- Mexico: Annual inflation slightly above expectations in first half of October; consensus for year-end CPI now higher

- Peru: New cabinet to seek confidence vote on Monday (October 25)

- Chile: President Piñera reappoints Mr Mario Marcel as Governor of the Central Bank

MEXICO: ANNUAL INFLATION SLIGHTLY ABOVE EXPECTATIONS IN FIRST HALF OF OCTOBER; CONSENSUS FOR YEAR-END CPI NOW HIGHER

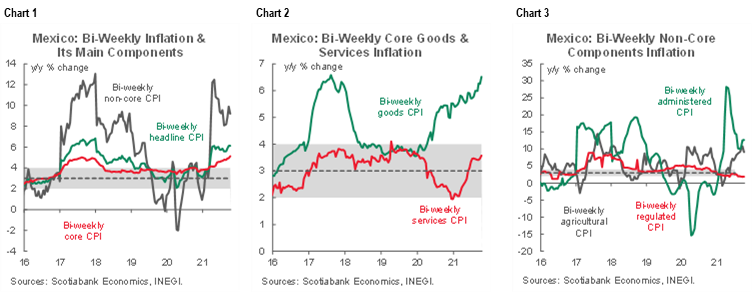

According to statistical agency INEGI, in the first fortnight of October, annual headline inflation stood at 6.12% y/y from a previous 6.13% y/y (chart 1), slightly above the 6.10% y/y of the Bloomberg consensus. Core inflation continued facing upward pressures, going from 4.93% y/y to 5.12% y/y. In particular, merchandise prices rose to 6.51% y/y from 6.25% y/y previously (chart 2), and services came in at 3.58% y/y from 3.46% y/y previously (chart 2, again). Non-core inflation decelerated from 9.89% y/y to 9.21% y/y, as the increase in energy prices from 12.61% y/y to 12.67% y/y was offset by some moderation in food items from 10.81% to 9.10% (chart 3).

In its sequential biweekly comparison, price dynamics maintained an upward trend, going from 0.21% 2w/2w to 0.54% 2w/2w (versus 0.51% 2w/2w consensus in the Citibanamex survey). By components, core inflation exceeded the 0.22% 2w/2w consensus, by rising from 0.13% 2w/2w to 0.33% 2w/2w owing to increases in both merchandise (0.37% 2w/2w) and services items (0.28% 2w/2w). Non-core inflation rose strongly, from 0.44% 2w/2w to 1.18% 2w/2w, as energy edged up sharply to 3.77% 2w/2w.

We also highlight a strong increase in inflation expectations for the end of the year, which the consensus estimate is now at 6.46% y/y, up from 6.29% y/y previously. In terms of monetary policy, we maintain our outlook of 25 basis point increases at the central bank’s upcoming two meetings in 2021, to end the year at a rate of 5.25% (current is 4.75%) and conclude the hiking cycle in 2022 with a terminal rate of 6.00%. With some risk of a more aggressive pace of hikes, our view could change, depending on the upcoming data on inflation for the rest of the year.

—Miguel Saldaña

PERU: NEW CABINET TO SEEK CONFIDENCE VOTE ON MONDAY (OCTOBER 25)

Peru’s new Cabinet headed by Ms Mirtha Vásquez will formally address Congress on Monday, October 25. The procedure is a requirement whenever there is a change of cabinet. The new Vásquez Cabinet was sworn in on October 6. The cabinet presentation before Congress tends to be more than just a formality. In the past the event has helped clarify the new cabinet’s agenda, and has shed light on the type of relationship the government may expect to have with Congress. Both issues are in play now as well.

The priorities of the new cabinet have already been outlined in a list made public on October 16. This list does not differ significantly from President Castillo’s inauguration speech or former Cabinet Head Bellido’s address to Congress. The focus continues to be on health and COVID-19; getting the economy back on track; maintaining fiscal and monetary stability; creating a new Ministry of Science and Technology; digital access and inclusion; giving priority in State resources to regions outside of Lima; strengthening the democratic system, promoting cultural diversity, and fighting corruption, among other issues. Although the cabinet address is not likely to go into too much depth, it could shed new light on what to expect in terms of State management and policy.

Although the cabinet has frequently helped clarify the relationship between the government and Congress, a positive vote of Confidence by Congress was, for a long time, largely a foregone conclusion. This has changed over the last five years, and now, once again, to give or not to give the cabinet a vote of Congress will be a Shakespearian dilemma for many members of Congress. The main point of contention revolves around the new Minister of the Interior, Luis Barranzuela, who was evicted from the police service on the basis of disciplinary action and more recently worked as an attorney defending Mr Vladimir Cerrón, the leader of ruling party Peru Libre, as well as a number of other party members, whom he would now be in charge of detaining if so instructed by the courts. Members of Congress are calling foul due to a conflict of interest. The vexing dilemma they face is deciding whether or not to give their backing to Ms Vásquez, widely seen by political stakeholders as an improvement over former Prime Minister Bellido, and at the same time have to accept Barranzuela as a result.

Meanwhile, social conflicts are multiplying. Three major conflicts involving blocking roads and highways have erupted in recent days: 1) at the Las Bambas copper mine; 2) in communities in the rainforest protesting against oil production activities; and 3) among coca leaf producers. The latter is a new development unlike the former two conflicts which have been recurring, however, it is unusual that three major protests should occur simultaneously and some analysts argue this could reflect an expectation among some that the Castillo Government presents an opportunity to obtain greater concessions. However, the conflicts appear to have caught the government off guard, and it is not clear just how the government will deal with these situations.

—Guillermo Arbe

CHILE: PRESIDENT PIÑERA REAPPOINTS MR MARIO MARCEL AS GOVERNOR OF THE CENTRAL BANK

Earlier today (Friday, October 22), through a press release, President Piñera reappointed Mr Mario Marcel as Governor of the Central Bank to a new 5-year term, a position he has held since December 2016 when he replaced Mr Rodrigo Vergara. The appointment does not require consultation with the Senate.

Although part of the market awaited the appointment of current Board member Rossana Costa to become the first woman Governor of the Central Bank in replacement of Mr Marcel, the decision to extend his mandate has been positively valued by the market, in a context where the independence of the Central Bank will be discussed by the body in charge of drafting the new Constitution. In February 2022 the mandate of Board member Joaquín Vial is due to end.

—Aníbal Alarcón

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.