- Colombia: Robust manufacturing and retail activity in September puts economy on track to close gaps versus pre-pandemic

- Chile: Early MPR normalization met with decreasing long-term nominal interest rates; risk of inverted Yield curve

- Peru: October inflation and 12-month expectations keep up pressure on the BCRP; political tensions; mining investment

COLOMBIA: ROBUST MANUFACTURING AND RETAIL ACTIVITY IN SEPTEMBER PUTS ECONOMY ON TRACK TO CLOSE GAPS VERSUS PRE-PANDEMIC

On Thursday, November 11, Colombia’s statistical agency (DANE) released its monthly economic surveys for September. Indicators showed a strong close to Q3-2021, especially for services sectors which strengthened their performance amid “back to normal” mandates across the country.

DANE will release GDP growth data for Q3-2021 On Tuesday, November 16. Given yesterday’s indices, we think activity could surpass our Q3 1.1% y/y (+4.7% q/q) projection and confirm that in Q3, the economy would indeed close the gap versus pre-COVID-19 levels.

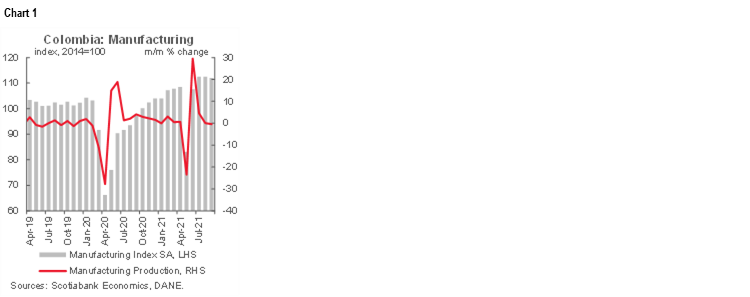

Manufacturing Production

Manufacturing production increased by a robust 15.5% y/y (close to market consensus +16.0%), while compared to the same pre-pandemic period (September 2019), the index grew by 12.2% (chart 1). On the employment side, the sector still shows a contraction of 1.8% versus pre-pandemic levels. In the YTD basis, manufacturing grew by 17.2% y/y, with mild gains in the employment side +1.9% versus Jan–Sept 2020. On a monthly basis, manufacturing contracted by 0.4% m/m (chart 1, again), the first contraction since May, a time when the nationwide strike interrupted the recovery. Either way, on a quarterly basis, manufacturing rebounded 12.7% q/q, consolidating activity levels above pre-pandemic.

In another report, which tracks enterprises sentiment, DANE emphasized that some industries are facing difficulties on their operations due to logistic issues related with input availability and it would impact the monthly performance.

Compared to the pre-pandemic period, the sector’s strongest gains came from beverages (+11.4%), chemical products (+31.1%), and food-related industries (+22.8%). Lagging the recovery are vehicle body manufacturing (-40.4%) and sugar and panela (sugar cane) industries (-6.5%). From the employment perspective, the main jobs contraction is reported in the clothing sector (-9.0%) and shoe manufacturing (-17.6%), both accounting for 83% of total jobs contraction.

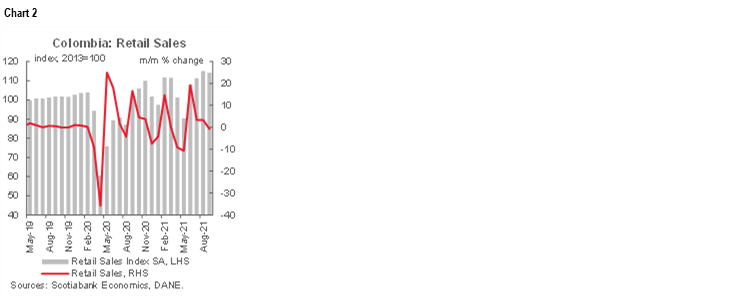

Retail Sales

Retail sales expanded by 15.3% y/y below Bloomberg’s survey (+19% y/y); and, compared to pre-pandemic levels (September 2019), retail sales are now 14.3% higher. On a YTD basis, retail sales increased by 20.4% relative to pre-pandemic (Jan–September 2019). Mobility and the return to in-person activities continued leading retail sales dynamics, which (excluding vehicles and gasoline) expanded by 12.1% YTD. Employment grew by 2.3% y/y, while compared with pre-pandemic the contraction is of 4.9%, as employment related to food service has been a hard-hit sector. On a monthly seasonally adjusted basis, retail sales contracted by 0.8% m/m (chart 2), probably impacted by expectations about VAT holidays in October, November, and December. On a quarterly basis, retail sales expanded 13.7% q/q, again showing activity levels surpassing pre-pandemic.

—Sergio Olarte & Jackeline Piraján

CHILE: EARLY MPR NORMALIZATION MET WITH DECREASING LONG-TERM NOMINAL INTEREST RATES; RISK OF INVERTED YIELD CURVE

In recent months, inflationary records have surprised the market, significantly above expectations in September and October. At the same time, 2-year inflation expectations are above the central bank target, standing at 3.5% according to the most recent Economic Expectations Survey (EES). At its October Monetary Policy Meeting, the central bank raised the Monetary Policy Rate (MPR) by 125 basis points and announced an early normalization of the interest rate which, in our view, could imply a new hike of 125 basis points in the December meeting, to leave it at 4%. Based on recent developments, the MPR would reach 5% by the end of the first quarter of 2022 according to our estimates, a level similar to that estimated by the analysts consulted in the EES.

On the other hand, long-term nominal interest rates have decreased in recent days. This is mainly due to political factors associated with the upturn of the right-wing presidential candidate, José Antonio Kast; the Senate’s rejection of the bill for a new withdrawal of pension funds and the possibility of limiting their adverse macroeconomic effects; and an expectation of a reduction of the fiscal stimulus in 2022.

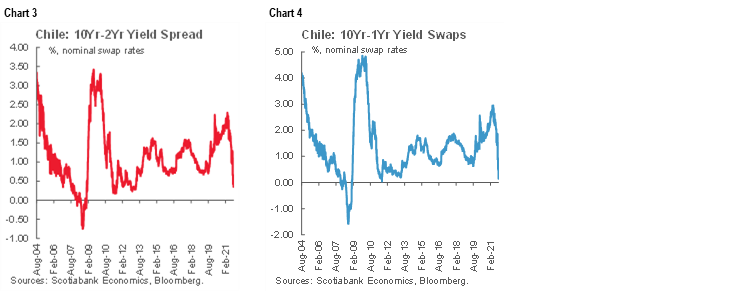

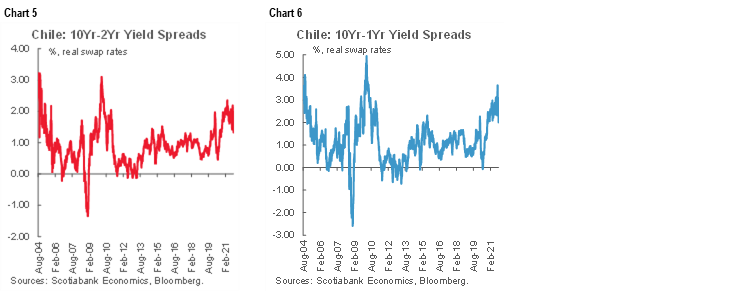

In effect, with the rise in short-term nominal interest rates and the fall in 10-year rates, we warn about the risk of having an inverted yield curve in the next few months. The spread between 10y nominal interest rate and short-term rates (1 and 2 years) is close to zero (charts 3 and 4), similar to that observed between 2011 and 2012. However, unlike a few years ago, the spread of real interest rates is positive (charts 5 and 6), due to the low level that the short-term real interest rate shows today. Behind that, is a higher inflation expectation today compared to that observed a few years ago.

We consider that the drop in the 10–2 year spread that we are currently observing is mostly associated with higher inflationary expectations and the consequent monetary normalization, in a context of an uncertain political scenario. Historically, a flattening yield curve and especially an inverted one has proved a robust deceleration indicator looking ahead 12 months or so. We consider that there is a risk of having an inverted yield curve in the coming months, in a context where the market is reducing GDP forecasts for next year. For now, the consensus expects a GDP growth around (or below) potential for the next two years. At Scotiabank, we project GDP growth of 4.5% in 2022 explained by a good performance of the first half but some deceleration during the second half.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

PERU: OCTOBER INFLATION AND 12-MONTH EXPECTATIONS KEEP UP PRESSURE ON THE BCRP; POLITICAL TENSIONS; MINING INVESTMENT

I. October inflation and 12-month expectations continue rising, putting pressure on the BCRP; withdrawal of monetary stimulus continues

As we commented in our Latam Daily (November 3, 2021), October inflation surprised market expectations again, driven by higher costs of inputs and imports and not by excess demand—according to the MoF—going from 5.2% y/y in September to 5.8% y/y in October, above the limit of the BCRP’s target range (between 1% and 3%), for the fifth consecutive month, reaching the highest rate since February 2009. Inflation also exceeded the BCRP’s 4.9% forecast for the year-end, which has an upward bias, according to the BCRP president. Core inflation rose from 2.6% y/y in September to 2.8% y/y in October, surpassing the 2% y/y target for headline inflation for the fifth consecutive month. All inflation trend indicators that the BCRP follows are above the target range.

The most recent survey by the BCRP on 12-month inflation expectations shows that it remained at 3.6% y/y in October, exceeding the upper limit of the target range for the third consecutive month. The inflation expectation for 2022 rose slightly from 3.25% to 3.30%. This situation is of concern to the central bank, as it could reflect that inflationary expectations are being disengaged from the target. The BCRP specified its view that inflation will return to the target range during the H2-2022 due to the reversal of the effect of transitory factors on inflation (FX rate, international prices of fuels and grains) and because economic activity will still continue below its potential level.

The pace of monetary expansion continues to decelerate, going from 3.8% y/y in August to 3.5% y/y in September, reflecting the withdrawal of monetary stimulus. However, loans expansion posted a slight rebound, from 2.4% y/y in August to 2.8% y/y in September, in line with the greater-than-expected recovery of the economy (chart 7). The BCRP statement reiterated that it will continue taking actions to mitigate the volatility of financial markets in a context of uncertainty. The BCRP has made a record FX intervention, due to the context of uncertainty. According to the BCRP, so far, capital flight has reached USD 15 bn, above its USD 14 bn forecast for the full year in September—most of it during Q2-2021. The BCRP has injected USD 16.7 bn of liquidity so far this year, with around USD 10.7bn in direct sales in the spot market and USD 5.4 bn in FX derivatives operations. Despite this, the NIR is higher than before the pandemic, which gives flexibility to the FX management of the BCRP.

II. Government completes issuance of global bonds for a total of USD 5.2 bn

This week the Ministry of Finance (MoF) placed the first social bond in euros for 1.0 bn with a 15-year term, complementing the issuance of bonds in dollars for USD 4.0 bn carried out at the end of October, with a term of 12, 30 and 50 years. The euro issue registered a bid to offer ratio of 2x with a coupon rate of 1.95%, 70 bps above the coupon rate obtained by a similar 12-year bond placed in March. The issuance of global bonds in dollars and euros will allow to pre-finance part of the needs for USD 9.5 bn foreseen for 2022 by the government.

—Mario Guerrero

III. Another cabinet member to be grilled by Congress

Congress voted (77 in favour, 34 against) on Thursday, November 11, to initiate impeachment procedures against the Minister of Defense, Mr. Walter Ayala. The process is scheduled for Tuesday, November 16. Mr. Ayala is being questioned for having removed the Chief of Staff of the Army, José Vizcarra, and of the Air Force, Jorge Chaparro, after both resisted attempts by the government to promote high-ranking officers to top positions, which is against the institutional authority of the armed forces. There is a strong likelihood that Ayala will be removed by Congress. Press reports state that the Head of the Cabinet, Ms. Mirtha Vásquez, had been in favour of requesting the resignation of Minister of Defense Ayala, but that President Castillo had defended him. Minister Ayala will first be questioned by Congress on the army events. Congress will then vote on whether or not to impeach him. If Minister Ayala is impeached, he will become the tenth cabinet member to be replaced, at a rate of one every eleven days.

Congress also voted on whether or not to initiate impeachment procedures on the Minister of Transportation, Mr. Juan Silva. In this case, however, the votes favoured Minister Silva, as only 27 votes were in favour of questioning him while 48 were against (and 39 abstentions). Minister Silva is a figure of controversy as he is widely viewed as favouring informal transportation workers over formalizing the transportation system to provide it with greater structure.

—Guillermo Arbe

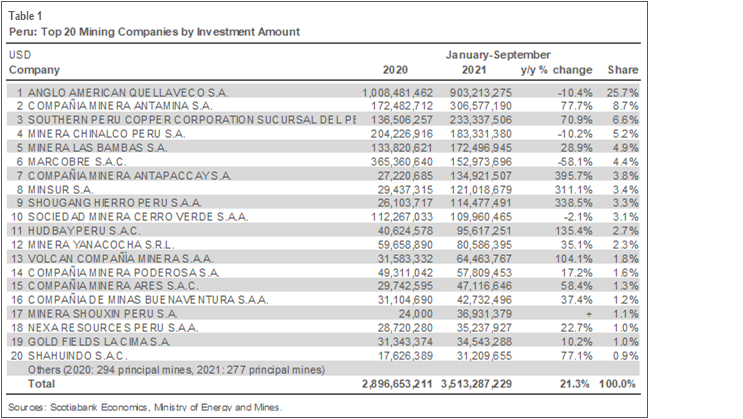

IV. Mining data continued recovering in September

Mining investment increased 55.9% y/y in September, according to data published by the Ministry of Mines. Investment increased 21.3% y/y (table 1), in the accumulated January–September period, driven by Antapaccay, Minera Chinalco with the Toromocho expansion and Anglo American with Quellaveco. The high level of increases largely reflects the low comparison base from the 2020 lockdown. However, the total investment in the two ongoing megaprojects Toromocho and Quellaveco, is slowing as construction is nearer to completion in 2022. To date, Quellaveco and the Toromocho expansion are 73% and 64% completed, respectively.

During the third and fourth quarters, investment is typically higher due to seasonal factors. We also expect mining investment to continue to approach pre-pandemic levels. Although the year started slow, the acceleration we are seeing skews upwards our earlier investment estimate of 19%. In 2022, we expect overall investment to slow and only increase for certain projects that are already underway.

Mining output continued to recover progressively in September. In the aggregate, copper production increased 10.9% y/y, and rose at nearly all major companies, including Minera Antamina (+24.6%), Cerro Verde (+8.1%), and Las Bambas (+4.2%), which together contribute more than 60% of the copper production, while the production fell at Southern (-3.0%) and Antapaccay (-9.2%). Production is likely to continue to increase with high metal prices as an incentive, in addition to high ore grades and new production from Mina Justa, which began operations in July 2021. Zinc output increased 30.5% y/y during the January–September period, driven by Antamina (+28.2%). Gold output increased 12.8% y/y continuing its recovery, although it has not reached pre-COVID-19 levels due to mine depletion (table 2).

—Katherine Salazar

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.