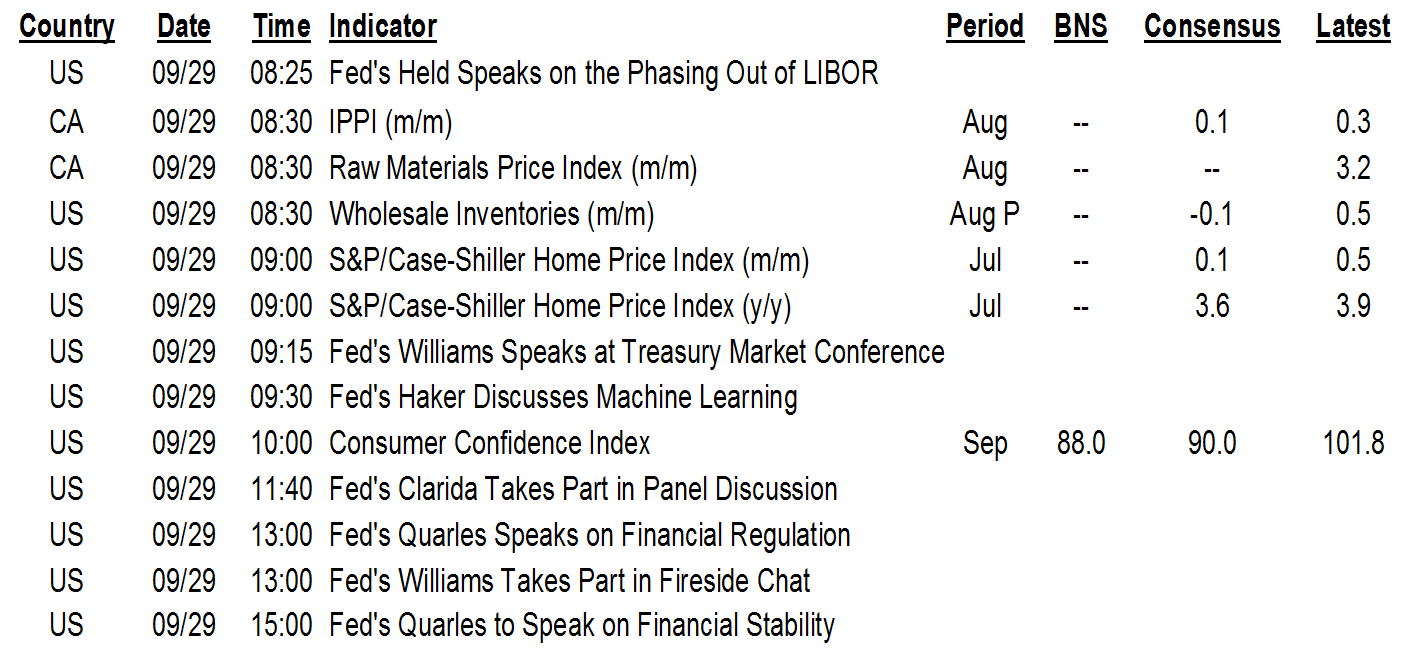

ON DECK FOR TUESDAY, SEPTEMBER 29

KEY POINTS:

- Risk-off sentiment driven by second wave, Presidential debate

- US consumer confidence rips higher…

- …with jobs plentiful supportive of nonfarm payrolls…

- …and most Americans saying they expect higher incomes

- Downside risk to Eurozone inflation buoyed by German figures

- Canada’s incidence of positive covid test results is rising…

- …but whether it is higher or lower than during wave 1 is unanswerable

- Wear your masks! The scientific evidence is overwhelming

INTERNATIONAL

A mild risk-off tone is taking back some of yesterday’s equity rally. There are few incremental catalysts. Calendar-based developments should be positive if anything, given strong US consumer confidence and slightly softer than expected German inflation that may buoy ECB easing bets. Markets may be more focused upon covid-19 risks and tonight’s first US Presidential debate. Ontario reported another 554 cases today and Quebec registered 799 cases. German Chancellor Merkel advised that the situation in Berlin is ‘serious’ and the UK registered a 40% rise in covid-19 deaths in England and Wales last week. CAD is getting caught up in the risk-off covid–19 and debate sentiment more than most along with the Mexican peso.

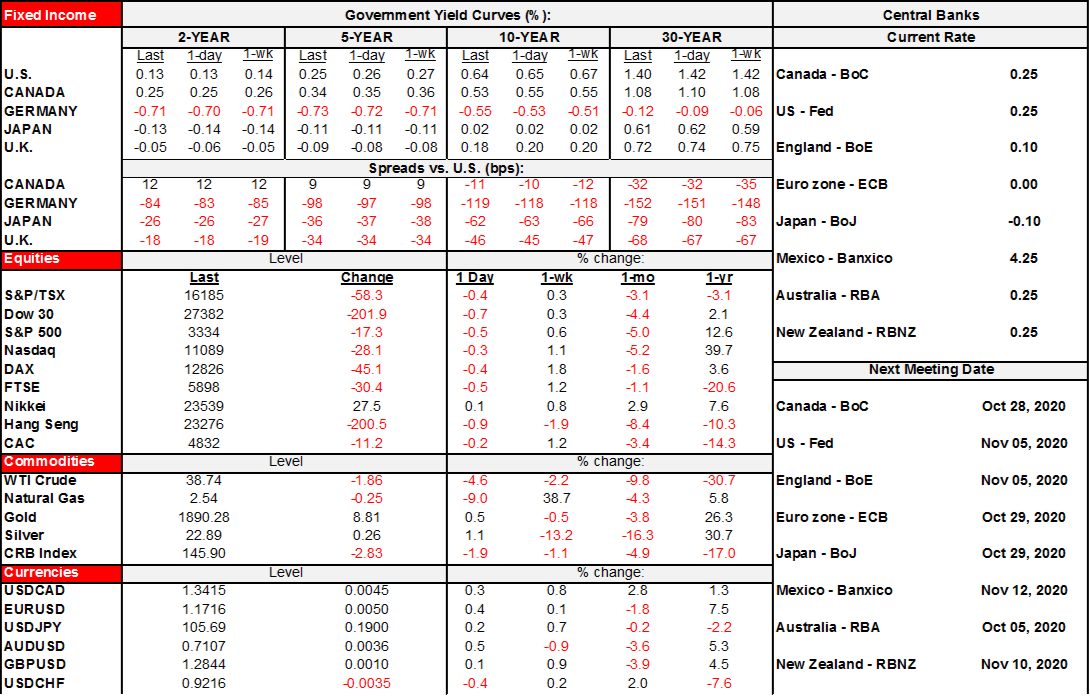

- Stocks are giving back a portion of yesterday’s rally. The US S&P500 is down by about ½% with the DJIA down ¾% and the Nasdaq is off by ¼%. The TSX is off by ½%. European cash markets are slipping by between ¼% and 1%.

- Sovereign bond curves are mildly bull flattening with 10 year benchmark yields down by 1–4bps across N.A. and Europe led by spread narrowing in Italy. The US and Canadian longer ends are dearer by 1–2bps.

- Oil prices are off by about a buck and a half in terms of both WTI and Brent. Gold is up US$11 to US$1892/oz.

- The USD is depreciating this morning, but unevenly so against the crosses. CAD and the Mexican peso are losing ground along with the yen as most other crosses appreciate.

German CPI inflation landed a touch weaker than expected at -0.4% y/y on an EU-harmonized basis (-0.1% prior, -0.1% consensus). This follows warning signs that emerged in state level data a few hours before this morning’s nationwide reading. Spanish CPI was unchanged at -0.6% y/y on an EU-harmonized basis. France and Italy release tomorrow ahead of Friday’s Eurozone add-up that may incrementally inform ECB risks.

UNITED STATES

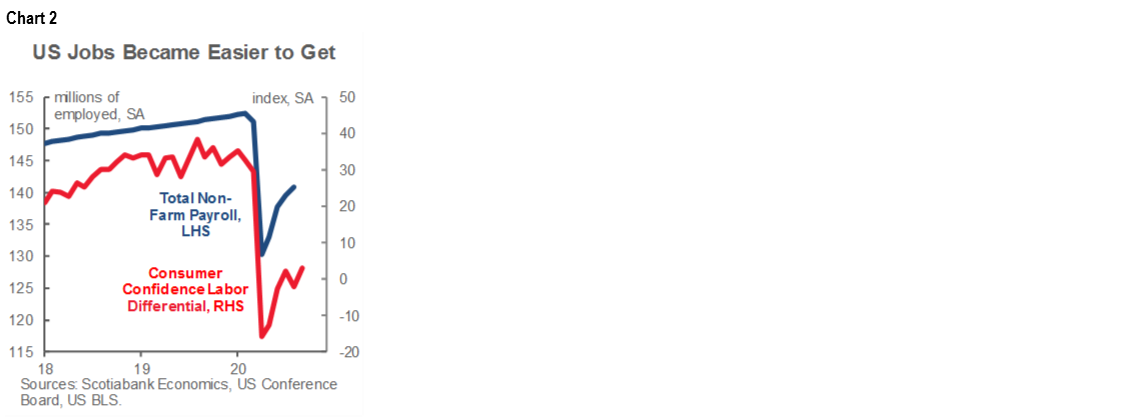

US consumer confidence came in considerably stronger than expected across headline results and details (chart 1). Markets ignored it, however, perhaps as they consider it to be further evidence of good news that downplays a sense of urgency within the GOP to negotiate further stimulus.

The Conference Board’s metric climbed to 101.8 from an upwardly revised 86.3 (previously 84.8) reading that smashed consensus expectations for a 90 print. The improvement was spread across the present situation (98.5, previous 85.8 revised up from 84.2) and expectations (104, from 86.6 revised up from 85.2) reading.

Two details are worth flagging. One is that Americans say jobs are more plentiful which is a positive signal ahead of Friday’s nonfarm payrolls given the rough correlation between the two readings (chart 2). Jobs plentiful minus jobs hard to get improved to +2.9 from -2.2 the prior month.

Second, the income components are supportive of the consumer sector. Not only did more people say incomes had increased in September than decreased, they also said they expect this to continue to be the case over the next six months while bumping up intentions to buy autos and appliances.

There are plenty of folks at risk with waning stimulus benefits, but the overall results indicate that there is enough of a cross-section in the economy that is experiencing the opposite dynamic to net out to an improvement in the overall income dynamics within the consumer sector.

CANADA

On the back of last evening’s note (here) I’ll offer two follow up points this morning.

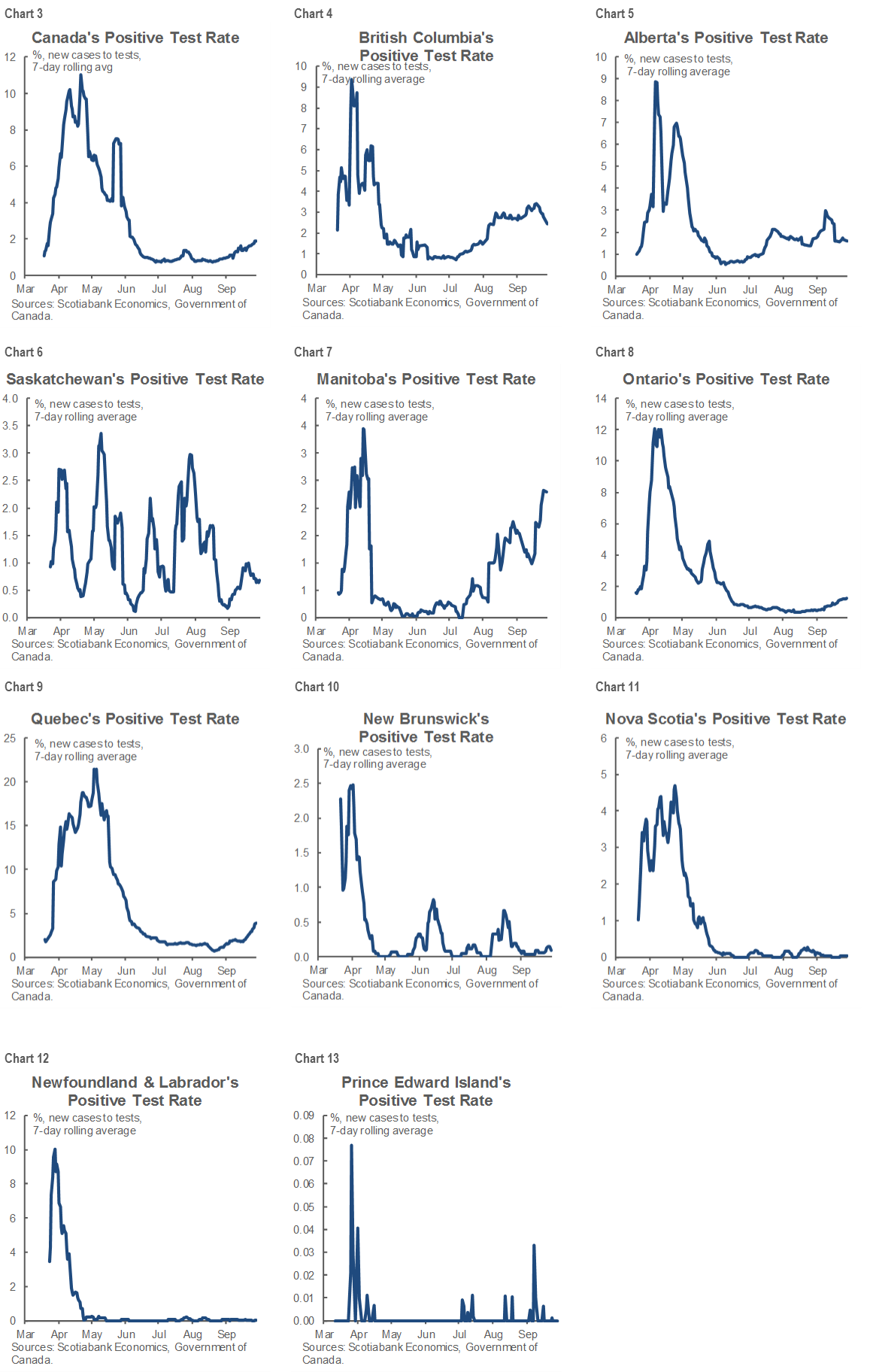

One concerns whether we’re getting more positive covid-19 test results in Canada now simply because of higher frequency testing. Charts 3–13 help to address this issue. The answer is that the incidence of positive test results as a share of overall testing volumes is rising at the national level, but the question of how this compares to the incidence rate during the first wave is unanswerable. The reason for this is how sample bias has likely changed over time.

How so? Back in the Spring there were more conditions attached to who could get a test. To get a test you had to either be a health professional or someone who could demonstrate a probable risk of potential exposure, such as living with someone who was showing symptoms. As testing broadened, this sample bias became more relaxed. In plain English, it’s likely that a higher share of people tested positive back in the first wave because the testing sample was biased toward a population that was more likely to be infected than today. Now, if due to testing delays and line-ups Canada is bringing back conditions attached to testing availability, then perhaps the positive incidence rate will creep higher again over coming weeks and months due to renewed sample bias. This should merit caution attached to attempts to interpreting the data in future.

The second—and frankly more distressing—issue is that apparently some folks still don’t believe that there is evidence to support wearing masks as a means by which the spread of covid-19 can be contained. I’ve lost all patience for such people. They are simply choosing not to listen or read anything. Here’s one piece of evidence. Check this one out. And this one. Here’s another. And another. Oh and there’s this one. Want more? Sure, this one. This one. And this one. Oh and this one. There are even more such studies in an increasingly well-established literature, but most folks would have gotten the point by now. Maybe it’s up to the health authorities to launch an advertising blitz during prime-time hours on conventional outlets and social media that neatly and graphically showcases the evidence. Or stiffen the penalties for noncompliance on the reasonable expectation that by now everyone should know better.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.