- Chile: CB surprised market expectations increasing MPR by 125 bps; Persistent dollarization by corporations & households

- Peru: PEN’s rally—currency reaches highest level since beginning of President Castillo’s administration

CHILE: CB SURPRISED MARKET EXPECTATIONS INCREASING MPR BY 125 BPS; PERSISTENT DOLLARIZATION BY CORPORATIONS & HOUSEHOLDS

I. Central Bank surprised market expectations increasing MPR by 125 bps; suspends foreign exchange purchase program

On Wednesday, October 13, the Central Bank increased the Monetary Policy Rate (MPR) by 125 basis points (bps), up to 2.75% (from 1.5%), well above market expectations. The board further assessed a less benign international economic scenario. Along with this, the CB also announced the end of the international reserves accumulation program, something we expected a few weeks ago (see our Latam Daily from August 19). The concern regarding the multilateral depreciation of the peso was also explicitly acknowledged.

Clearly, the exchange rate has become somewhat of a nightmare for the Central Bank (CB). Not only did they increase the MPR above expectations, but they also suspended reserve accumulation in order to give greater consistency to the macroeconomic scenario. It made little sense to continue normalizing monetary policy and, at the same time, continue accumulating reserves when it had already achieved a significant increase of USD 14 bn in international reserves since the program was announced last January, with purchases of USD 7.4 bn.

The missing ingredient to see the Chilean peso below USDCLP 800 again is that—if approved—the fourth pension withdrawal includes plenty of restrictions so it does not generate disinvestment of more than USD 10 bn, and that it closes the door to additional withdrawals until a consensus pension reform is achieved. It appears that the fourth pension fund withdrawal bill indeed has a good chance to succeed.

Following September's high inflation record (1.2% m/m), the Board of the Central Bank recognizes that headline inflation has exceeded the forecast in last September's Monetary Policy Report, but mainly in its most volatile components. They highlighted that core inflation continues around the projected level. As it rarely does, the Board anticipated a correction in its inflation projection, pointing to an annual inflation by the end of 2021 above 6% (5.7% previously projected).

In terms of global risk sentiment, the Central Bank reports a less benign scenario due to: a moderation in global growth prospects; an increase in inflation mainly due to the rise in fuel prices; a less expansionary monetary policy stance in developed and emerging countries; higher interest rates, and a depreciation of currencies against the US dollar.

For October and November, we expect inflation to print somewhat above historical averages, which will feed into the monetary policy decision of December 14. As a result, we expect the CB to hike again by 100–125 bps in the last month of the year. This will bring MPR slightly above its neutral level earlier than anticipated in the September MPR. Our view is that the new December Monetary Policy Report will not only correct inflation projections upwards, but also make an upward correction to the 2022 GDP forecast, which currently stands at 2%. We estimate a 2022 GDP expansion of no less than 4.5% given the growth inertia and abundant liquidity.

Market reaction: the CB affirmed its concerns about inflationary dynamics and the CLP depreciation. Moreover, the Board was willing to surprise the market on two consecutive occasions and has suspended the purchase of foreign currency at 62% of the announced purchases (USD 12 bn initially). We estimate some appreciative pressure over CLP. We also expect a slight increase in short-term swap rates.

II. Persistent dollarization by corporations and households in a context of political uncertainty

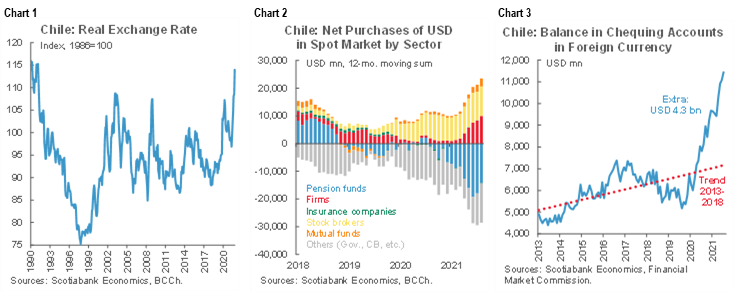

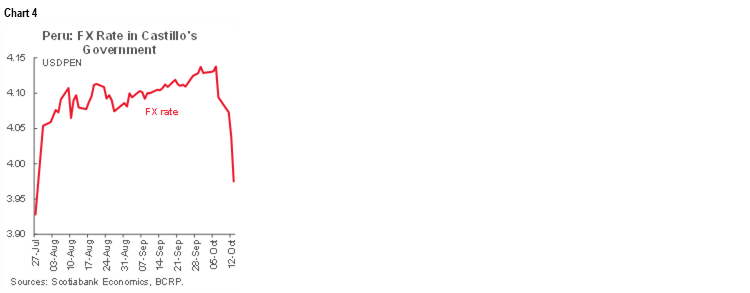

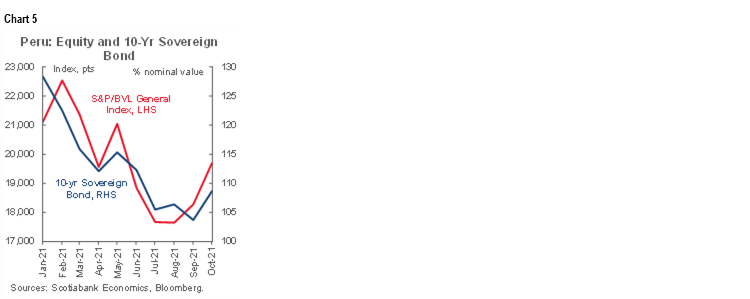

According to our estimations, the Real Effective Exchange Rate reached its highest level since February 1991 (chart 1). Even with the Government and Pension Funds selling US dollars, increasing the liquidity of foreign currency in the local market, the political uncertainty has driven a strong multilateral depreciation of the Chilean peso (CLP). Moreover, it is observed a rise in the net purchases of US dollars by some market participants, like stock brokers, mutual funds and corporations (chart 2). Likewise, since the end of 2019 the balance in checking accounts denominated in dollars is USD 4.3 bn above its trend value before the social unrest (chart 3).

In our view, the depreciation of CLP is explain by a higher degree of political uncertainty, due to the presidential election, pension fund withdrawals and the Constitution process. In this context, we observe a persistent dollarization by enterprises and households.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

PERU: PEN’S RALLY—CURRENCY REACHES HIGHEST LEVEL SINCE BEGINNING OF PRESIDENT CASTILLO’S ADMINISTRATION

Positive market sentiment continues after the last week’s cabinet changes. The country’s currency, PEN, which is the variable most sensitive to expectations, posted the best performance among emerging market currencies on Wednesday, October 13th (+ 1.7%), along with the South African rand (+ 1.1% ZAR) and the Swedish krona (+ 1.1% SEK), reaching its best level in two and a half months, accumulating an appreciation of 4% from its record of 4.14 (chart 4)

This movement is the largest since President Castillo took office, and it leaves behind—for now—an episode of high political uncertainty, promoted by the former chief of the cabinet, Guido Bellido, who had proposed the nationalization of the Camisea gas field. A new political tone has been further strengthened with the ratification of Julio Velarde as president of the BCRP’s Board, and an announcement by the new chief of the cabinet, Mirtha Vasquez, that a new constitution would not be a priority under her administration. The ruling party, Peru Libre, has nonetheless continued its efforts to collect signatures in favor of a referendum on that issue.

The supply of dollars has been dominated in recent days by flows of offshore investors driven by the change in local political sentiment and by the level of undervaluation of Peru’s assets. For example, the relative improvement with respect to other markets, such as Chile, which is itself undergoing some political volatility, is visible. So far this month, Peru’s Central Bank (BCRP) has sold dollars in the spot market for US$ 392 million, of which US$ 10 million were sold after the cabinet change, at USDPEN 4.039, which could be interpreted as a sign that the central bank would feel more comfortable with an FX rate below USDPEN 4.00, as it would help to moderate inflationary expectations. No sales have been made below that level.

Technically, the FX rate has been making a corrective movement of the rise that goes from USDPEN 3.58 to USDPEN 4.14, breaking the 50-day moving average (4.10) and the 100-day moving average (4.01), so this level would become a short-term resistance. We see supports at USDPEN 3.96 (channel resistance formed since the pandemic) and USDPEN 3.92 (38.2% Fibonacci level). This corrective move occurs within uptrend. The trend change signal would be activated with falls below USDPEN 3.86–3.84 corresponding to the 200-day moving average. If the PEN had depreciated the same as the average of emerging currencies since the beginning of the year, it would be around USDPEN 3.82. If the FX rate continues to develop its technical correction, we keep our forecast of 4.15 for the year-end. The PEN accumulates a depreciation of 9%, behind the CLP (15%) and the TRY (11%) since Peru’s first presidential electoral round earlier this year (April 11th).

The increased appetite for risk also reflects expectations for the possibility of new sovereign bond issues to complete this year's public financing and next year's pre-financing. Minister Francke has also ratified his intention to continue supporting private investment and confirmed that the official expectation of economic growth for next year is 4.8%, a rate close to that expected by the IMF in its most recent forecast (4.6%). Our GDP forecast (2.6%) sounds conservative by comparison, as we still see uncertainty regarding the performance of private investment.

Other Peru’s assets have also reflected a quick reaction from investors to recent political changes. So far in October the general index of the stock market (S&P/BVL) has risen 7.7% (chart 5), the yield of the 10-year sovereign bonds has fallen 66bps and the global bond in dollars in 10 years 17bps, while that 5-year CDS has been reduced by 12bps.

The expectation that the Federal Reserve will announce a reduction in monetary stimulus in November, possibly following up with interest rate hikes earlier than expected, have been reflected in a strengthening of the US dollar, which recently reached its highest level in a year, and in higher yields of Treasury bonds—which in two years reached their highest level in 18 months—which would limit a greater rally of the PEN in the short term.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.