- Mexico: Banxico delivered a somewhat dovish 25 bps hike on Thursday

- Peru: BCRP raises rates by four consecutive months but says it doesn’t imply tightening cycle

MEXICO: BANXICO DELIVERED A SOMEWHAT DOVISH 25 BPS HIKE ON THURSDAY

As was expected by the consensus of economists, but seemingly disappointing the MXN and what was discounted into TIIE, Banxico hiked 25 bps in its November 11 meeting (chart 1). The TIIE curve was almost fully pricing in a 50 bps hike in both this meeting and the next, while MXN was up almost 0.7% on the day. Following the decision, the peso retraced to almost flat versus the USD, suggesting markets were taken off guard by the less-hawkish decision. Heading into Thursday, about 80% of economists (including our house call) had anticipated a 25 bps move, and about 20% looked for a 50 bps hike. However, there had also been a discussion of the Board possibly ending up in a three way split, with one vote supporting no change, two votes voting for 25 bps, and two more for 50 bps. In the end, the final decision left the Board split the same way as in its previous decision, with four votes for +25 bps, and Deputy Governor Esquivel supporting no change. Key points in the statement include:

- On the external front, the Board continued to see supply chain disruptions, fiscal stimulus, and a decomposition of spending towards merchandise (away from services) as the main drivers of global inflationary pressures—as well as commodity price shocks. The Board also took note of the accelerating withdrawal of global monetary policy stimulus and cautioned this could affect monetary and financial conditions. In some ways, this seems to continue to support the view of inflationary pressures being temporary, but there also seems to be added caution on market stability/volatility in the face of policy reversal in core markets.

- On the domestic front, the Board highlighted an economic contraction is likely in Q3, which is expected to reverse in the final quarter of the year, as well as an increase in financial market volatility. However, the Board also noted that slack remains present in the economy, although performance by sector remains highly uneven.

- Banxico highlighted the continued rise in both headline and core inflation in Mexico and noted the rise in inflation expectations for both 2021 and 2022, but highlighted that long term inflation expectations remain anchored. With this, the argument of inflationary pressures being temporary is reinforced, but balanced against it (and likely supporting the hikes) is the counter argument of the need to avoid a contamination of the price formation process. On this same direction, it’s worth noting that Banxico’s balance of inflation risks is skewed 5:3 in favour of upside risks.

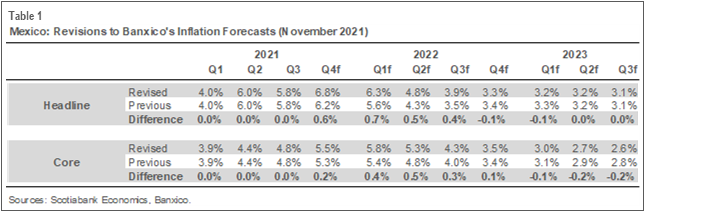

- Banxico made important upward revisions to both headline and core inflation forecasts for the next 12 months, but some modest downward revisions as we move into 2023 (table 1).

- The tone of the statement did not show a material shift to the hawkish side, which we take as support for our view that the pace of hikes will continue to be 25 bps per meeting, sustained without interruption until the first meeting of 2022, then followed by gradual tweaks to eventually take policy back to neutral settings (6.0%) at the end of 2022.

—Eduardo Suárez

PERU: BCRP RAISES RATES BY FOUR CONSECUTIVE MONTHS BUT SAYS IT DOESN’T IMPLY TIGHTENING CYCLE

The Board of Peru’s central bank (BCRP) raised its key interest rate by 50 bps to 2.00% at its meeting on Thursday, November 11, in line with market consensus according to a Bloomberg survey, the interest rate swaps market (2.3% with a term of six months) and our own forecast. Inflation expectations are above the target range, putting pressure on the BCRP to react by raising its benchmark interest rate.

In our Latam Weekly (October 22, 2021) we raised our benchmark rate forecast from 1.50% to 2.50% for end-2021, so we expect a new increase of 50 bps for the December meeting. Later, in our Latam Weekly (November 5, 2021) we further raised our forecast from 3.50% to 4.00% for 2022. This materializes the bullish bias that we have already observed in interest rates. Despite this adjustment, monetary policy would not lose its expansionary orientation, as interest rates would remain in negative territory in real terms.

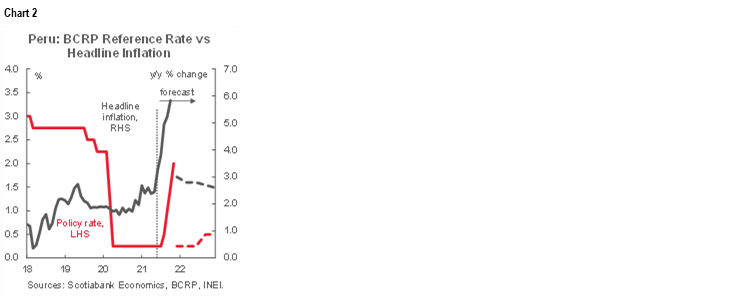

The BCRP’s president had previously indicated that he would continue with his policy of gradually raising the benchmark interest rate (chart 2). Compared with other economies in the region, the reference rate in Peru is relatively low. The BCRP statement emphasizes it is best to keep the expansionary stance of monetary policy for a prolonged period through the gradual withdrawal of monetary stimulus. The real interest rate of the monetary policy remains in negative territory, at -1.6% in November after the decision, reaching above -2.0% for the first time in six months. Likewise, the Board further indicated that it will remain attentive to new information regarding inflation expectations and the evolution of economic activity “to consider, if necessary, modifications in the monetary policy position”, a wording that has been used in cycles of interest rate hikes in the past.

The BCRP also pointed out that expectations about the economy continued to improve in October, although some indicators remain in negative territory. The president of the BCRP, Julio Velarde, recently pointed out that the economy could grow 13.2% this year, a rate higher than the forecast of 11.9% that the central bank made in September. Velarde pointed out that the higher growth rate is not only a consequence of a rebound but also of the actions taken by policymakers.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.