Next Week's Risk Dashboard

• Trump’s condition

• US stimulus talks

• Wave 2 tracking

• Brexit meeting

• Canadian jobs

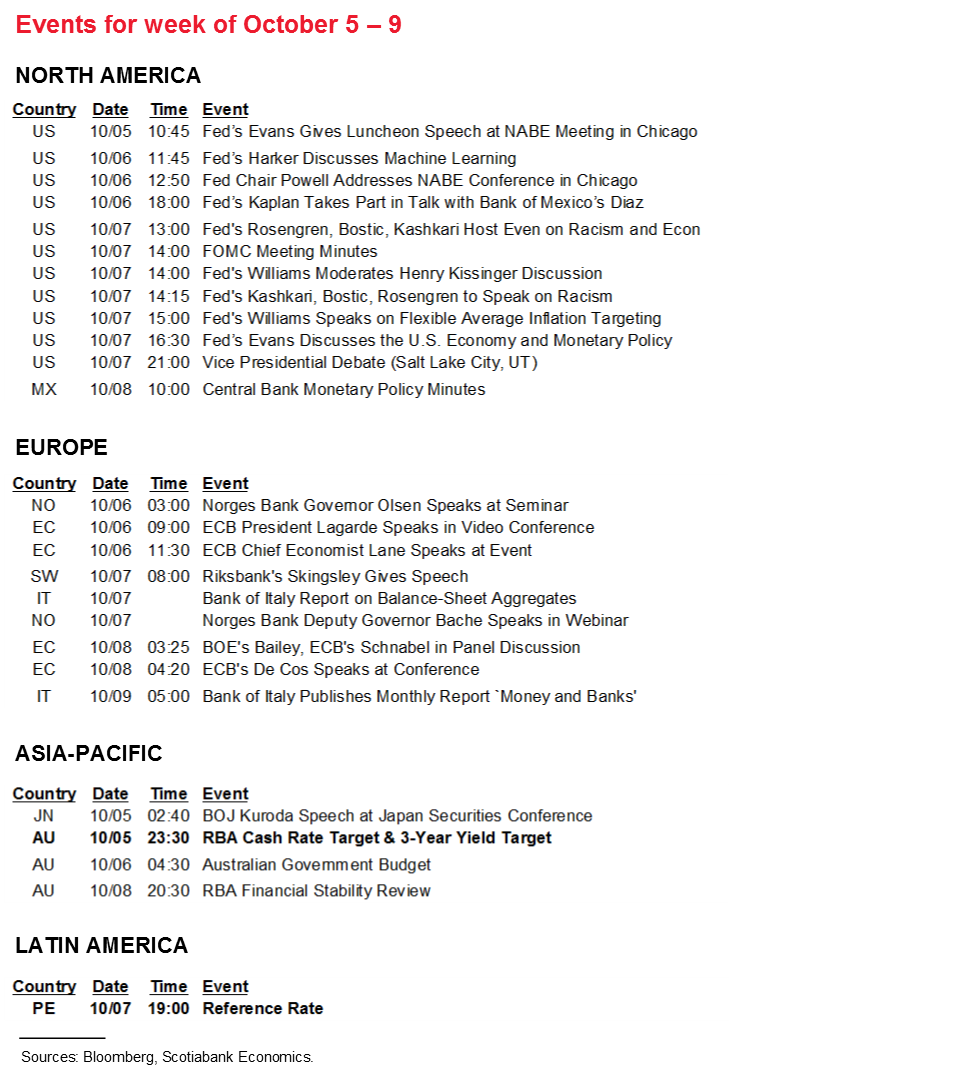

• BoC’s Macklem

• FOMC minutes

• Germany’s economy

• UK economy

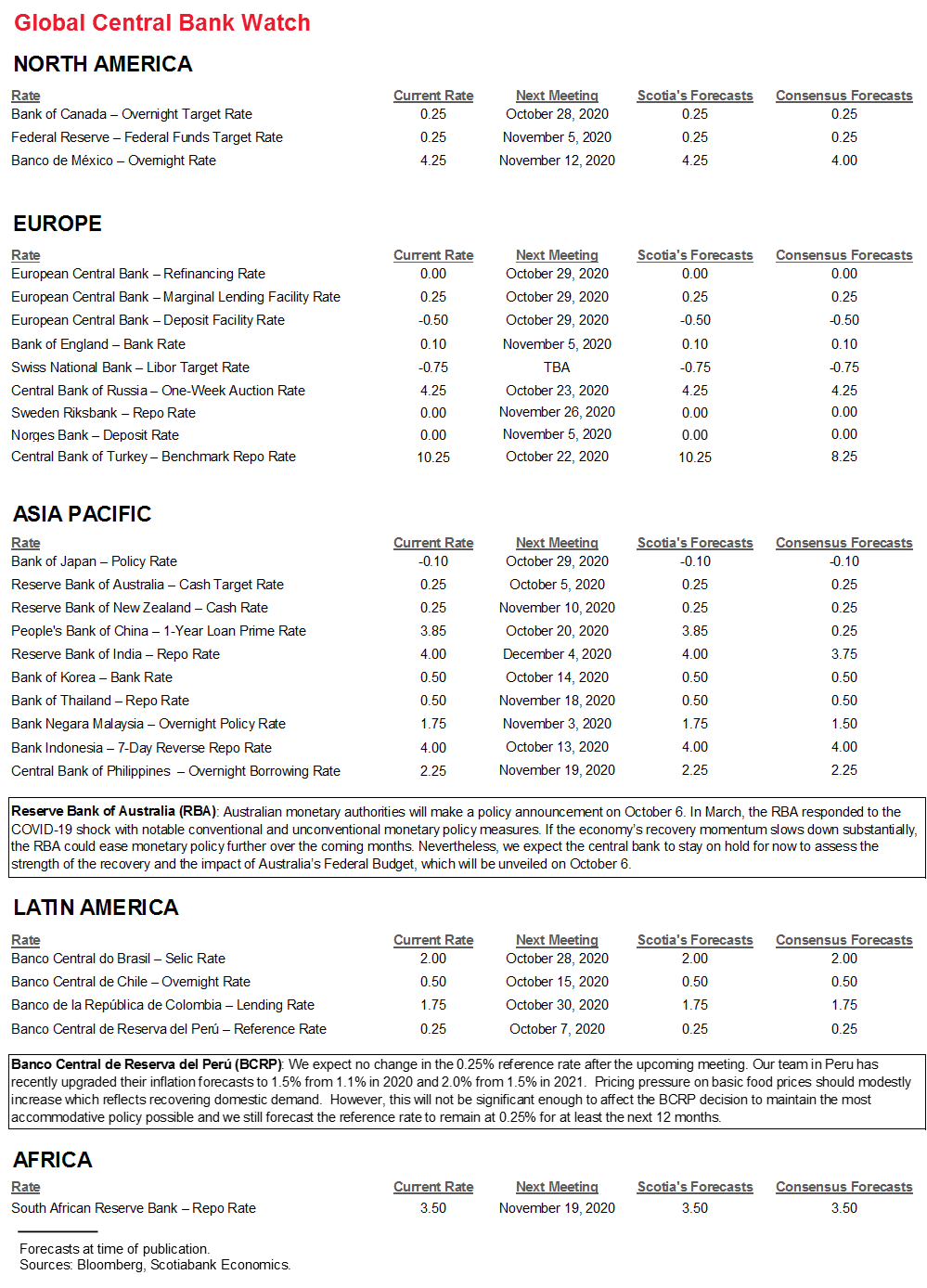

• CBs: RBA, Peru

• ECB-speak

• CPI: Brazil, Chile, Colombia, Mexico…

• …SK, Philippines, Taiwan, Norway

Chart of the Week

The start of a new trading week could be informed by several material developments. One will be ongoing negotiations toward a US fiscal stimulus package. Two will be a weekend Brexit meeting.

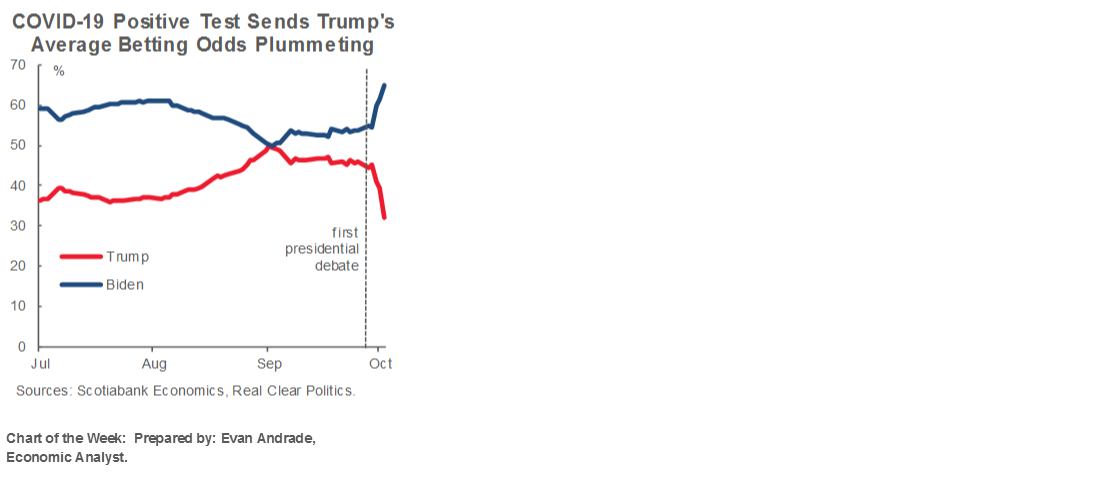

Third will be US President Trump’s condition and implications for the November 3rd election. Late on Friday he was admitted to Walter Reed hospital on medical advice for ‘a few days.’ He has developed a fever and was given the experimental antibody drug Regeneron under a compassionate use request. This is clearly not your standard go home and quarantine yourself order. The President’s age and general condition pose higher risks but he has privileged access to the best medical care and treatment. As depicted by Evan Andrade’s chart of the week on the front cover, market betting on the election outcome has been materially impacted and developments over the coming week could prove to be highly material to markets.

Then there are all of the other more calendar-based forms of global market risk over the coming week.

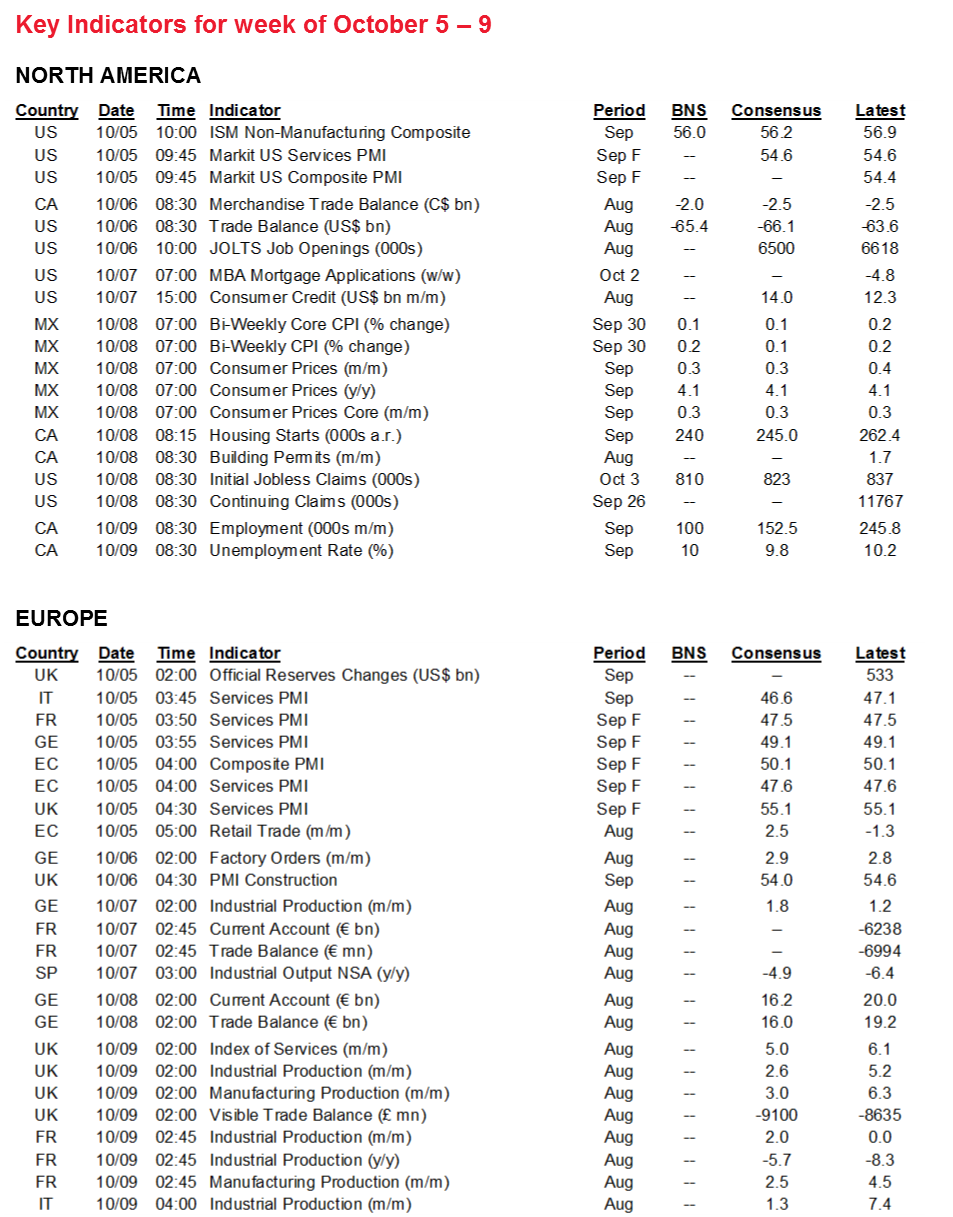

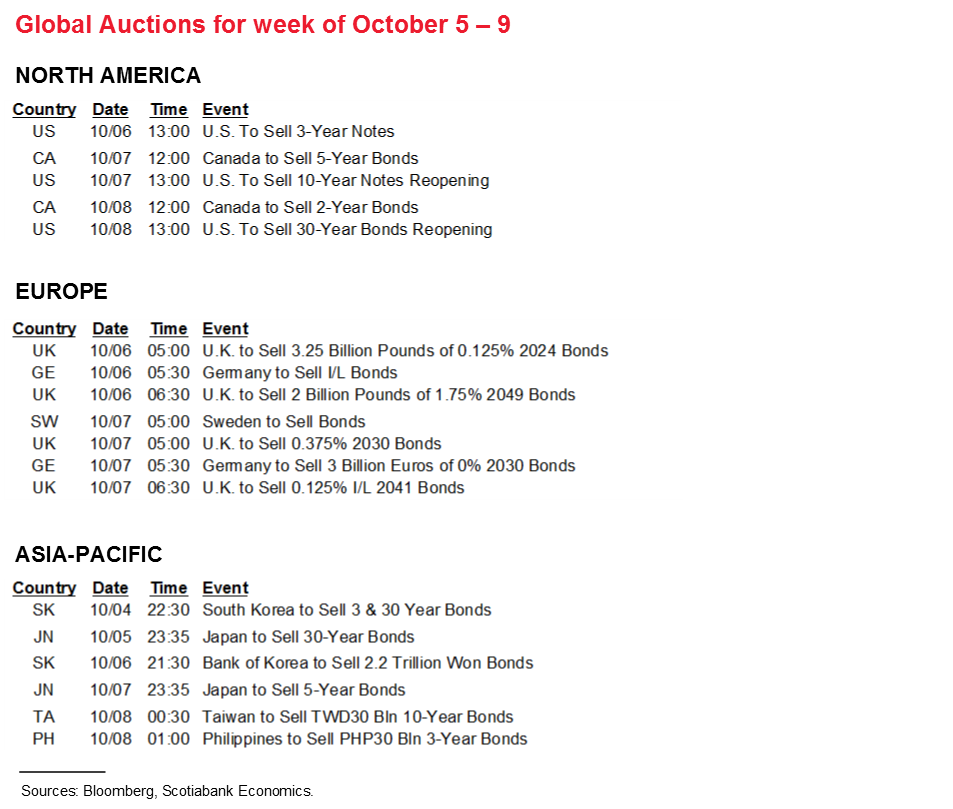

1. CANADIAN JOBS—RETURN TO SCHOOL EFFECT?

Canada releases job growth figures for September on Friday. I’ve pencilled in 100k with an unemployment rate of 10% for a mild improvement. We’ve already seen a material cooling in the pace of new job growth from 290k in May to 953k in June, 419k in July and then 246k in August which has generally mirrored the pace of reopening plans across the country.

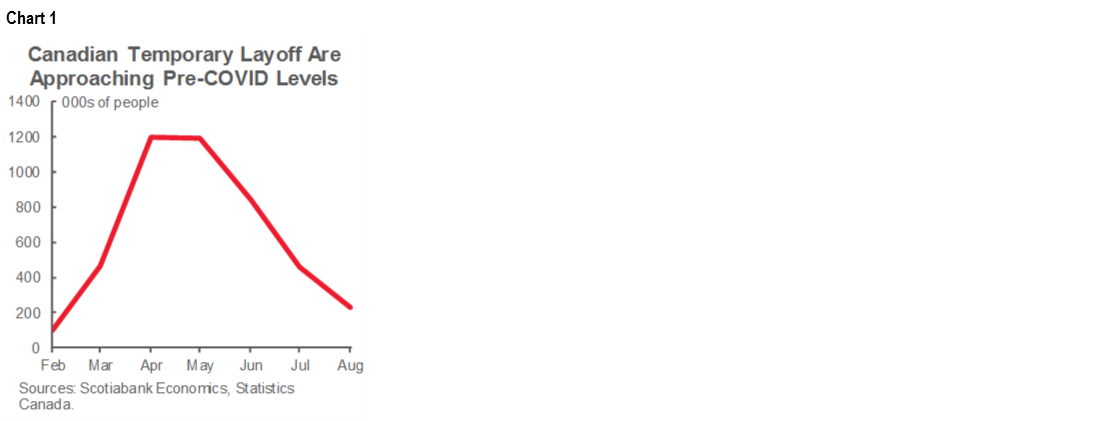

Like the US, the ranks of the temporarily unemployed have been thinned which suggests a waning callback effect (chart 1). Those on temporary layoff have fallen from a peak of 1.2 million in April to 231k in August. As the callback effect diminishes, the question becomes how many are getting jobs and how many are going on permanent layoff. Like the US (here), Canada is transitioning toward a period when continued job growth will have to be more reliant upon organic growth and much less so on returning furloughed workers.

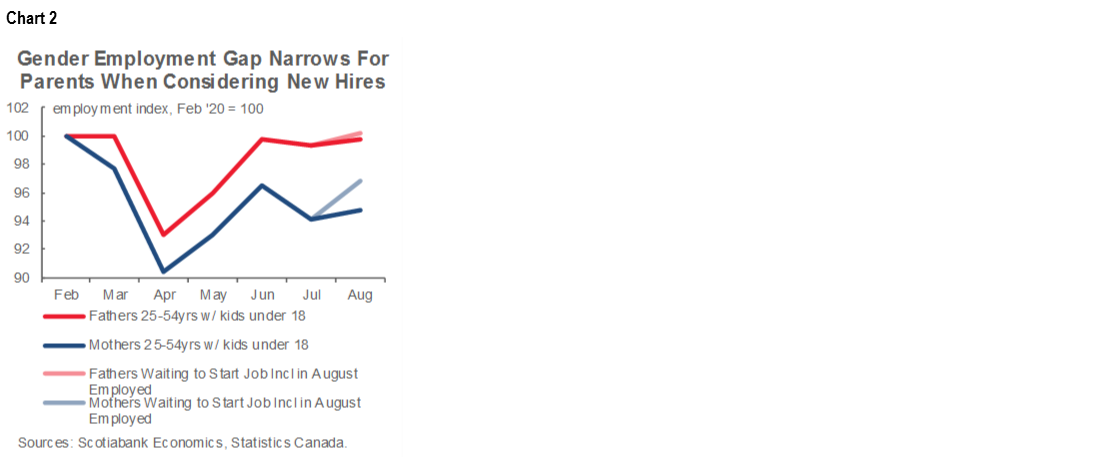

Unlike the US, however, Canada’s school year generally starts in September whereas it can start in August and September in parts of the US. This raises two possible and competing effects. One is whether sending the kids back will result in more women being able to accept work given the disproportionate gender effects (chart 2).

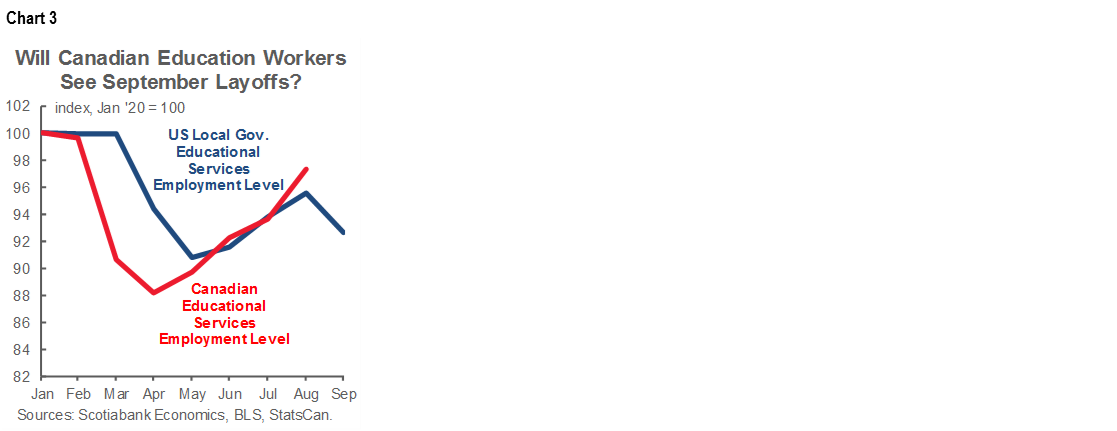

Second is how many teachers and other education sector workers returned this September. In recent years, September results in a seasonally unadjusted gain in education sector workers equal to around a quarter million jobs. Chart 3 demonstrates the correlation between movements in education sector jobs in the US and Canada this year. Canada’s education jobs fell earlier and harder than in the US during the first wave of COVID-19 cases as the country embraced earlier pre-emptive moves than the US generally pursued. Does the drop in US education sector jobs during September portend something similar north of the border? If so, then on a proportionate basis it could pose a drag effect on employment.

Markets may well have cause to fade the employment numbers, however, and for multiple reasons. One is the likely dominance of external global factors on markets over the coming week. Two is that Bank of Canada Governor Macklem will deliver a speech the day before that will be available by 8:30amET at a Global Risk Institute event (here). The topic will be known by early next week. See his interview in the Globe and Mail here. Last, backward-looking jobs numbers are likely to be relegated to the peanut gallery as market observers pay more attention to forward-looking growth risks including the one covered in the next section.

2. SECOND WAVES

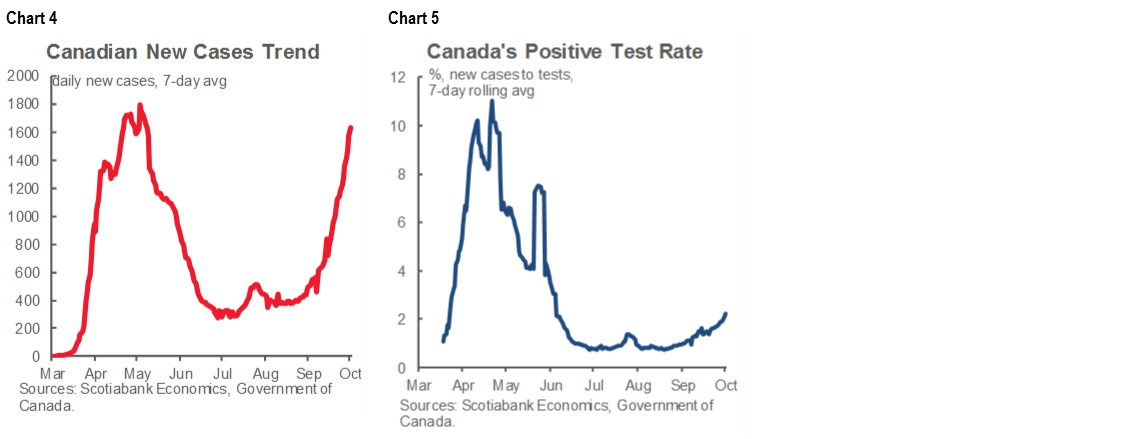

President Trump can at least be comforted that he’s not alone in getting caught up in a second wave of global COVID-19 cases. Multiple countries around the world are in a second wave. For example, charts 4–5 show the outbreak of cases north of the border in Canada.

Several points can be addressed. One is that cases are clearly trending sharply upward.

Two is that as I’ve argued previously it is misleading for some to argue that the only reason for this is increased testing frequency. For starters, the positive rate as a share of tests has marginally increased during wave 2. The bigger point is that you cannot compare wave 1 and wave 2 positive rates because the samples dramatically changed between the two periods. During wave 1, one could get a test if you were a health professional, symptomatic or had a reasonable probability of being exposed to someone who was, such as a family member. Because test kits were scarcer during wave 1, this intrinsically focused the pool upon people who were proportionately more likely to be infected. Thus, the higher rate of positive test results during wave 1 likely represented sample bias. During wave 2, testing kits became more readily available and restrictions relaxed such that the sample became less intrinsically biased toward infected individuals. Thus, we can’t answer the question whether the rate of positive incidence is higher, lower or about the same during wave 2 as it was during wave 1 without having identical sample characteristics over time which is impossible.

So this is where logic comes in. When the economy reopens and people get up in each other’s faces with a fraction still reticent to adhere to the advice of health professionals and common sense, would you not expect to see an upturn in cases that respect for data should not counsel ignoring?

In determining what to do about it, however, a delicate balance must be struck as reopening plans get suspended and rolled back to contain the spread of the virus but without doing the same degree of overall damage as during wave 1. The probability of a business surviving diminishes through serial shutdowns. The probability of much greater economic and social hardship marked by large scale bankruptcies and wider fiscal deficits rises with serial shutdowns.

3. US STIMULUS PLANS

As this publication is being distributed there is still no deal on another US stimulus package. Talks are continuing and the probability of success or failure may impact the Asian market open to start the week.

House Speaker Pelosi has flagged five areas of disagreement between the negotiators including jobless benefits, transfers to state and local governments, controls on funding for COVID-19 testing, tax credits for dependents and earned income and discretionary funding. She has stated that President Trump’s positive test may have positively influenced negotiations while others disagree. Members of the House of Representatives are now on recess and would have to be summoned back for a vote while members of the Senate will be on recess at the end of next week.

4. BREXIT

UK Prime Minister Boris Johnson and European Commission President Ursula von der Leyen will hold a video call this weekend on Saturday afternoon as Johnson has sought to achieve a trade and security deal by the October 15th European Council leaders summit in Brussels ahead of the December 31st crash out deadline. Fisheries and the quest for a level playing field to avoid either side harming the other’s competitiveness are the main sticking points. The outcome of their call may inform next steps in terms of Brexit risks into Monday’s Asian market open. It is a change of tactics with the UK PM embracing a direct hands-on role.

5. FOMC MINUTES

Exactly what happened at this meeting?! Maybe someone hogged all the red jujubes and left the icky green ones for everyone else. In any event, recall that the FOMC meeting on September 15th–16th introduced unexpected dissension in the ranks when two officials voted against the statement (recap here). This happened just three weeks after the virtual Jackson Hole symposium at which the revised Statement on Longer-Run Goals and Monetary Policy Strategy introduced more dovish overshooting language. One consideration will be whether debate and opposing views were somewhat more prevalent across non-voting FOMC members.

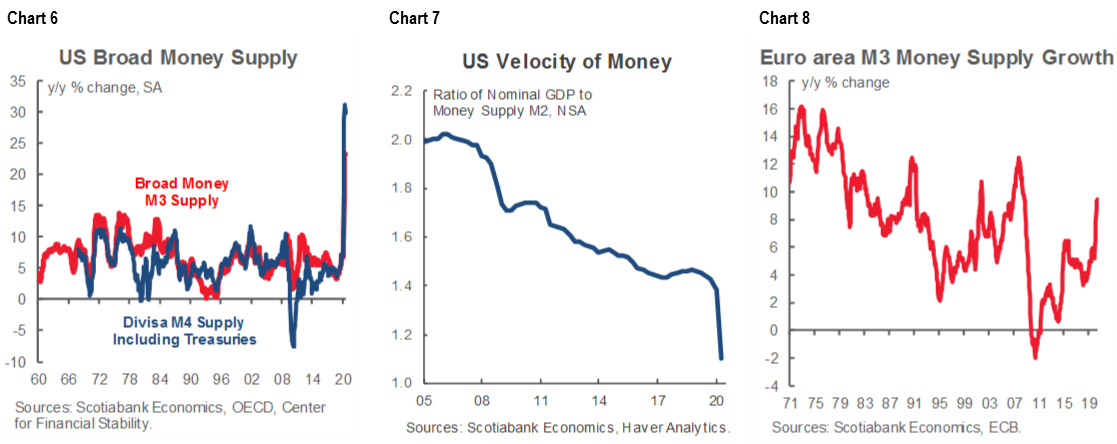

Markets may be sensitive toward any further indications that officials are not fully invested in an inflation overshoot. Minneapolis Fed President Kashkari for one still doesn’t sound convincing to me. There are multiple drivers of inflation risk, but the fastest rate of growth in broad money supply in at least six decades could be one avenue through which committee members may be hesitant to over-commit to relaxed inflation targets along a timeline marked by “we’re not even thinking about thinking about raising rates” (chart 6). Some of this growth in money supply is to offset a decline in the velocity of money (chart 7). Note, however, the key distinction between today and the Global Financial Crisis. Back then, the banking sector and balance sheet nature of the recession that brought deleveraging took broad money supply sharply lower, and the Fed’s balance sheet expansion only sought to fill this pit for a time. This may have played a role in limiting progress toward inflation targets post-GFC. Today’s pandemic shock posed a very different recession driver and policy response such that monetary policy has driven broad money growth toward the 25–30% range. If this turns out to be a transitory shock with an eventual vaccine waiting in the wings, then the monetary policy dialogue could well become more complicated particularly given evidence to date of a modest snap back in core inflation. By contrast, the Eurozone’s growth rate in broad money remains considerably weaker (chart 8).

6. EXTRA CREDIT

Two regional central bank decisions will pair up with ECB-speak and miscellaneous economic indicators to round out the week’s expected developments.

Rising case counts across much of Europe make tracking the recovery through backward-looking readings a tad moot perhaps, but the coming week’s focus will be primarily upon Germany and the UK. German factory orders are expected to continue rising in August’s reading (Tuesday), ditto for industrial output (Wednesday) and exports (Thursday). UK industrial output figures should also post further gains for August (Friday) along with that same day’s readings for the service sector, monthly GDP, construction output and trade. As UK covid-19 cases rise, so do downside risks to GDP growth (chart 9). Factory reports from Italy and France arrive that same day.

Only a handful of US releases are due out including ISM-services for September (Monday) that may face downside risk partly as reopenings get halted or rolled back in some parts of the country. Weekly jobless claims are expected to keep grinding lower on Thursday and watch JOLTS job openings for continued progress on Tuesday.

Canada will also update a few readings such as trade figures for August (Tuesday), the Ivey purchasing managers’ index for September (Wednesday) that covers both private and public sectors, and housing starts during September (Thursday).

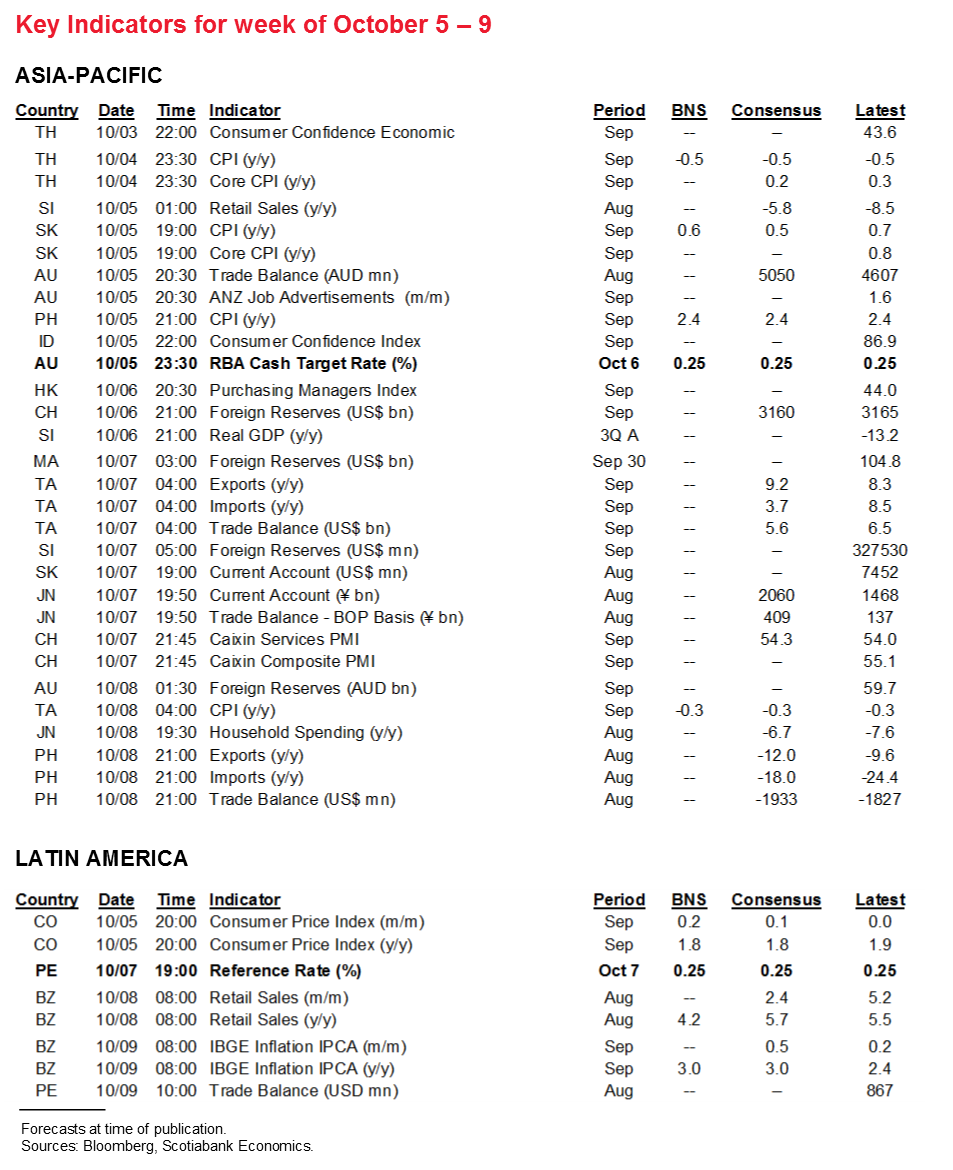

Peru’s central bank is expected to remain on hold at 0.25% Wednesday.

ECB-speak will bring out some heavy hitters including President Lagarde (Tuesday, Wednesday), the ECB’s Chief Economist Phillip Lane (Tuesday), and several other officials. Watch for broader reaction to the recent further weakening of Eurozone inflation.

A wave of inflation reports will arrive across Latin American and Asian markets. Colombia (Monday), Peru (Wednesday), Mexico and Chile (Thursday) and Brazil (Friday) will be joined by South Korea and Philippines (Monday) and Taiwan (Thursday). Norway will also update inflation on Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.