- Colombia: BanRep is expected to hike 100bps; meanwhile, annual headline inflation is seen at its lowest level in six months

- Mexico: Inflation edged up unexpectedly in the first half of January

- Peru: Inflation could be around 9% in January

The overnight session is ushering a loss in US equity futures of about 1% for the S&P500 from yesterday afternoon after weak cloud business guidance from Microsoft. There were no major drivers for the global market mood overnight. Crude oil is unchanged at writing after some short-lived choppiness in early European dealing, while copper trades a touch weaker against practically flat iron ore prices.

The dollar is picking up a more mixed feeling as we head into the North American session after a more favourable Asia session as US yields somewhat steady after heading lower with the London open. The CLP is giving up a sliver of yesterday’s gains after again (briefly) trading under the 800 pesos per USD mark earlier today with the BCCh’s ongoing USD forward sales weighing on the USDCLP cross on Tuesday. The key 800 pesos level should act as a near-term floor. Meanwhile, the MXN is unchanged on the day after trading in a narrow band overnight while the BRL starts out the day with a respectable 0.5% gain.

Mexican economic activity widely missed estimates in data for November released this morning. Output in the country contracted 0.45% m/m, or about 0.3ppts weaker than the median forecast to Bloomberg, translating into a 3.28% y/y increase falling short of the consensus estimate of 3.95% y/y. The monthly decline is the largest seen since August 2021 (then, a huge 1.55% m/m drop) and follows flat activity in October after three decent growth months.

This isn’t the freshest data, considering that yesterday’s bi-weekly H1-Jan CPI is a more relevant print for Banxico than a stale November IGAE reading. But, it does somewhat complicate the hawkishness that had built after the inflation print (see Mexico section below). The weakness for the month was led by the services sector with a massive 0.94% m/m contraction (again, one has to go back to August 2021 for the most recent weaker month for the sector). Across services, weakness was relatively widespread across tertiary sectors but hotels and restaurants, wholesale and retail trade, and transportation and warehousing services seem to have had a particularly bad month. We’ll see where economic data come in over the coming months, but for now Banxico will likely set today’s print aside and focus on the upside risks to core inflation reflected in yesterday’s inflation release.

In the day ahead we’ll watch developments in Peru (as is customary) after the country’s Congress extended the deadline to make a decision on an early election to February 10. Pres Boluarte highlighted that she does not intend to cling to power and hopes that a decision on necessary election reforms is made soon; she also again called for a “national truce” to solve differences with protesters. Our Peru economists highlight comments from Fin Min Contreras on the government’s expectations for inflation—set to accelerate in January due to protests-related disruptions. Contreras also put at over PEN2.1bn the economic impact since December from the protests (roughly 0.2ppts of GDP).

—Juan Manuel Herrera

COLOMBIA: BANREP IS EXPECTED TO HIKE 100BPS; MEANWHILE, ANNUAL HEADLINE INFLATION IS SEEN AT ITS LOWEST LEVEL IN SIX MONTHS

January’s Citi survey, which BanRep uses as one of its guides on inflation expectations, the monetary policy rate, GDP growth, and the COP, was published yesterdays.

Highlights:

- Economic growth in 2022 is estimated at 7.74%, 0.19ppts below the previous survey, probably reflecting that the economic slowdown will materialize in Q4-2022 GDP data due on Feb 15. For 2023, markets expect an expansion of 1.20%, slightly higher (+0.06pts) than seen in the previous survey. For 2024, growth is projected at 2.55%, down from the previous expectation of 2.72%.

- Inflation expectations deviated further from BanRep’s target range. January’s monthly inflation rate is expected to be, on average, 1.78% m/m and 13.27% y/y, which is an increase of 0.15ppts from the December reading, translating into the lowest acceleration in six months—showing that inflation may be hovering around a potential ceiling.

- Scotiabank Economics is below consensus with projections of 1.63% m/m and 13.08% y/y. In January, indexation effects and food costs will lead to upside price pressures. The rainy season has been historically hard for some Colombian regions, which would keep food prices elevated. Additionally, indexation to past inflation, indirect indexation of some labour-intensive services to the minimum wage, the expiration of some tax waivers in airfares, and higher gasoline prices will keep monthly inflation high.

- Consensus expects inflation to close 2023 at 8.78%, above the previous projection of 8.0%. Inflation is expected to continue to deviate from BanRep’s target range (defined between 2% and 4%) as inflation expectations for Dec-2024 are at 6.35%—significantly higher than the previous estimate of 4.62%.

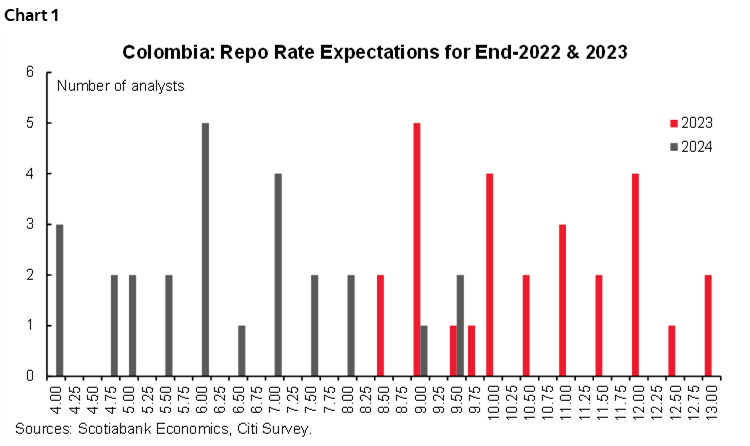

- For the January monetary policy meeting, 13 out of the 25 analysts in the survey expect a move of 100bps to 13%. Eight analysts see a 75bps hike and three analysts are calling for a 50bps hike. Medium-term expectations are very dispersed; for December 2023, expectations range between 8.5% and 13%, the mode is at 9%, while the median is at 10.50%. For December 2024, estimates sit between 4% and 9.50%, with both the mode and median response at 6% (chart 1).

- Scotiabank Economics has an official call for a 100bps increase in January to 13%. Although the board can remain data dependent, we expect this hike to be the last one of the hiking cycle.

- USDCOP forecasts for December 2023 is at 4,767 pesos with an appreciation in the peso to 4,649 in December 2024.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

MEXICO: INFLATION EDGED UP UNEXPECTEDLY IN THE FIRST HALF OF JANUARY

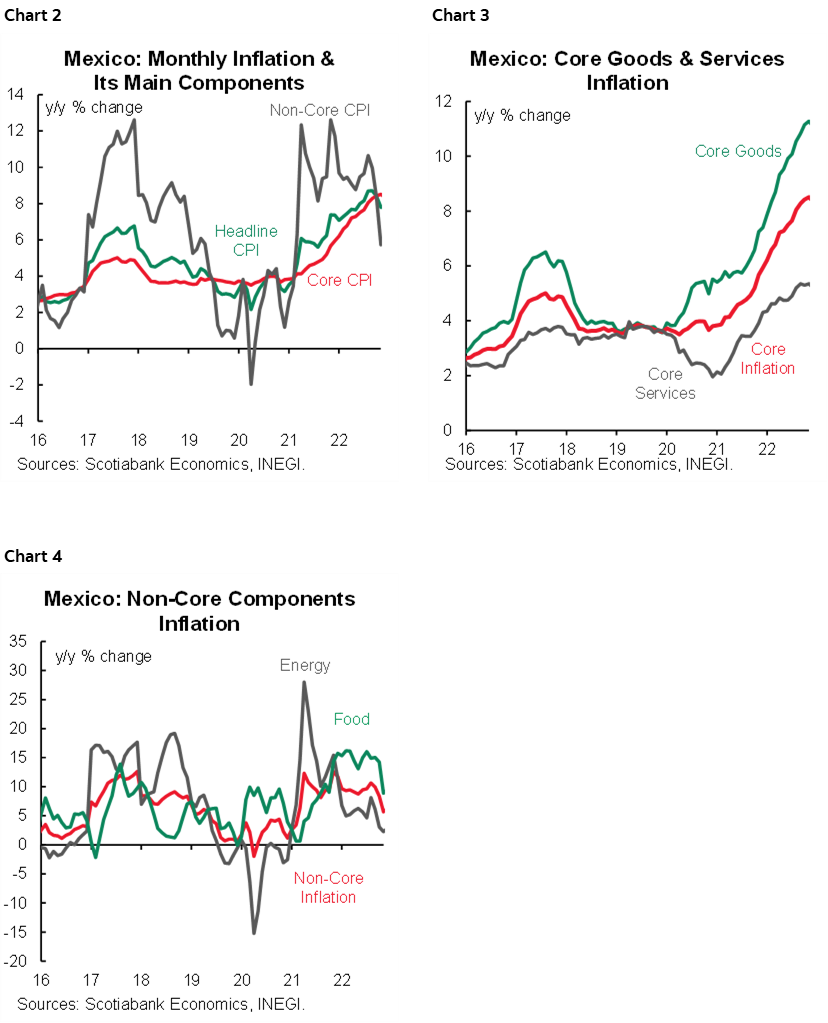

Inflation surprised to the upside as it edged up in the first fortnight of January. Headline inflation came in at 7.94% (chart 2), above 7.86% previously and the 7.85% seen by consensus. Core basket prices also soared, to 8.45% (chart 3) from 8.34% (vs 8.32% consensus). In particular, services inflation continues on the rise, going from 5.17% to 5.47%; on the flip side, that for merchandises marginally decelerated to 11.02% (from 11.10%). However, the non-core item (chart 4) slightly moderated from 6.46% to 6.44% despite higher commodities prices. Food moderated from 9.99% to 10.20%, and energy prices rose from 2.63% to 2.79%; despite the increase, we believe fiscal subsidies could have absorbed the shock on oil due to higher energy prices, as it happened a year ago.

On a 2w/2w basis, headline inflation went from 0.10% to 0.46%, above the 0.38% consensus. Core inflation also beat expectations, going from 0.19% to 0.44% (vs 0.32 expected). Non-core item rose from -0.19% to 0.51%.

As the minutes of the last Banxico meeting noted, uncertainty regarding inflation remains high, and this latest print considerably above consensus shows that risks are still biased to the upside. The possibility of diverging inflation trajectories in the US and Mexico also lights up the incidence of internal upside risks. De-anchoring expectations is also a source of concern for Banxico’s board. In this sense, after the bi-weekly reading, year-end analysts’ forecasts could show upward revisions, suggesting some stickiness in both core and headline trends. In particular, the Citibanamex survey showed a 5.08% year-end consensus for 2023 headline inflation (4.98% previously), and 4.07% for 2024. In monetary policy implications, for now, we remain with our view of a 25bps hike in February and reiterate our view of an 11.00% terminal rate, after a final hike in March. However, we also acknowledge some risks to the upside for both the terminal and year-end rate (10.50%). We will reassess with incoming inflation data; the next print is released on the same day as Banxico’s decision, on the 9th of February.

—Miguel Saldaña

PERU: INFLATION COULD BE AROUND 9% IN JANUARY

Finance Minister Alex Contreras noted that inflation in January will be high because of the current social unrest that also boosted inflation in December. However, the minister considered that the increase in food prices that has been observed so far this month will be temporary. According to the MoF, year-on-year inflation will be between 8.8% and 8.9% in January, higher than the 8.5% posted at end-2022, which would translate into a new inflation peak, exerting greater pressure on monetary policy. Our monitoring of key prices suggests that inflation could even exceed 9% for the current month.

Until now, the BCRP, like us, considers that the peak of inflation was seen in June 2022 (at 8.8%). Inflation has been on a downward trajectory since then, but not as steeply as expected. The recent social protests have had an impact on the economy, inflation, and the exchange rate, while their duration is still uncertain. The MoF indicated that the impact on prices should be reset in the coming weeks, but this to us more than a projection seems like wishful thinking.

This could mean a higher starting point for our inflation forecast for the year, so our projection of 4.5% at end-2023 faces upside risks.

The government has been crafting subsidies for the most vulnerable sectors of population, raised the Christmas bonus in the last December, and will seek to generate employment with the "Impulso Perú" and "Con Punche Perú" programmes to cushion the negative impact on the purchasing power.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.