FORECAST UPDATES

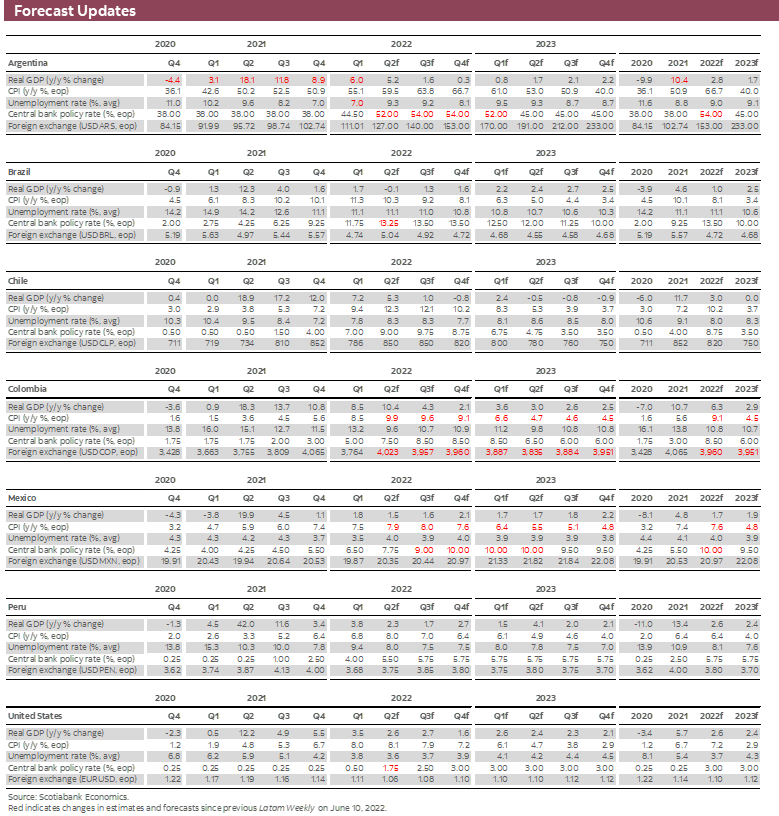

- Aggressive policy rate hikes by the Fed and other advanced economy central banks, with signals of more to come, have led Scotiabank economists to revise their projections. See the full set of changes in the forecast tables below.

ECONOMIC OVERVIEW

- With the election of leftist candidate Gustavo Petro in Colombia’s June 19th presidential run-off, there is a Quadfecta of populist presidents in the Pacific Alliance.

- A key mandate of these presidents is a better distribution of income. In this respect, they resemble past populist Latam governments whose macroeconomic programs typically hurt the very groups that they were intended to benefit.

- There is reason to believe, however, that the current wave of populist macroeconomics differs from earlier programs featuring dirigiste economic policies and ultimately led to macroeconomic imbalances with fiscal and/or exchange rate crises.

- The new populism seeks to achieve income redistribution through targeted income transfers while preserving the benefits of macroeconomic stability.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

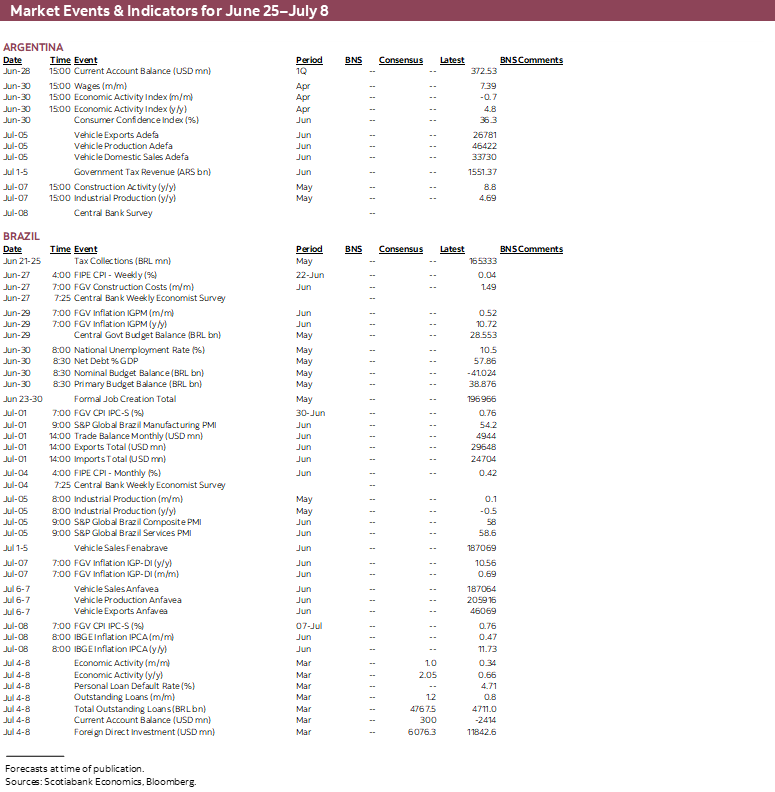

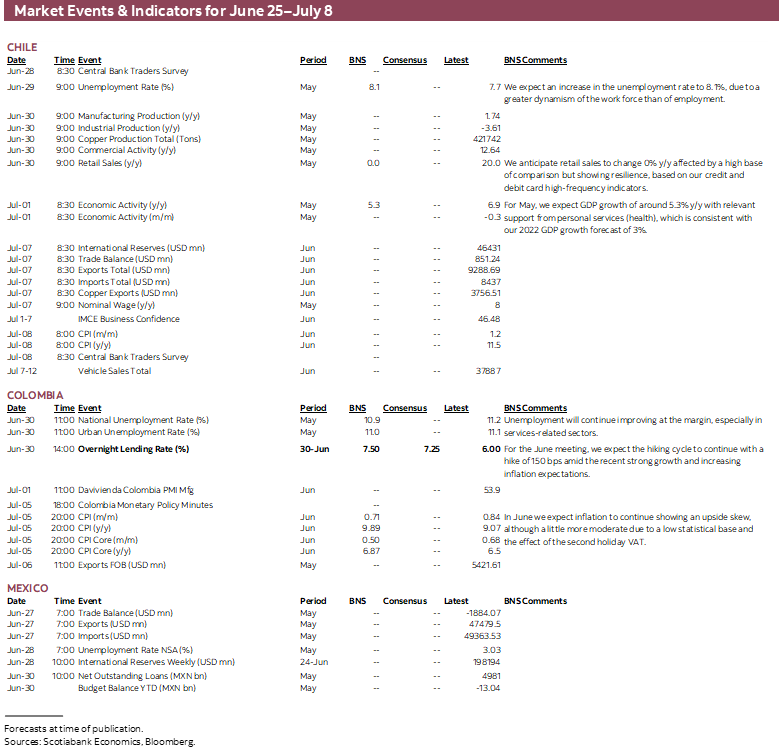

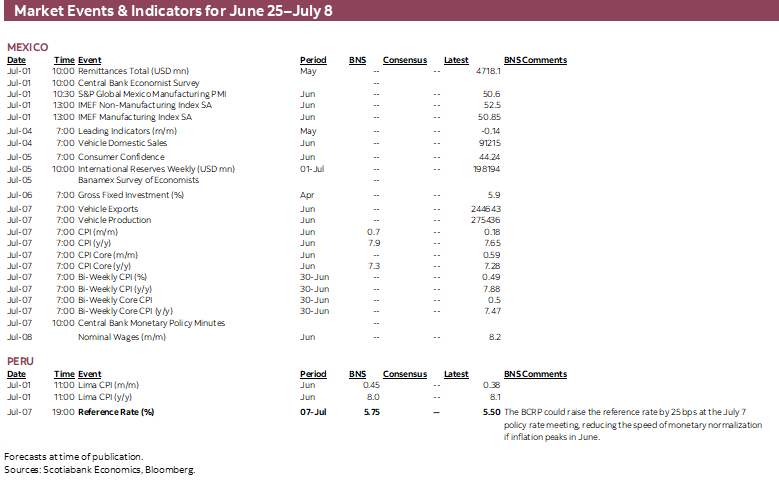

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period June 25–July 8 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: The Times They Are A-Changin’

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- The election of a Quadfecta of populist presidents in the Pacific Alliance naturally raises questions regarding economic policy frameworks and strong institutions that have characterized much of the Latam region for the past two decades.

- A comparison of recent populist macroeconomic programs with “classical” populist policy regimes suggests the “times are a-changin’.” While both episodes share similar initial conditions—discontent with the status quo—more recent populist economic programs have embraced the importance of avoiding large macroeconomic imbalances that ultimately lead to inflation and fiscal and/or exchange rate crises.

- This eschewal of macroeconomic tools to achieve real wage gains means that governments do not need to rely on dirigiste economic policies or high tariffs to guard against the steady accumulation of price pressures or erosion of foreign exchange reserves.

- Instead, redistribution can be pursued through targeted income transfers to the poorest. Such policies may promote economic growth and political stability by growing the middle class, both of which can have important benefits for domestic residents as well as foreign investors.

POPULIST MACROECONOMICS OLD AND NEW

Bob Dylan’s iconic protest song, “The Times They Are ‘A-Changin’,” captured the zeitgeist of the mid-1960s and the battles then being waged over civil rights in the US. It has a line—“for the loser now, will be later to win”—that could well be invoked in the Latam political scene today. Over the past few years, presidential elections in the region have produced administrations of a decidedly populist hue. And while the policy details differ, the common denominator of these governments is a promise to address poverty and elevate the downtrodden. In some respects, this trend harkens back to earlier decades when the region was known for dirigiste economic policies and high inflation.

In stark contrast to most countries in the region, however, Colombia had traditionally been remarkably impervious to populist policy regimes. The June 19th election of the leftist candidate, Gustavo Petro, thus came as something of a surprise, notwithstanding polls showing that outcome was possible—if not likely. Coming on top of last week’s announcements of more aggressive tightening by the Fed and other advanced country central banks, which shook financial markets, the election has focused attention on Colombia and the region more broadly.

The purported goal of populist governments is to achieve a better distribution of income, such that the gains from economic growth are more widely shared. The objective is undoubtedly laudable. But it is not always achieved. In fact, as two prominent economists, Rudiger Dornbusch and Sebastian Edwards, warned 30 years ago, after surveying the experience of the previous half-century or so, the hard truth is that “... populist policies do ultimately fail; and when they fail it is always at frightening cost to the very groups that were supposed to be favored”. [Dornbusch and Edwards, The Macroeconomics of Populism, University of Chicago Press (1991)] They acknowledged the role of external shocks in undermining populist economic programs, but argued that the extreme vulnerability that makes destabilization possible is usually the result of unsustainable domestic policies. Their conclusion begs the question of whether today’s wave of populism will fare any better—whether well-intentioned policies to foster development, address poverty, and reduce inequality will succeed.

The starting point to answering those questions is to assess the extent to which current populist programs share key characteristics with the failed efforts of the past. Dornbusch and Edwards identified three key features of populist macroeconomics.

The first feature is the initial conditions. Dissatisfaction with the economy’s performance, the feeling that things can be better, creates fertile soil in which macroeconomic populism can grow. This is coupled with a highly uneven income distribution that creates a political and social problem, cultivating support for a radical or heterodox approach to economic policy.

The second characteristic of populist macroeconomics is summed up in just two words—no constraints. According to Dornbusch and Edwards, macroeconomic populists circa 1990 explicitly rejected the relevance of resource constraints on macroeconomic policy and downplayed the risks of sustained deficit finance. In this perspective, expansionary fiscal and monetary policies are not inflationary (with a stable exchange rate) because spare capacity and decreasing long-run costs contain cost pressures, while price controls can always be deployed to squeeze profit margins.

The third element highlighted by Dornbusch and Edwards is what could be labelled the “three R’s” of populist macroeconomics: reactivation, redistribution (of income), and restructuring (of the economy). In short, the policy prescription is to use macroeconomic policies to redistribute income, typically through real wage increases that are not to be passed on into higher prices. And if inflation does develop, real depreciations (devaluations) are avoided to prevent the erosion of living standards and because of a conviction that they will not have a positive impact. Instead, the economy is restructured—often a euphemism for increased protectionism—to conserve foreign exchange and support real wages and higher growth.

So how does the current wave of Latam populist macroeconomics compare with earlier versions? To start, the two episodes clearly share similar initial conditions. Across the region, there is today a wellspring of dissatisfaction with the persistence of high inequality and grinding poverty as in earlier decades; this dissatisfaction has provided a base for populist politics. In Chile, for example, that underlying sense of discontent likely fueled demands for social change and constitutional reform, which Scotiabank’s team in Santiago point out could have important implications for the conduct of macroeconomic policy going forward. Some progress has been made in reducing inequality (as measured by a Gini index) over the past two decades, but in most countries the decline has been very gradual.

At the same time, the fact that greater progress has proven elusive despite the broad-ranging structural and macroeconomic reforms, many of which were introduced in the 1990s and early 2000s, may have increased the appeal of populist macroeconomics. These reforms fostered macroeconomic stability and removed a plethora of price (and other) distortions, creating conditions conducive to long-term investment and growth; yet there may be a perception that not all have shared in the benefits, with those at the bottom of the income distribution left behind. The current inflationary environment reveals the fallacy of this proposition: those most affected by high inflation are poorly paid workers in the informal sector who have seen their real wages eroded by steep increases in the prices of key commodities. Nevertheless, the persistence of inequality and high poverty remains a major challenge.

What about the second element of populist macroeconomics, the “no constraints” feature? In earlier decades, macroeconomic policy-making was broadly characterized by the prevalence of fiscal dominance. This is a situation in which sustained large fiscal deficits, incurred in pursuit, for example, of high real wages, deflect central banks from the goal of inflation control. In effect, central banks are relegated to the subordinate role of financing government spending. And though not all past cases of fiscal dominance led ineluctably to hyperinflation, some did. (Meanwhile, Venezuela provides a contemporary example.)

While pre-1990 populist macroeconomics may have explicitly rejected the relevance of key resource and financial constraints, this does not seem to be the case today. Thanks to reforms introduced over the past 20 years, central banks in the Latam region now have greater operational independence and explicit inflation-targeting mandates. It is fair to say that these innovations constitute a revolution in economic policymaking; the success of which has been truly remarkable. In fact, regional central banks proved to be far more proactive in addressing nascent inflation threats from so-called “temporary” inflation over the past year than their advanced economy peers. In any event, armed with explicit inflation-targeting frameworks and operational independence, central banks are less susceptible to fiscal dominance by spendthrift governments.

Equally important, the central banking revolution would likely not have been successful if governments had not coordinated with their central banks. Governments across the region also adopted fiscal rules to anchor spending and ensure sustainable public finances. This longer-term perspective with an emphasis on fiscal probity yielded important benefits, including lower borrowing costs as international ratings agencies and foreign investors recognized the reduced risk of a fiscal crisis. (And as the late Doug Purvis drilled into us in grad school, a bond held by a foreign investor is a claim on domestic production. The more you transfer to foreign bondholders, therefore, the less that is available to domestic citizens.) The adoption of a longer-term approach to fiscal policy also broke the pattern of pro-cyclical fiscal responses that had long plagued the region, in which fiscal policy was stimulative in periods of economic expansion and contractionary in periods of economic recession. Needless to say, the result was an amplification of the cycle—growth spurts followed by economic crashes.

The importance of this long-term approach to fiscal sustainability is clear in the fiscal responses to two large, and in some sense unprecedented, external shocks. Fiscal policy responses in most Latam countries were counter-cyclical in both the global financial crisis and, more recently, the pandemic. In both cases, measures were introduced to support the most vulnerable and shield the economy from the shock to external demand. Those responses were made possible by the conscious (or implicit) rejection of the “no constraints” paradigm that characterized previous episodes of populist macroeconomics.

Moreover, governments remain committed to fiscal rules and ensuring debt sustainability. Across the region, fiscal balances that deteriorated sharply as pandemic supports were rolled out are now on the mend. Notably, while the evidence is preliminary and limited, it seems that the biggest rebounds in public finances are in countries that provided the largest support packages either by way of direct fiscal support or through access to pension fund savings. (Admittedly, as the Scotiabank team in Lima have noted, in the case of Peru, this may be the unintended effect of an inability to successfully execute public investment projects.) And while it is too early to say with any certainty what the Petro administration in Colombia will do, there are grounds for optimism, given his technocrat background and training in economics, that he too will reject the “no constraints” paradigm.

The third feature of earlier populist macroeconomics identified by Dornbusch and Edwards is the three R’s. For the most part, governments in the region have eschewed efforts to raise living standards using the blunt tools of macroeconomic measures to run a “hot” economy, the reactivation “R”, even while pursuing redistribution objectives, the second “R”. In Brazil, for example, former-President Luis Ignacio Lula da Silva’s bolsa familia program used targeted income transfers to elevate the incomes of the poorest. His policies were designed not to generate inflation or major macro disequilibria. The same could also be said of Ricardo Lagos and Michelle Bachelet in Chile as well as others in the region.

Because they have avoided the large macro imbalances that ultimately lead to fiscal or exchange rate crises, new populists have generally not adopted dirigiste measures. Such policies, including price controls and steadily rising tariffs, were needed in the past to suppress incipient inflation or prevent the loss of foreign exchange reserves that would in time lead to an exchange rate crisis. Nor has there been a wholesale retreat from the increased integration with the global economy that has marked the past two decades, including through free trade arrangements with advanced economies and regional initiatives, the most important being the Pacific Alliance initiative. Similarly, there is little talk of large-scale restructuring of the economy (the third “R”), which in the past was often associated with higher tariffs and an increased degree of autarky. (Though recent Mexican measures with respect to the energy sector may dampen foreign investment and bear close monitoring.) In short, policymaking in the Latam region has been remarkably consistent over the past two decades, despite the emergence of a new populism.

The conclusion that emerges from this review is that today’s wave of economic populism differs from earlier (or classical) populism in one critical respect: it recognizes that resource and financial constraints are important; that it is impossible for “the loser now to later win” in the midst of a fiscal or exchange rate crisis. In this regard, the times really may be a-changin’. Should that indeed be the case, the encouraging takeaway is that the lessons of the past have been learned.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—CLP Depreciation: Beyond External Factors

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

COVID-19 SITUATION IN CHILE

The daily number of confirmed COVID-19 cases has continued to increase in recent days. The test positivity rate rose to 14%. For now, however, occupancy rates of ICU beds and COVID-19-related death rates are stable at low levels. Meanwhile, the vaccination campaign has reached 92.6% of the eligible population. The rollout of booster (third) doses continues—reaching 14.9 million people—and the new booster dose (fourth) is in progress—with 8.9 million people covered. Overall, mobility is stable at high levels in June, which will continue supporting the economic activity, mainly services.

NEW CONSTITUTION IN PROGRESS

On Monday, July 4, the constitutional convention will deliver the final text of the new constitution after it is reviewed by the preamble, harmonization and transitory norms commissions. President Boric will then call for an exit referendum, to be held on September 4. While polls currently show more people in favour of rejecting the new constitution (46% according to the Cadem poll), we expect a tight result.

For now, the harmonization commission incorporates into the text the work of the transitory norms commission, which was completed in mid-June and adds 57 articles to ensure a gradual implementation of the new constitution. Among other articles, the commission added the supermajorities needed to reform the text of the constitution. These are four-sevenths until March 2026 for all articles except for “substantial” matters, which must be approved by referendum or by a two-thirds majority in both chambers.

CLP BETWEEN 900–920 COULD TRIGGER FOREIGN EXCHANGE INTERVENTION

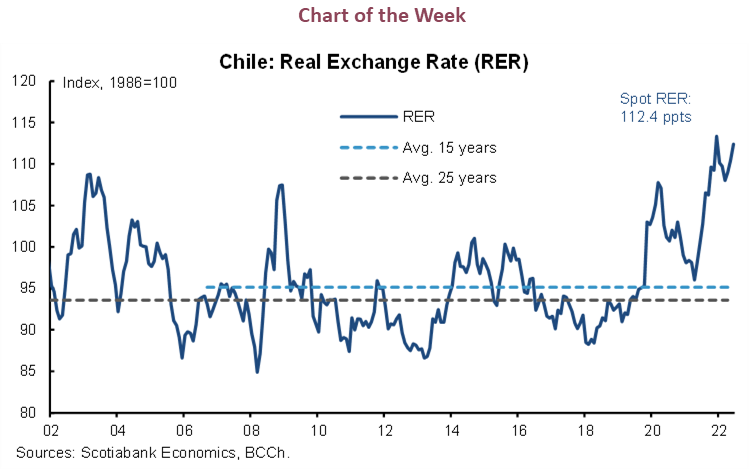

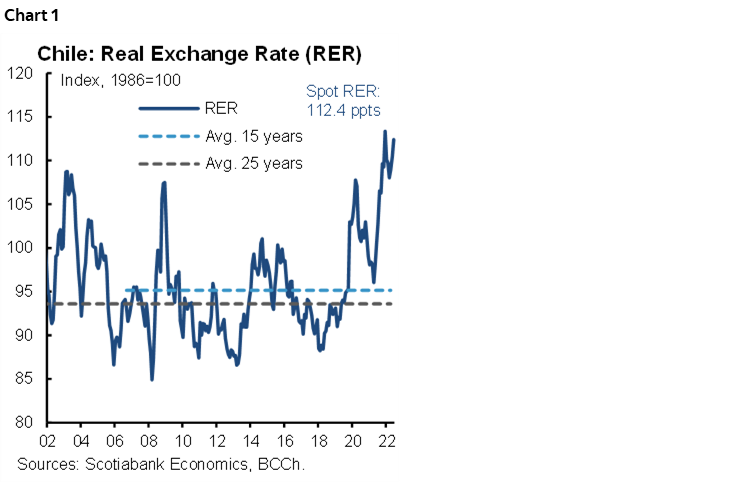

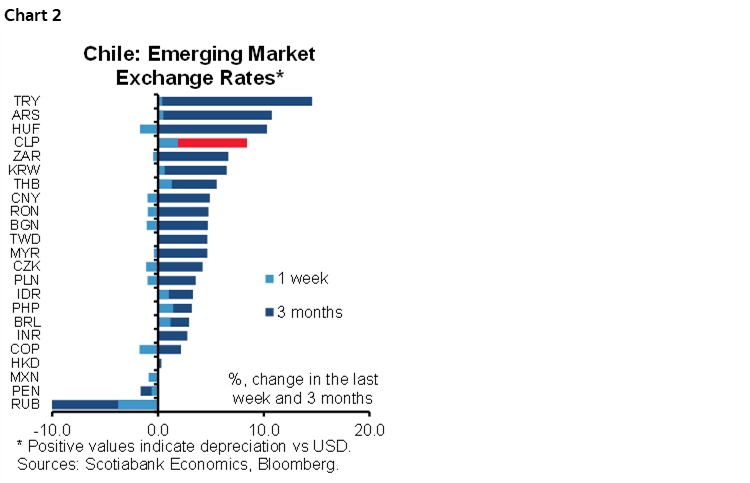

The Chilean peso (CLP) has experienced a steady depreciation against the US dollar since April 2022, recently exceeding CLP 880. For many, this reflects the appreciation of the US dollar in the wake of an accelerated rate of policy normalization by the Federal Reserve. In our view, however, there is an idiosyncratic component in the CLP depreciation that is evident in a real exchange rate (RER) that in June reached its second highest level since the floating exchange rate regime was implemented in 2001 (chart 1). We estimate the RER around 112.4 points in its base measure (1986=100), just 1% below the level reached in December 2021 in the middle of the second presidential round, despite the increase in external prices and recent high inflation abroad.

The depreciation of the CLP goes beyond external factors and is driven by higher domestic political uncertainty and portfolio balance factors. Simple models to determine the CLP point to a misalignment since October 2019 (social unrest) of between CLP 70–100 with respect to traditional determinants. More recently, the CLP has been subject to an increased level of misalignment, even after controlling for political uncertainty. In fact, the misalignment becomes evident when we observe that the CLP is among the currencies with the greatest depreciation against the US dollar in recent days (chart 2).

CLP depreciation has not been accompanied by short-term liquidity problems as in the past. The on-shore spread with external interest rates remains stable for all terms, suggesting that the CLP depreciation is not responding to the absence of foreign currency or exchange rate mismatches. However, we cannot rule out the possibility that, prior to the exit referendum for the new Constitution on September 4, there may be episodes of foreign currency illiquidity that may require central bank intervention to avoid the undesired increases to the cost of sovereign financing.

Meanwhile, pension fund administrators (AFPs) are not cushioning the unwinding of carry trades. Short-term foreign investors have been betting in favour of the CLP since the beginning of 2020. With some temporary easing, the NDF position was in positive territory earlier this year, but since April it has started to unwind, coinciding with a more aggressive stance by the Fed regarding the evolution of inflation. This unwinding, which brings with it the purchase of USD forward, has not been contained despite the improvement in the interest rate differential. Equally worrisome has been the diminished buffering role of AFPs that have not been big sellers of USD in the face of a modest shift in contributors to conservative funds. A similar phenomenon, although somewhat more intense, occurred after the social unrest, where external and local movements towards the purchase of USD (spot and forward) exacerbated the depreciation of the CLP.

Arguments have already been made in support of foreign exchange intervention or other measures to mitigate the idiosyncratic depreciation of the CLP. However, the success of these measures is not assured. Even though traditional indicators to assess the adequacy of international reserves (IR) give mixed messages, albeit with a slight positive bias, there are insufficient reserves to conduct a large-scale intervention in the event that the central bank opts for a direct sale of dollars in the spot market.

In our view, if the CLP depreciates towards 900–920 through end-June, the central bank would likely move faster than expected at July’s monetary policy meeting in raising rates and implement a foreign exchange intervention coordinated with the Ministry of Finance (micro/macroprudential measures). In this scenario, we do not rule out an accelerated USD liquidation process to finance the fiscal spending committed for the rest of the year.

A LOOK AHEAD

In the next fortnight, the central bank will release May GDP growth on July 1. For its part, the statistical agency (INE) will publish the unemployment rate for the quarter ending in May to be released on June 29), the economic activity by sector (on June 30), and the CPI for June, on July 8. In addition, as we mentioned above, the constitutional convention will deliver the final text of the new constitution to President Boric on July 4.

Colombia—Post-Election Economic Opportunities and Challenges

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Maria Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

Colombia held the second round of presidential elections on June 19 in which the leftist candidate Gustavo Petro was elected with 11.28 million votes, 50.44% of the total. The turnout was 58.09% (22.66 million votes), above the level of 54.91% observed in the first round and the strongest participation observed since the 1998 elections (62.59%). The new administration will begin its mandate in an economy with a strong institutional framework and with economic and social challenges that intensified in the pandemic. A pragmatic government will be key to forging consensus with Congress.

In his first speech as President-Elect, Petro called for a national agreement and dialogue to build consensus toward the goal of a peaceful society with social and environmental justice. In his remarks, President-Elect Petro recognized that he does not have a strong majority in Congress and will need to seek a consensus on most of his proposals, which for us means that the strong institutional framework that has been established in Colombia will prevail, reducing the probability of sudden changes in key policy frameworks.

What are the strengths and challenges of Colombia's economy? And what are the upcoming milestones to keep an eye on?

Colombia has robust political institutions buttressed by independent economic institutions such as the central bank that should ensure prudent macroeconomic management and, as the fiscal rule remains a target anchor, we expect the new government to act according to these policy rules.

At the same time, the new president inherits challenges and high expectations. During the pandemic, poverty and inequality increased. On the fiscal side, the new president must ensure the consistency of existing programs with fiscal sustainability. That said, notwithstanding the Medium-Term Fiscal Framework that shows Colombia on track to achieve its fiscal goals earlier than expected, ensuring this consistency, and achieving these goals, will require the new government to pare back some social programs and increase fiscal revenues. All of the above make us think that before proposing new social programs, fiscal reform is necessary.

In this respect, the finance minister will thus have the difficult task of moderating expectations and reconciling them with current fiscal constraints. We think any of the current candidates for finance minister will maintain markets’ confidence and have the capability to negotiate with the very diverse Congress. As part of the potential fiscal reform, the President-Elect is expected to reduce tax exemptions, especially in the corporate sector, and increase the base for individual wealth taxes. Moreover, the new government is likely to avoid changes to the VAT to contain social discontent. The major challenge will be to resist pressures to dilute the ambitious proposal to raise COP 50 tn (5% of GDP) in new fiscal income when the bill eventually passes through Congress. In the same vein, increasing gasoline prices is an upside risk for inflation but one that is necessary to avoid further fiscal liabilities.

On the monetary policy front, the new government will have the opportunity to change two board members until 2025; that said, we maintain our expectation of an independent central bank acting in line with traditional rules, and a hiking cycle reaching a terminal rate at 8.50% in July 2022.

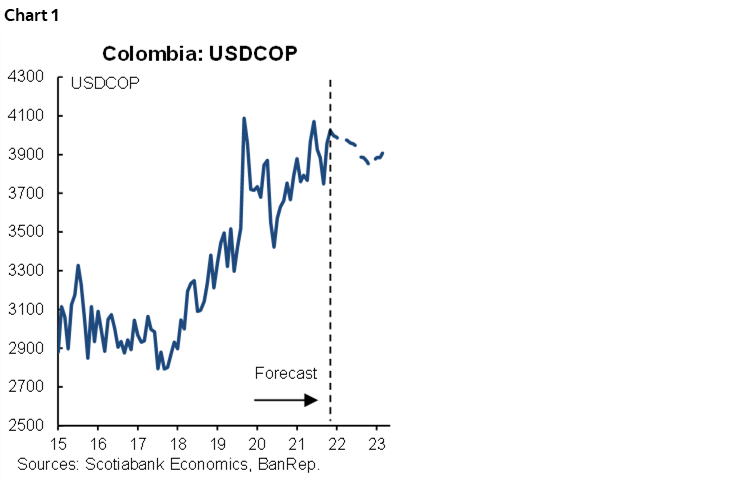

Regarding markets, the presidential results point to new information that impacts our current FX projection. On the Tuesday after the elections, the FX reversed the gains shown after the first round, indicating that a new premium was structurally priced in the USDCOP. As a result, we revised our forecast FX path for 2022 and 2023 (chart 1). We now expect the exchange rate to hover around 3,980 pesos in the second half of 2022 and around 3,900 in 2023. Despite high commodity prices, we think that a stronger US dollar from Fed tightening and some degree of political risk premium will prevent the FX from appreciating significantly in the medium term.

Mexico—Banxico Needs to Remain Hawkish on Rates

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

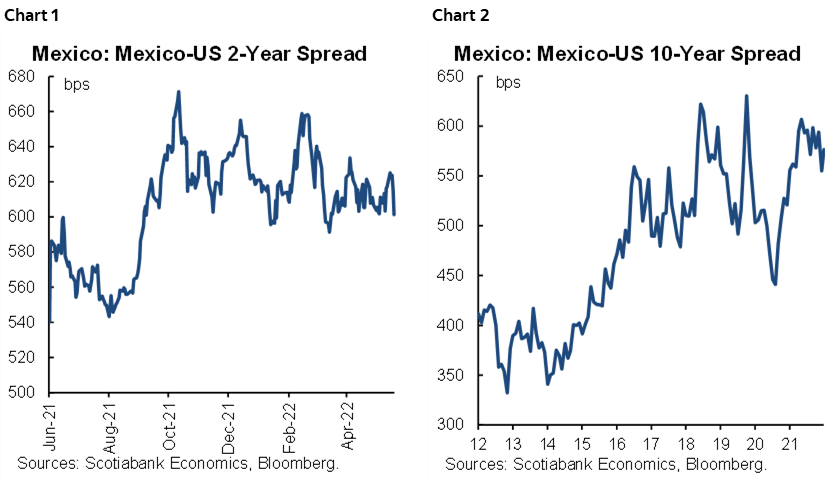

Over the past few years, the spread of the Mexican yield curve over its US counterpart has widened from around 400 bps to roughly 600bps (charts 1, 2). The spread widening kicked off gradually back in 2015 and consolidated at its current levels around 2018, maintaining a spread about 200 bps wider than its previous levels. Using the country’s CDS as a proxy for credit premium, today’s credit spreads are broadly consistent with the levels we saw before the widening started. This, in turn, suggests that the bulk of wider spreads is explained by rising FX/inflation premium (the total spread should be the sum of credit, inflation/FX and liquidity premium).

This finding has direct implications for monetary policy. In particular, for the next policy meeting, we expect Banxico to match the Fed’s policy rate actions to maintain a spread advantage in the policy rate, which has thus far helped anchor MXN in a volatile global market environment. In fact, even when USTs had a single-day 30 bps spike ahead of the last FOMC meeting, the beta of m-bonos to USTs remained near 1:1. This was a positive signal of resilience given that Mexican markets are typically not so robust in response to such violent moves in core markets. We expect Banxico to remain prudent, helping to anchor domestic markets.

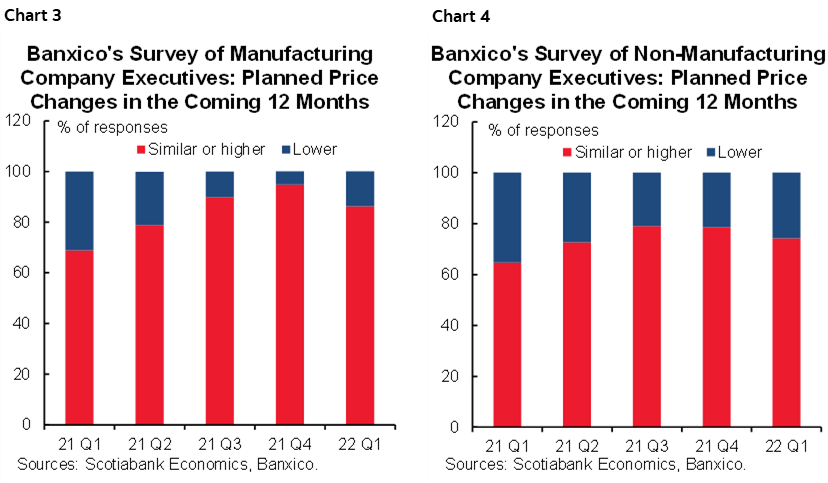

At the same time, there is some good news on the inflation front. In the latest Banxico survey of company executives’ plans for price changes in the coming 12 months, the share of executives who plan to increase their prices at a similar or faster pace declined somewhat relative to the previous quarter (charts 3, 4). The share of manufacturing sector executives planning similar or faster increases is 86% (down from 94%), and in the service sector the share that plans similar or faster increases is 74% (down from 79%).

Despite the positive signal, however, pricing intentions remain an overwhelmingly upward risk to inflation in Mexico, which we believe warrants a continued hawkish stance by the central bank—in addition to the need to preserve the spread relative to the Fed which we discussed above. In this respect, the latest Banamex survey of private expectations saw yet another upwards drift in expected 2022 inflation, with consensus now looking for 7.05% year-end inflation (5 bps higher than the previous print). The consensus expectation for 2023 also moved 5 bps higher, to 4.43%. We expect inflation will peak in Q3-Q4 but will remain relatively sticky to the downside.

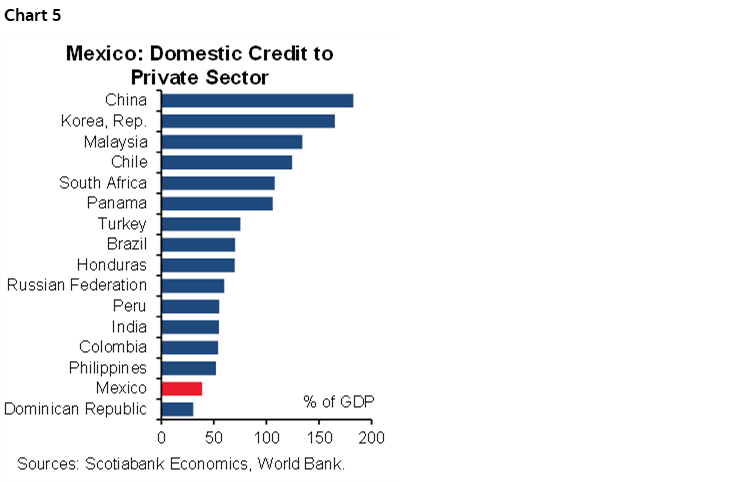

Another reason why we believe caution from Banxico is warranted, is the relatively shallow transmission channel Mexico has for monetary policy. Even by emerging market standards Mexico has abnormally low financial sector penetration (credit/GDP near 40%), which means that rising rates have a much shallower channel to affect the economy than in countries with comparable income levels (chart 5). This makes Banxico a central bank that is not well-placed to “chase inflation”. We therefore expect Banxico to continue to at least match the Fed’s hiking pace over coming months.

Peru—BCRP not Quite at the End of its Rate Hike Cycle, Amidst Ambivalent Growth Signals

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Richard Avila, Analyst

+51.1.211.6000 Ext. 16558 (Peru)

richard.avila@scotiabank.com.pe

The BCRP produced its quarterly Inflation Report and presentation on Friday, June 17. There are two features that we would like to highlight. The first is that the BCRP expects inflation, currently at 8.1% yearly, to peak in July. The second is that the BCRP lowered its GDP growth forecast for 2022 from 3.4% to 3.1%, narrowing the gap with our own forecast of 2.6%, (it maintained its 2023 forecast at 3.2%). These two features, taken together, suggest that the BCRP could be leaning towards ending its cycle of reference rate hikes sooner rather than later.

We perceive two reasons why the BCRP could hold the view that inflation will peak in July. One is that the comparison base will be higher beginning in July. Monthly inflation in the last six months of 2021 averaged 0.68%, compared to 0.36% in the first half. If monthly inflation remains at, or is lower than, the 0.63% level registered in the year-to-May, then inflation should start to decline to some degree. The second reason we believe the BCRP expects inflation to turn is that it could conceivably be expecting global commodity prices to stabilize. This already appears to be happening already for several commodity imports that are key for Peru, including wheat and edible oil inputs, as well as container and freight costs. But, oil and gas, which is the most important imported commodity for the country, is another story. Whether the BCRP inflation expectations are met or not will largely depend on the uptrend in global oil prices stalling or reversing. This factor will, therefore, also determine whether the BCRP will be able to end its reference hike cycle as soon as it would like.

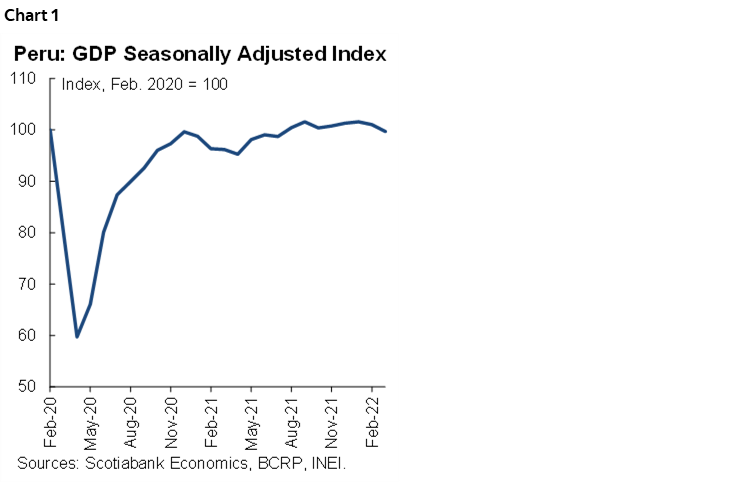

The BCRP appears to be showing increasing concern regarding growth. GDP growth for January–April was 3.8%, y/y. The BCRP’s full-year 2022 forecast of 3.1% would require that growth fall well below 3.0% for the remainder of the year. We expect something similar. Part of the reason is that moderate y/y growth in the year-to-date continues to reflect a rebound from an economy hampered by mobility restrictions last year, and this rebound will not last. Note also that growth was rather more disappointing in m/m terms, falling for the second consecutive month in April (-1.0%) following a -1.3 m/m drop in March (chart 1).

The counter argument here is that there will be an inflow of resources from pension fund withdrawals beginning in July that may amount to as much as 2.5% to 3% of GDP. It is not easy to determine how much of this will actually flow into the economy through consumption, as opposed to going into savings or used to reduce household debt, but it ought to stimulate consumption, nonetheless. This inflow should help to counter the impact of inflation, on real household income levels.

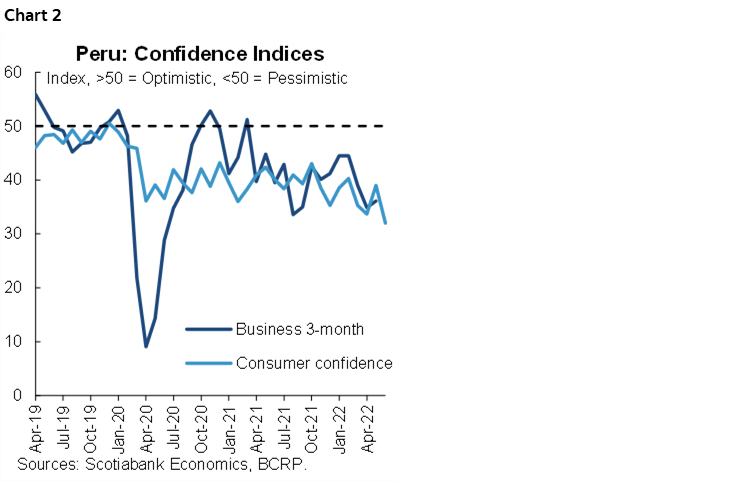

The backdrop to this growth scenario is copper prices, which are starting to appear as an emerging risk. Copper prices dropped below the USD4/lb level on June 22nd for the first time since early 2021. Although there is plenty of room for metal prices to decline further before macro accounts are jeopardized, the downtrend could reinforce the sense of malaise in the country attributable to prolonged political uncertainty and affect business and consumer confidence, which are already in the doldrums (chart 2).

The PEN has tightened its range to 3.70 to 3.80 in June, showing strength that is somewhat surprising, but very welcome given global inflation. This relative PEN strength may not last if copper (and other metal) prices continue to decline.

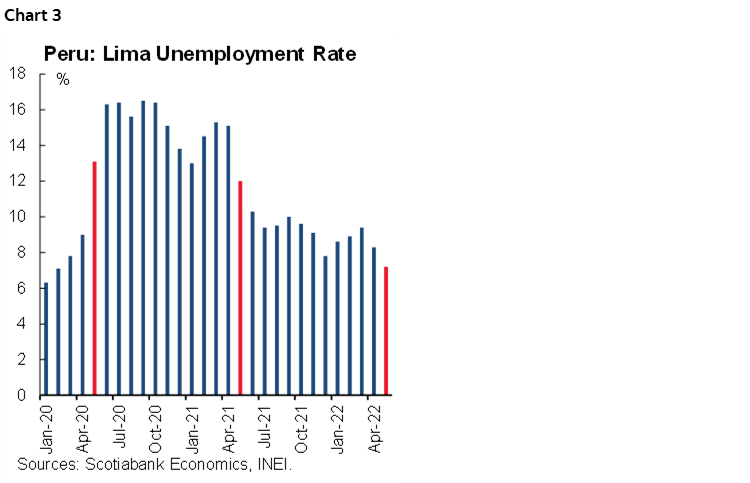

Employment has been a pleasant surprise recently. Unemployment in Lima fell to 7.2% in May, down from 8.3% in April, and from 9.4% in Q1- 2022 (chart 3). Mining and agroindustry led in jobs growth. Agroindustry is easy enough to understand, as the sector has been expanding non-stop for some time now. As for mining, one may assume that employment growth is linked to the new Minas Justa and Quellaveco projects coming on stream.

On the political front, the government continues to navigate several increasingly notorious corruption investigations. And yet, there does not appear to be any short-term danger of an impeachment of President Castillo. There are, however, two points of interest. One is the government’s position regarding the recent Summit of the Americas. Unlike other leftist regimes, Peru did not protest the absence of Cuba, Venezuela and Nicaragua from the Summit. Instead, what stood out was the photo op that President Castillo—wearing a business suit (no necktie, however)—took with President Biden. In foreign policy at least, the Castillo Regime does not seem interested in aligning itself with the other leftist governments of the region. The second topic of interest is that in just over a month the Castillo Regime will have completed a full year, and it will be very intriguing to see what messages he will give in his yearly address. This should provide us with an idea as to what his second year in office may look like, and how it may differ from his first year.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.