FORECAST UPDATES

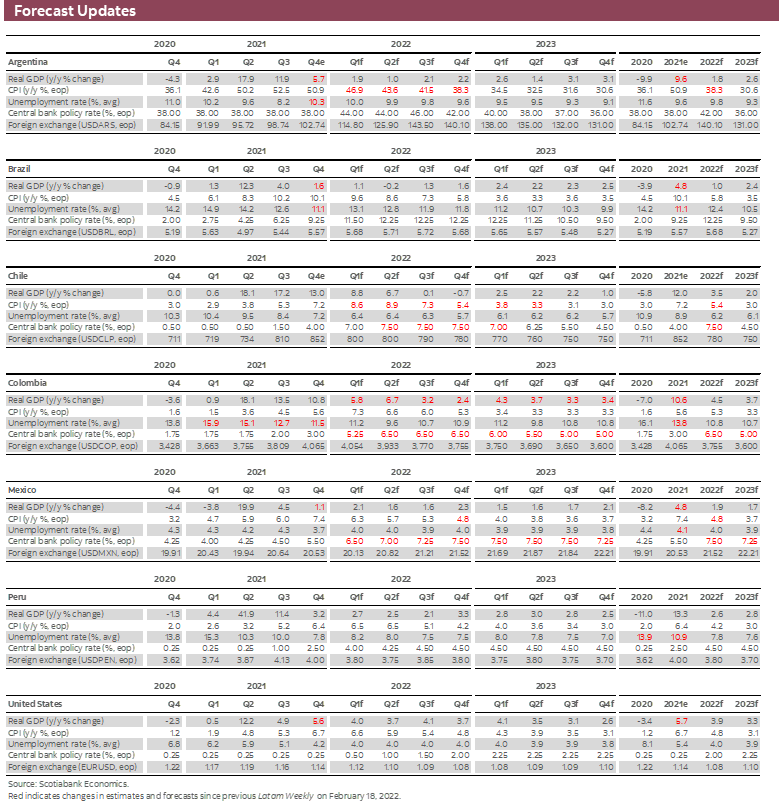

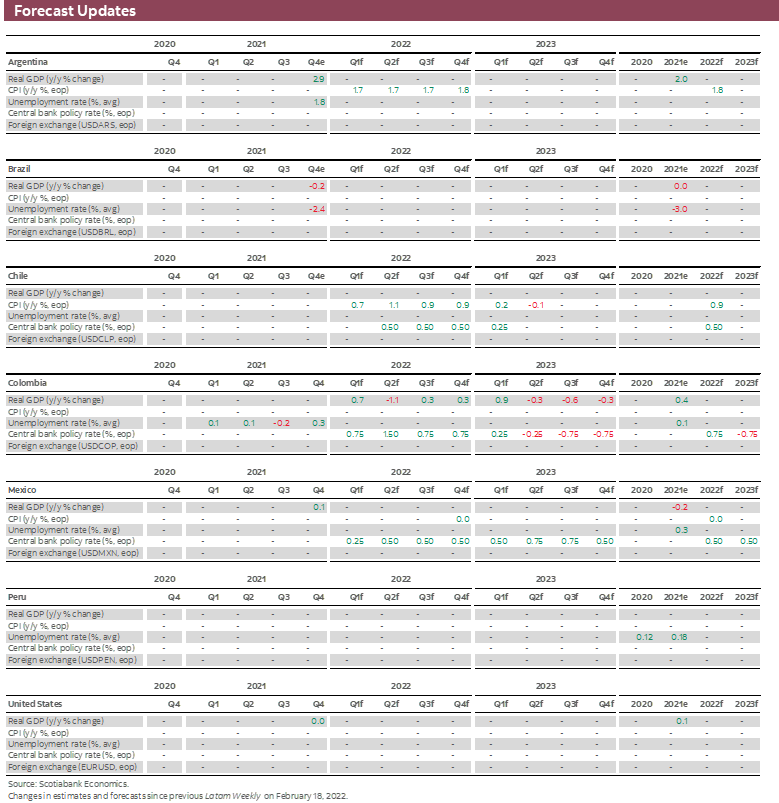

- The Russian invasion of Ukraine has led to marked increases in global commodity prices and fomented additional uncertainty with respect to the near-term outlook for inflation, growth, and key policy rates. Scotiabank economists in the Latam region will be assessing the impact of geopolitical developments in the days ahead. See the latest revisions made to their forecasts in the table below.

ECONOMIC OVERVIEW

- The long-term impacts of the Russian invasion are unknown at this point, but it is already clear that it will be a humanitarian disaster. The human costs of war revive the “Pottery Barn Rule,” by which countries resorting to military force to achieve political objectives have moral obligations.

- The invasion will also impose large costs on a global economy still struggling to recover from the effects of the COVID-19 pandemic.

- For the Latam region, however, the near-term economic costs could be offset by the positive terms-of-trade shock from higher commodity prices. Higher prices of key exports should generate increased fiscal revenues and strengthen external balances.

- Given an environment of heightened geopolitical risk, governments in the region should use fiscal windfalls to strengthen institutions and pursue sound policies.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

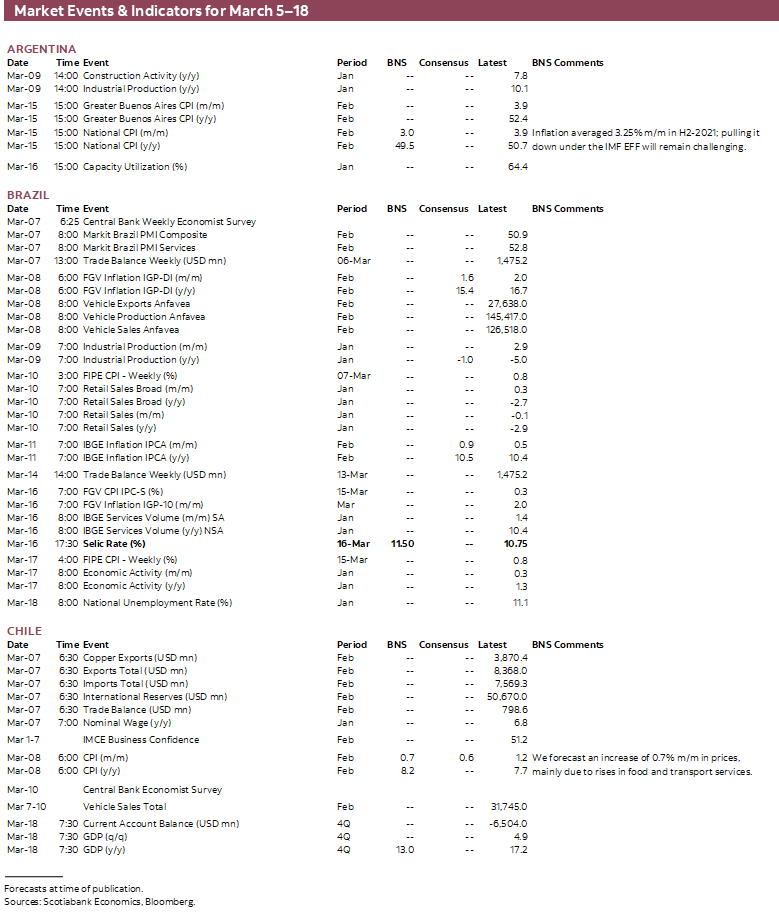

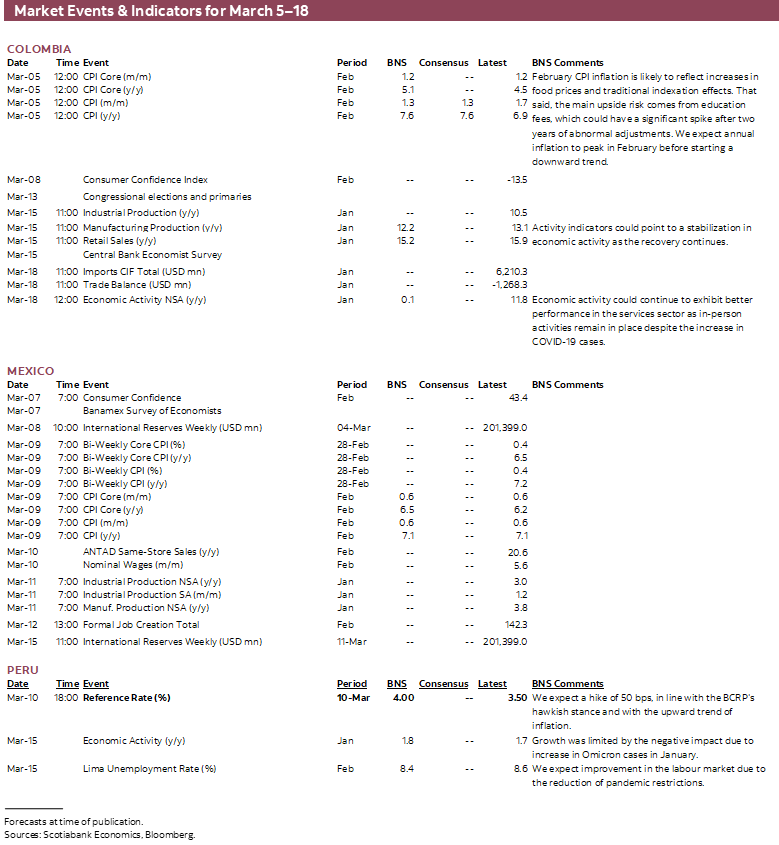

- A comprehensive risk calendar with selected highlights for the period March 5–18 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: The Pottery Barn Rule

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Whatever the eventual outcome of the Russian invasion of Ukraine, it is already clear that it is a humanitarian disaster in the making. Rather than an adroit realpolitik gambit, the invasion appears to be a strategic miscalculation that will impose costs on the global economy.

- And while the Pottery Barn rule—“you break it, you pay for it”— referenced by then-Secretary of State Colin Powell on the eve of the second Iraq war will assuredly not apply, Russia’s invasion of Ukraine and the geopolitical risks it foments add new uncertainty to the global economic outlook.

- In the near-term, commodity prices have risen across the board as a result of heightened geopolitical tensions. If these higher prices are sustained, they would constitute a favourable terms-of-trade shock to Latam commodity producers. In this respect at least, the ill wind of war may blow some good.

IT’S AN ILL WIND

With Latam central banks focused on containing inflationary impulses that threaten medium-term price stability commitments, attention will increasingly turn to the implications for growth. Meanwhile, the intensification of geopolitical risks stemming from Russia's invasion of Ukraine, and what the invasion may portend for the rules-based international order, amplifies the threats to global, and regional, growth. Investors and policymakers alike may well be asking “what else can go wrong?”.

Rather than an adroit realpolitik gambit, as a certain “very stable genius” has opined, the invasion looks more like a colossal strategic miscalculation with each passing day, one that is certain to inflict costs on the global economy, in addition to leading to wholly unnecessary and indefensible suffering and loss of life. As then-Secretary of State Colin Powell warned President Bush on the eve of the second Iraq war, the apocryphal Pottery Barn rule—“you break it, you pay for it”—applies in modern warfare. That is, nations resorting to military force to achieve political objectives have certain moral obligations. The original literal rule may (or may not) apply in pottery stores. And while Powell’s metaphorical reformulation wasn’t necessarily observed in Iraq, it is already clear that it won’t be followed in the case of the Russian invasion of Ukraine. Tragically, the human costs measured in terms of deaths and lives irrevocably shattered will be incalculable.

From the perspective of the dismal science, the only questions are how much damage will be done and what the economic impacts will be. The initial market reaction to the invasion was pretty much what would be expected. Global equity markets that immediately sold off on February 23 quickly bounced back and have since alternated between risk-on and risk-off modes. Global currency markets, meanwhile, have reflected “safe haven” effects, with the US dollar appreciating broadly against the currencies of non-commodity-producing countries.

Over the longer term, financial markets are likely to be subject to heightened levels of volatility, reflecting pervasive uncertainty with respect to the economic impacts of the conflict. One unknown is the extent to which geopolitical uncertainty leads to a delay in consumption and investment decisions. Growth prospects could be dampened, for example, if businesses hold-off on investment, waiting for greater clarity on the long-term implications of the war, as they exercise the option value of waiting.

The effect that sanctions and possible retaliatory counter-sanction measures have on global supply chains, and thus inflation, is obviously a key issue. Fed Chair, Jerome Powell, in congressional testimony this week, indicated that, while the implications of the war are uncertain and will have long-lived effects measured in years, they would not deter prospective interest rate hikes.

Powell indicated that he would be proposing a gradual 25 bps start to the tightening cycle at the Fed’s next meeting but did not rule out a more aggressive pace of tightening if warranted by inflation developments in the months ahead. His comments were welcomed by financial markets, likely because they signaled the Fed’s commitment to price stability. Strong US employment numbers released March 4 strengthen the case for action.

For its part, the Bank of Canada (BoC) pulled the trigger and raised its key interest rate this week following the release of strong growth numbers, undeterred by the potential uncertainties generated by the attack on Ukraine. In this regard, the BoC joins the Bank of England in starting what will likely prove to be a long, steady process of tightening, with the Fed close behind.

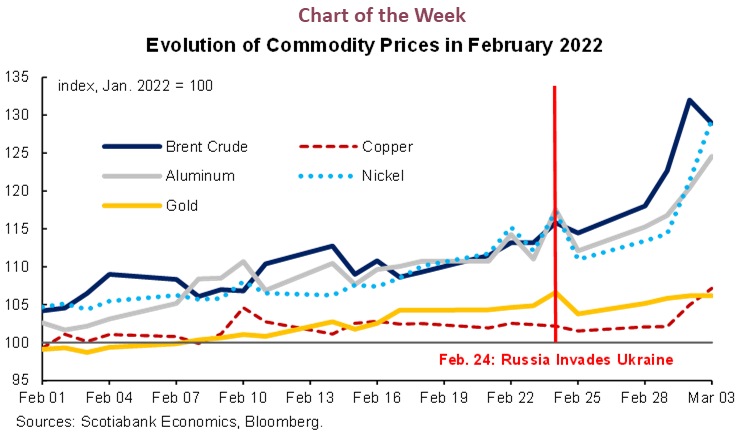

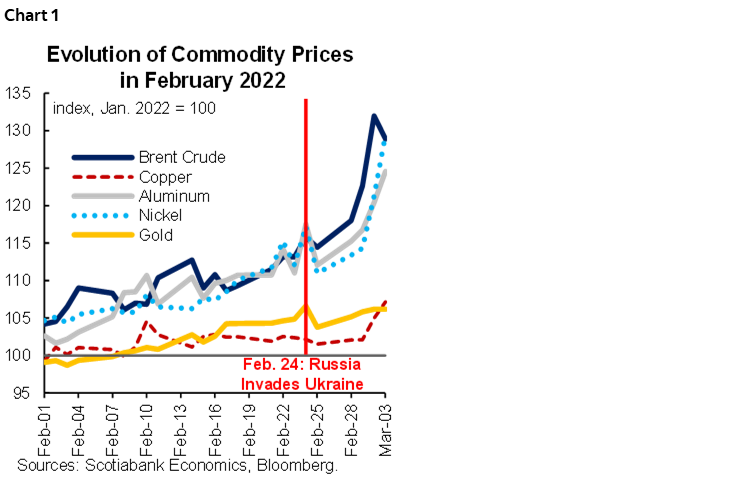

The impact on commodity markets is both clearer, as Scotiabank’s Marc Desormeaux notes, and of direct importance on the Latam region. Most commodity prices have continued the upward trajectories they had mapped out prior to the invasion (chart 1). Oil has been the most obvious beneficiary of the war given Russia’s share of global production, with oil prices rising to $ 118/bbl in trading on March 4th. But given Russia’s role as a major producer of copper, nickel, and aluminum the potential for supply disruptions has likewise pushed these prices higher. Meanwhile, the prospect that shipments of wheat and other cereal from Ukraine could be disrupted has also pushed their prices to record levels on international markets. And with the prevailing uncertainty as to how the conflict will play out, there is material upward pressure on commodity prices going forward. That scenario, should it play out in the weeks and months ahead, does not bode well for inflation.

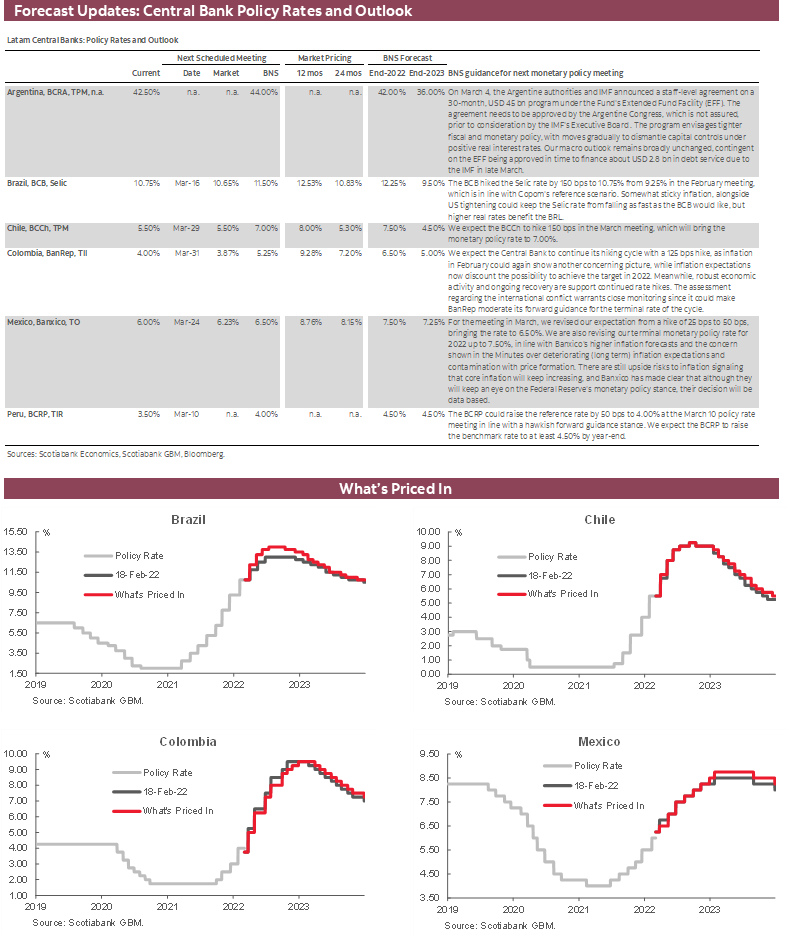

It is clear, therefore, that in the wake of the Russian invasion Latam financial markets will have to price in increased inflation risks, and thus the potential for more aggressive monetary policy tightening, large terms of trade shocks, as well as potential hits to external demand. At the same time, even before the invasion of Ukraine, Latam markets faced the prospect of less favourable financial conditions as advanced country central banks were poised to raise rates, leading possibly to a shift in investor risk appetite away from regional assets. That potential challenge is coming closer.

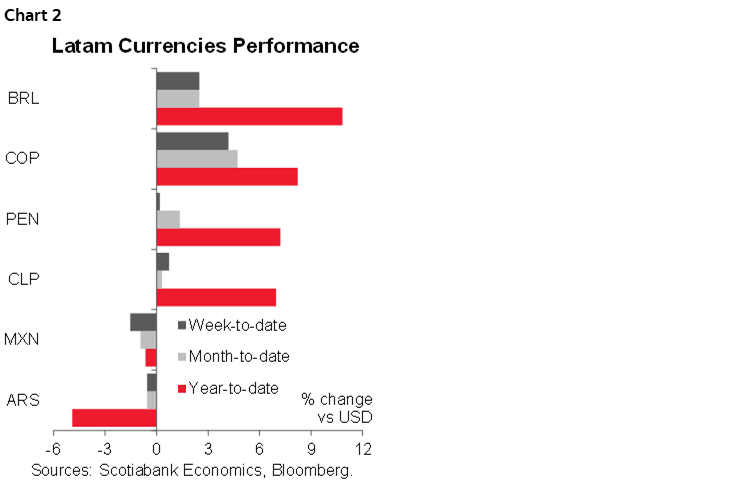

To this point at least, however, foreign exchange markets in the region have responded positively to heightened geopolitical risks. Most Latam currencies have appreciated modestly against the US dollar, reflecting the favourable terms-of-trade effects from higher commodity prices (chart 2). Mexico is an outlier here, despite being an important oil producer. This is likely explained by the fact that Mexico is no longer a net exporter of oil. And as our experts in Mexico City have stressed in past editions of the Latam Weekly, uncertainty over key policy frameworks, such as energy reforms, may have suppressed foreign direct investment flows. Argentina’s peso has also depreciated against the US dollar, once again underscoring the costs of unstable policy frameworks that likely contributed to previous delays in ramping up production of the Vaca Muerta gas reserves.

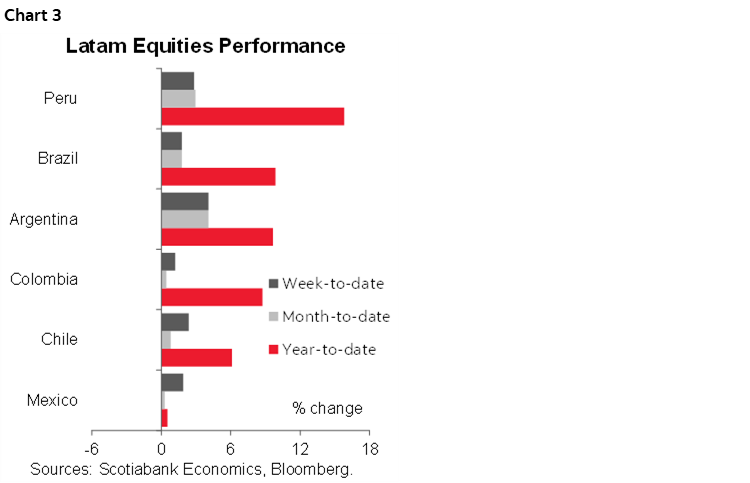

Latam equity markets have likewise risen in recent days, probably in anticipation of higher profits from the commodity price windfall (chart 3). However, equity investors have had to balance the impact of rising commodity prices with the potential for higher inflation and the possibility of more aggressive tightening by Latam central banks and higher interest rates, which would depress equity prices. In contrast, higher domestic policy rates would support local currencies.

Looking ahead, the growth, inflation, and policy rate forecasts of Scotiabank’s teams in the region will evolve over time as new information comes in and the uncertainty that currently clouds the outlook is dispelled. While that process will take some time, one thing is already certain: there are several factors to consider. For example, our economists in Lima note below (see country notes) that the oil price assumption on which their inflation forecast for 2022 was based clearly no longer holds. While futures markets are pricing a decline in prices from recent highs, the longer that oil (and cereal) prices remain above their assumptions, the larger the risk of the material upside revisions.

Meanwhile, Scotiabank economists in Santiago point out (see below) that Chile’s exposure to direct external demand shocks from the invasion is low given imports from and exports to Russia are very low. Higher copper prices represent a favourable terms-of-trade shock, with positive effects on public finances and incomes. And while higher oil prices will exert upward pressure on inflation, this effect will be limited by government subsidies that could help temper the response by the central bank.

In Colombia, Scotiabank’s team also highlights (below) that the positive terms-of-trade effect should have a positive fiscal impact through higher government revenues, while reducing current account deficits. An improved fiscal outlook, combined with a narrowing of the current account, would mitigate two potential risks. In this regard, as our economists in Bogota argue, it is important that the government capitalize on the “mini-boom” generated by higher commodity prices to reinforce sound policy frameworks. This is good advice at any time, but is especially so in periods of increased uncertainty, such as that likely to prevail over the coming months.

Against this backdrop of economic and geopolitical uncertainty, early indicators suggest that for most Pacific Alliance countries the positive terms-of-trade effects associated with the current geopolitical risk-on environment—higher commodity prices—could outweigh possible negative effects from, say, weaker external demand. In this sense, the old saying “it’s an ill wind that doesn’t blow some good” may apply. But it is early days, and the full impact of the whirlwind unleashed by Mr. Putin remains unknown. What is clear is that, whatever the economic effects, the invasion of Ukraine has already been a humanitarian disaster.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Job Creation Strong while Activity Moderated in January; Hostilities in Ukraine will likely have Limited Impacts

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

As the omicron variant advances, the daily number of confirmed COVID-19 cases has continued to increase in recent days—albeit at a slower pace. The test positivity rate fell to 20%. However, the occupancy rate of ICU beds is increasing, while the COVID-19-related death rate rose to its highest level since mid-2021. Meanwhile, the vaccination campaign has reached 93.2% of the eligible population. The rollout of booster (third) doses continues—reaching 12.3 million people—and the new booster dose (fourth) is in progress.

ECONOMIC ACTIVITY MODERATES IN JANUARY, SUPPORTED BY STRONG JOB CREATION AND SERVICES

On Monday, February 28, the statistical agency (INE) announced that the unemployment rate rose to 7.3% in the three months ending in January. The increase in the unemployment rate is explained by a larger rise in the labour force (0.5% m/m) relative to employment (0.4% m/m), a phenomenon that we expect to continue in the coming months, as more people re-enter the labour market before financial assistance programs end, which will result in the gradual reduction in household liquidity.

In the three-month period ending in January, 35k jobs were created as compared to the previous period. By sector, formal employment increased by 46k people, while 11k informal jobs were lost.

On Tuesday, March 1, the central bank (BCCh) released the Imacec for January, which grew 9.0% y/y. The health and business services sectors made the largest contributions to Imacec’s year-on-year growth, followed far behind by commerce. The dynamism of business services reflects the resilience of private investment as shown by imports of capital goods and the continued execution of important projects despite political uncertainty.

Imacec’s seasonally adjusted series shows a drop of 1% m/m in January, which confirms a smooth deceleration of activity. Indeed, in seasonally adjusted terms, the growth of 1.3% m/m in services stood out, coming on top of several months of expansion. Although a gradual slowdown in trade (-3.2% m/m) was observed, households are likely cushioning the decline in fiscal transfers by building up liquidity in chequing accounts (USD 17 bn as of January 2022). Looking ahead, the start of the Universal Guaranteed Pension payments in February, which provide resources to older age groups with a high propensity to consume, should help fuel spending.

MoF ISSUED USD 2 BN IN INTERNATIONAL BOND MARKETS, COMPLETING PLANNED FOREIGN CURRENCY BORROWING FOR 2022

On Wednesday, March 2, the Ministry of Finance (MoF) reported issuing Treasury bonds in international markets totaling USD 2 bn, as part of the government’s 2022 financing plan. For 2022, the government’s plan considers issuing Treasury bonds for a total of USD 20 bn, within the debt limit authorized by the 2022 Budget Law, of which USD 6 bn corresponds to foreign currency offerings. This issuance completes the total amount of foreign currency issuances contemplated for 2022, equivalent to USD 6 bn. The issuance reached a total demand of USD 8.1 bn, 4.1 times the allocated amount. The yield was 4.346% (200 bps spread over the US Treasury rate). The MoF also announced the injection of USD 4 bn to the Economic and Social Stabilization Fund (FEES) in January, using the resources from the last issuance. We do not rule out that this new USD 2 bn issuance could be injected to the FEES.

CONSTITUTIONAL ASSEMBLY CONTINUES DRAFTING NEW CONSTITUTION

In the last two weeks, the various thematic commissions established to draft the new constitution continued voting (both in general and on an article-by-article basis), while the Fundamental Rights Commission (50 articles) and Environment Commission (38 articles) presented elements of their reports to the floor of the Assembly. The floor of the convention also approved new proposals from the Justice Systems commission that had been rejected in the first stage of voting, and after modifications will be included in the draft of the new constitution.

Each proposal needs a two-thirds majority in the Assembly (103 votes) to be approved. If an initiative is rejected, it goes back to the original commission to be discussed, modified, and put to a vote on the floor of the Assembly in a second round. This process will extend to April 28, at which point the Assembly will have the final draft of a new constitution. After that, a Commission of Harmonization will ensure the consistency and coherence of the approved norms.

TENSIONS IN UKRAINE WILL LIKELY HAVE LIMITED IMPACTS

Hostilities in Ukraine are generating different effects across countries, mainly through financial markets. The price of copper increased owing to supply worries, given that Russia is the seventh largest exporter of the commodity. This represents a positive development for the Chilean economy and for the public finances and would generate higher incomes for the country. The Chilean peso (CLP) has been relatively stable, however, trading around CLP 800 per dollar. While the increase in oil prices will have an impact on inflation, this effect will be limited owing to the subsidies from the government under the Fuel Prices Stabilization Mechanism (MEPCO). We think that the central bank will not react with additional hikes in the benchmark rate in part because the negative effect on global economic activity could moderate the long-term inflation pressures coming from a supply shock. In this respect, recent developments have not had a significant impact on long-term interest rates.

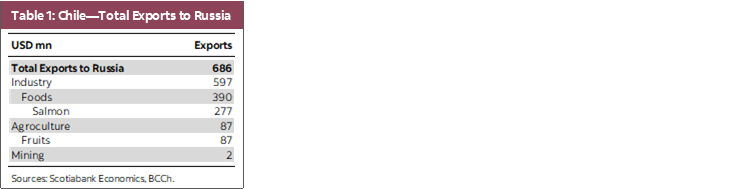

Meanwhile, Chile’s exposure to external demand shocks is low given Chilean imports from and exports to Russia are very low. In 2020, the value (in USD) of imports from Russia was 0.8% of the total. Similarly, the value of exports reached USD 686 mn in the same period (0.9% of the total), of which USD 597 mn was of industry, mainly foods (salmon) (table 1).

In the fortnight ahead, on March 8, the statistical agency (INE) will release inflation data for February. On March 18, the central bank will publish the national accounts of the last quarter of 2021. In the political arena, on March 11, the new government will take office, led by President-elect Gabriel Boric.

Colombia—Twin Deficits and the Impact of High Oil Prices

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

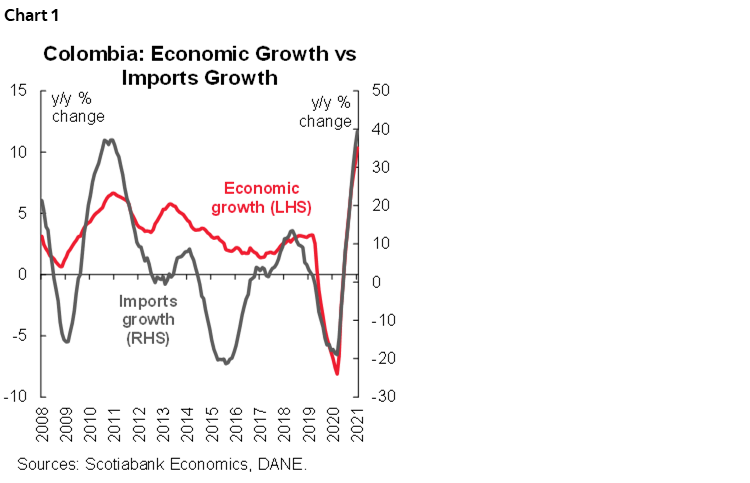

Historically, the Colombian economy’s most grievous fault has been the high current account deficit, which since 2005 (when new GDP methodology started) has averaged 3.5% of GDP. However, the underlying factors that have led to high external deficits have also facilitated their financing and have made large deficits sustainable. In fact, strong investment that is financed by foreign direct investment is the main driver for endemic imbalances. And the need for increased imports of durable goods and inputs during phases of investment recovery in Colombia is usually mirrored in higher FDI that endogenously finances the current account deficit (chart 1). The pandemic changed that, at least temporarily.

During 2020 and 2021, Colombia had an average current account deficit of 4.3% of GDP. But in contrast to past episodes of large deficits, this time investment wasn’t the main driver. Rather, it was higher fiscal expenditures that widened the current account deficit, and which in turn account for higher external and domestic indebtedness as external imbalances were debt financed.

The current account has activated alarms about the Colombian economy, since not only was the external deficit especially high compared with peers in 2020 and 2021, but the fiscal deficit also showed a significant deterioration surpassing 7% of GDP. As a result of all that the real exchange rate has depreciated by more than 14% since 2019 and remains weak. Accordingly, we anticipate the trade balance will continue to be deeply negative in 2022. Against this backdrop, structural changes to improve fiscal accounts and ensure external sustainability remain a significant challenge for Colombia.

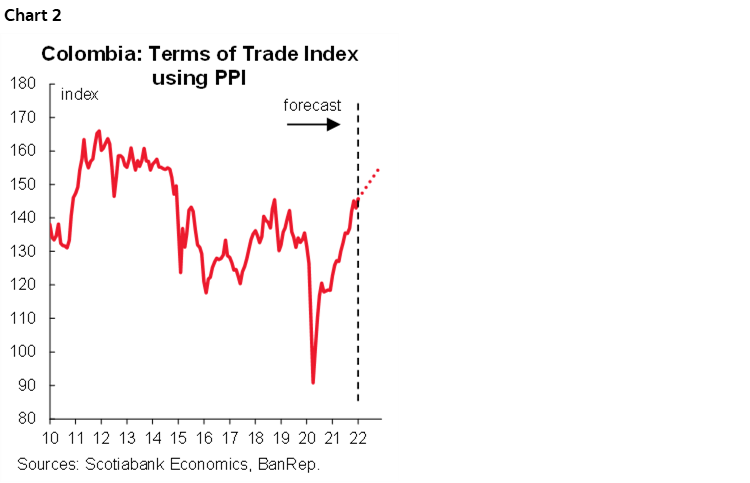

Recent geopolitical developments have led to a significant spike in commodity prices of at least 15% since the Russian invasion of Ukraine on February 24. On balance, we think Colombia’s terms of trade (ToT) should improve (chart 2). In fact, our calculations indicate that if the relationship between import prices and export prices behaves broadly similar to the last three years (during which export prices exhibited 2.5 times more volatility than import prices, on average) and with oil prices 14% higher than 2021 (USD 80 per barrel on average) the ToT should increase by around 7% relative to 2021. In that event, the trade deficit could be reduced by almost half a point of GDP for every USD 10 per barrel, which ensures that the current account deficit will begin to correct and go below 5% of GDP in 2022. While still larger than the 2020 deficit of 3.4% of GDP, this would mark an improvement over the 5.7% of GDP deficit registered in 2021. At the same time, the still-high current account deficit in 2022 will reflect the consolidation of the economic recovery, especially FDI-fueled capital investment that finances the external deficit.

In terms of fiscal accounts, the official 2022 budget has an assumption of average Brent price at USD 70 per barrel. And according to the Ministry of Finance, on average, for each additional USD 1/bbl in the price of oil Colombia would receive COP 400 bn of additional revenues per year. Therefore, if the price of Brent averages USD 80 per barrel in 2022, Colombian fiscal revenues would increase by COP 4 tn (0.33 ppts of GDP). Such a windfall could bring the fiscal deficit this year to below 6% of GDP, and below the original target of the Financial Plan of 6.2% of GDP.

Again, very positive news at the margin, but we cannot ignore that Colombia still has challenges in its fiscal accounts. The next president must guide congressional passage of a structural fiscal reform to consolidate government accounts and send a message of fiscal responsibility to the markets.

All in, higher oil prices help the Colombian economy and will ease some pressure on asset pricing, especially in the FX market and the local yield curve, which should flatten somewhat as a lower fiscal risk premium would help at the long-end. Nevertheless, Colombia needs to take advantage of this mini-boom from higher commodity prices and make structural improvements to the fiscal accounts while fostering further industrialization that would help the economy reduce its dependency on capital and raw materials imports, thereby reducing the medium-term current account deficit.

Mexico—Inflation Looks to be even Stickier than we Thought—We are Revising both Inflation and Policy Rate Forecasts Higher

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The continued surge in global commodity prices and inflation, along with domestic factors, have once again led us to review our terminal Banxico policy rate, as well as our year-end headline and core inflation forecasts. We are concerned about the continuing evidence that Mexican inflation goes far beyond supply chain disruptions. We believe there are at least two other major drivers of domestic inflation:

The first is the uneven recovery of the economy, on both the demand and supply side. Our estimates suggest that supply has surpassed pre-pandemic levels in several categories, but demand recovery has been even stronger, meaning we have some price pressures driven by the closed output gap.

Second, rising producer prices, combined with the long period of contraction and stagnation in Mexico (2019 and 2020) have put pressure on companies to restore their financial metrics. Price pressures on Mexican firms have not only come from spikes in commodity prices and supply chain disruptions, but also from policy decisions, such as increases in corporate income tax collection during the recession, restrictions on the use of the outsourced labour, and strong minimum wage hikes.

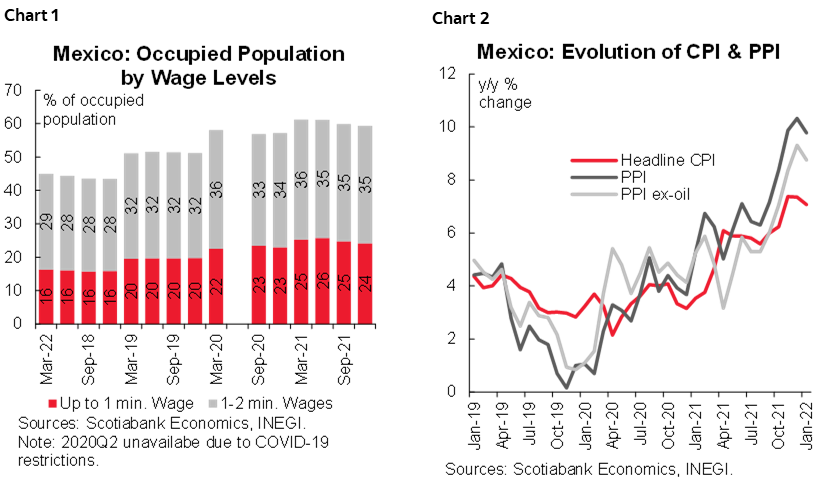

Since 2018, the share of Mexican workers earning minimum wages has increased from 16% to 24% (chart 1). It is not clear whether this increase in the share of minimum wage earners is driven by the aggressive increases in minimum wages observed over the past 3 years such that rising minimum wages have caught up to the market wage, or if it is due to the protracted stagnation of the Mexican economy and high unemployment driving down market wages to the minimum wage. (With data on nominal wage revisions hovering mostly in the 4–7% range over the past 3 years, we think the former is the most likely explanation.) Anecdotally, in our recent discussions with corporate and commercial clients, we increasingly hear that this year’s wage negotiations are proving to be the most complex in at least the past 15–20 years, as companies argue minimum wages are putting much more pressure on their wage negotiations this time around. We believe this will put further cost pressures on firms—making inflation stickier going forward (chart 2). Accordingly, we are modestly revising both our headline and core inflation forecasts higher, reflecting this added stickiness.

Given all the developments above, we now anticipate a 7.5% terminal rate by Banxico (achieved by the end of 2022).

Peru—Lions (Inflation) and Tigers (Politics) and Bears (Russia)…

Guillermo Arbe, Head Economist, Peru

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The political situation in Peru is too unstable to go into in much depth here, lest whatever we state today be overtaken by events in the making. The main issue currently is the intense flak that President Castillo is taking over new allegations of his involvement in acts of corruption. As a result, members of the opposition are once again preparing a motion for his impeachment. And yet, it still does not seem likely that they will get the votes. Why? Well, because Congress is divided into thirds: those that are right of centre, who are promoting the impeachment; those left of centre, who are against, and those linked to interest groups, who mostly like things just the way they are. The interest group advocates hold the balance, and enough of their members in Congress apparently find the government’s anti-institutional policies, or simple lack of policies, as too beneficial to wish to change the current state of affairs.

No date has been set for impeachment proceedings, but another key date is approaching fast. The Cabinet has been summoned by Congress on March 8 for the legally required vote of conference hearing. One wonders if the Cabinet will be intact on that date. President Castillo, apparently seeking to appease Congress, sacrificed his controversial Minister of Labour, Juan Silva, who is at the centre of one of the corruption scandals. Silva resigned on March 1 and has yet to be replaced. Another controversial figure, the Minister of Health Hernán Condori, may not last much longer after the Medical Doctors Association called for his ouster on Wednesday.

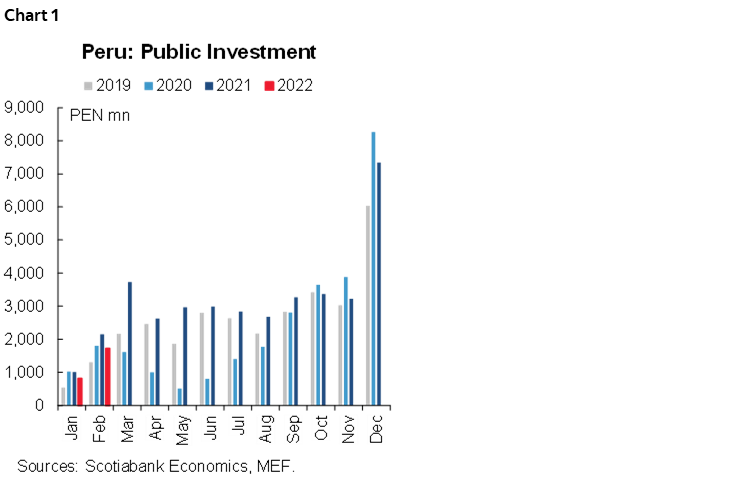

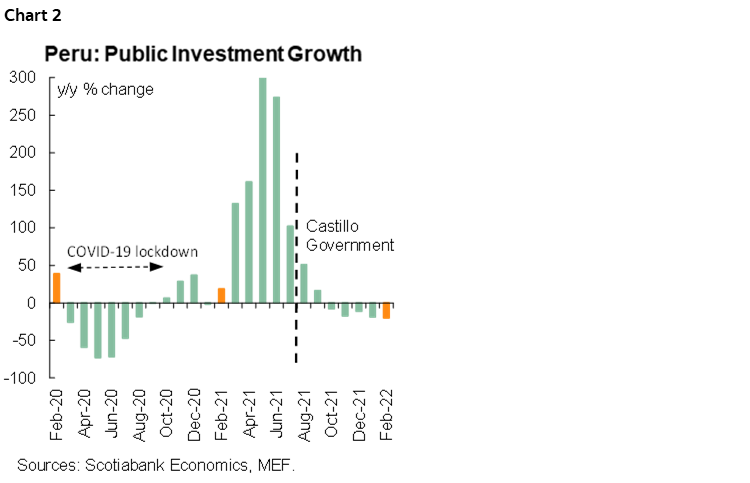

Peru’s economy has so far proved quite resilient to political events. However, there are incipient signs that this may be starting to change. Public investment has fallen sharply this year, down 19.6% y/y in February following an 18.8% y/y decline in January. In fact, public investment has now fallen for five consecutive months, in year-on-year terms. Perhaps not too much should be read into these figures, however, as public investment was particularly high during much of the 2020–2021 period due to COVID-19, and current public investment levels are higher than in pre-COVID-19 2019 (chart 1). Nevertheless, public investment, which was a leading driver of the economy, is now more of a drag on the economy, and one of the reasons why GDP growth has been trending at 1% to 2% since Q4-2021.

One wonders if there is not a governance issue as well (chart 2). It cannot be easy to adhere to an investment schedule with such frequent changes in Cabinet members. The Ministry of Transportation is a good example. It commands nearly half of government investment but has become embroiled in corruption allegations and credibility issues which have likely affected its capability for investment execution. It is not surprising that central government investment is leading the decline, down 29% y/y in January, versus smaller, but still disconcerting, drops in of regional (-5.4% y/y) and local (-15.3%) public investment.

Based on initial information, we expect growth of under 2.0%, y/y in January. December pointed the way as to what to expect in 2022, with its low 1.8% y/y GDP growth.

The slowdown in growth increases the BCRP quandary, as inflation continues to hover at uncomfortably high levels. Yearly inflation rose from 5.7% in January to 6.2% in February. Given that inflation is being driven mainly by high imported energy prices and soft commodity prices, which are being exacerbated by the war in Ukraine, the BCRP will be very hard put to return inflation to the 1% to 3% target range. The BCRP has been stimulating a PEN appreciation and trying to manage inflation expectations, which were at a manageable 3.7% yearly in January.

Still, things have changed since Russia’s invasion of Ukraine. Our forecast of 4.2% inflation for full-year 2022 was based on WTI oil prices well under USD 100/bbl, and the stabilization of soft commodity prices, especially wheat, soy and maize. We can no longer hold to these expectations. However, it’s early in the Ukraine conflict, and uncertainty over how the war will develop is still too high for us to hasten with new forecasts. Suffice it to say that our inflation forecast is under revision, and we attach a material upside risk to it.

In light of this, we will monitor our forecast for the BCRP (4.50% by mid-2022) but note that higher inflation will not automatically mean that the BCRP will be more aggressive in raising its reference rate, given the risk of a slowdown in GDP growth at the same time.

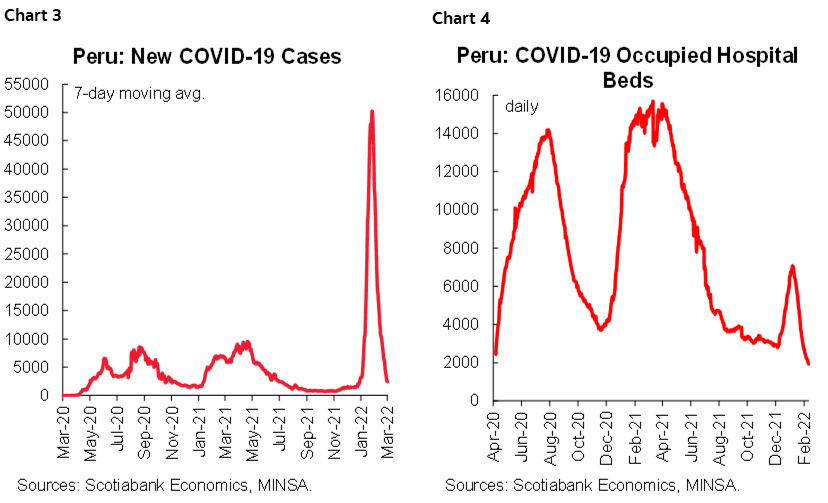

To end on a more positive note, COVID-19 has all but disappeared (chart 3), hospitalizations have fallen (chart 4), and mobility restrictions have been almost completely removed. New cases, and occupancy of hospital beds and ICU beds are all at levels not seen since April 2020, only the second month after COVID-19 first made its appearance in the country.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.