- Colombia: October CPI lands below expectations due to VAT holiday; dynamic affirms our call for December hike

COLOMBIA: OCTOBER CPI LANDS BELOW EXPECTATIONS DUE TO VAT HOLIDAY; DYNAMIC AFFIRMS OUR CALL FOR DECEMBER HIKE

Monthly CPI inflation was 0.01% m/m in October 2021, according to DANE data published on Friday, November 5. This result was below the median forecast in BanRep’s survey (0.18% m/m), Bloomberg’s survey (0.22% m/m), and Scotiabank Economics’ projection (0.20% m/m). Foodstuff inflation led the gains, while the VAT holiday more than offset price increases.

October’s CPI result brings annual headline inflation to 4.58% y/y, up from 4.51% y/y in September (chart 1), still above the ceiling of BanRep’s target range (2%–4%) for the third month in a row and the highest since mid-2016. Core inflation fell again from 3.03% to 2.86% y/y, while ex-food and regulated goods inflation was 2.02% y/y (down from 2.28% in the previous month). Reduction in core inflation was mainly due to the temporary impact of the VAT holiday, however, it would contribute to lower indexation effects and should have a more lasting effect since November and December will also have more VAT holidays.

The previous dynamic could lead to ongoing divided opinions at the central bank’s Board in relation to inflation expectations and rates. Our base-case scenario is now of a 50 bps hike at the December 17 monetary policy meeting. For 2022 we expect the monetary policy rate to close at 5% (from a previous expectation of 4.50%). Find all our recently updated forecasts in Friday’s Latam Weekly here.

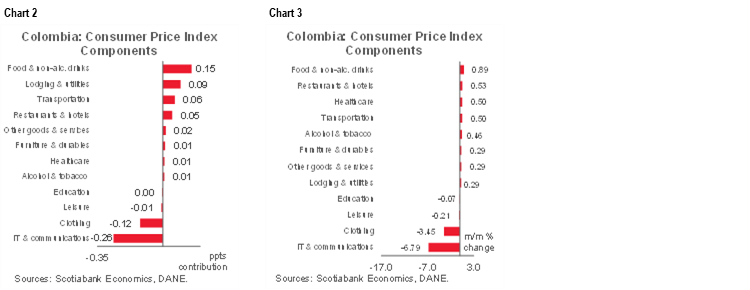

Looking at the Colombia’s October CPI numbers in detail, 2 out of 12 sectors retreated (charts 2 and 3), which was enough to offset positive pressures of foodstuff prices. The main highlights are:

- Foodstuff and restaurants inflation had the larger contributions (+15 bps and +9 bps, respectively). In the case of foodstuff inflation (+0.89% m/m), main gains came from meat (+1.54% m/m), milk (+1.94% m/m) and fresh fruits (+3.53% y/y). Meat and milk prices are showing impacts of scarcity due to climate issues but in the case of meat due to a higher trade effect since this year Colombia increased meat exports.

- However, some key prices continued declining, mainly eggs (-2.83% m/m) pointing to some normalization after the significant impact from the nationwide strike earlier this year, and rice (-3.68% m/m). Restaurant & hotel’s inflation in October contributed to the overall inflation to the same degree as in the previous month, due to higher food prices.

- The VAT holiday contributed to reducing the overall inflation figure as clothing prices posted a contraction of 3.45% (-12bps), a similar reduction to that observed the previous year during the VAT holiday of November. This effect would contribute to a moderate indexation effect ahead of 2022, however it is a temporary factor that will be reversed early in 2022.

- Another negative contribution came from the information and communications sector (-6.79% and -26pbs), as a result of a new campaign from the new competitor in the telecom services sector. We don’t expect this to happen again in the near future.

Looking at annual inflation across major categories, goods inflation fell to 2.63% y/y (versus 2.97% y/y in September), while services inflation fell by 23 bps from 2.01% y/y to 1.79% y/y. Regulated-price inflation increased by 20 bps to 6.14% y/y, due to utility fees which are facing effects from the exchange rate depreciation but also normalization after subsidies implemented one year ago.

Having landed below expectations, October’s inflation will likely moderate overall year-end inflation expectations, which is key since indexation effects would be lower. The core inflation metric also fell due to a temporary factor (VAT holiday), however, we think it won’t significantly change the central bank’s discussion as normalization in the monetary policy rate is responding more to a better economic activity expectations. That said, in terms of monetary policy, our base case scenario is now of a 50 bps rate hike for the December 17 BanRep meeting, likely still with a split decision. In 2022, we would face a new acceleration in inflation as VAT holiday effects would be reversed, which is why despite Friday’s good news regarding inflation, we still expect a hawkish rate hike in December.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.