- Chile: Senate Commission approved fourth pension funds withdrawal; Santiago walks back reopening plan due to COVID-19 infections

- Colombia: Citi survey shows the majority of analysts expect a 25 bps hike in October’s meeting

- Mexico: Economic activity surprised on the downside in august, as services dropped amid high contagion rates

- Peru: The new Vásquez Cabinet brings new faces but government policies remain largely unchanged

CHILE: SENATE COMMISSION APPROVED FOURTH PENSION FUNDS WITHDRAWAL; SANTIAGO WALKS BACK REOPENING PLAN DUE TO COVID-19 INFECTIONS

I. Senate Commission approves fourth 10% pensions withdrawal; further debate expected

Earlier today (Tuesday, October 26), a Chilean Senate Committee (on Constitution, Legislation and Justice) approved, in the general sense, the bill for the fourth 10% pension fund withdrawal, meaning that individual articles within the law can still be debated and modified. The proposal, approved by the Lower House in late September, was approved with 3 votes in favour and 2 against, as expected. Now, the fourth pensions withdrawal bill will go to the Senate floor, where it would need a two-thirds majority to be approved (26 senators). The date of the debate in the Senate is not yet defined. If approved, the bill will go back to the same Senate Committee, to be debated and voted in particular (each individual article). Lastly, a committee made up of Lower House and Senate members would work out any differences between the House and Senate versions of the bill. The resulting bill would then return to the House and Senate for final approval.

In recent days some senators of opposition parties announced that they will vote against, putting into question the approval of the bill in the Senate. If approved, the bill will likely contain changes to limit the adverse macroeconomic effects noted by the central bank and the government.

—Anibal Alarcón

II. Santiago walks back reopening plan due to COVID-19 infections

On Monday, October 25, Chile’s Ministry of Health announced that the Santiago Metropolitan Region will take a step back in its reopening “Paso a Paso” plan. The region will move from its current “Initial opening” phase (which allows unrestricted mobility, schools, and business activity to operate with some capacity restrictions), back to “Preparation” starting on October 27. “Preparation” implies greater restrictions for some activities, emphasizing greater social distancing in restaurants and limiting the number of customers in the commerce sector.

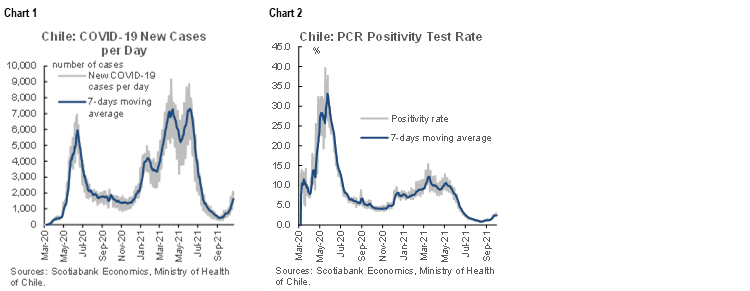

The measure is based on the rise in COVID-19 cases in recent weeks (chart 1). According to government figures, the PCR positivity test rate increased to 4% in the Metropolitan Region and to 2.7% in the whole country (chart 2). It is worth noting that Chile’s vaccination campaign has reached 90% of the eligible population, while the rollout of booster (third) doses keeps moving forward, now surpassing 5 million people.

The Santiago Metropolitan Region represents approximately half of Chile’s GDP and population. We do not expect, however, a significantly adverse impact on economic activity as a result of these new announcements, but all will depend on the evolution of new COVID-19 cases and any further changes in the “Paso a Paso” plan. For now, we are keeping our GDP growth forecast of 11.2% for this year.

—Jorge Selaive, Anibal Alarcón, & Waldo Riveras

COLOMBIA: CITI SURVEY SHOWS THE MAJORITY OF ANALYSTS EXPECT A 25 BPS HIKE IN OCTOBER’S MEETING

Colombia’s central bank (BanRep) uses this survey as one of the expectations measures on inflation, monetary policy rate (MPR), GDP, and COP.

Key points from June’s Citi survey released earlier today (October 26) include:

- Growth forecasts improved again. In 2021, the GDP recovery is expected to hit a pace of 8.71% y/y, higher than the previous survey’s 8.26% y/y consensus; it is the sixth upside revision in a row. Upside revisions came as coincident indicators (i.e. retail sales and manufacturing) have pointed to a robust economic recovery. For 2022 and 2023, economic growth expectations are relatively unchanged, for 2022 GDP growth stand at 3.69% (previous: 3.58%) and for 2023 3.27% (previous: 3.27%), respectively.

- Inflation expectations increased again for Dec-2021, although they remained anchored for 2022. October’s monthly inflation rate is, on average, expected to be 0.20% m/m and 4.78% y/y; consistent with our own expectation. In October we expect a downside impact from the VAT holiday of 8 bps. However, on the other hand, foodstuff inflation will remain high. For December 2021, the survey’s average projection is 4.90% y/y, above the previous survey expectation (4.78% y/y). By December 2022, inflation is expected to hit 3.57% y/y, slightly above the central bank’s target.

- Analysts are divided amid October’s monetary policy meeting. 17 out of the 25 analysts (68%) expect a 25 bps hike in the monetary policy rate for the October 29 meeting (Friday), while 8 analysts expect a 50 bps hike. For Dec-2021, the majority expect the monetary policy rate closing at 2.50%, in Scotiabank Economics we expect the same, while five analysts expect a close at 2.75% and six at 3%. For 2022, the median policy rate expected is 4%, in Scotiabank Economics, we expect for Dec-2022 the rate at 4.50% (chart 3).

- The USDCOP forecasts point to a slight appreciation in the currency through December 2021. On average, respondents expect a level of USDCOP 3,720 by the end of 2021 (previous survey: 3,724) and USDCOP 3,654 by 2022 (previous 3,647).

—Sergio Olarte & Jackeline Piraján

MEXICO: ECONOMIC ACTIVITY SURPRISED ON THE DOWNSIDE IN AUGUST, AS SERVICES DROPPED AMID HIGH CONTAGION RATES

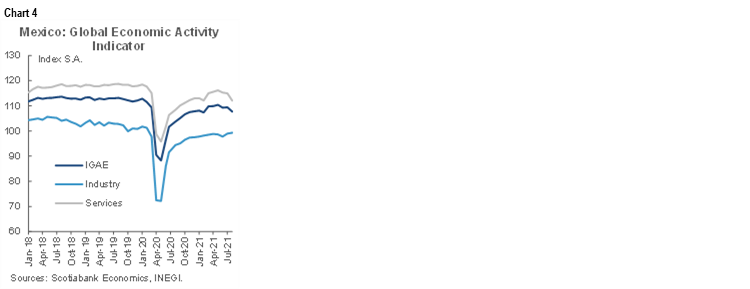

Statistical agency (INEGI) published the monthly GDP proxy (IGAE) (chart 4), or economic activity index for August, which declined more than had been expected from 0.1% m/m to -1.6% m/m (versus 0.2% m/m of consensus) measured with seasonally adjusted series. Within sectors, the industry moderated from 1.2% m/m to 0.4% m/m on a monthly basis, affected by the disruptions in value chains and input scarcity, especially in manufacturing and the automotive industry. Services fell sharply from -0.2% to -2.5% m/m, in line with the increase in contagion from the Delta variant and lower consumer confidence, although restrictions were not as stringent as in the two previous COVID-19 waves. In particular, professional services plummeted -31.4% m/m, affected by the implementation of the outsourcing reform, which limited outsourcing services and forced companies to incorporate formerly outsourced employees, although the effect was most likely statistically intensified by the subindex methodology. Retail services moderated, wholesale trade dropped, and hospitality services was the only subsector that increased in August. In September, consumer confidence advanced as contagion rates diminished notably, thus we expect better consumption conditions in services for the coming months. Lastly, agricultural and livestock activities declined -2.4% m/m from 1.0% m/m previously.

In annual comparison with n.s.a., the IGAE moderated from 7.1% y/y to 4.5% y/y, well below the expected 6.4% y/y. Thus, most likely the GDP flash figures to be released this Friday will show a q/q drop in economic activity suggesting a pause in the recovery pace. We expect services to resume their path to recovery as COVID-19-related risk decreases due to a slower pace of infections and a higher vaccination rate. Yet, uncertainty in the industrial sector could maintain some weakness in investment, below pre-pandemic levels, which could maintain a modest recovery in economic activity for the remainder of the year.

—Miguel Saldaña

PERU: THE NEW VÁSQUEZ CABINET BRINGS NEW FACES BUT GOVERNMENT POLICIES REMAIN LARGELY UNCHANGED

The new cabinet, headed by Mirtha Vásquez since October 7, stood before Congress yesterday, October 25, to present the guidelines of its government plans. This is a legal requirement every time there is a change in cabinet. Congress must then debate on whether or not to award the cabinet its vote of confidence. Yesterday’s debate was suspended, however, on news that Congressman Fernando Herrera had suffered a heart attack. Unfortunately, Herrera did not survive. The debate will not resume until Thursday, November 4.

In the past, the vote of confidence has rarely been in dispute per se, and the cabinet presentation had more to do with ascertaining the government’s policy intentions and determining how close a working relationship the government and Congress would forge. Times have changed, however, and with the polarized political environment that has existed over the past few years, the vote of confidence has become more of an issue. At the same time, the presentation continues to be useful in providing insight into policy priorities.

In a nearly two-hour presentation, Vásquez sought to appease Congress and offered to work together in good faith in favour of political stability and common economic and social goals. Much of the policy blueprint that Vásquez outlined reiterated proposals already announced in earlier occasions by President Castillo and other government officials. These included:

- Defeating COVID-19 and putting into place a series of health improvement initiatives.

- The “second agrarian reform”, consisting of the construction of irrigation infrastructure and reservoirs, and of promoting agrarian cooperatives.

- Social programs, including more transfers to households.

- Reviving the economy, including USD 871 mn in public-private projects. This is particularly interesting as this is the first time that officials of the Castillo Government have ever mentioned PPPs.

- Country-wide access to natural gas. The catch is that this would be under “contract conditions that are beneficial to the country” which ratifies the intention of modifying the contract for operating the Camisea gasfields. Later in the day, President Castillo went even further, stating that the government and Congress should work together on a law to expropriate or to nationalize (“estatizar o nacionalizar”) Camisea. Since government officials, including Castillo and Finance Minister Pedro Francke, had stated in the past that Camisea would not be expropriated, it is not clear if Castillo’s latest statement represents a change in policy or simply a lack of detail. Note that the government has never really clarified what it means by the term “nationalize”.

- Seek special powers for a tax reform. No details were given, outside of a general statement that this would be done without affecting current legal standings nor the overall competitiveness of private companies.

- Prioritize improving education, health, communications and small infrastructure investment.

- The creation of a Ministry of Science and Technology. This idea is not new, but now there is a deadline: the proposal will be ready by the first quarter of 2022.

- On education, Vásquez’ offer that schools will not be fully open until July 2022 was controversial and largely disappointing, domestically, despite the accompanying announcement that nearly PEN 600 mn will be invested in improving health conditions at schools.

- There was no clear proposal for managing social conflicts, outside of “insisting on the logic of a transformative dialogue”, which, of course, has been going on for years, if not decades, with very tenuous results. However, one announcement by Vásquez of potentially great importance for mining that was of a legal initiative currently in the works that would divide the country up in terms of what resource exploitation activities can be undertaken where. This initiative would likely reduce the areas in which new mining endeavors could take place.

- Vásquez also stated that the government was preparing a new anti-corruption plan, which will be delivered in a question of weeks.

- She also stressed that organized crime and drug-trafficking would be tackled rigorously. In terms of the drug trade, less emphasis would be given on coca crop eradication, and more effort put into contesting money laundering and drug transportation.

- Finally, Vásquez repeated the government’s commitment to do its part in the struggle against climate change; endorse regional trade treaty MERCOSUR; and seek strong relations with neighboring countries regardless of ideologies.

Overall, most of these proposals have been repeated sufficiently to give us more confidence that they truly are part of the government agenda. At the same time, however, they appear to be still a work in progress, with very little details available. Most analysts are inclined to believe that Congress will award the Vásquez Cabinet a vote of confidence, although this is not a given, and a lot can happen from now until November 4.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.