- Chile: Senate rejects fourth pension funds withdrawal; tone moderates and congressional commission to debate changes

- Mexico: Headline inflation above market expectations in October; we expect a 25 bps policy rate increase Thursday

CHILE: SENATE REJECTS FOURTH PENSION FUNDS WITHDRAWAL; TONE MODERATES AND CONGRESSIONAL COMMISSION TO DEBATE CHANGES

On Tuesday November 9, Chile’s Senate rejected the pension funds withdrawal bill that the lower house had approved. As a result, a mixed commission of deputies and senators will now be formed to study and modify the bill. Several of the senators indicated that the bill would have to include adjustments and restrictions to be approved. Some takeaways:

The restrictions, which we have discussed in earlier Latam Dailies (on October 6, and October 26) would go along the lines of reducing the maximum withdrawal amount. These would include levying taxes on the withdrawal but more importantly, several senators indicated that an agreement would have to be reached to ensure this is the last withdrawal.

The bill’s defeat is especially challenging for presidential candidate Ms Yasna Provoste (centre-left), a current Senator and supporter of the bill who had hoped to see it succeed, boosting her chances of advancing to the second presidential round (December 19).

The timing for an eventual fourth withdrawal bill “with restrictions,” would be after the first round of the presidential election. Therefore, the speed of the mixed commission to dispatch the new bill will depend not only on the members of said commission but also on electoral dynamics surrounding the eventual candidate running on the political left. At the moment, polls would seem to favour Gabriel Boric as the candidate representing the left at the presidential second round vote.

There is little doubt that the fourth pension funds withdrawal defeat generates a greater appetite for Chilean assets, since it would show political moderation in Congress, as well as a withdrawal with restrictions that would mitigate the negative effects.

—Jorge Selaive

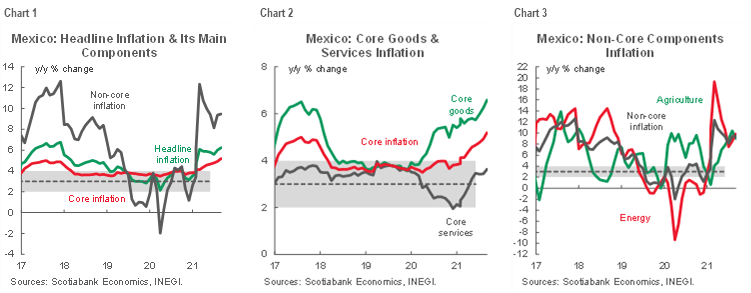

MEXICO: HEADLINE INFLATION ABOVE MARKET EXPECTATIONS IN OCTOBER; WE EXPECT A 25 BPS POLICY RATE INCREASE THURSDAY

Headline inflation in October landed above expectations again, accelerating from 6.00% y/y the previous month to 6.24% y/y (versus 6.19% y/y consensus), according to data by statistical agency, INEGI, released yesterday (November 9) (chart 1). Core inflation also accelerated, from 4.92% y/y to 5.19% y/y (chart 2), as merchandise prices rose from 6.26% y/y to 6.58% y/y, and services prices increased from 3.43% y/y to 3.64% y/y. Non-core inflation rose from 9.37% y/y to 9.47% y/y (chart 3), as energy prices accelerated from 11.69% y/y to 13.44% y/y, while food prices moderated from 10.41% y/y to 9.02% y/y.

In its sequential monthly comparison, headline inflation accelerated from 0.62% m/m to 0.84% m/m, exceeding the 0.75% m/m of the consensus. Its core component maintained upward pressures, rising from 0.46% m/m to 0.49% m/m. Merchandise moved from 0.68% m/m to 0.60% m/m, while services accelerated from 0.21% m/m to 0.38% m/m. Non-core inflation also accelerated, from 1.10% m/m to 1.87% m/m, energy soared from 1.13% m/m to 4.59% m/m, while food moderated from 1.38% m/m to 0.38% m/m. Thus, inflation maintains an upward trajectory at a faster pace than expected by analysts.

In terms of monetary policy implications, we maintain our expectation of a 25 basis point increase at the Bank of Mexico’s policy meeting tomorrow (Thursday). However, the composition of board votes could change, taking into account that a majority (but not all) members consider the decision to raise rates a useful signal of commitment to the inflation target, therefore it is possible that at least one member could vote for a 50 bps hike. However, all board members seem to agree that the increase might not be effective in tackling down inflation given its mainly supply-side nature.

Headline expectations for the end of the year remain on the rise, as consensus in the Citibanamex survey moved up from 6.46% y/y to 6.67% y/y at the end of 2021, with a higher grade of dispersion, as most of the respondents maintain an expectation of a 5.25% by the end of 2021.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.