FORECAST UPDATES

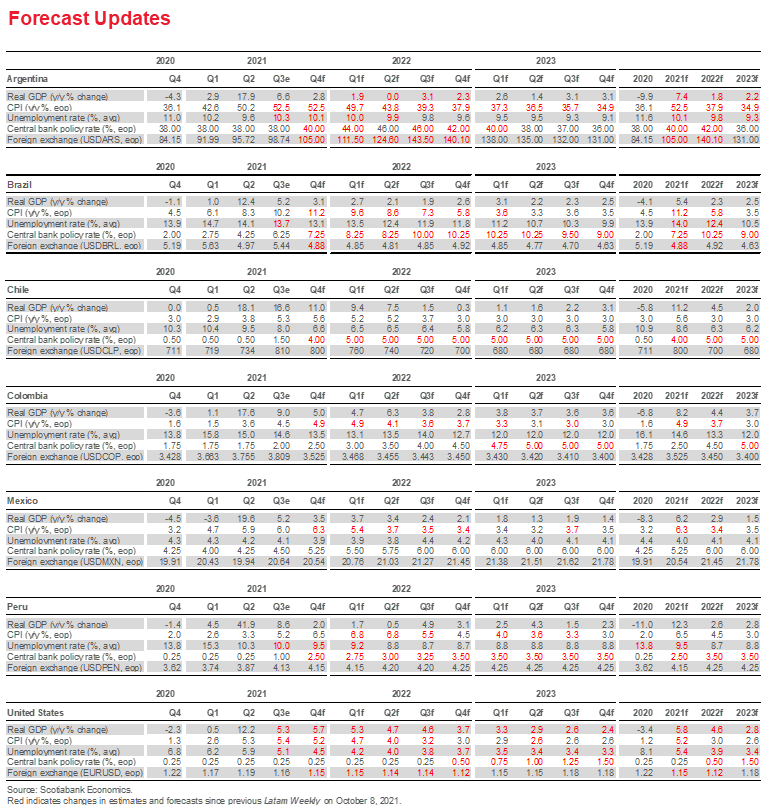

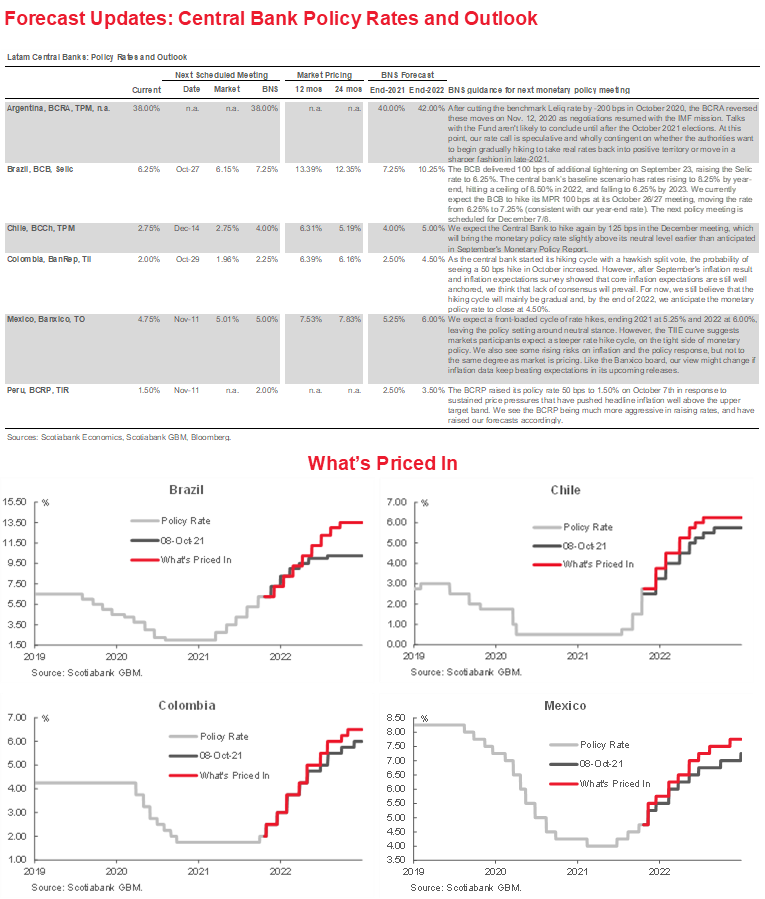

- Inflation and policy rate forecasts have been revised across the region. Key changes include those for Chile, where a further increase of the key policy rate in December is expected, to 4.00%. In Peru, we now expect a year-end reference rate of 2.50%, up from 1.50%. For 2022, while we maintain our forecast of four 25 bps increases, this implies a year-end rate of 3.50%.

ECONOMIC OVERVIEW

- With attention focused on inflationary pressures, a stocktaking of the recovery in Latam economies can help identify potential risks. The surprising strength of the rebound is reflected in evolution of forecasts for growth and inflation over the course of 2021, which have been revised up—significantly so in some countries.

- An uneven recovery could propagate supply shortages and bottlenecks, adding to price pressures. On balance, our stocktaking of the recovery to date suggests that good progress has been made thus far, but that risks remain.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period October 23–November 5 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Taking Stock of the Recovery

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Latam economies have made important progress towards recouping the output losses suffered in the pandemic. However, recovery has been accompanied by increased risks of persistent inflation.

- And as output returns to potential and full employment is restored, the risk of inflationary “overheating” rises. But inflation could also be affected by the pace of growth that generate supply bottlenecks and shortages that generate price pressures.

- In this respect, surprisingly robust growth has led to a progressive mark-up of projected growth in 2021. Similar increases in inflation forecasts have also been made.

- An uneven recovery that could propagate supply shortages and bottlenecks is another factor that could weigh on the inflation outlook. While there is some cause for concern in this regard, the overall picture is reasonably encouraging.

- A stocktaking of the recovery might thus be summarized as: good progress thus far, but risks remain.

GOOD PROGRESS THUS FAR, BUT RISKS REMAIN

A year and a half after the onset of the COVID-19 pandemic, output and employment in Latam countries are gradually returning to their pre-March 2020 levels. As case load and test positivity rates decline across the region countries can see light at the end of the tunnel. There is some uncertainty, however, as to whether that light is a runaway locomotive of persistently higher inflation that could unmoor inflation expectations, threatening long-standing price stability commitments.

Central banks in the region have embarked on a tightening cycle to rebalance monetary conditions—consistent with the need to avoid that outcome. In this regard, the balance of opinion contends that higher inflation is likely to prove temporary, as it reflects supply chain shortages and base effects that should dissipate over time. But should price pressures prove persistent, more aggressive interest rate increases would be needed to bring inflation down, with the concomitant output losses that would entail. In these circumstances, a stocktaking of the recovery can help in the assessment of future policy actions.

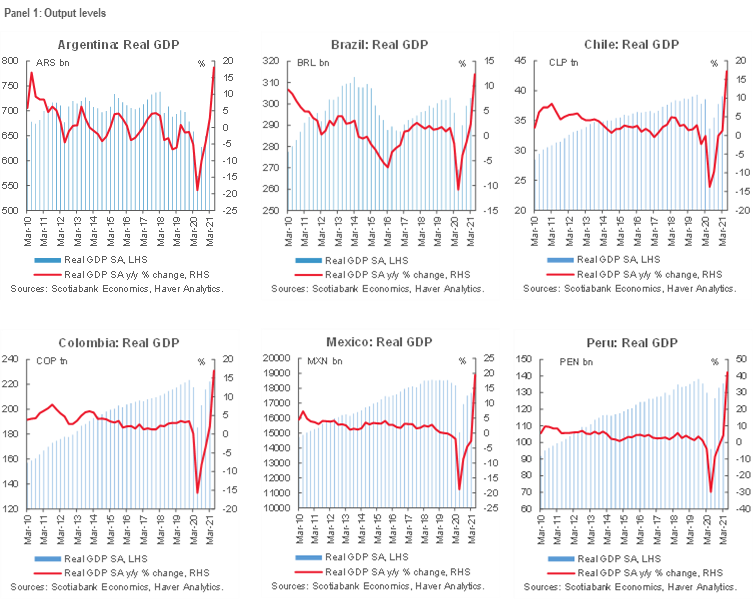

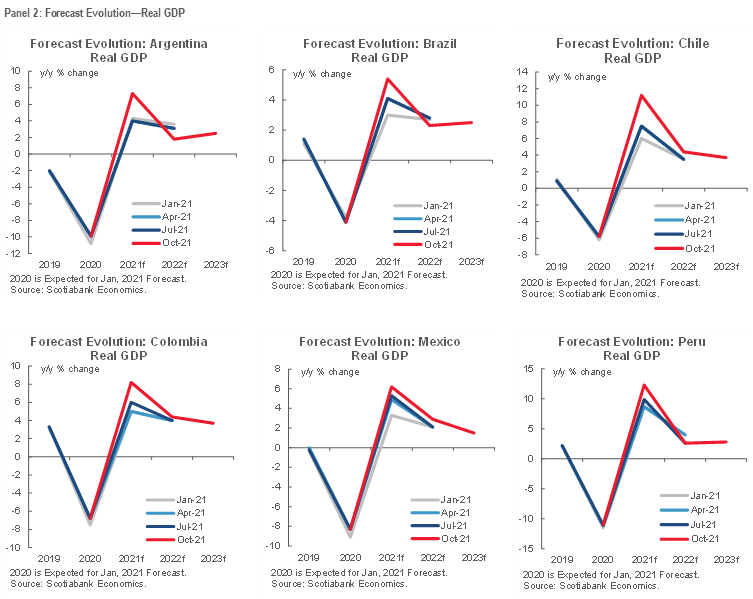

Looking at the current level of output relative to pre-pandemic output levels is a good starting point (panel 1). Progress has been made across the region. In Colombia, output has already returned to its pre-pandemic level. Brazil and Chile are likewise expected to recover on this basis in 2021. In Mexico and Peru, output is expected to return to its pre-COVID-19 level in 2022. Meanwhile, the recovery is progressing at a more languid pace in Argentina; pre-pandemic output there is not expected to recover until 2023.

Labour market indicators relate a similar story. Unemployment rates have declined as lockdown measures have been relaxed and employment has increased (chart 1). The recovery in unemployment has not necessarily mirrored the rebound in output, reflecting the fact that unemployment typically displays more persistence (“going up like an elevator, but coming down like an escalator”).

Further declines in unemployment rates will depend on the pace of employment growth going forward, as well as the labour force participation rate. Effective measures to contain the pandemic and facilitate mobility may be the key to bringing workers back. And while this would slow the decline in the unemployment rate, it would be unambiguously beneficial in terms of dissipating price pressures from labour shortages.

Inflation concerns may be driven not just by the recovery of output and employment to pre-pandemic levels, however, but also by the pace at which output is growing. The faster the rebound in economic activity, for example, the greater the potential for supply bottlenecks. In this regard, the expected pace of recovery in Latam countries has been progressively raised, as stronger-than-expected output data has come in. This effect is seen in the evolution of Scotiabank forecasts over the course of 2021 (panel 2). Our country economists have revised upwards projected growth for 2021: in the case of Chile, significantly so; with more modest increases In Brazil, Mexico and Peru.

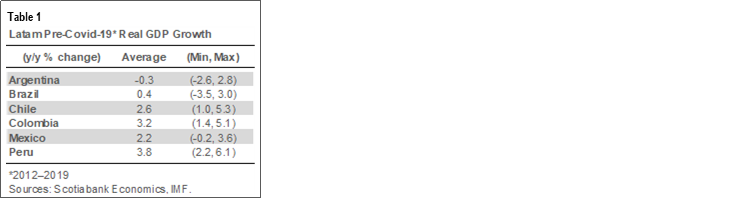

Growth is expected to moderate over the forecast horizon, as would be consistent with output eventually converging on potential and a return to full employment. For the most part, by 2023, Pacific Alliance countries (PAC) are projected to expand at a rate well below a pre-COVID-19 (2012–19) average (table 1), suggesting that possible “speed limit” effects, if any, would be negligible. Our team in Colombia, however, expects 2023 growth above its pre-COVID-19 average—albeit only slightly so. In contrast, Argentina and Brazil are expected to grow well above their pre-COVID-19 averages. But their growth performance prior to the pandemic was marred by severe recessions and idiosyncratic shocks that make a comparison with current projections problematic.

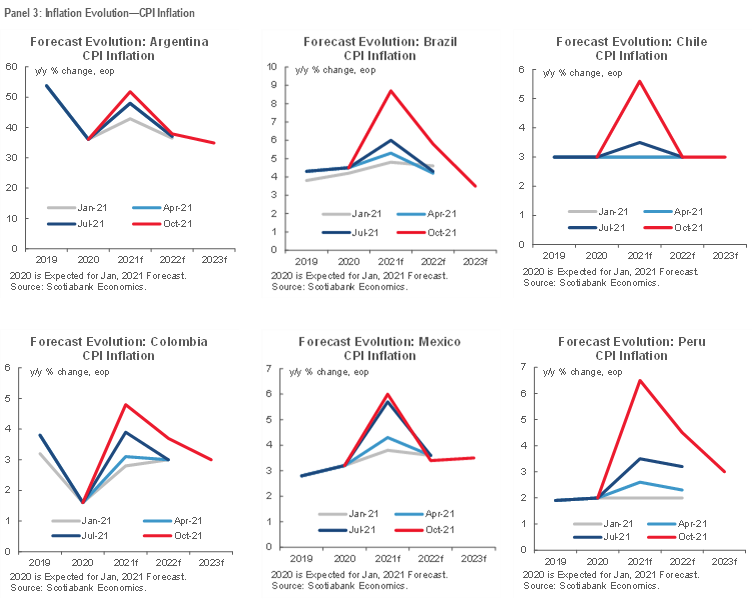

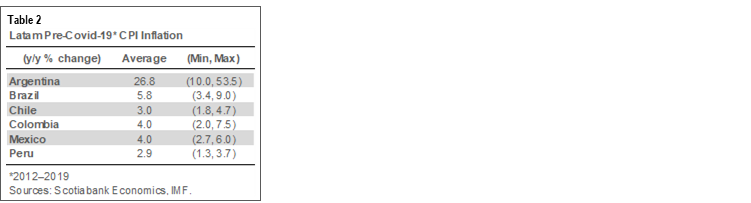

The sharp rebound in economic activity across the region is mirrored in the upward revisions made to inflation forecasts across the region (panel 3). As evidence of higher-than-expected inflation has accumulated, Scotiabank economists raised their projections for 2021 inflation, with the largest revisions in Brazil, Chile and Peru. At the same time, our country teams see price pressures dissipating over time, with inflation falling in 2022. In the PAC, inflation is generally expected to return to within inflation target ranges by 2023 (sooner in the case of Chile), broadly consistent with pre-COVID-19 performance (table 2). Projections of inflation returning to target ranges over time reflect the credibility of central banks’ inflation-targeting frameworks and underscore the importance of the proactive policy actions they have taken to support price stability commitments.

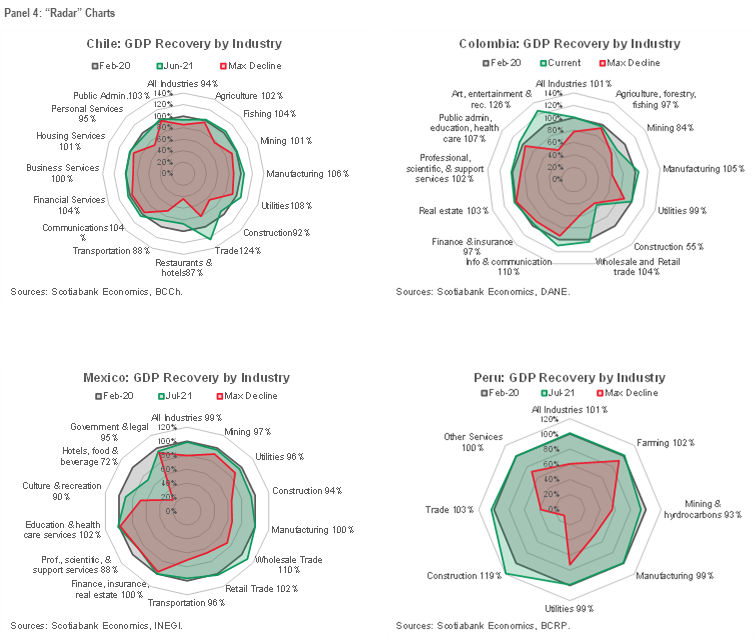

While important progress has been made in terms of the economic recovery, not all sectors have recovered at the same pace (panel 4). Uneven progress could pose serious impediments to further growth and full recovery. For example, various “frictions” in moving workers from one sector to another could lead to persistent unemployment in some sectors; more worryingly from an inflation perspective, they could generate localized labour shortages in other regions, resulting in higher costs that put upward pressure on prices. Moreover, the loss of firm-specific human capital during the pandemic, combined with lags involved in training new employees, could lead to shortages of key intermediate inputs that are required for the production of other goods.

A review of “radar” charts on the sectoral recovery in the PAC identifies some areas for concern (panel 4). In Chile, most sectors have fully recovered from the pandemic shock, with some sectors (e.g., trade) well above pre-pandemic level. But a key sector—transportation—lags behind. A similar picture is evident in Colombia, where the construction sector remains well below pre-pandemic levels of activity. Likewise, in Mexico, the mining, utilities and construction sectors lag behind other sectors. In some respects, the situation there appears reasonably balanced, though as the discussion below notes, there is an important regional dimension that could have significant effects on price pressures in the economy. In Peru, while most sectors have fully recovered pre-pandemic output levels, the important mining and hydrocarbon sector remains slightly behind.

Caution should be exercised in analyzing these charts given the substantial time lags in data availability, which possibly make any inferences “stale”. At best, they should be viewed as a snapshot at a period of time and may not reflect the current situation. That being said, while there is evidence of uneven recoveries across sectors, and thus potential concern, the overall picture they portray is broadly encouraging.

In this respect, a stocktaking of the recovery in the Latam region and the outlook for inflation can be summed up as: good progress thus far, but risks remain.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Persistent Inflationary Pressures Accelerate Withdrawal of Monetary Stimulus

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

56.2.2619.5435 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

56.2.2939.1495 (Chile)

waldo.riveras@scotiabank.cl

The daily number of confirmed COVID-19 cases has risen in recent days, reaching its highest (yet still low) level in almost three months, owing to an increase in the positivity rate to 2.5% in the last week (chart 1). The vaccination campaign has reached 89% of the target population, while the occupancy of ICU beds slightly increased, but remains at low levels. The COVID-19-related death rate continues to decline. Meanwhile, the rollout of booster doses keeps moving forward, reaching almost 4.3 million people. Thanks to these developments, mobility has returned to pre-pandemic levels in activities related to the workplace, retail and recreation. As of October 22, more than 95% of the population has reached the highest degree of mobility in the “Paso a Paso” Plan. And from October 1, the curfew and the quarantine phase no longer apply anywhere in the country.

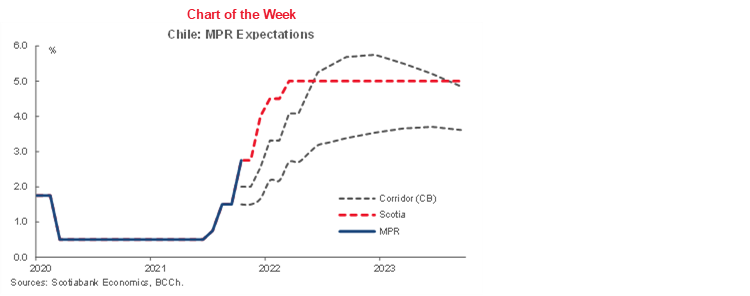

On Wednesday, October 13, the central bank (BCCh) increased the Monetary Policy Rate (MPR) by 125 basis points (bps), to 2.75% (from 1.5%), well above market expectations. In terms of global risk sentiment, the BCCh reported a less benign external outlook. The Board also recognized domestic challenges, with headline inflation exceeding the forecast in September’s Monetary Policy Report, mainly in its most volatile components. In this context, the Board anticipates revising its inflation projection, with an annual inflation by the end of 2021 likely above 6% (5.7% previously projected). In addition, the central bank suspended the reserve accumulation program started in January, consistent with the rebalancing of monetary conditions dictated by the macroeconomic scenario. In sum, the Board affirmed its concerns about inflationary dynamics and the depreciation of the Chilean peso (CLP). Accordingly, we expect the BCCh to hike again by 125 bps in the December meeting, bringing the MPR slightly above its neutral level earlier than anticipated in its September’s Monetary Policy Report (chart 2).

On Tuesday, October 19, the Ministry of Finance reported the issuance of Treasury bonds denominated in CLP, for a total of USD 1.1 bn. In 2021, Chile has now issued public debt totaling USD 27.5 bn. Of the total issued this year, USD 25.1 bn use margin debt authorization, which by law is approved up to a ceiling of USD 27 bn.

In the political arena, a group of opposition deputies presented an impeachment accusation against President Piñera based on possible crimes of bribery and tax evasion in the sale of Minera Dominga. President Piñera has already been formally notified, having 10 days to present his response to a Commission of five deputies. Subsequently, the Commission will present its report to the lower chamber to initiate the discussion. The lower chamber of the Congress will vote on the impeachment bill in the second week of November; a simple majority (78 deputies) can move the bill to the Senate, where a two-thirds majority is needed for approval.

The October 18 Cadem poll showed a statistical tie between the far-right candidate José Antonio Kast and the left-wing candidate Gabriel Boric on the road to November’s presidential election. In our view, the survey reflects a reordering within the political forces of the left and right. Sebastian Sichel (centre-right) is losing support following complaints about the irregular funding of his political campaign in 2009, while Kast is gaining some of that support with a better performance in recent debates. Meanwhile, Yasna Provoste could be capturing some of the votes lost by the centre-right candidate, though in our opinion she will likely have more support in the November election than is currently reflected in the polls. For now, according to the Cadem poll, Boric remains the strongest candidate in a runoff against either Sichel, Provoste or Kast.

In the fortnight ahead, on Thursday, October 28, the BCCh will release the Minutes of the last Monetary Policy Meeting. In addition, on Friday, October 29, the INE will publish the unemployment rate for the quarter that ended in September, as well as the indicators of economic activity by sectors for September. Lastly, on Tuesday, November 2, the CB will release September’s economic activity index (Imacec).

Colombia—Indexation Effects on Inflation are an Important Concern for BanRep

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Inflation has become a critical issue worldwide. While global supply chain bottlenecks and energy and other commodity price increases are perceived as transitory phenomena, clear signs of stabilization remain elusive. In Colombia, inflation has reflected the impact of international trends, as well as domestic effects, including the disruption generated by nationwide strikes and the effects of normalization of key prices that were frozen during the pandemic. Even though current shocks could prove to be temporary, the timing of price pressures matters given that they are taking place at a critical time of the year, in which many agents are about to decide price changes ahead of the coming year. That is why the central bank is worried about the potential long-lasting effect of the current temporary shock.

In this regard, December inflation in Colombia serves as a relevant reference to adjust prices each year. We can distinguish two main groups: i) prices indexed to the previous year’s inflation, and ii) prices indexed to the minimum salary growth (inflation + productivity). Therefore, even if current price shocks prove temporary, since they are taking place at the end of the year, they could affect some core inflation components in the year ahead. In fact, the hawkish stance of BanRep’s Board members suggests they are closely watching expectations of core inflation expectations.

The most important inflation-indexed item is rental fees (26% of total inflation), while items indexed to the minimum wage are labour-intensive services, such as restaurants (8.79% of total inflation) and domestic services (1.06% of total inflation). Other services such as utility fees have also increased; for example, water utilities can increase fees whenever accumulated m/m inflation exceeds 3%. Meanwhile, educational fees (4.41% of total inflation) reflect several factors, including December inflation. By our estimates, around 40% of the CPI basket in Colombia is affected by past inflation, and this group on average accounts for 75% of the increases on inflation and minimum salary (chart 1). This implies that current inflation pressures could have longer-than-expected lasting effects.

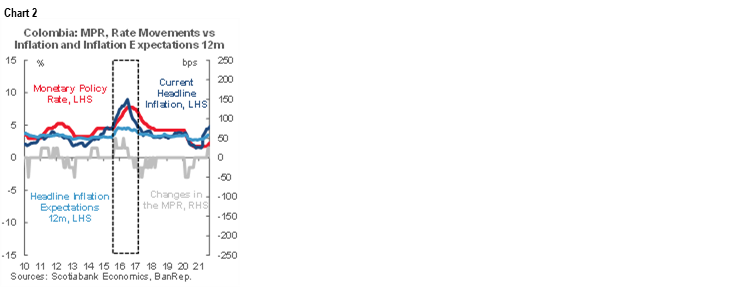

Past episodes illustrate these effects. In 2015–2016 Colombia faced a complicated inflation scenario which combined the impact of a significant FX depreciation due to the oil prices shock and the worst Niño Phenomenon in at least 50 years. Despite the temporary nature of those shocks, they triggered indexation effects, with significant impacts on core measures. In this case, the central bank resumed a paused hiking cycle with 50 bps increases, the strongest hiking reaction in recent history (chart 2). For that reason, we see now the Board closely monitoring the evolution of core inflation expectations, and why current transitory pressures matter.

Looking ahead, we expect inflation to close 2021 at 4.9%, and 2022 at 3.7%. However, indexed items are expected to close the year around 4.7%, which would drive core inflation to 3.7% by the end of next year, the highest since 2018. That said, in our forecast, price pressures normalize in 2023 and core inflation converges to the 3% target. In the meantime, signals of higher core inflation could motivate difficult discussions among the central bank’s Board, opening the possibility to a 50 bps hike, especially in Q1–2022 when inflation could accelerate. In this respect, every BanRep meeting could be a fine-tuning exercise of the analysis of the normalization process. For now, the basics stand, meaning the output gap is still negative and recent indicators suggest that economic recovery is not guaranteed.

All in all, even though core inflation could increase due to indexation effects, in the absence of further shocks such effects could be fully absorbed by 2023 and inflation expectations could remain well-anchored, as is currently the case. Based on this scenario, we keep our view of a gradual hiking cycle, with the policy rate closing 2021 at 2.50% and 2022 at 4.50%.

Mexico—What is Driving Mexico’s Inflation?

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

A major debate is ongoing in Mexico over what is driving the country’s inflation spike. There is widespread acceptance that global reflation (particularly in commodity prices), supply side disruptions, and to some degree base effects account for a major share of the recent inflation spike.

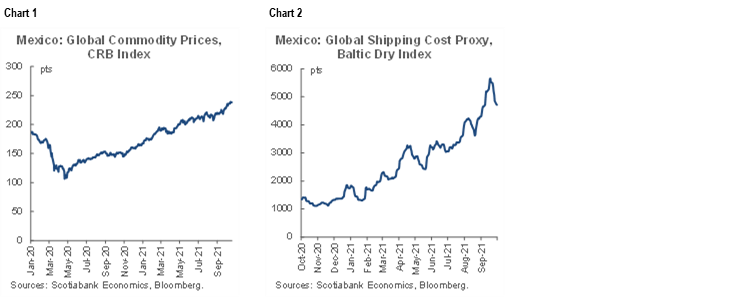

- On the commodity price front, we’ve seen the CRB index (a basket of commodity price futures which includes the international prices of both natural gas and oil) essentially double off its lows a year ago (chart 1). Numerous reasons lie behind the strong increase in global commodity prices, and include the recovery of demand, supply side constraints, as well as very high shipping costs (chart 2). Besides those external factors, important parts of Mexico were hit by a severe drought earlier in the year, driving up some agricultural prices (similar to what happened in parts of South America).

- Supply side constraints, which are affecting the manufacturing sector globally, are also seen as a big part of the explanation behind the current inflation spike in Mexico. The most widely documented shortages are in components such as microchips and steel, but the problem is widespread. In Banxico’s latest Quarterly Inflation Report, box 1 discusses the supply disruptions impact on US inflation, and box 3 does the same for Mexico.

- On the base effect front, we see two main base effects pushing inflation upwards. The first—steep increases in energy prices between late Q2 and early Q3—is largely behind us. Going forward, services inflation is likely to be pushed higher owing to base effects, peaking at the turn of the year, and lingering until early Q2–2022. On the positive side, looking ahead to next year, base effects should help dampen inflation from April onwards.

However, we think there are other factors driving Mexico’s inflation spike, including:

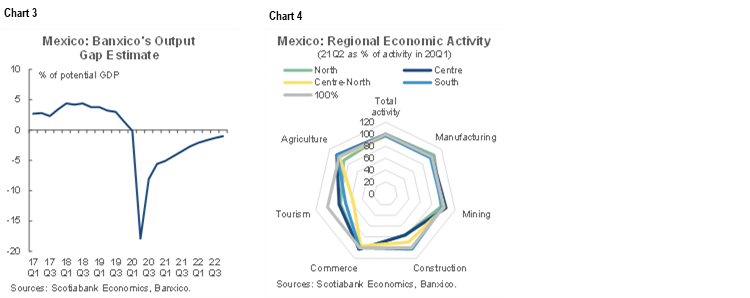

- Even though on average, we agree with Banxico’s assessment that we still have idle capacity until at least late-2022 (chart 3), we also think the output gap has closed in several key sectors—including those that have less elastic demand, and where supply chains are more complex and the price contamination process can be more severe. The bulk of the country’s recovery has taken place in the agricultural sector, manufacturing, and commerce. It is also regionally concentrated in the centre and centre-north of the country (chart 4), which is consistent with the sectoral recovery (the manufacturing and agro-industrial hub of Mexico). Sectors that have had the strongest recoveries (food and goods) tend to have less-elastic demands than sectors where the recovery has been slower (such as tourism and entertainment) and have more sophisticated and deeper supply chains, such that a player bumping into supply constraints can have bigger spillover in contaminating the price formation process.

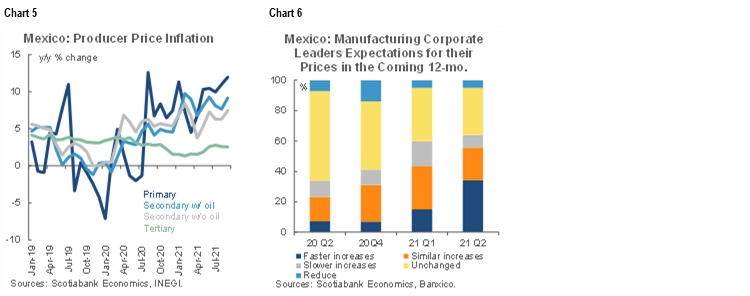

- Firm profit margins are another issue that we think explains Mexico’s inflation spike. Whereas the recession in the US lasted 2 quarters, in Mexico the economy underwent an eight-quarter stretch of flat and contracting growth, leaving companies with a tougher stretch to swallow. In addition, since mid-2020, producer prices for the primary and secondary sectors have been rising fast (chart 5). Firms are likely to take the opportunity to reverse the squeeze on margins and pass along those costs to consumers, which seems to be consistent with Banxico’s survey from September, in which 55% of manufacturing company executives said they plan to increase their prices at an equal or faster pace than currently over to consumers (chart 6).

With inflation risks rising (Banxico has made upward revisions to its inflation forecasts in three of its last four updates), the market has been discounting an increasingly steep rate hike cycle from the central bank (chart 7). The TIIE curve is currently pricing in a terminal nominal rate of 7.5%, which would be on the “tight side” of monetary policy, suggesting an expectation that risks of a policy mistake are rising (consistent with the increase in breakeven inflation in the Udi market). Our house view is that Banxico will deliver a front-loaded cycle that, combined with favorable base effects in 2022, will allow Banxico to leave its policy settings in neutral, which we estimate is somewhere around a 6% nominal policy rate. However, we do see rising risks to the upside, but not to the same degree as the TIIE curve is pricing in.

On other topics, Bloomberg reported that Mexico and the IMF are considering a 20% cut to the country’s Flexible Credit Line (currently around USD 63 bn) as global uncertainty fades and pandemic related risks fall.

Peru—Relief as Velarde Stays and a New Cabinet Head is Appointed; Economic Concerns Shift to Inflation and Monetary Policy

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Mario Guerrero, Deputy Head of Economic Research

51.1.211.6000 Ext. 16557 (Peru)

mario.guerrero@scotiabank.com.pe

The BCRP raised the reference rate by 50 bps, to 1.50% (chart 1), this month. In its guidance document the BCRP continued to state that the increase is not part of a cycle of increases. However, the BCRP has now raised rates for a third consecutive month, by 125 bps since August, and is likely to continue. We now expect the BCRP to increase the reference rate by 50 bps in both November and in December. As a result, we expect a year-end reference rate of 2.50%, up from 1.50%. For 2022, although we are maintaining our forecast of four 25 bps increases, this now implies a year-end reference rate at 3.50%.

Note that we are maintaining our inflation forecasts at 6.5% for 2021 and 4.5% for 2022. Thus, our view that the BCRP will be more aggressive in raising rates has to do with our perception of the BCRP’s behaviour, not with a change in perception regarding inflation. The BCRP has been acting more aggressively than its guidance has suggested in recent months, and we are aligning our expectations more with this practice. It would appear that the BCRP is finally coming around to the idea that inflation is more persistent than initially hoped. At the same time, the BCRP is probably more comfortable raising rates in an environment in which so many peers and global central banks are doing the same. But, mostly, the BCRP is mindful of the fact that inflation expectations are rising. Currently, 12-month future expectations are at 3.64%, up from 3.07% a month ago. With inflation at 5.2% and rising, expectations will continue escalating, putting pressure on the BCRP to continue to act. Note that, whether by design or not, since it began raising the reference rate in August, the pace has been in line with inflation expectations, and the real reference rate has remained fairly stable at just over -2.0%. If, as we expect, inflation continues rising to 6.5% or more in the next few months, then inflation expectations will have a lot of ground to cover to close the gap. It’s difficult conceiving of the BCRP allowing the real reference rate to fall below -2.0% in this scenario. If anything, it may become even more aggressive.

Inflation in Peru is mainly, but not entirely, due to global factors such as soft commodity import prices, energy prices, and higher freight and logistics/distribution costs for imports. However, the rising USDPEN FX rate has also been contributing to inflation. This, at least, has now begun to work in the BCRP’s favour. The FX rate has plunged from highs of over 4.10 prior to October 6, to levels in the lower 3.90s currently (chart 2). The about-face was due to the fall of the Guido Bellido Cabinet, and his replacement, on October 6, by Mirtha Vásquez as Head of the Cabinet. At nearly the same time, the government finally ratified Julio Velarde as Head of the BCRP (approval by Congress is still pending, but is expected), together with three suitable board of directors members. Both decisions produced a sense of relief in the business community, markets, press and most of the political community and public opinion.

Even as politics have been affecting financial and FX markets, its impact on growth and the real economy has been less evident. Thus, GDP growth was a solid 11.8% y/y, in August, the new government’s first full month in power, comfortably in line with our full-year forecast of 12.3%.

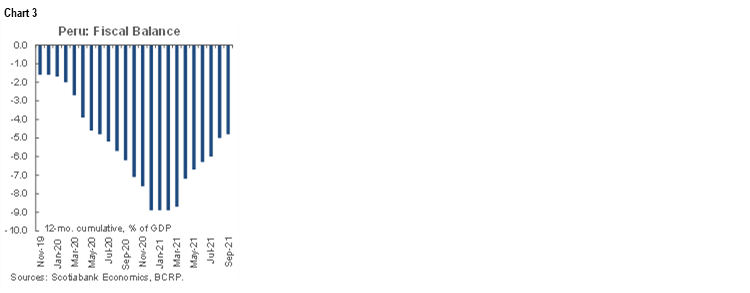

Peru’s shambolic politics is likely to have influenced ratings agencies in recent weeks. This week, Fitch lowered Peru’s rating from “BBB+” to “BBB”, and Moody’s changed its outlook for Peru from “stable” to “negative”, despite a sharp improvement in the fiscal balance in recent months. Peru’s fiscal deficit to September has fallen to 4.8% of GDP (chart 3), a significant decline from 8.9% of GDP at the turn of the year. What is even more impressive is that September saw a considerable increase in government spending, up 26% y/y (and 46% versus 2019), and yet fiscal revenue rose even more, 47% y/y (and 21% versus 2019). Fiscal revenue is soaring, not only compared to the low 2020 base, but also versus pre-COVID-19 2019. The two factors behind this leap—high metal prices (income tax revenue was up 45% YTD in September) and greater registered sales (domestic sales tax revenue was up 40% YTD in September)—are not due to temporary factors and are likely to persist going forward. This is giving the government room to increase spending. If fiscal accounts continue performing as strongly as these trends indicate, it will become increasingly difficult for ratings agencies to downgrade Peru further going forward.

Former Cabinet Head Guido Bellido was widely viewed as someone representing the radical wing of Perú Libre, and whose brief performance was fraught with questionable initiatives and confrontations with State institutions. There is hope that things will change for the better with Mirtha Vásquez heading the Cabinet, although it is not clear to what degree. Vásquez is a member of the leftist party Frente Amplio and has been known for her opposition to certain mining projects. And yet, she is viewed as a moderate and, perhaps more importantly, as a person that can be reasoned with, a reputation she gained when she presided over Congress from November 2020 to July 2021. She is also not likely to interfere with independent State institutions. Furthermore, through her appointment, President Castillo appears to have taken yet another step away from Perú Libre’s radical wing. However, the government still needs to improve its State management capabilities, deal with emerging social conflicts, and there is plenty of risk of over-imaginative labour and/or sector policies. Vásquez’ designation has reduced, but not eliminated, political and policy risk, but it does provide hope that the government’s agenda will be more reasonable than was feared under Bellido.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.