- Chile: Congress discusses fourth pension withdrawal

- Colombia: Moody’s affirms the country’s Baa2 rating and raises the outlook from “negative” to “stable”

- Peru: Cabinet shuffle but political challenges remain; mining output and investment recovered in August

CHILE: CONGRESS DISCUSSES FOURTH PENSION WITHDRAWAL

On Wednesday October 6, discussions on the fourth withdrawal of pension funds began in the Senate commission on the constitution. The pension regulator, the central bank as well as the finance minister will review the expected impacts on inflation, interest rates, among other issues in coming days. A key issue to be addressed is whether to postpone the discussion of withdrawal of funds from insurance companies, given the risk of insolvency that regulators have warned about and the greater complexity of the discussion. Our expectation is that a new withdrawal is unlikely to be similar to the previous ones in view of the greater clarity of the macroeconomic and financial effects that it could have. In this respect, adjustments to the bill could be made to mitigate potential collateral damage.

—Anibal Alarcón

COLOMBIA: MOODY’S AFFIRMED THE COUNTRY’S BAA2 RATING AND RAISES THE OUTLOOK FROM “NEGATIVE” TO “STABLE”

On Wednesday, October 6, Moody’s affirmed Colombia’s rating at Baa2 (two notches above investment grade threshold) and improved the outlook from “negative” to “stable” (table 1). Moody’s emphasized that the track record of prudent macroeconomic management and capacity to build consensus as a positive aspect. They also underscored that this capacity arose even in the middle of social tensions. Additionally, the international rating agency highlighted that fiscal reform approved in September will support debt stabilization and that the stable outlook assumes that future administration will continue committed to fiscal sustainability.

That said, Moody’s still sees Colombia’s debt metrics as compatible with Baa2 rated peers. They expect the debt-to-GDP ratio to reach 68% in 2021, in line with the deterioration observed in peers countries. Prospects for economic growth are positive, however, with the gap versus 2019 activity to be closed in 2021, making Colombia one of seven countries (in a total sample of 19 in Baa rating) to accomplish this in 2021.

Balance of risks:

On the positive side, Moody’s said Colombia would be upgraded if the government achieves a downward trend in debt-to-GDP metrics, addressing structural fiscal challenges such as a narrow revenue base and expenditure rigidities. On the negative side, Moody’s would downgrade Colombia if the debt-to-GDP ratio continues to increase and if the country becomes more reliant on external debt to finance the current account deficit.

Our take:

We think yesterday’s Moody’s decision is a positive surprise since improving the outlook affirms the confidence in the strong institutional framework Colombia has constructed. Regarding risks, we expect the economic recovery to continue, with upside potential for better than expected performance, which would translate to stronger fiscal results (lower deficit). On the external side, we consider the widening of the current account deficit over the last year to have been led by the public sector deficit; however, this dynamic could reverse should FDI rebound in the H2-2021 amid the better macroeconomic environment. These factors will continue reducing the risk of a downgrade in the medium term.

—Sergio Olarte & Jackeline Piraján

PERU: CABINET SHUFFLE BUT POLITICAL CHALLENGES REMAIN; MINING OUTPUT AND INVESTMENT RECOVERED IN AUGUST

I. New episode of political tension culminates in cabinet change

On October 6, President Castillo announced the resignation of the Chief of the Cabinet, Guido Bellido. This is one more step in distancing himself from the official Peru Libre party. The president appointed Mirtha Vasquez, Former President of Congress during the Sagasti Administration, as new Chief of Cabinet. She has a left-wing profile, but is not considered a radical, so her appointment could lead to a drastic change with respect to the tone that Bellido had established. Vasquez’s appointment should improve relations between the Executive and Congress, given her congressional experience. This would be an important turnaround amid recent political tension with Congress. President Castillo also replaced 6 ministers out of a total of 19, drawing on individuals with more technical profiles for productive sectors such as Energy and Mining, and Industry. The Minister of Economy, Pedro Francke, was confirmed in office, as was expected. In social sectors, President Castillo made changes to the Education, Culture, Labour and Interior portfolios, calling on individuals who accompanied him in the electoral campaign (Education), members close to the Peru Libre party (Labour and Interior), and human rights activist (Culture).

Various parties and political analysts reacted favourably to the appointment of the Vasquez Cabinet, as they believe that it will help reduce tension, although the official Peru Libre party disagreed with the appointment. This could be interpreted as a good sign, although it could open a new source of political tension, mainly within Congress.

Guido Bellido as Chief of the Cabinet for the last two months and representative of the left-wing linked to Vladimir Cerrón, Head of the official Peru Libre party, played a destabilizing role, with contradictory messages and confusion that exacerbated political uncertainty. He recently made the Camisea gas field negotiation conditional on its nationalization if the Camisea consortium—made up of Pluspetrol, Repsol, Hunt Oil, among others—did not agree to pay more taxes. Negotiations were scheduled to begin this Wednesday, but were abruptly postponed by the government. Bellido also supported the ex-Minister of Labour, Iber Maraví, who was questioned in Congress for his links with terrorism, when questioned by Congress under a motion of “confidence” (which could lead to a political impasse if Congress presented a motion of no confidence to the minister).

Support for President Castillo weakened during the first two months of government. Nearly 61% of the population believe that President Castillo does not have the leadership capacity to solve the country’s problems, according to an Ipsos poll. The Cabinet changes announced yesterday could help address this perception. However, political issues remain. In this respect, the government’s bill on the “question of trust”, a mechanism used by the Executive to require cabinet approval by Congress, is outstanding. Meanwhile, the official party Peru Libre, continues to collect signatures in favour of a referendum on a Constitutional Assembly.

Social conflicts with mining companies have also been a recurrent issue and will be the first challenge the new cabinet faces. MMG Ltd., operator of the Las Bambas mine, had to suspend production for a few days owing to a road blockage that prevented the transportation of the mineral. Although the company reached an agreement with the community, another community that uses the same transport route has announced other road blockade protesting against the Antapaccay mine operated by Glencore. Finally, the northern Peruvian oil pipeline, which has also suspended its operations due to social protests.

In financial markets, a short-term correction in the PEN, which has largely reflected political tensions (chart 1), could be possible after reaching a record level of 4.14 last week.

—Mario Guerrero

II. Mining output and investment recovered in August

Mining (metals) output increased 5.1% y/y in August. Production is still 6% below pre-pandemic (August 2019) levels. This is the fifth consecutive month that production has risen, with tin (23%), silver (23%), gold (14%), iron (13%), lead (6%), copper (4%) and molybdenum (3%) contributing to higher production levels, while decreases in the production of zinc (-4%) attenuated the rise. In July, the Mina Justa mine started producing, with commercial production (181,000 TMF) expected in 2022.

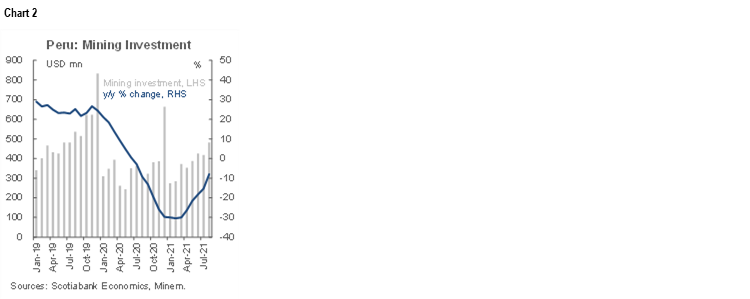

Mining investment increased 60% y/y in August (chart 2). However, investment was 10% lower than August 2019 because, while the megaprojects Quellaveco by Anglo American and Ampliación Toromocho by Chinalco continued to lead investment, the flow of investment spending is decreasing as they are near to end their construction. Both projects are expected to start production in 2022. Smaller projects such as Pampacancha by Hudbay, Ampliación Santa María by Cía. Poderosa and Ampliación Shouxin by Minera Shouxin are expected to sustain some investment going forward.

—Katherine Salazar

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.