- Chile: Door opens to new round of pension fund withdrawals; political impact of Pandora Papers

- Colombia: September inflation increased on mixed effect; split rate vote at BanRep’s October meeting likely

CHILE: DOOR OPENS TO NEW ROUND OF PENSION FUND WITHDRAWALS; POLITICAL IMPACT OF PANDORA PAPERS

I. Door opens to a new (fourth) round of pension fund withdrawals

Political dynamics among the political opposition are shifting support in favour of a new round of pension withdrawals. Opposition Senators who had previously expressed their refusal to a new withdrawal have more recently stated that they are now open to discuss the bill and even to approve it if the necessary adjustments are made. The low approval—around 10%—of Ms Yasna Provoste, a centre-left candidate for Christian Democracy, Socialist Party and other ex-Concertación, appears to be moving such key Senate votes.

The political scene is very liquid and there are still many barriers to overcome. Even if 26 votes are obtained in the Senate to approve the bill, it can be modified and returned to a mixed commission of senators and deputies, and then returned to a vote in both chambers. If it is approved in that commission and in the chambers, the president has the right to a veto, which has not been used in previous withdrawals, but could be used this time since the government has spent a lot of political capital in opposing this bill. The Senate vote is scheduled for October 27.

What kind of modifications would the Senate propose then? Several. Among them: that withdrawals pay income tax; that a longer term is given to withdraw; decreasing the maximum withdrawal amounts (currently at USD 5,500 per person); among many others. The central bank has warned that a new withdrawal of funds (USD 20 bn per the bill approved in the lower house) would pressure inflation by stimulating consumption and eventually overheating the economy. This would lead to the process of increases in the monetary policy rate being more intense than already considered.

II. Pandora Papers lead to potential constitutional indictment against President Piñera

The release of the Pandora Papers have led an important group of parliamentarians to prepare a constitutional indictment against President Piñera that would be presented as early as next week. According to the government, this accusation would have little foundation, but political analysts have pointed out that the electoral scenario offers maneuvering room for opposition candidates, notably Ms Yasna Provoste who lags behind in the polls. Consequently, we see a high probability that this accusation will be presented and discussed in Congress, although we see low probability that it means an early departure for Mr Piñera.

—Jorge Selaive

COLOMBIA: SEPTEMBER INFLATION INCREASED ON MIXED EFFECT; SPLIT RATE VOTE AT BANREP’S OCTOBER MEETING LIKELY

Monthly CPI inflation was 0.38% m/m in September 2021, according to DANE data published on Tuesday, October 5. This result is close to the median forecast in BanRep’s survey (0.30% m/m), Bloomberg’s survey (0.35% m/m), Scotiabank Economics’ projection (0.32% m/m) and the previous month’s 0.45% m/m. However, its breakdown deserves a closer look, because despite the overall number being closer to expectations, its composition was surprising as core inflation fell while annual headline inflation rose.

August’s CPI result brings annual headline inflation to 4.51% y/y, up from 4.44% y/y in August (chart 1), above the ceiling of BanRep’s target range (2%–4%) for the second month in row, and the highest since mid-2016. On the other side, core inflation fell from 3.11% to 3.03% y/y, while ex-food and regulated goods inflation was 2.23% y/y (down from the 2.32% in the previous month). As we discussed yesterday, this could lead to ongoing divided opinions at the central bank’s Board in relation to inflation expectations and rates. Our base-case scenario remains a 25 bps hike at the October 29 monetary policy meeting. However, there is a chance of a 50 bps hike if inflation expectations increase and show significant deviations from the target in the medium term.

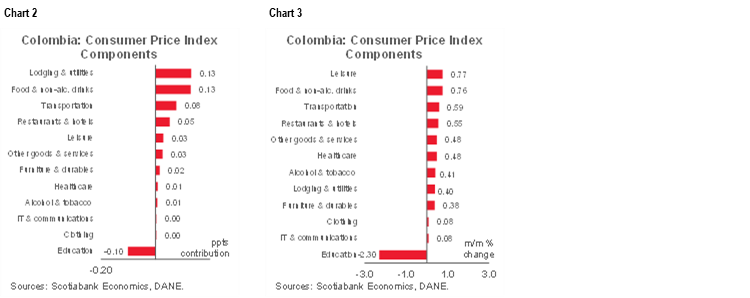

Looking at the September numbers in detail, only 1 out of 12 sectors retreated (charts 2 and 3). Once again, foodstuff inflation posted one of the highest gains. The main highlights are:

- Foodstuff and lodging & utility sectors had the largest contribution (+13 bps each). In the case of foodstuff inflation (+0.76% m/m), main gains came from pork (+3.59% m/m), meat (+1.19% m/m), chicken (+0.91% m/m) and fresh fruits(+2.56% y/y). However, some key prices are declining, such as eggs (-5.85% m/m) rice (-3.59% m/m), and onions (-4.86% m/m), pointing to some normalization after the significant impact from the nationwide strike earlier this year. We expect foodstuff inflation to moderate in the coming months, however, increasing inputs prices is something to keep an eye on, especially imported commodities such as soy and corn. On the other side, restaurant & hotel’s inflation in September contributed to the overall inflation to a lesser degree than in previous months, a trend that we expect would continue.

- On the lodging & utilities sector, the main positive contribution of utility fees (+1.13% m/m) were water (+2.09% m/m), and electricity (+0.96% m/m). Rental fees increased by 0.19% m/m, showing normalization effect after the pandemic.

- The only negative contribution came from education-related services (-2.92% m/m and -10 bps), which was unexpected but explained by the implementation of temporary subsidies in university fees for the low-income population.

- It is worth noting that food inflation and regulated prices continued leading inflation. However, core prices remained under control, and, despite the majority standing on the side of increases, in some cases we perceived moderation, affirming that as reopening consolidates, sudden prices changes are vanishing.

Looking at annual inflation across major categories, goods inflation increased to 2.97% y/y (versus 2.73% y/y in August), while services inflation fell by 24 bps from 2.16% y/y to 2.01% y/y. Regulated-price inflation fell by 26 bps to 5.94% y/y, since one year ago, normalization on utility fees started as some subsidies expired. That said, September is showing a mixed result, as core inflation components—especially services-related inflation—are decreasing.

All in all, despite September’s inflation results landing close to market consensus, they showed mixed signals. Core inflation metrics are falling due to a temporary factor (education subsidies), which reduces pressures ahead of the year-end inflation and, thus, indexation effects. In the last quarter of the year, inflation will face new downward pressures with the VAT holiday, which in our opinion would contribute to maintaining inflation expectations anchored in the medium term, especially in core metrics. That said, in terms of monetary policy, our base case scenario is still a 25 bps rate hike for the October 29 BanRep meeting, although a split decision would prevail, making our base case scenario a close call given the possibility of a 50 bps hike. With prices showing a mixed effect, however, we still think that the majority of board members would prefer to make cautious rate hikes.

—Sergio Olarte & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.