- Colombia: Consumer confidence slightly down m/m as future perceptions turn less optimistic

- Mexico: Headline inflation in August moderated as expected, but annual core inflation still on the rise; expect rate hike by end-September

COLOMBIA: CONSUMER CONFIDENCE SLIGHTLY DOWN M/M AS FUTURE PERCEPTIONS TURN LESS OPTIMISTIC

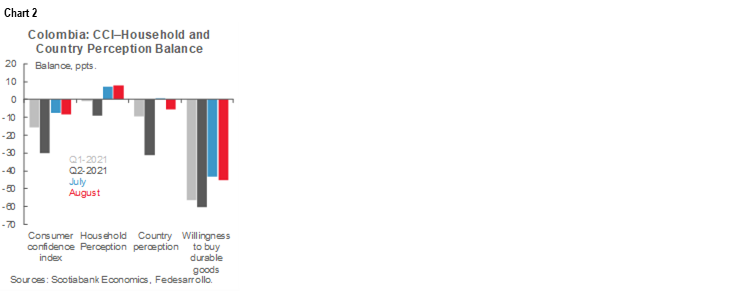

Data released by the Fedesarrollo statistical agency on Wednesday, September 8 show the Consumer Confidence Index (CCI) data for August at a balance of -8.3 ppts, declining from the -7.5 ppts in July (but above June’s -22.3). In August, as the economic reopening and social stability consolidated, consumers showed a better perception of current conditions, however, their assessment about the future eased somewhat (chart 1), likely weighted by inflation and FX depreciation and reflected in a more subdued willingness to buy houses and durable goods. Vaccination rollout continued in August albeit with some interruptions which could also have impacted optimism.

Looking at August’s details:

The Current Conditions Index rose to -29.9 ppts from July’s -31.7 ppts, its highest level since February 2020. Although consumers’ perceptions of the current situation remained deep in negative territory, recent improvements suggest that people believe that the worst of the pandemic and social unrest is over. Consumers’ appetite to buy new durable goods remained low, in fact, it deteriorated to -45.1 ppts from the -43.3 ppts of the previous month, but it is the highest level since the pandemic began (chart 2).

- The Expectations Index fell by 2.4 ppts from July’s 8.6 ppts level (chart 1, again). This index is still in positive territory reflecting improved perceptions of households’ future versus their current situation. The country assessment improved to 3 ppts versus the previous 1.8 ppts, which for now shows that concerns about next year’s general election are low. However, despite households’ expectations that better times are ahead for the country, they are not as confident about improving their economic wellbeing.

- Consumer confidence numbers improved in three of the five major cities surveyed at the regional level, with latecomer Cali now leading the gains. Medellin and Bogota are the cities with the lowest consumer confidence, where willingness to buy houses and durable goods fell, indicating some effect from the exchange rate.

- August readings varied across socioeconomic status: high-income households had the most significant decline from the +2.3 ppts to -10.1ppts, while the low-income population posted an improvement from -15.4 ppts to -9.8 ppts. Middle-income household’s confidence retreated by 5.4 ppts to -6.4 ppts.

Overall, August’s consumer confidence moderated despite a consolidation of the economic reopening. It appears that consumers are facing new challenges such as higher inflation, labour market lagging the overall economic recovery, and the FX depreciation, among others. How consumer confidence evolves will be revealing as presidential campaigns pick up the pace over the coming months. For now, consumer confidence is close to a neutral level which would support the economic recovery.

—Sergio Olarte & Jackeline Piraján

MEXICO: HEADLINE INFLATION IN AUGUST MODERATED AS EXPECTED, BUT ANNUAL CORE INFLATION STILL ON THE RISE; EXPECT RATE HIKE BY END-SEPTEMBER

According to the statistical agency INEGI, in August, headline inflation in August moderated to +0.19% m/m (chart 3) from a previous +0.59% m/m, in line with the +0.18% m/m consensus of analysts participating in the Citibanamex survey. This result came in mainly because of a drop in energy prices owing to recent price controls in the gas sector, and despite a continued monthly increase in the core component. In annual terms, headline inflation stood at +5.59% y/y, marginally below the +5.60% y/y anticipated and down from July's +5.81% y/y.

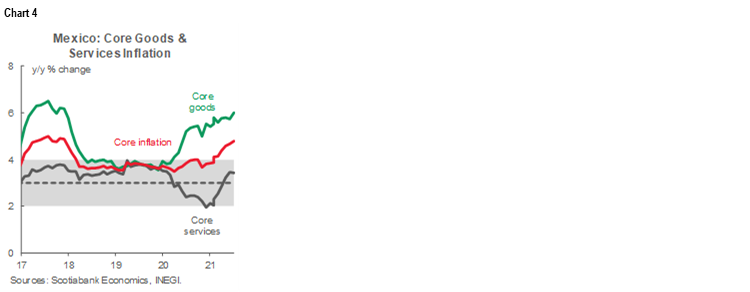

Core inflation continued above expectations although it moderated somewhat, registering a +0.43% m/m change, down from a previous +0.48% m/m in July and above the +0.42% m/m consensus. In annual terms core inflation accelerated from July’s +4.66% y/y to +4.78% y/y (chart 4), pressured by changes in the consumption dynamics favoring goods (+5.99% y/y from +5.74% y/y in July) over services (+3.43% y/y from +3.46% y/y in July) (chart 4, again), although both facing upside trends as more economic sectors reactivated owing to lower COVID-19-related restrictions.

On the other hand, non-core inflation showed some cooling signs, decreasing -0.52% m/m, driven by the above-mentioned drop in energy prices (-3.50% m/m) resulting from the government's strategy to implement price controls on domestic gas. Annually, non-core inflation again moderated from +9.39% y/y in July to +8.14% y/y in August (chart 5).

Our forecasts suggest that inflation will remain outside the monetary policy target range of 3.0% (+/-1%) for the rest of 2021 and will end the year at a level of around 6.0%, pushing the central bank to increase the monetary policy rate by 75 basis points and close the year at 5.25%. In this regard, we are anticipating that, at its September 30 meeting, Banxico will increase the benchmark rate by an additional 25 basis points to 4.75%. For the rest of the year, we anticipate that energy and food price pressures will be replaced by services price rises.

—Miguel Saldaña

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.