- The Fed hiked 75bps…

- ...and why markets took communications more dovishly than expected

- BoC is forecast to follow the Fed with 75bps in July

Fed funds upper limit (%):

Actual: 1.75

Scotia: 1.75

Consensus: 1.50

Prior: 1.0

After scaring the pants off markets by leaking guidance to preferred media outlets on Monday, what was delivered today was largely taken in stride with markets putting a slightly positive slant on it. The ages old trick of setting up expectations to be really bad and then making it feel less hurtful on the day itself actually worked.

In keeping with this morning’s note that leaned toward a dovish market reaction relative to what had become priced, the two-year Treasury yield plunged by about 19bps as the communications unfolded with most of the move occurring during the press conference. The 10 year yield fell about 14bps so the 2s10s curve slightly bull steepened. The USD depreciated by about ¾% on a DXY basis. The S&P500 edged up by about ¼%.

Please see here for the original statement and here for the Summary of Economic projections including the ‘dot plot’ or rate expectations.

RATE GUIDANCE

The Fed funds target range was hiked by 75bps with the upper limit rising to 1.75% as priced and expected by about one-third of the Bloomberg consensus including Scotia’s 75bps call. Not all primary dealers forecast the hike given the uncertainty around the Fed’s in-blackout guidance toward 50bps and whether news outlets on Monday were talking 75bps on their own or acting as Fed whisperers.

During the presser, Powell said that the next move on July 27th could be either a 50 or 75 basis point hike. That was more ambiguous relative to the fact markets were firmly priced at a 75bps move then. This is one reason we saw markets respond dovishly to the communications.

If the Fed goes 50 in July after guiding it thinks it will hike by 175bps more from here over the year’s remaining four meetings, then that could imply that they will have, say, three 50bps moves in a row and then a quarter point hike in December.

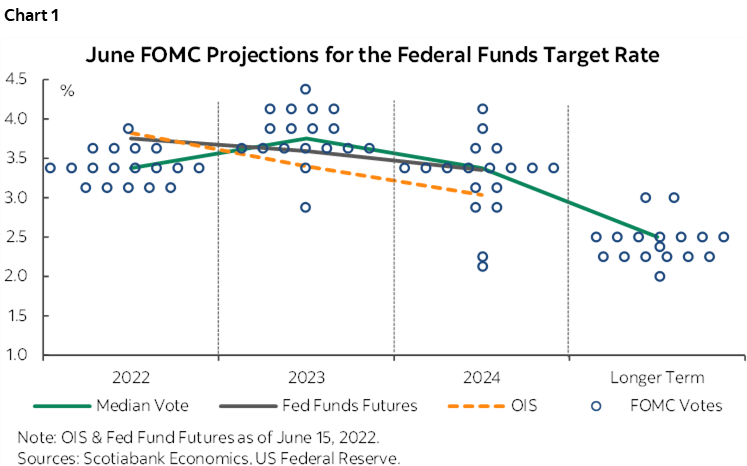

The SEP including the dot plot (chart 1) outlined expectations for the fed funds rate to rise to 3.4% by the end of this year, 3.8% by the end of next year and 3.4% in 2024. Unless they see a very transitory overshoot over the first half of 2023 before easing somewhat later in the year, then the message is that the FOMC sees the terminal rate as being about a quarter-point lower than where markets were pricing into next year (4%). This is another reason for the somewhat dovish market reaction relative to what had become priced.

The neutral rate forecast was essentially unchanged at 2½% as the math only took the median up a tick to 2.5% on the dot. There was probably very low risk of a material adjustment here in any event, but not moving up reinforced the relative dovishness.

In fact, I love the dot plot as either the pictorial depiction of the views was a sheer coincidence or they have a sense of humour. I’m hoping it’s more the coincidence angle. The dots depict patterns marked by up-pointing arrows in each of 2022–24.

STATEMENT CHANGES

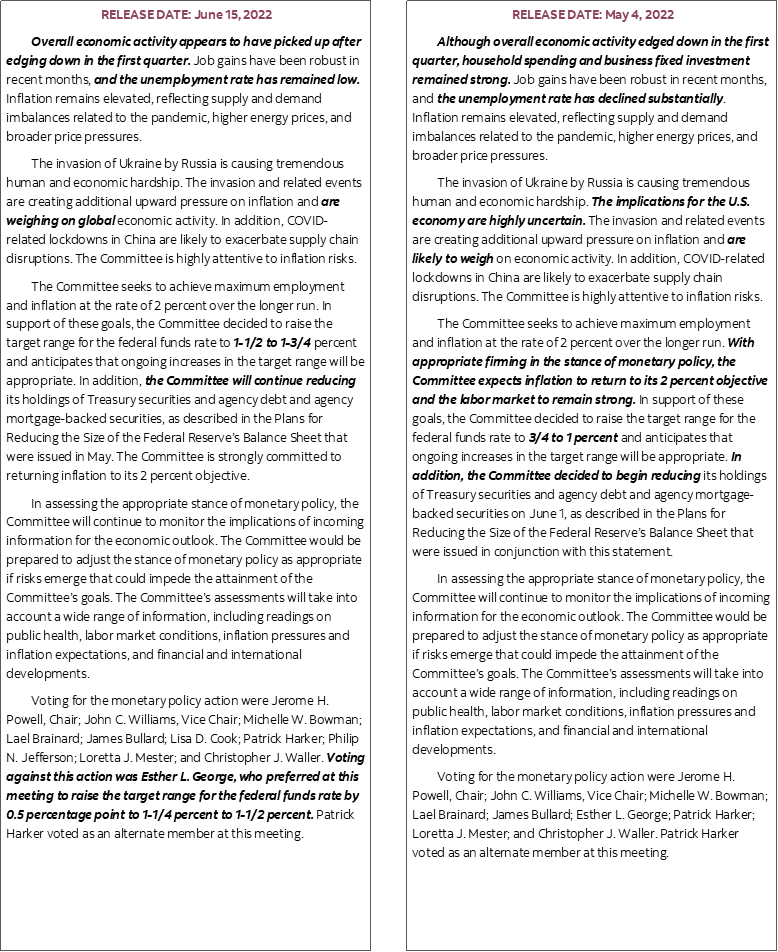

There were a few statement changes that are highlighted in the statement comparison at the back of this note. None of them were all that meaningful in my opinion.

- the current conditions paragraph emphasized that activity “appears to have picked up after edging down in the first quarter” which compares to the prior statement’s past tense reference to Q1 GDP and its composition.

- the current conditions paragraph also now says the “unemployment rate has remained low” instead of “has declined substantially” which acknowledges it has flatlined at 3.6% for the past three months.

- reference to the Ukraine War’s effects being “likely to weigh on economic activity” have been put in a more affirmative sense that now says “are weighing” and with reference to “global” activity.

- Gone is reference to how the implications for the U.S. economy of the war in Ukraine are “highly uncertain” which is perhaps a tacit green light to turn more aggressive with hikes.

- Also, the third paragraph now struck out reference to how “appropriate firming in the stance of monetary policy” will achieve the Fed’s dual mandate goals. When questioned on that in the presser, Powell basically said that’s because they don’t see inflation as just being under the control of monetary policy versus supply side and other factors.

A DISSENTER HAS SOME EXPLAINING TO DO

KC President Esther George dissented by preferring a half point hike at this meeting. I’d like to hear her rationale. She has traditionally been somewhat more hawkish. Did she dissent because she is relatively less hawkish than others this time? Or because she thought they should have stuck to prior guidance because not doing so could diminish the reliability and usefulness of that guidance in future? Or maybe she thought it was ethically questionable to have done what the Fed did with the press on Monday in which case I’d give her a big pat on the back.

SO MUCH FOR FUTURE EASING

If there is one thing to take as a mildly hawkish signal it is the fact they don't really budge very far off the terminal rate overshoot in 2023 as we go into 2024. The median rate projection drops from 3.8 in 2023 to 3.4 in 2024. I might have thought they could have signalled somewhat more of a movement lower that far out after a transitory terminal rate overshoot, but the effect is pretty small.

FORECASTS

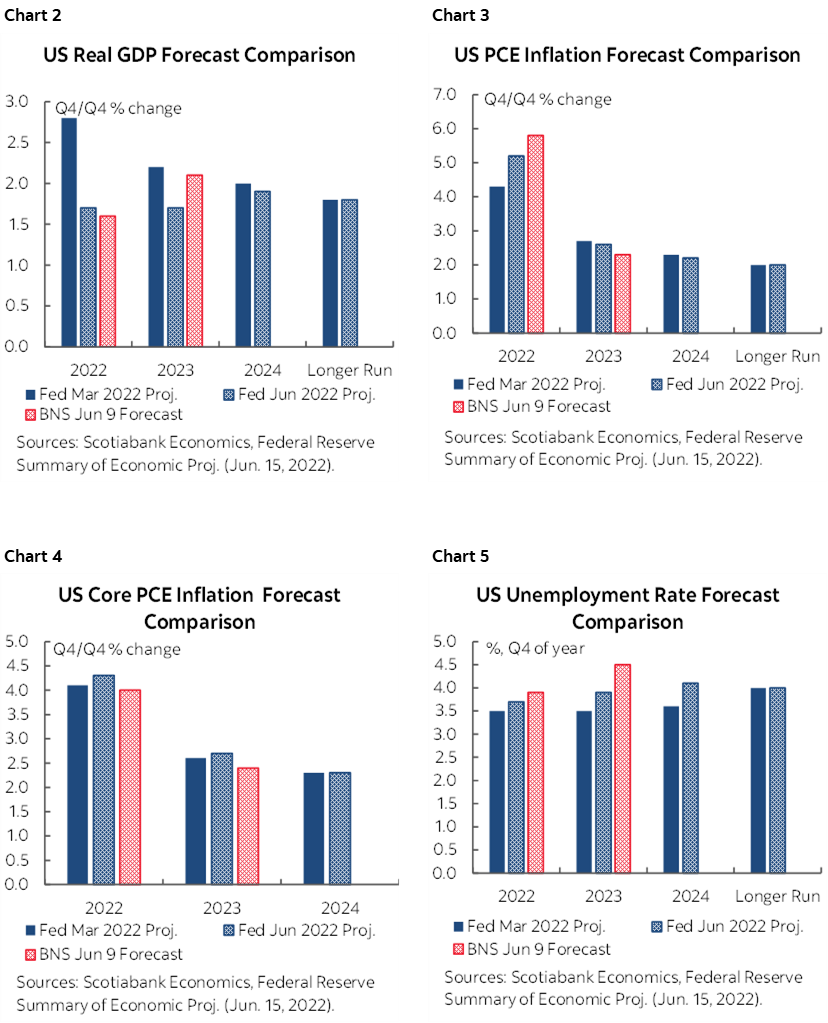

The FOMC downgraded growth forecasts and raised forecasts for the unemployment rate a touch. It raised this year’s total inflation forecast, and lowered it a tick in each of the next two years. They also raised core PCE inflation forecast for this year but for next year only edged it up a tick and then left it unchanged at 2.3% in 2024. That continues to signal that they think this will be a prolonged period of inflation riding above target. Please see charts 2–5.

Their message on growth is that it won't slow any lower than potential at any point and hence we'll stay in mild excess demand but without going further into this state, or open excess capacity. They are counting on supply chain effects to kick in and drift inflation lower while classic Phillips curve arguments stay fairly stagnant and with only a mild backing up in the UR. This is indeed contestable.

There were no changes to longer run inputs etc on potential growth, UR, PCE.

BALANCE SHEET ON AUTO-PILOT FOR NOW

There were no alterations to the balance sheet plans as expected. When questioned on the effects of QT, Powell said that the plans were laid out in advance, they are being delivered and are well understood by markets. I think that’s true for now, but we need to get to the scenario around what happens when reserves are diminished by a material amount of QT and that probably won’t happen until into next year once the Fed swings from $45B/mth of roll-off now to full implementation at a US$90B/mth pace from September onward.

NO WAY TO COMMUNICATE

At issue is still the ethical matter of how the Fed can get away with planting stories with preferred media outlets. Today’s explanations from Chair Powell matched the tone of the articles on Monday to a perfect ‘t’ which makes it abundantly clear the Fed picked up the phone to manage the messaging that day. He got off light in the questioning around this issue during the presser because he was talking to the folks who get to sell more subscriptions when the Fed does this. I remain of the view that this is no way to communicate and sets a double standard for everyone else. They may face an uphill battle getting markets to believe what they say into future meetings even just one-meeting ahead at a time.

Powell argued that they said they would be ‘nimble’ in response to incoming data when explaining the shift from prior guidance to expect 50bps at this meeting to delivering 75bps. He said that last Friday’s inflation reading plus the UofM measures of inflation expectations changed things during blackout and so "the committee decided that a larger increase was needed at this meeting." Not so fast. You should have conditioned your guidance toward a possible 75 if such data had surprised but there was no such guidance. That makes the Fed look erratic and uber sensitive to the latest whiffs. It seems that every time he shows up he has another latest and greatest reading to point toward in order to justify a sudden epiphany. Recall last December that after spending the whole year in denial toward inflation, he said it was the employment cost index that changed his mind. Maybe next time try on how the FOMC is simply way behind the curve and how it doesn’t hurt to fess up.

When asked when were forecasts revised and submitted in light of the flap over the media stories on Monday, Powell said that the Summary of Economic Projections reflect the 75bps move and that Committee members had that in hand when their forecasts were submitted. I’d add that recall the forecasts are first submitted on Friday before the meeting but that they can be changed up to the night of the first day of the meeting (ie: last night).

It’s unlikely that we will get the same flap over adjusted expectation during the next FOMC blackout. Powell emphasized how it is very unusual to get material data late into blackout and that he has only seen it happen 1 or 2 times in his ten year memory or so. Further, at least into the July meeting we shouldn't have this same issue of new info into the blackout at least in terms of the measures he cited as influencing their thinking during the blackout. CPI lands on July 13th, UMich inflation expectations land on the 15th and then the Fed goes into blackout on the 16th. Only the Conf Board measure of inflation expectations arrives the day before.

Q&A GUIDANCE & MISCELLANEOUS MATTERS

Miscellaneous matters also helped to either reinforce prior messaging or add somewhat further guidance.

On labour markets, Powell said they are expecting supply and demand for labour to come back into balance but that they are not expecting much of an employment hit. His argument is likely similar to one or two other central banks I’ve heard on the topic in that they seek to dent job vacancies as an indicator of excess demand for labour. It might also be the case that companies could horde labour going forward; when labour supply isn't growing quickly and it costs to hire and retrain, employers may be loathe to let go of talent out of fear they’ll never get it back.

In response to a question on whether the dot plot projection for the peak in the terminal rate is going to be enough to cool inflation (perhaps in reference to opinions like Bill Dudley’s) Powell simply said the 3.5–4% terminal rate range is “in the range of plausible numbers” but that "We'll know when we get there."

When asked what he means by wanting to see "compelling" evidence that inflation is coming down before they have comfort that their goals are on the path to being met, Powell referenced last summer when there was a bit of a head fake. That likely reinforces my impression that they would want 6–12 months of durable evidence that inflation is cooling with measures of expectations reinforcing this before they cool off tightening.

The projections may be making a rather heroic assumption with respect to the rapid cooling of inflationary pressures accompanied by an inconsequential impact upon the unemployment rate. Even if the Phillips curve turned out to be still relatively flat there should be some significant effect of tighter monetary policy in order to cool inflation, though I think the curve is probably being shifted structurally steeper now. Put another way, for the FOMC projections for inflation to be cut down to being 2-handled with an inconsequential impact upon the UR basically assumes either it's all supply chain driven inflation (which it isn't) or just farcical and fanciful thinking that is politicized in the set of overall messages.

There were several questions about soft landing and Powell answered them all saying he still thought that this was achievable, that this is what the projections are showing and that there was a path to such an outcome. Powell’s strongest statement came when he said "There is no sign of a broader slowdown in the economy that I can see" and added “We are not trying to induce a recession now, let’s be clear about that.”

When asked whether QT will make things ‘worse’ , Powell replied by saying they've communicated their plans clearly in advance, markets understand what they are doing, Treasury issuance is down and it's understood and accepted at this point. I would say we’ll need to see into next year once there has been a material decline in reserves.

BANK OF CANADA TO FOLLOW THE FEDERAL RESERVE

We are officially forecasting the BoC to hike by 75bps at the July meeting. I think they could've done it without the Fed anyway, but it doesn't hurt to have your big bro standing up for you in the playground.

1. BoC guidance was open to it already but also to a higher terminal rate

2. Next week's inflation will have them running out of kleenexes at the BoC. I’m expecting a full percentage point acceleration toward 7.8% on genuine drivers that only includes 0.2 added by inclusion of used vehicles and with no further material effect from updated basket weights.

3. The July 4th BoC surveys will light up inflation expectations again.

4. The BoC—like the Fed—is far behind and needs to accelerate its catch up toward a neutral rate range.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.