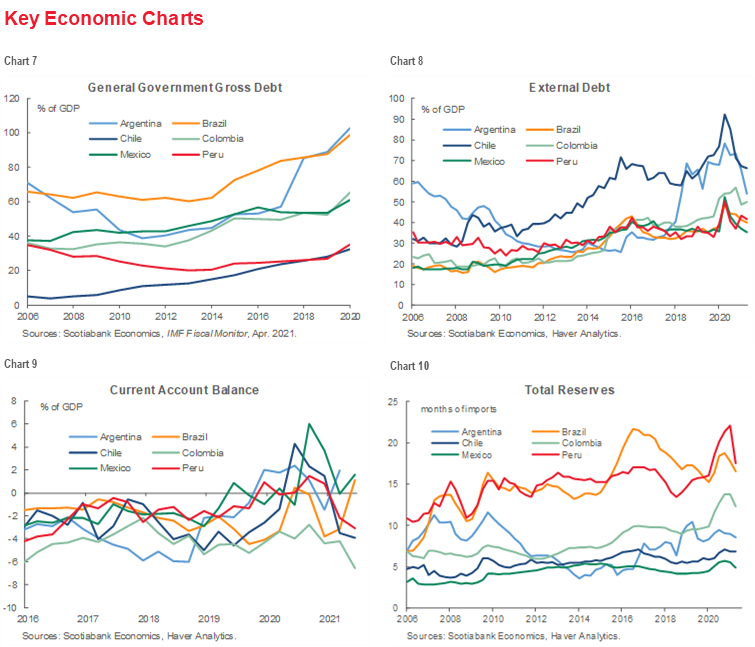

Fiscal authorities also responded to the pandemic with extraordinary measures to support the most vulnerable and sustain economic activity. The result was a marked deterioration in fiscal balances (chart 6) and a corresponding increase in general government gross debt as a share of GDP (chart 7). While public sector balance sheets provided a shock absorber through the pandemic, and an increase in debt-to-GDP ratios is consistent with that role, increases in Argentina and Brazil, which pre-date the COVID-19 event are noteworthy. Looking ahead, a further deterioration in public finances, particularly in the run-up to elections, could weigh on investor confidence.

Such concerns could be aggravated by external vulnerabilities, including external debt burdens (chart 8), current account balances (chart 9), and international reserves (chart 10). At this point, however, there is little indication of potential problems.

KEY MARKET CHARTS

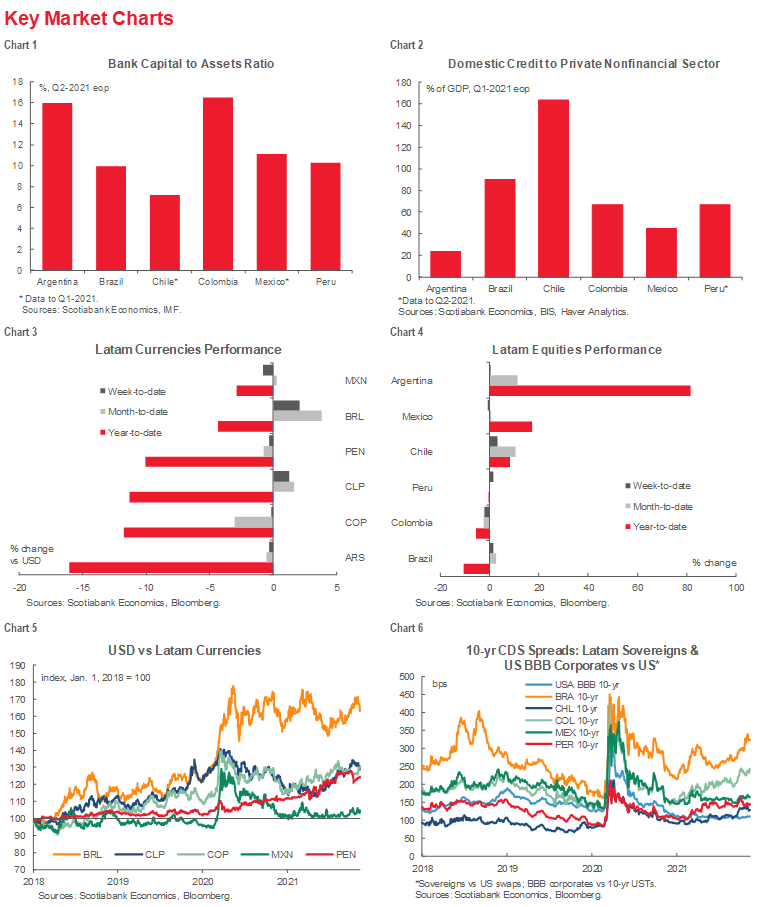

Financial markets in the Latam region have largely reflected two factors over the past six months: central banks’ tightening cycle and political uncertainty. In Brazil, for example, the real has appreciated against the US dollar in recent weeks on the back of the central bank’s policy (chart 3). The Peruvian currency, meanwhile, has rallied against the dollar, recouping the losses sustained earlier in the year as political uncertainty in the run-up to the presidential elections and the extended interregnum that followed took a toll on the pen. With that uncertainty reduced, and the administration in Lima projecting a more moderate tone, the financial environment has improved. In contrast, increased political uncertainty in Brazil, reflecting growing opposition to the president, has likely hurt local equity markets, which have underperformed relative to all other regional markets (chart 4).

The effects of the same two factors can also be discerned in a longer-term perspective. Latam currencies depreciated early in the pandemic, consistent with inflation-targeting regimes with flexible exchange rates, as central banks took extraordinary actions (chart 5). Similarly, 10-year CDS spreads on Latam sovereigns widened considerably in March 2020, but narrowed through the balance of the year (chart 6). Spread widening in Brazil, Colombia and Peru in 2021 has likely reflected political considerations and other idiosyncratic factors, such as the nationwide strikes in Colombia that had disrupted production earlier in the year.

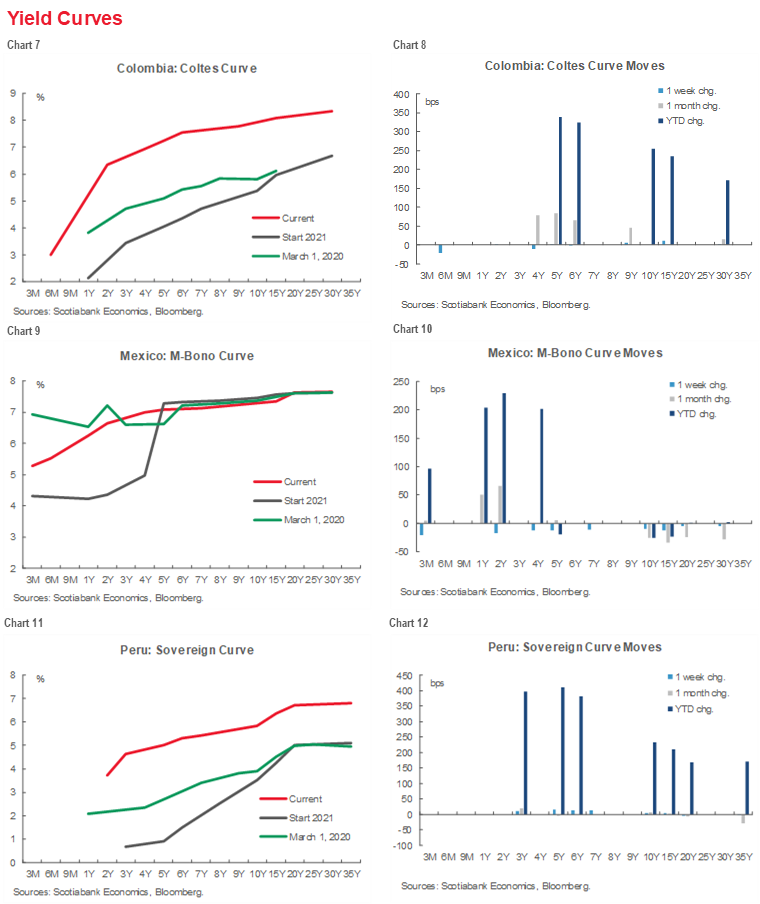

YIELD CURVE CHARTS

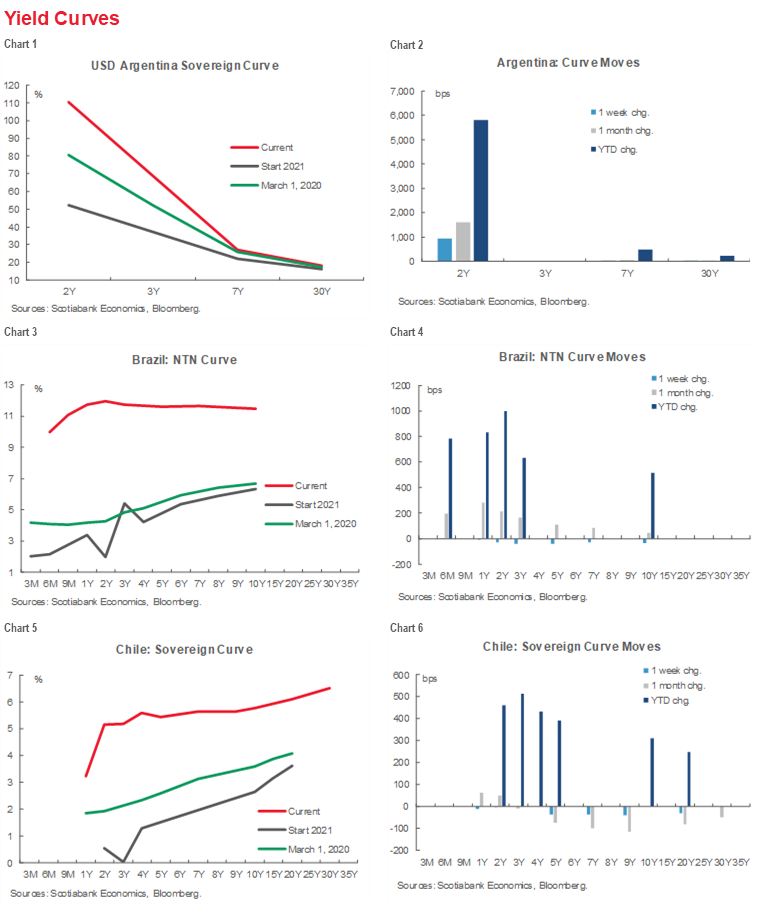

Latam sovereign yield curves have shifted up over the year as central banks started tightening monetary conditions (charts 1–12). Most sovereign curves have shifted up more or less uniformly over all maturities as markets have priced-in the effects of inflation and central banks’ reponses to price pressures. Argentina, which features a highly inverted yield curve reflecting the pervasive uncertainty regarding near-term debt sustainability, is an exception. Mexico’s curve is another exception. While the short-end of the curve has shifted up since the start of the year, beyond the medium-term it remains firmly anchored at its position at the start of the year.

KEY COVID-19 CHARTS

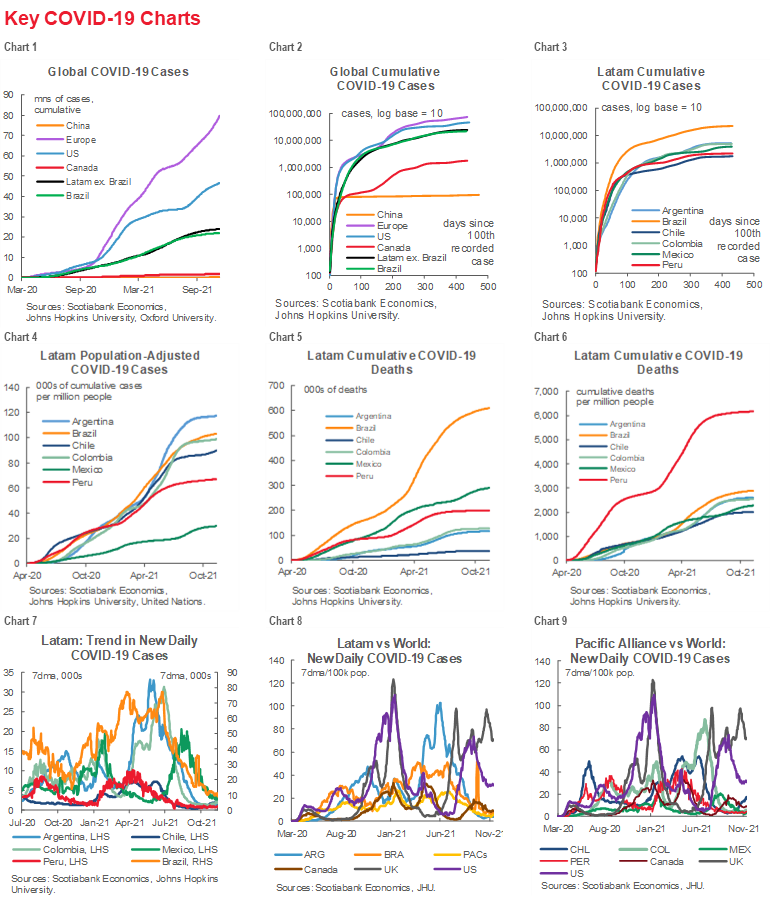

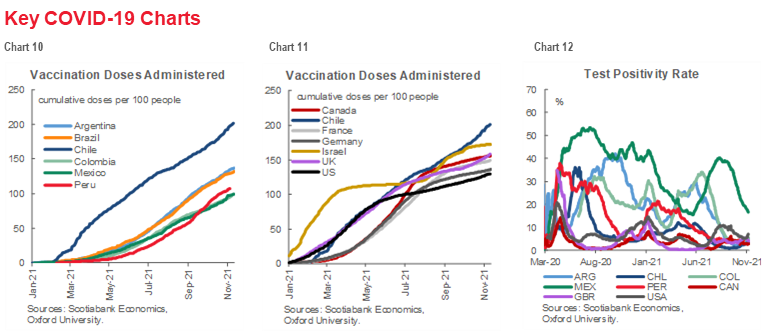

It was noted above that much of the uncertainty clouding near-term prospects has cleared. Unknowns related to the evolution of the pandemic remain, however. Charts 1–12 provide key monitoring tools. Of especial importance in this regard is the continued decline in new daily cases (chart 7) and test positivity rates (chart 12). At the same time, tracking vaccine doses administered (chart 10) provides a guide to the robustness of the recovery. Chile continues to stand out, not only in the region, but internationally, in this regard.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.