ECONOMIC OVERVIEW

- While global markets pay attention to the Fed’s decision on Wednesday, our focus will be on Peruvian inflation data for January and Brazil’s central bank’s announcement that same day.

- The week will also feature a series of macro releases in Chile and Mexico reflecting the state of the local economies at the close of 2022.

- January CPI data for Lima out next week will reflect the impact of protests on supply chains and food prices.

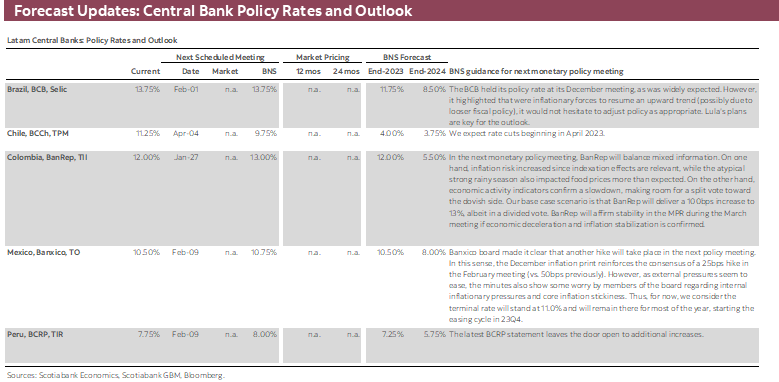

- We don’t anticipate any change to the BCB’s Selic rate, as the bank is set to leave it unchanged at 13.75%—amid anxiety-inducing comments from Lula on the institution’s independence.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

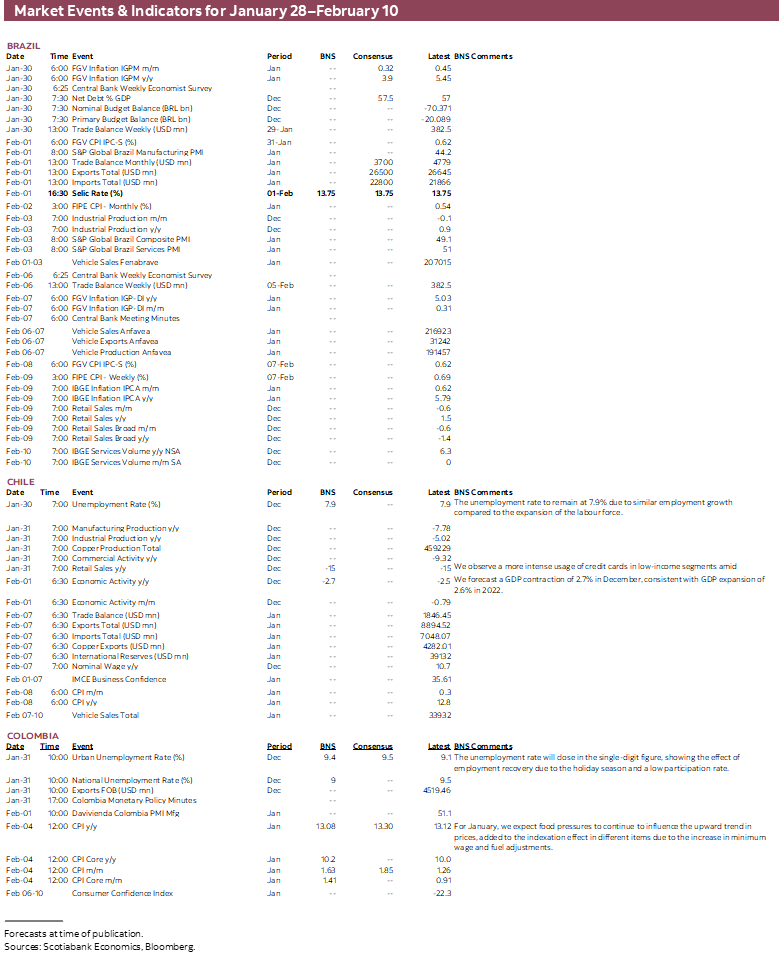

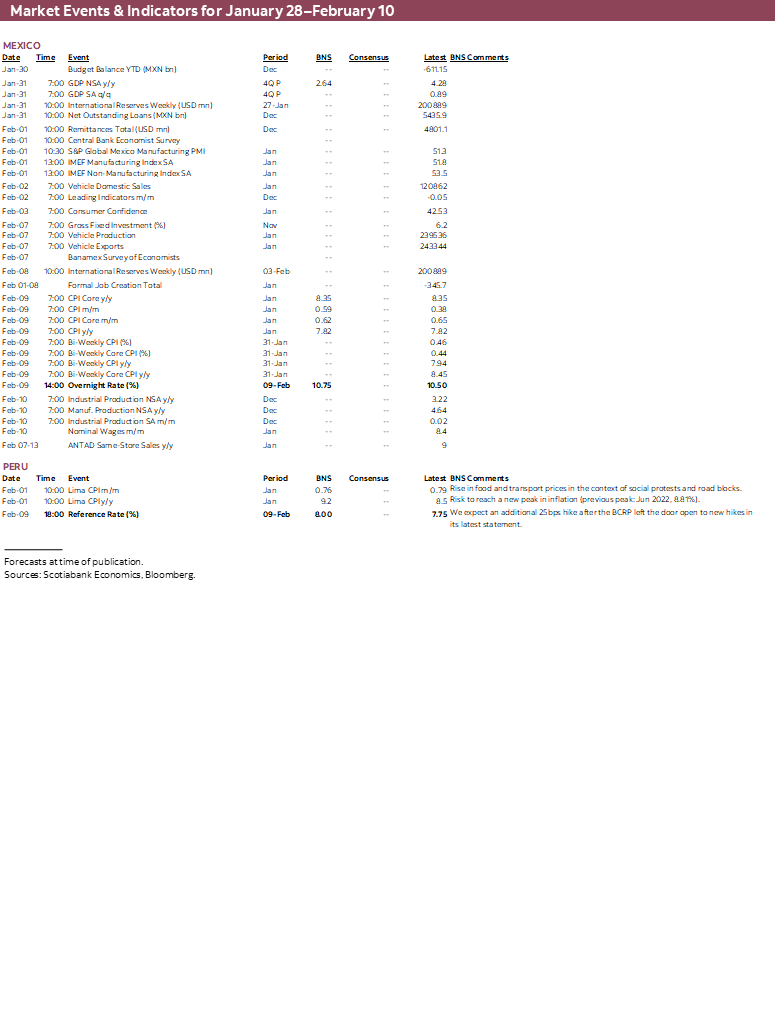

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period January 28–February 10 across the Pacific Alliance countries and Brazil.

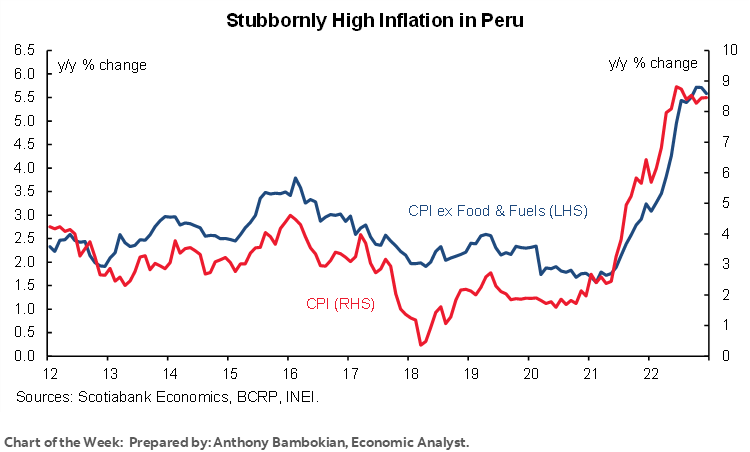

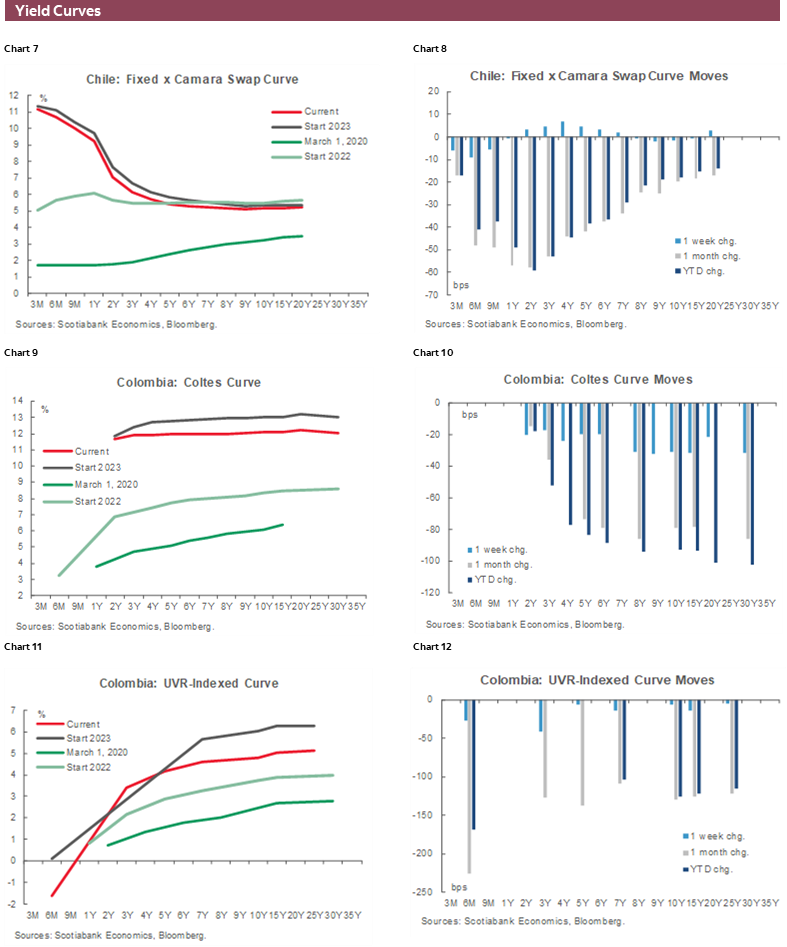

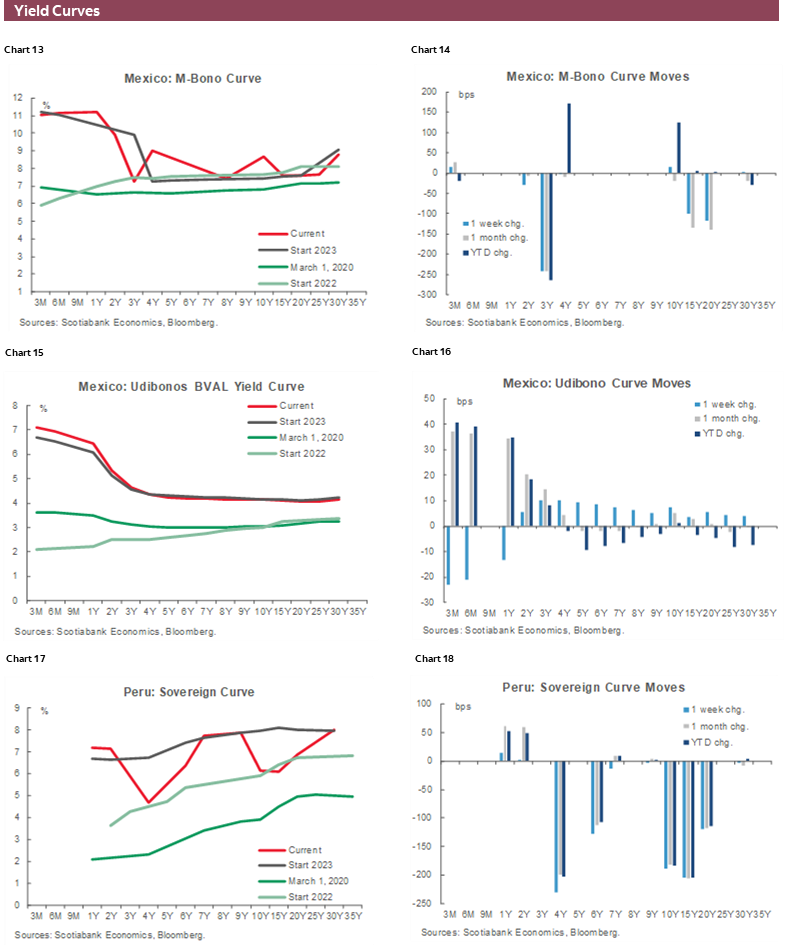

Chart of the Week

ECONOMIC OVERVIEW: PERUVIAN INFLATION; BCB DECISION; COLOMBIA’S POLITICAL ROADMAP

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- While global markets pay attention to the Fed’s decision on Wednesday, our focus will be on Peruvian inflation data for January and Brazil’s central bank’s announcement that same day.

- The week will also feature a series of macro releases in Chile and Mexico reflecting the state of the local economies at the close of 2022.

- January CPI data for Lima out next week will reflect the impact of protests on supply chains and food prices.

- We don’t anticipate any change to the BCB’s Selic rate, as the bank is set to leave it unchanged at 13.75%—amid anxiety-inducing comments from Lula on the institution’s independence.

While global markets pay attention to the Fed’s decision on Wednesday, our focus will be on Peruvian inflation data for January and Brazil’s central bank announcement that same day.

The week will also feature a series of macro releases in Chile and Mexico reflecting the state of the local economies at the close of 2022 (see the respective country’s sections). In Colombia, we’ll read through BanRep’s meeting minutes for its January 27 decision to better judge the path ahead for rates in the country; we expect BanRep to hike by 100bps in its policy announcement later today. In today’s Weekly, our economists in Bogota discuss the political backdrop in the quarters ahead.

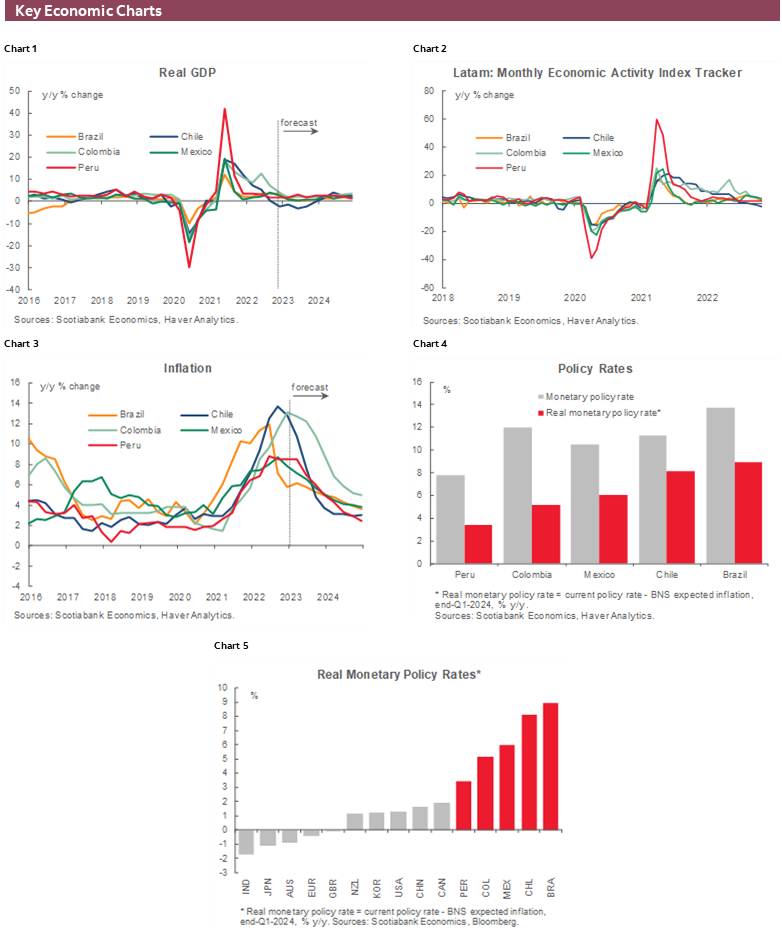

As we highlighted in Wednesday’s Latam Daily, January CPI data for Lima out next week will reflect the impact of protests on supply chains and food prices. There is a decent chance that these upside pressures will see inflation climb past what we thought had been the cycle peak in June 2022, when it printed 8.8% y/y.

Overall, inflation remains stubbornly high in the country—even abstracting from the impact of the protests—which is set to keep the BCRP at the ready in case there is no clear sign of decelerating price gains (see Chart of the Week). Our team in Peru forecasts headline inflation at 9.2% y/y and 0.76% m/m.

We don’t anticipate any change to the BCB’s Selic rate, as the bank is set to leave it unchanged at 13.75%—this is a widely held view among economists with no obvious reason to shift in either direction (yet, at least in the case of cuts).

Lula’s comments doubting the need for an independent central bank have caused some anxiety, and there's a risk that he chooses to replace the BCB’s Mon-Pol Director Serra in coming weeks with someone that may be more amenable to a loosening of policy sooner rather than later. Mid-month inflation data released earlier this week showed only a marginally lower rate of year-on-year price gains, at 5.87%, and edged past the median bi-weekly estimate submitted to Bloomberg, coming in at 0.55% vs 0.51% expected.

The BCB is in no position to cut rates yet as it assesses the impact on prices of the Lula administration’s social support programmes. Markets feel the same way with rate cuts not seen until the final quarter of 2023.

Note that the global calendar for next week doesn’t quiet down all that much after the Fed, with the ECB and BoE also set to increase rates by 50bps the following day—with the former, in particular, expected to stick to a hawkish tone.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Weak Economic Activity Figures and Appreciation of the CLP Would Support the Fall in Annual Inflation in the Coming Months

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

On Monday, the statistical agency (INE) will release unemployment data for the quarter ending in December, which we expect to show an unchanged jobless rate of 7.9% due to comparable increases in the labour force population and employment. The weakness of the labour market continues despite the government’s support for formal employment, having extended the Labour Emergency Family Income (IFE laboral) until June 2023, a policy that aims to generate 600,000 new formal jobs. According to our estimates, the delay in the execution of public investment in 2022 resulted in a failure to create more than 100,000 formal jobs last year. In this sense, it will be relevant to accelerate the pace of execution of public investment in 2023 to support the labour market.

At mid-week, the central bank (BCCh) will release GDP figures for December, where we see a contraction in output of 2.7% y/y, to result in a 2.6% annual GDP expansion in 2022. According to our estimates, we will see a decrease in non-mining GDP compared to the previous month, led by losses in all economic sectors. Our baseline scenario considers contractions in monthly GDP growth during the first half of 2023, which would partially reverse in the second half of the year. With this, we forecast a 1.7% drop in GDP in 2023.

In a scenario of a weak labour market and an economic contraction, paired with a multilateral appreciation of the CLP in recent months, we continue to see an aggressive cut in the monetary policy rate at the April meeting. In our view, 2-year inflation expectations will be close to 3% and the main drivers of inflation will continue to signal a slowing in y/y inflation towards the BCCh’s target.

Colombia—A Busy Legislative Agenda is About to Start in Colombia

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

The year has started very positively for local assets. The country’s nominal yield curve had fallen by more than 60bps in the YTD (to January 25), while the USDCOP is at its lowest since October 2021, showing that markets received new issuance very well (COLTES 2033 and the 10y global bond).

On the macro side of the ledger, economic activity remains robust. However, it has begun to show a healthy moderation as households rearrange spending given the impact of high inflation and high consumer credit borrowing rates. In the case of inflation, prices will exhibit higher persistence amid the harsh rainy season that puts supply chains under pressure in an area of the country that is a key producer of some food products. However, at Scotiabank Economics, we still see a high likelihood that a ceiling in headline inflation will be reached in Q1-2023 due strong statistical base effects (see previous Weekly). That said, BanRep is probably in the final stages of the hiking cycle, but this will need to be confirmed by the behaviour of inflation in coming months.

As for local politics, 2023 is a key year for the government. Regional elections will take place on October 29, following a crowded political agenda presented by the government that will start to be discussed in February. That said, Congress was called for extraordinary sessions starting on February 6, which increased the number of legislative weeks from 13 to 19. In February, they expect to present National Development Plan to have final approval by May; this discussion will be in parallel to the debate about the budget top-up, which is expected to conclude in April. Both proposals are essential to know the direction of the government’s programme and the use of the additional tax collection from the tax reform.

In the case of reforms, the first to be discussed will be the Health Reform. The government will send the proposal to Congress in February (debates in March/April). We think that despite the health reform not being a direct market mover, it will prove how strong political support for the government is.

Pension and labour reforms will be sent to Congress on March 16; both complete the picture for a busy first legislature. Regarding the pension reform, we don’t have new information. The only new news was from Ocampo speaking in Davos, giving some indirect clues that the government is possibly discussing changing parameters such as the retirement age, contributions, etc. That said, we must wait and see for the official draft.

It is important to say that Colombia is an expert in discussing fiscal reforms. Still, we don’t have the same ability to discuss health, pension, and labour reforms, since those topics have been, by tradition, sensitive points in Colombian politics. It depends on the government’s communications strategy if the discussion noise negatively impacts markets. For now, the Finance Ministry has emphasized that all reforms must comply with a fiscal responsibility framework. Let’s see how the conversation goes and how the markets take all these developments.

Mexico—Most Recent Data Seem to Put Banxico at a Tougher Junction—Is that the Case?

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

The most recent Mexican data seems to put Banxico at a tough junction, with growth slowing much faster than anticipated in November (the IGAE monthly GDP proxy fell from +4.41% y/y to +3.28% y/y, contrasting with a consensus expectation of +3.95% y/y), while inflation quickened. CPI data for the first half of January showed not only headline, but also core inflation edging in the wrong direction, with headline climbing 8bps to 7.94% y/y (putting it 2X the top of Banxico’s tolerance interval), and core rising 11bps to 8.45% y/y. However, despite this undesirable turn in data, we tend to agree with Deputy Governor Heath’s assessment that even though data is not fully conclusive, we’ve likely seen the peak in inflation.

It was also noteworthy that new board-member Omar Mejia made some of his first public comments on January 25th, stating that in the upcoming February 9th meeting, Banxico’s major driving factors will be the recent inflation print, as well as the Fed’s own decision. That link to the Fed seems to suggest that decoupling from the Fed is not yet in sight, even though we do anticipate it to take place as we head towards H2-2023. Omar Mejia, the new member of the board is considered to be a mentee of Deputy Governor Galia Borja, and we perceive he is not expected to deviate from the mid-point of Banxico’s board in the hawk-dove spectrum. With that in mind, his appointment likely tilts Banxico’s needle marginally towards a more hawkish bend in its discourse relative to December 2022, but we’d argue it has no implications to monetary policy decisions in the coming year, as Esquivel was a lonely voice in the board over recent months and lacked the voting power to sway the board’s decisions (even though we think it’s noteworthy to point out Esquivel was among the boards strongest defenders of the central bank’s independence).

What does this mean for Banxico’s monetary policy in the looming February 9th meeting? We think the deterioration in the data, alongside new Deputy Governor Mejia’s comments suggest that decoupling is off the table for at least February’s meeting, and potentially even the March 30th MPC decision. US swaps are pricing in a 98% probability that the Fed’s next move will be a 25bps hike (with marginal odds of a +50bps move), which would support the view that Banxico will follow on its heels 8 days after. Similarly, US swaps are placing 80/20 odds between another +25bps by the Fed on March 22nd, and a hold. That second decision for Banxico could be the one where Banxico deocuples and holds, but the recent turn in inflation reduces those odds in our view.

Peru—Roadblocks are Affecting Inflation Dynamics

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The state of political turbulence is having a material impact on the economy, in particular on GDP growth and inflation, as well as on the political calendar.

On Wednesday, February 1, the inflation figure for January will be released. We expect yearly inflation to shoot up to above 9% in January, from 8.5% in December. The protests, and more specifically, the roadblocks, have changed the dynamics of inflation since December. We had expected inflation to decline in December, January and February, and instead inflation rose in December, and is likely to rise to a 9.0%–9.5% range in January–February. Domestically produced agricultural prices make up the bulk of price increases. These are products that are most vulnerable to roadblocks, although low productivity due to lack of fertilizer and below par rains share part of the blame.

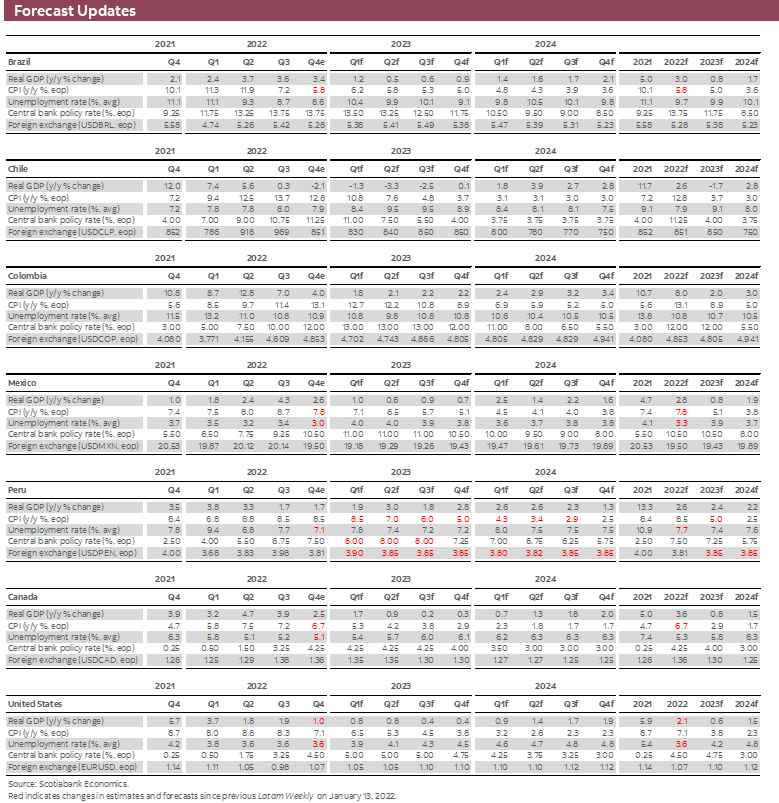

Inflation is likely to rise again in February, as some of the impact of January price increases will spill into the following month. We continue to expect inflation to decline beginning in March, due to a high y/y base, but the impact on domestic cost structure of higher inflation at the start of the year will raise the trajectory for the rest of the year. As a result, we are raising our full-year 2023 inflation forecast from 4.5% to 5.0%. This is above market consensus, which generally has inflation below 4.0% for 2023, although we expect this to change soon.

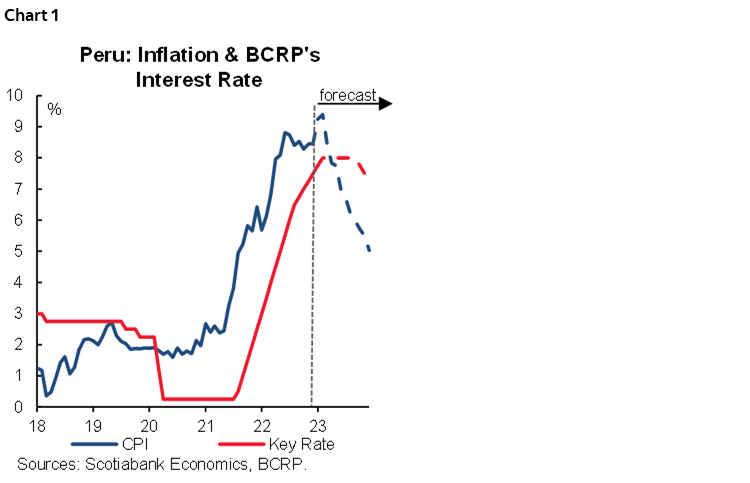

Given our expectation that inflation will escalate in January–February, we now expect the BCRP to raise its reference rate to 8.0% at its February meeting, up from 7.75% currently (chart 1). We continue to revise our view on the reference rate on a month-to-month basis, given price uncertainty and indeterminate guidance by the BCRP.

One of the issues the BCRP must also be contemplating is the impact of political turbulence on GDP. Our GDP forecast is under review, as we now see compelling downside to our current forecast of 2.4% growth in 2023.

The protests continue to be contained to the southern portion of the country, where tourism, transportation, public investment and commerce have been disrupted. Mining operations have been affected partially. Four mines have been under duress of some nature, including Minsur, Antapaccay, Las Bambas and Constancia. The Minsur tin mine has halted production, output is reduced at Antapaccay, while Las Bambas has announced that the roadblocks may begin affecting production within days, as the company cannot access the inputs it needs. Incidents were reported at Constancia (Hudbay), but we understand that production continues. Other large mines in the south, including operations at Cerro Verde, Cuajone and Toquepala (Southern Peru) and the new Quellaveco mine, have not reported incidents.

Meanwhile, we are now receiving reports that the roadblocks are affecting the agroindustry in the important Ica region. A number of large companies have stated that it is likely that they will not harvest production under current conditions in which roadblocks would prevent the harvested output from being taken to port for export.

The Ministry of Finance claims that the protests have caused a loss in production amounting to over USD500mn over the December–January period, of which a little over half corresponds to January. This would represent approximately 1.7ppts of growth. Given that our GDP growth forecast for January was 2%, we would now be looking at nearly nil GDP growth in January. Note, however, that the Ministry of Finance has not changed its forecast range of 3.1% to 3.9% GDP growth for full-year 2023. The Ministry of Finance has reiterated its intention to accelerate infrastructure investment.

The political turbulence is subsiding very slowly, but is still loud enough to impact the political calendar. This week Congress voted in favour of moving forward the beginning of the next legislative session from March 1 to February 15. Presumably, this would be with the view of expediting the process to move the 2026 elections to April 2024. At the same time, Congress is under pressure to move the elections forward even more, to December 2023. The issue is that this would mean having to start from scratch in the approval process, from the introduction of legislation, to a first Congressional approval, and then a second one. This process would take longer, which makes it politically more difficult. For now, a second congressional vote to allow for early elections to be held in April 2024 appears to be the path of least resistance.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.