- Chile: September inflation exceeds all expectations; revised CPI forecast FY 2021; President Piñera to be investigated

- Peru: BCRP hikes rate by 50 bps to 1.50%; with inflation up, we update our interest rate projection FY 2021 and 2022

- Colombia: Consumer confidence reached its best level since Jan-2020

- Mexico: Inflation accelerates in September further drifting away from Banxico’s inflation target

CHILE: SEPTEMBER INFLATION EXCEEDS ALL EXPECTATIONS; REVISED CPI FORECAST FY 2021; PRESIDENT PIÑERA TO BE INVESTIGATED

I. September inflation exceeds all expectations—among highest levels in 20 years; revised CPI forecast FY 2021

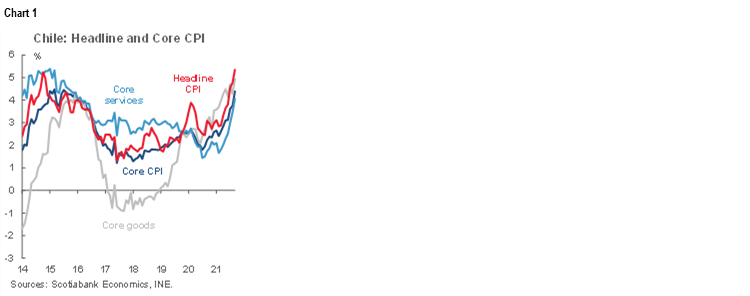

September CPI increased 1.2% m/m (5.3% y/y, chart 1), above both the market and our own expectations. By category, food prices increased 2.1% m/m, with an incidence of 0.4 percentage points (ppts), while transportation increased 2.7% m/m, with an incidence of 0.36 ppts. September’s inflation is typically high, but the 2021 record was the second highest in 20 years.

Furthermore, these increases are quite general, across all basic basket categories (chart 2). The inflationary diffusion indicator of the CPI reached 62.7%, above the historical range for the month, showing that a large number of products, especially goods, have begun to inject greater inflationary pressures. Thus, the diffusion of goods reached 70.3%, exceeding its historical range, while the diffusion of services continued to show an upward normalization, standing at 50%, around its average.

Taking all this into account, we are revising our 2021 CPI inflation projection from 5.0% to 5.6%. We expect a certain inflationary break in October given the high comparison bases remaining for several goods, but we will also have seasonal and gasoline price increases that make us expect a monthly CPI record around historical averages for October.

September’s CPI surprise will doubtless have an impact at next week’s monetary policy meeting, as we believe the central bank’s Board will have little option but to hike the policy rate by 75 bps, and perhaps even consider 100 bps. More in-depth analysis will follow in our upcoming publications.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

II. President Piñera to be investigated by the National Prosecutor

The National Prosecutor, Jorge Abbott, decided to initiate a criminal investigation ex officio for the alleged crimes of bribery and tax evasion in the sale of Minera Dominga, which would involve President Sebastián Piñera. The decision was based on the recommendations of the report issued by the Anticorruption Unit of the National Prosecutor's Office (UNAC), which analyzed information revealed by the international journalistic investigation Pandora Papers on the purchase agreement of Minera Dominga, carried out in a tax haven, at the end of 2010. This investigation is expected to be expedited given its public relevance.

The Chilean peso experienced a significant depreciation with respect to other currencies when news of this investigation became known. We believe it unlikely that this will result in charges against the president, but as long as the investigation lasts, we expect that Chilean financial assets would maintain a relative penalty compared to other peers.

—Anibal Alarcón

PERU: BCRP HIKES RATE BY 50 BPS TO 1.50%; WITH INFLATION UP, WE UPDATE OUR INTEREST RATE PROJECTION FY 2021 AND 2022

I. BCRP hikes rate by 50 bps and announces gradual withdrawal of monetary stimulation

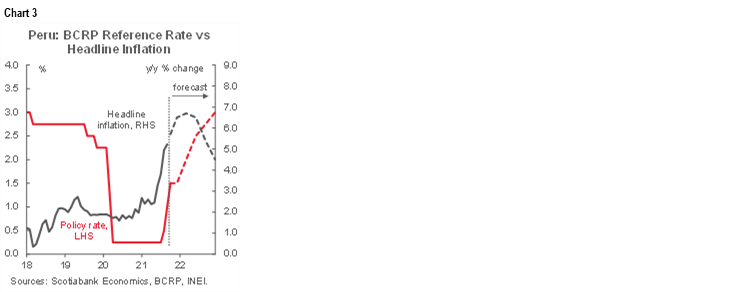

The Board of Peru’s central bank (BCRP) raised its key interest rate by 50 bps to 1.50% at its meeting on Thursday, October 7. The decision was expected by the market consensus according to a Bloomberg survey and the interest rate swaps market (1.4% with a 3-month term). We expected at least a 25 bps hike, but the decision to increase by 50 bps does not surprise us given the upward interest rate bias. The BCRP’s president had previously indicated that they would continue with their policy of gradually raising the benchmark interest rate as the previous level (1%) was exceptionally low (chart 3).

The BCRP statement emphasizes it is best to keep the expansionary position of monetary policy for a prolonged period through a gradual withdrawal of monetary stimulus. The real interest rate of the monetary policy remains in negative territory, at -2.1% in October after the decision. The Board further indicated that it will remain attentive to new information regarding inflation expectations and the evolution of economic activity "to consider, if necessary, modifications in the monetary policy position", a wording that has been used in cycles interest rate hikes in the past.

The BCRP also pointed out that expectations about the economy have improved slightly in September, recovering compared to August, although they remain in negative territory. The BCRP’s president considers that improvement in business expectations will be important for a greater recovery of the GDP in 2022. For next year, the BCRP estimates GDP growth of 3.4% noting that growth momentum is strong, but that could be impacted by negative expectations.

II. Rising inflation (and expectations) pressuring the BCRP; we update our interest rate projection FY 2021 and 2022

As we discussed on Monday, inflation rebounded again in September, driven by higher costs of inputs and imports, going from 5.0% y/y in August to 5.2% y/y in September, above the limit of the BCRP target range (between 1% and 3%), for the fourth consecutive month, and reaching the highest rate since February 2009. Inflation also exceeded the BCRP forecast of 4.9% for year-end, which has an upward bias, according to recent statements by the BCRP’s president. Core inflation remained at 2.6% y/y in September, although it exceeded the 2% y/y target for headline inflation for the fourth consecutive month. The BCRP statement no longer refers to trend inflation indicators, as these had been creeping upward.

The most recent BCRP’s survey on inflation expectations 12 months ahead is increasing, from 3.1% y/y in August to 3.6% y/y in September, exceeding the upper limit of the target range for the second consecutive month. This situation is of concern to the central bank as it could reflect inflationary expectations are being disengaged from the target. However, it emphasized that inflation expectations for 2022 are located at 3.3% slightly above the upper limit of the target range. The BCRP confirmed its view that inflation will return to the target range in the next 12 months due to the reversal of the effect of transitory factors on inflation (FX rate, international prices of fuels and grains) and because economic activity will continue below its potential level.

Inflation expectations are already beginning to reflect this bias, pressuring the BCRP to react by raising its benchmark interest rate, leading us to raise our own reference rate projection from 1.25% to 1.50% in 2021, and from 2.50% to 3.00% in 2022. This materializes the upward bias that we had already observed in the interest rates. Despite this adjustment, monetary policy would not lose its expansionary orientation, since interest rates would remain in negative territory in real terms.

Monetary expansion has materially slowed, from 32% in 2020 to 3.8% y/y in August, reflecting the stricter position of the BCRP, which has been affecting the dynamism of loans, which in the same period went from 11.8% to 2.4% (chart 4).

The BCRP’s statement confirmed that it will continue taking actions to mitigate the volatility of the financial markets in the context of uncertainty. In the FX market, the BCRP has injected USD 14.5bn of liquidity so far this year, with around USD 10 bn in direct sales in the spot market and USD 4.5 bn in operations with FX derivatives, despite which the USDPEN rate hit a record 4.14 last week. The BCRP’s president, Julio Velarde, pointed out that exchange controls do not work and clarified that his institution is not “all powerful” to stop the rise of the dollar. As part of its toolbox, the BCRP implemented new FX swaps with fixed rates in soles and dollars so that agents can participate without having to seek hedges with variable interest rates.

Also, per our Latam Daily on Monday, Peru’s government has ratified Mr Julio Velarde as a Head of the BCRP’s Board. The other three members nominated by the President have a profile of social researchers, albeit without specialization in monetary policy. The selection of the remaining three members is pending (to reach a total of seven board members), who will be appointed by Congress. In this regard, the Congressional Economic Commission has approved the criteria for the selection of the remaining directors, based on knowledge, with a minimum experience of 10 years, and defined the legal impediments and conflicts of interest.

—Mario Guerrero

COLOMBIA: CONSUMER CONFIDENCE REACHES ITS BEST LEVEL SINCE JANUARY 2020

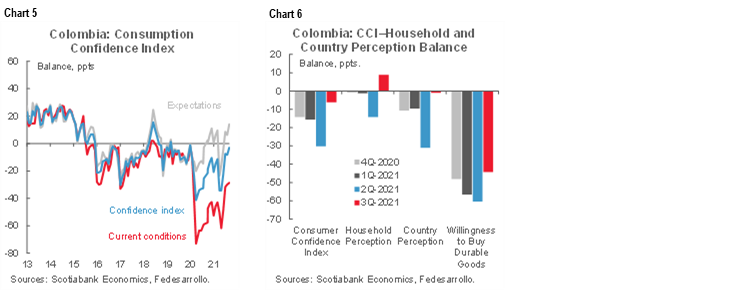

Colombia’s Consumer Confidence Index (CCI) in September reported a balance of -3 ppts, improving from the -8.2 ppts in August and reaching its best level since January 2020. The data was released by Colombia’s Fedesarrollo statistical agency on Thursday, October 7.

In September, Colombian main cities continued lifting restrictions for massive events and indoor capacity. Therefore, under the current environment, consumers’ assessment about the future has rebound significantly (chart 5), showing optimism about the country’s economic future. It is worth noting that the assessment of current conditions also improved as consumers perceive their households currently are doing better (chart 6).

Looking at September’s details:

- The Current Conditions Index rose to -28.7 ppts from August’s -29.9 ppts, its highest level since February 2020. Although consumers’ perceptions of the current situation remained deep in negative territory, it is showing progress and is at the best level since the pandemic began. Consumers’ appetite to buy new durable goods remained low, however, it improved to -44.3 ppts from the -45.1 ppts of the previous month. We think, current price dynamics within a labour market which still is consolidating gains, are moderating consumers’ willingness to purchase durable goods.

- The Expectations Index increased by 7.9 ppts from August’s 6.2 ppts level (chart 5, again). This index reached its best level since mid-2018, consumers are optimistic about the economic future and now this confidence is improving also the perception of economic wellbeing in their households.

- Consumer confidence numbers improved in four of the five major cities surveyed at the regional level, with Medellin now leading the gains, while Cali remains a latecomer remaining in the territory, mainly on lower willingness to buy durable goods. On the other hand, willingness to buy houses improved in all cities but Barranquilla.

- In September confidence rebound across socioeconomic status: high-income households had the most significant rebound from the -10.1 ppts to 2.6 ppts, while the low-income population posted an improvement from -9.8 ppts to -4.2 ppts. Middle-income households’ confidence increased by 3.8 ppts to -2.6 ppts.

Overall, September’s consumer confidence strengthened as Colombia is consolidating a strong reopening. It appears consumers are more optimistic about the future and the assessment of current conditions is improving at a slower pace. That said, we expect that as the labour market consolidates and main cities continue allowing traditional services to operate, the sentiment will further improve, translating into better consumption numbers.

—Sergio Olarte & Jackeline Piraján

MEXICO: INFLATION ACCELERATES IN SEPTEMBER FURTHER DRIFTING AWAY FROM BANXICO’S INFLATION TARGET

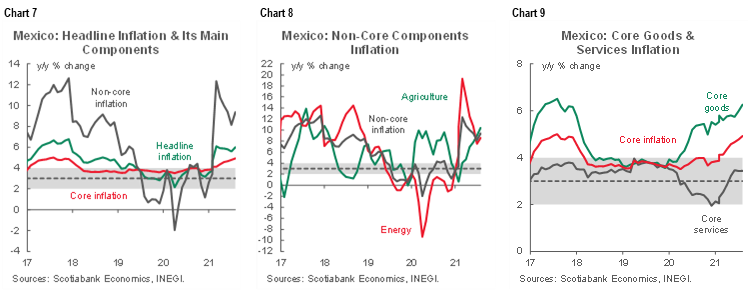

Headline annual inflation in September edged up from a previous 5.59% y/y to 6.00% y/y, (chart 7) per Mexico’s statistical agency, INEGI. This was in line with the Bloomberg consensus and twice the central bank’s (Banxico) inflation target of 3.0%. By components, non-core inflation rebounded from 8.14% y/y to 9.37% y/y, due to a rebound in energy prices, as well as persistent increases in the food subcomponent (chart 8). Core inflation upheld its upward trajectory, standing at 4.92% y/y, up from 4.78% y/y in August (chart 7, again). Merchandise inflation rose from 5.99% y/y to 6.26% y/y, while services stood at 3.43% y/y (chart 9).

In its sequential monthly comparison, headline inflation surpassed analysts’ expectations in the Citibanamex Survey of 0.059% m/m, as it accelerated from 0.19% m/m to 0.62% m/m. The core component maintained its upward pace, rising from 0.43% m/m to 0.46% m/m, from 0.47% m/m expected. The non-core component rebounded to 1.10% m/m from -0.52% m/m, after August's price control policy in the natural gas market put downward pressure on prices, seeing a rebound in September.

Looking ahead, upward pressures, highlighting increases in energy and food prices, in merchandise prices owing to inputs scarcity and logistical problems, as well as in services owing to disruptions given the greater reactivation in this sector, could maintain the upward trajectory of inflation for the remainder of the year. In this sense, analysts expect inflation to continue accelerating during the last months of 2021, closing the year above 6.0% (6.29% consensus in the Citibanamex Survey).

Within the monetary policy implications, we maintain our outlook for gradual interest rate hikes of 25 basis points during the remaining two meetings of the year, ending 2021 at 5.25% and the hiking cycle at the end of 2022 at 6.0%, around the neutral interest rate, subject to how inflation data develops over the coming months. We might expect a more aggressive stance if inflation behaves above expectations.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.