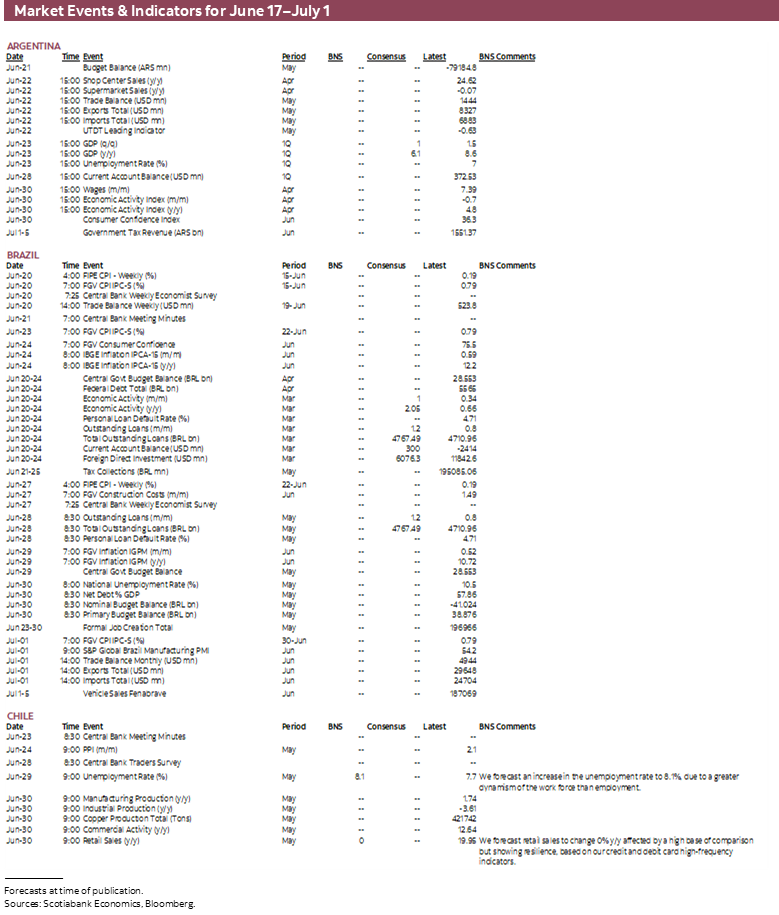

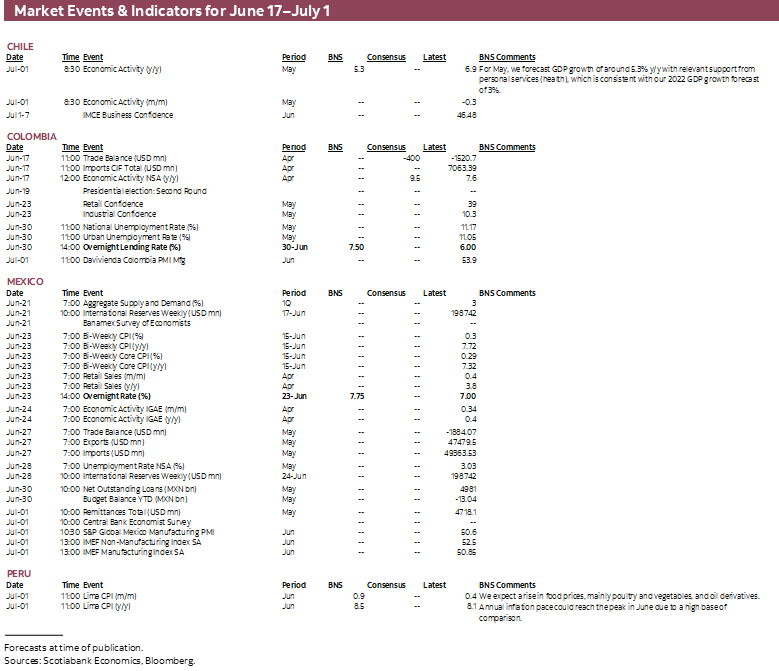

- Fed tightening highlights a week in which advanced economy central banks accelerated the pace of tightening and/or signaled more aggressive actions to rein in inflation and prevent inflation expectations from becoming unmoored.

- The initial market reaction to the Fed’s 75 basis point hike was “dovish,” as the Fed burnished its price stability credentials. But a subsequent large bearish decline and increased volatility in markets suggests the Fed has its hands full convincing markets that a soft landing is still possible.

- For the Latam region, market gyrations translate into less favourable external financial conditions, which increase the premium on sound policy frameworks and strong institutions.

Well, if not the world, then financial markets. The past week saw some dramatic moves by key central banks as markets looked into the eyes of a bear. The Fed’s 75 basis point rate hike and more aggressive communications, signalling the possibility of another 75 bps move, certainly caught the market’s attention. As Scotiabank’s Derek Holt pointed out, however, the initial market reaction was surprisingly dovish. That response followed earlier sharp downward movements in financial markets, reflecting growing pessimism that a so-called soft landing, in which the Fed succeeds in returning inflation to target without triggering a recession, is becoming progressively less likely.

For the Latam markets (and emerging markets around the globe), higher advanced economy interest rates, coupled with skittish investor risk appetite, make for a less favourable financial environment, albeit one that the region has managed through with considerable poise. Past editions of the Latam Charts and Latam Weekly have noted that central banks in the region have been proactive in fighting inflation; indeed, they have led their global peers. In this respect, an interesting counterfactual to consider is what financial conditions would be had Latam central banks temporized with price pressures as others have done.

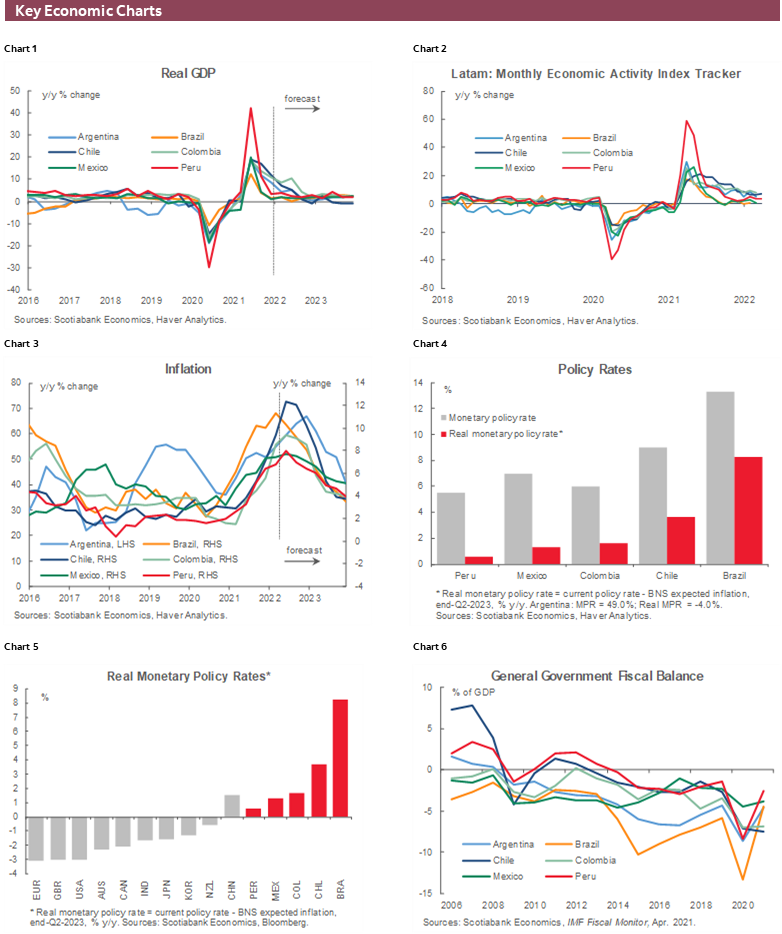

KEY ECONOMIC CHARTS

Regardless of this alternative scenario, and the growing external risks, it is apparent that the regional recovery remains on track. Scotiabank teams expect real GDP growth to moderate to pre-pandemic levels (chart 1), as output and employment levels return to where they were before the pandemic struck. The latest prints—economic activity in Colombia, GDP in Peru—are consistent with this trend. Nevertheless, the risks to this outlook have increased and high-frequency monthly activity indicators (chart 2) should be closely monitored for nascent signs of a stalling economy.

High inflation continues to persist across the region, with headline inflation running above central banks’ inflation targets (chart 3). But strong commitments to price stability, coupled with the policy actions already taken and the additional steps that have been telegraphed, lead our country teams to anticipate a gradual return of inflation to target over the coming year. With the policy rate hikes Latam central banks have put in place, policy rates are now positive in real (after inflation) terms, significantly so in Brazil and Chile (chart 4). In this regard, the proactive response by the region’s central bankers stands out in comparison to their global peers (chart 5).

At the same time, the strong economic rebound in 2021 and continued growth in 2022 have been instrumental in bringing down large pandemic-related deficits (chart 6). Fiscal outcomes in Peru have been especially impressive, though possibly inadvertent as the government investment has atrophied. Colombia’s public finances have likewise improved significantly, with it now appearing that the country is on track to return to its medium-term fiscal anchors much faster than anticipated.

Improved fiscal outlooks should help the region weather the financial storms that may be brewing in global financial markets. Lowering debt-to-GDP ratios (chart 7) and reducing external debt burdens (chart 8) would provide a confidence boost to investors anxiously watching external financial conditions. Moreover, sound public finances would also rein in large current account deficits (chart 9) in Chile and Colombia and help bolster international reserves that serve as a buffer to external shocks.

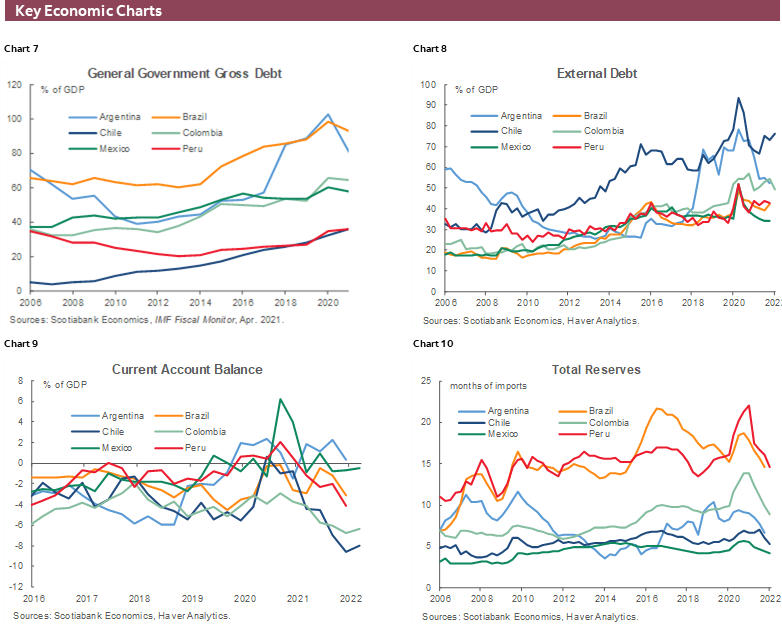

KEY MARKET CHARTS

Despite the shared financial shock of an appreciating US dollar, growing concerns of recession, and continuing geopolitical tensions, regional financial markets have performed reasonably well through the first half of 2022. Most currencies are up against the USD since the start of year (chart 3), though the strength of the dollar has clearly weighed on Latam currencies more recently. And while many regional equities markets are down on the year, these movements should be viewed in the context of volatile global markets (4). That is not to say, however, that there aren’t risks to price into financial assets. Political and policy uncertainty remains across the region, with constitutional drafting in Chile, a presidential election in Colombia, concerns with respect to policy changes that could dampen foreign investment in Mexico and continuing political machinations in Peru. Such uncertainty may be reflected in exchange rates (chart 5) and CDS spreads on Latam sovereign bonds (chart 6), which have waxed and waned in response to indications of greater or lesser uncertainty.

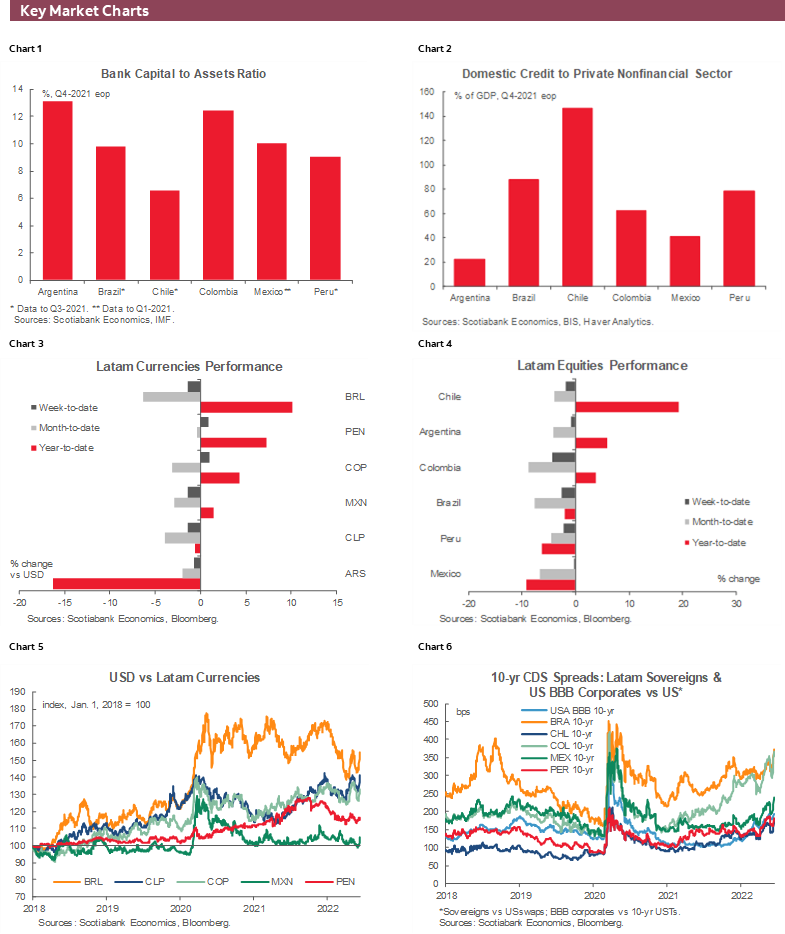

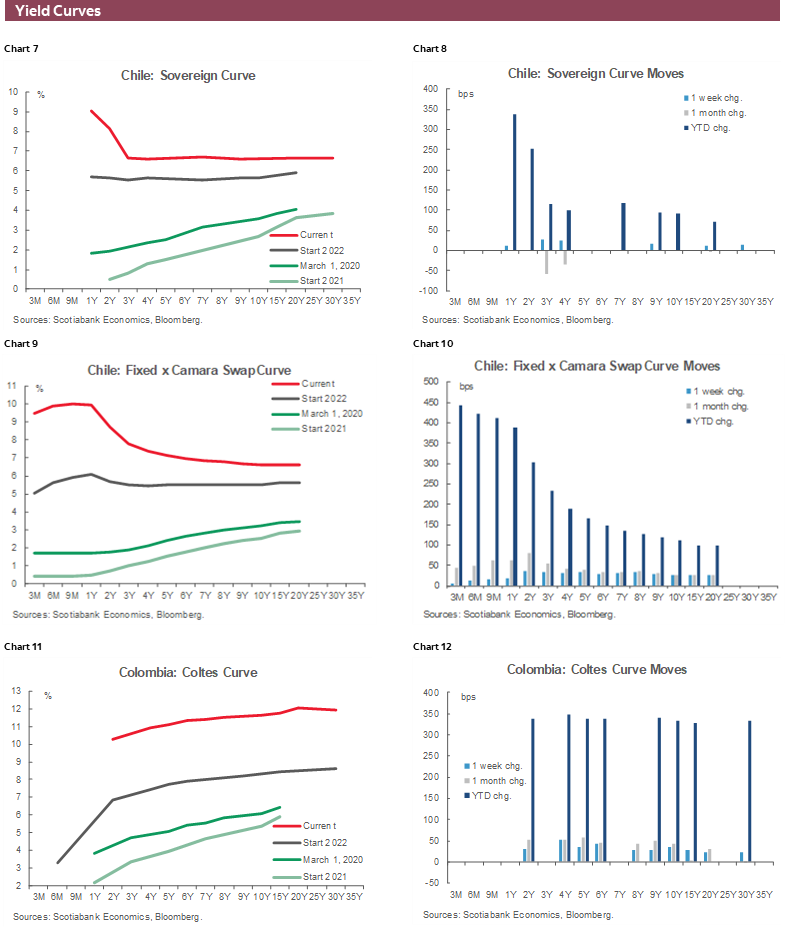

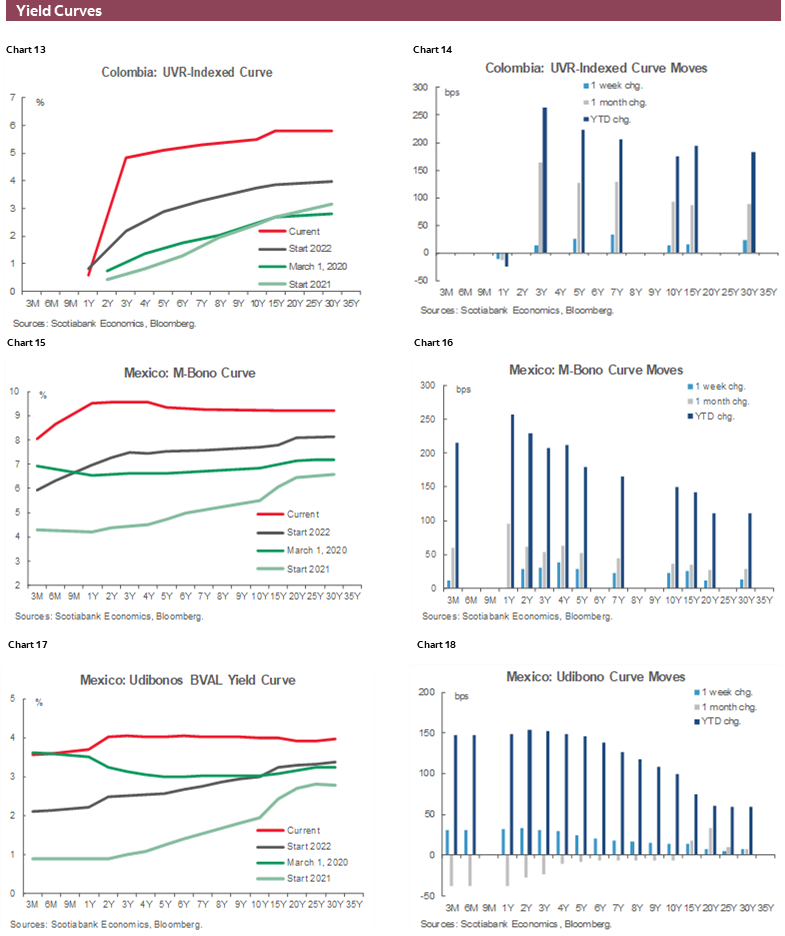

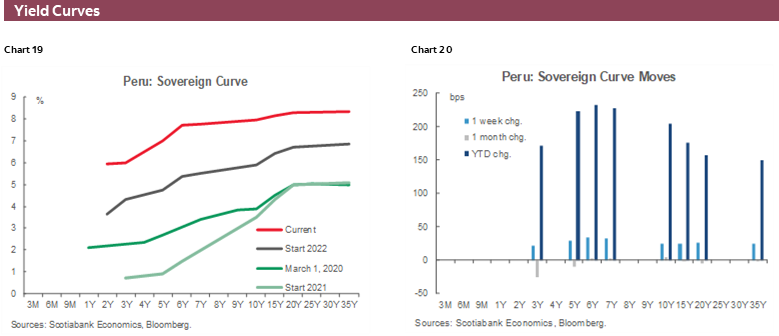

YIELD CURVES

Most yield curves across the region are now inverted or flat (charts 1–20). As noted in previous editions of the Latam Charts, this could be an early indicator of recession, albeit one that should not be given inordinate weight. Colombia and Peru are the exceptions here, as they have been through the yield curve inversion in other Latam countries.

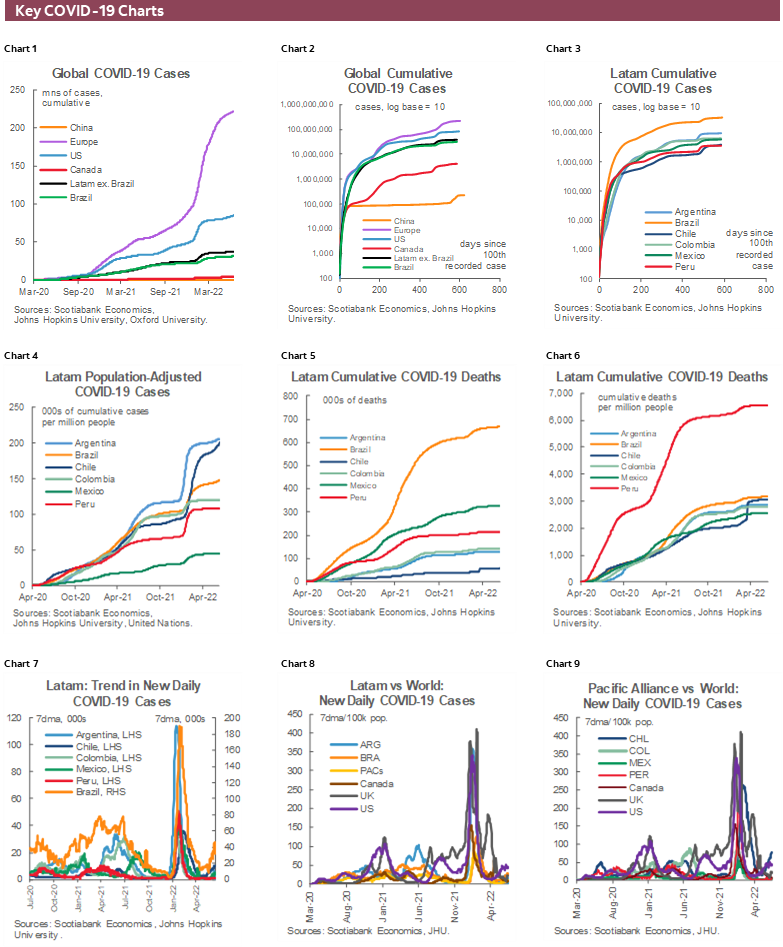

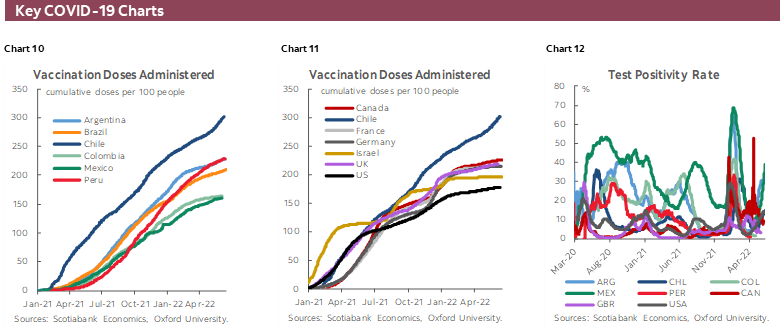

KEY COVID-19 CHARTS

Jurisdictions around the world are easing masking and vaccine requirements as the COVID-19 virus fades from public consciousness, if not public health concerns. Key monitoring charts for what remains a potential threat to public health and economic health are provided below.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.