- Colombia: Medium-Term Fiscal Framework, a guideline for the next government

COLOMBIA: MEDIUM-TERM FISCAL FRAMEWORK, A GUIDELINE FOR THE NEXT GOVERNMENT

On Tuesday, June 14 Minister José Manuel Restrepo presented the Medium-Term Fiscal Framework (MTFF), which provides the clearest insights into the government’s thinking about the country’s current fiscal outcomes and long-run economic prospects. The MTFF gives a general perspective on the key factors influencing the main fiscal goals and their sustainability over a ten-year perspective. Minister Restrepo highlighted that Colombia is achieving its long-term goals earlier than anticipated, with financing dynamics likely to normalize at faster pace than expected, as reflected in a lower projection of debt requirements in 2023.

Our take is that, despite the optimistic outlook, the new government will still have a challenge to achieve the path projected in the MTFF-2022. A critical challenge concerns the gasoline price stabilization fund, especially as regards the best timing to reduce the subsidy to avoid a larger deficit, increasing gasoline prices. In our perspective, fiscal reform is needed to achieve the optimistic projections presented in the MTFF in terms of fiscal income and to support fiscal expenditures, which in terms of percentage of GDP are not retreating to pre-COVID-19 levels.

All in all, we think the MTFF is credit positive. However, the international environment will be difficult amid FED tightening, which will dominate FI sentiment. In structural terms, it will be key to see if the new government provides continuity with respect to the current fiscal approach, especially in proposing structural fiscal reform and the confirmation of the fiscal rule as a medium-term anchor.

Key readings from the MTFF

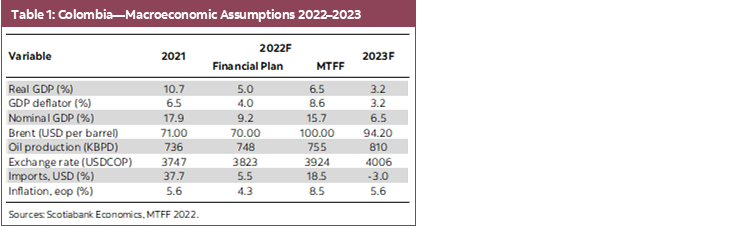

Macroeconomic assumptions (table 1):

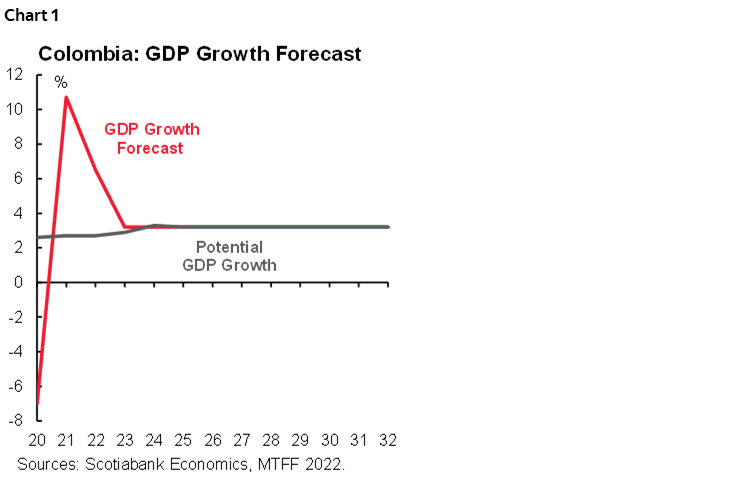

- GDP was revised to the upside from 5.0% to 6.5% y/y in 2022, while in 2023 the MoF projects 3.2% (chart 1). According to government calculations, economic growth will reflect still strong private consumption and a better investment dynamic. That said, Minister Restrepo said that the economy is recovering faster than expected, and the employment gap is almost closed.

- In 2023, the MoF expects investment to make a higher contribution to GDP along with higher exports. Meanwhile, consumption is expected to moderate to its medium-term trend. All in, by the end of 2023, Colombia’s GDP is expected to be 1.6% below the pre-pandemic trend. Minister Restrepo said that in 2023 investment in infrastructure due to the 5G projects will propel growth. Additionally, services exports, mainly tourism, will also contribute strongly.

- As the main challenge, Minister Restrepo emphasized the current account deficit, which is projected at 5.7% of GDP in 2022 and 4.5% of GDP in 2023. However, MoF estimates that the financing will be mainly through FDI (86%).

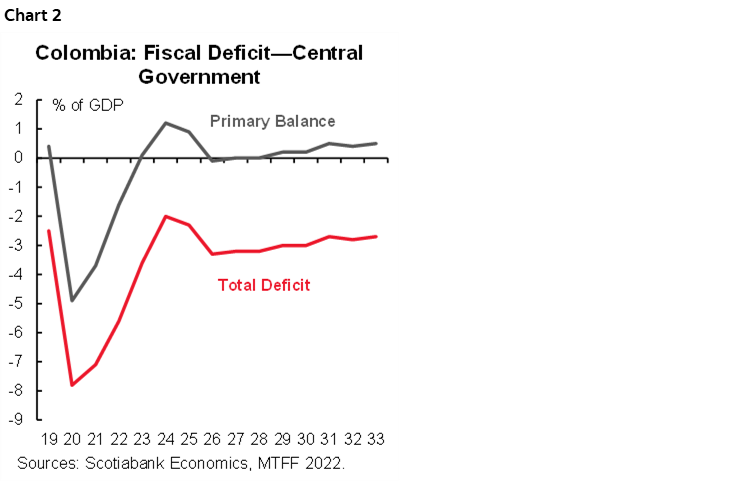

Fiscal deficit:

- The fiscal deficit target improved from 6.2% of GDP to 5.6% of GDP (chart 2). Minister Restrepo highlighted that tax collection has been stronger than expected and the target of net tax collection increased by COP 19 tn (about 1.8 % of GDP) to COP 202.4 tn in 2022. That said, fiscal deficit reduction will be 1.50 ppts as compared to the previous year, the largest reduction in 30 years.

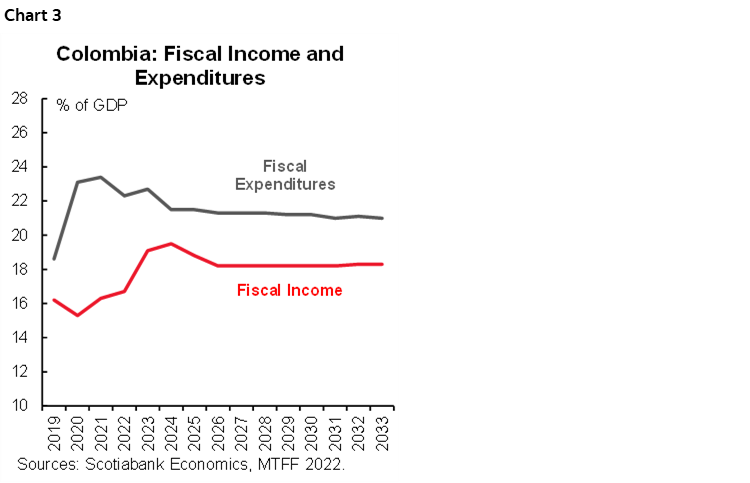

- Starting in 2023, fiscal income is expected to increase significantly as the effects of the fiscal reform approved in 2021 (chart 3) kick in. Fiscal expenditures are likewise expected to remain well above pre-pandemic levels at around 21% of GDP, but it is not clear if the new government will allow some temporary expending programs created during the pandemic to expire.

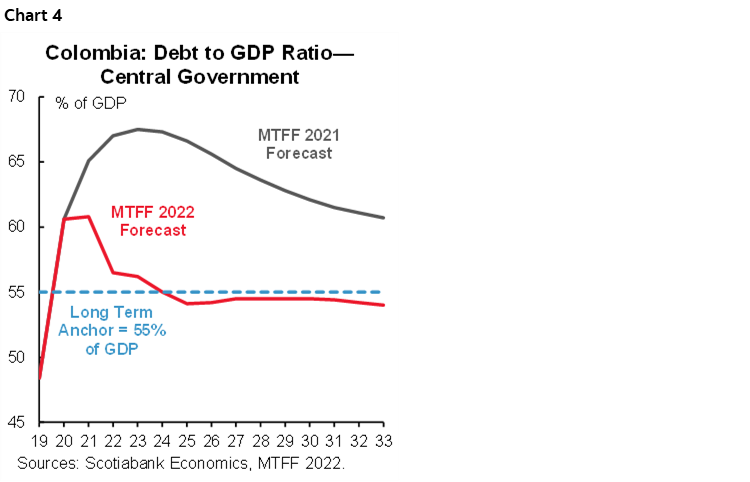

- In terms of debt, 2022 is expected to close with the debt-to-GDP ratio at 56.5%, close to the long-term anchor of 55% of GDP (chart 4), which was not expected to be achieved until 2033.

Gasoline Price Stabilization Fund

- The government will pay COP 14.2 tn of the current fund’s deficit. It will, however, propose a new rule to adjust gasoline prices gradually, making them compatible with international prices, as well as the schedule of payment. Implementation will depend on the new government. Having said that, there is a discussion around gradual increases of the gasoline prices as soon as in July to start to close the gap with international prices. If this happens, inflation could close 2022 above 9.5%.

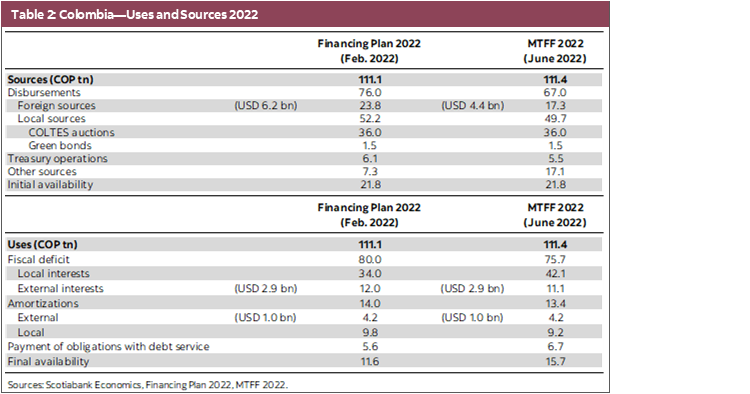

Financing plan 2022 (table 2):

- A favourable outlook and higher tax collections in 2022 are contributing to a moderation in financing requirements.

- On the international side, financing will be reduced, especially on the expected issuance of global bonds, which now would hover around USD 1.6 bn, while multilateral financing will remain expected at USD 3.2 bn.

- Local sources are expected to finance COP 49.7 tn. TES issuances would total COP 36 tn under the MTFF, with green bonds auctions expected at COP 1.5 tn.

- Looking ahead, the government expects to close the year with a higher cash buffer than was projected in the Financing Plan (COP 15.7 tn versus the previous estimate of COP 11.61 tn).

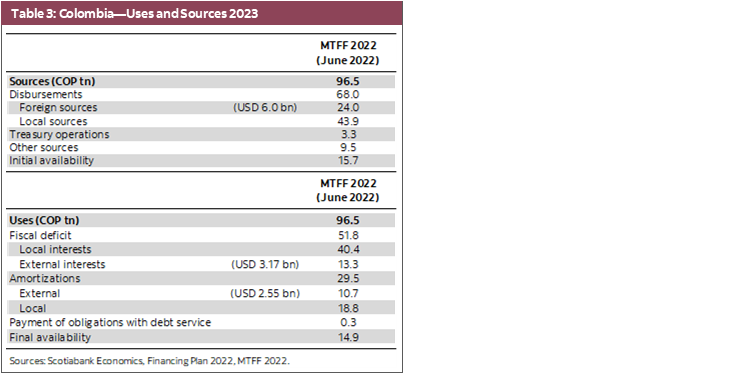

Financing plan 2023 (table 3):

- Tax collections are expected to increase by 2ppts of GDP, representing 16.8% of GDP and returning to primary fiscal surplus, while the fiscal deficit will drop from 5.6% of GDP in 2022 to 3.6% of GDP in 2023. Funding needs in 2023 will represent 6.7% of GDP, which is even lower than the 2015-19 average (8.3% of GDP).

- In 2023, 66% of issuances will be in the domestic market, consistent with the objective of reducing FX exposure and avoid volatile international markets next year. We did not know how much domestic debt will be issued through auctions in the market maker program. However, we expect something similar to 2022 auctions or maybe a bit less than the COP 36 tn of this year.

—Sergio Olarte, Maria (Tatiana) Mejía & Jackeline Piraján

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.