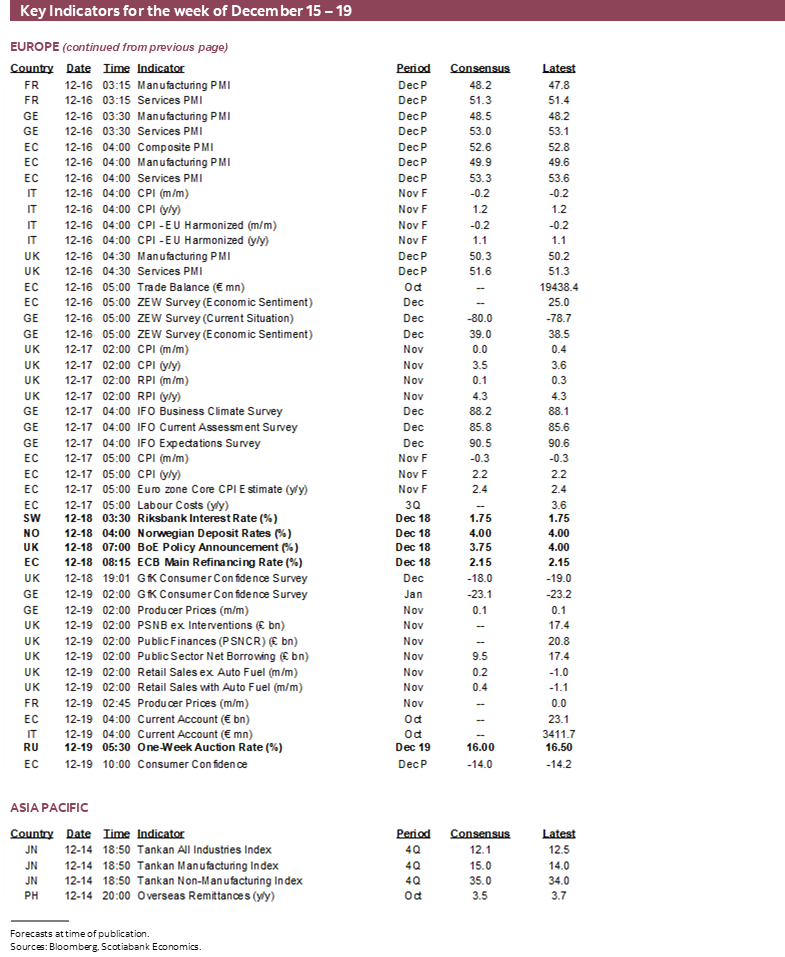

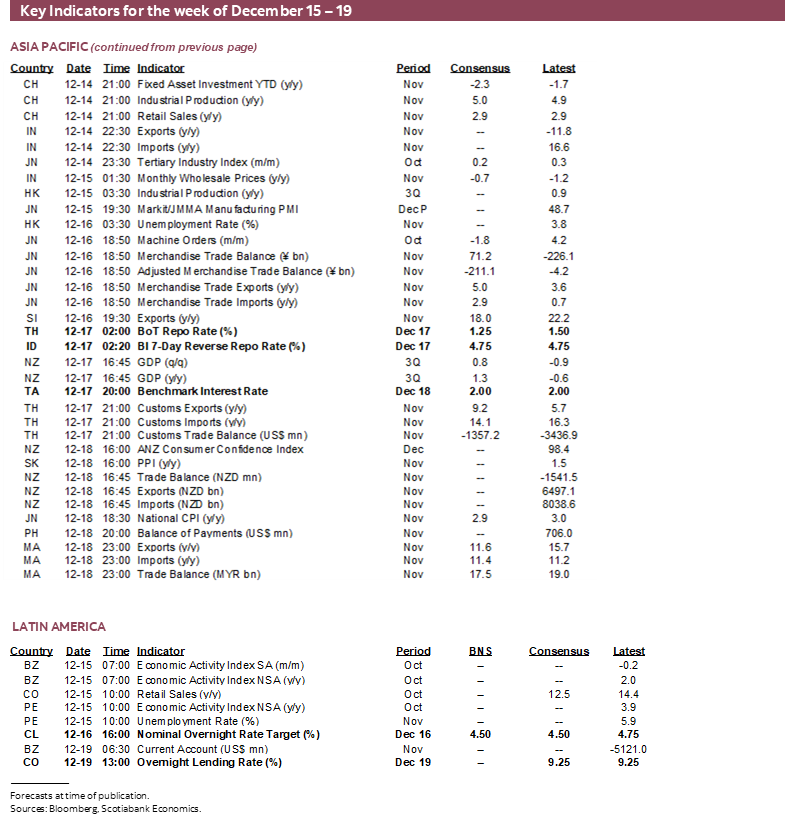

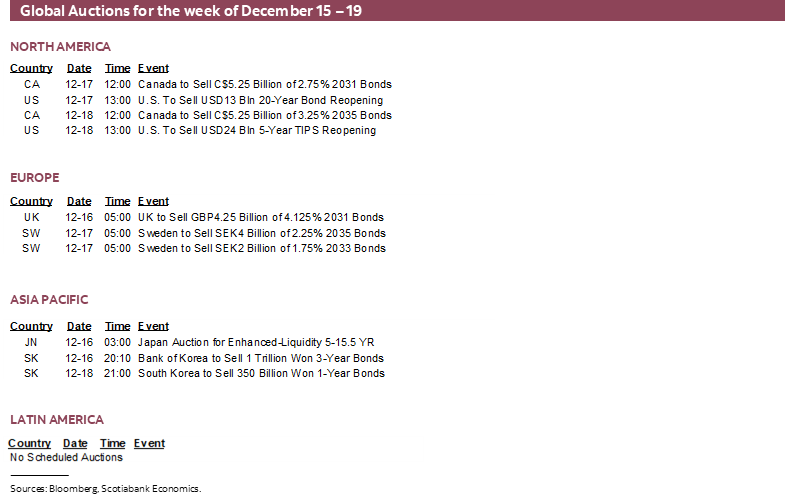

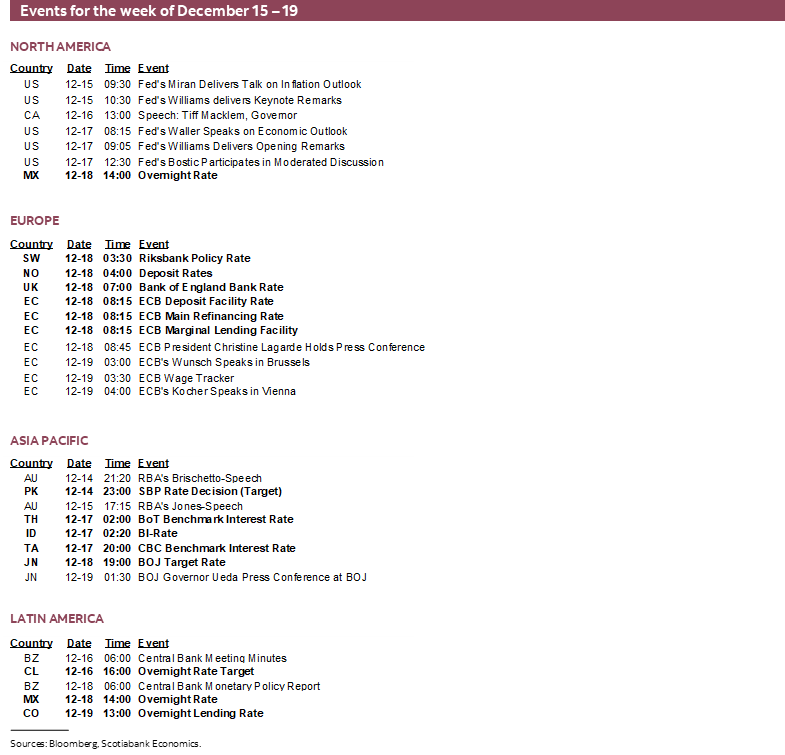

Next Week's Risk Dashboard

- Markets embrace the end of easing for a growing number of central banks

- A dozen central banks to weigh in this week

- BoJ expected to hike

- ECB to display greater confidence it’s done

- BoE could cut into neutral…

- …as long as key data cooperates

- Banxico — less dovish, if not hawkish

- Chile’s election could buoy local markets

- BCCh may cut after the election

- BanRep to hold amid political risk, weakening COP

- Nonfarm payrolls — two in one with the least conviction all year

- US CPI guesswork

- Canadian CPI — one of two before the next BoC

- PMIs: US, UK, Eurozone, Japan, India, Australia

- Riksbank — will it green light market tightening?

- Norges Bank — markets don’t believe it will keep easing

- BoT — better late than never

- BI is a toss up for a surprise-prone central bank

- CBCT to extend its long pause

- Russian central bank expected to cut again

Chart of the Week

Dearly beloved rate cuts, we hardly knew you. Did they go too far?

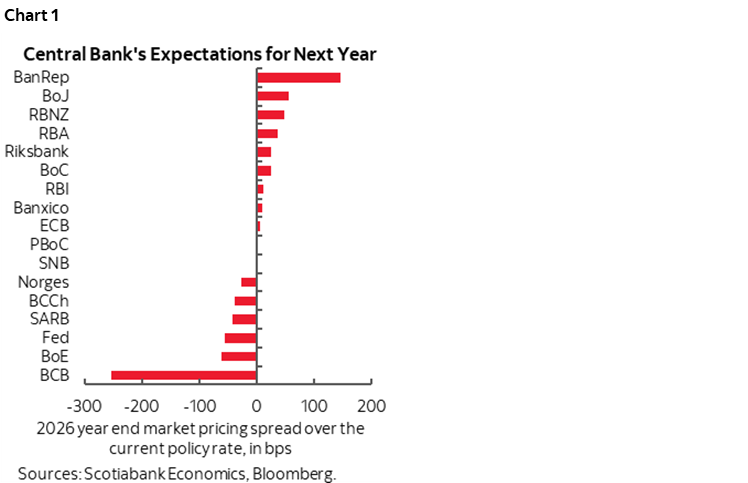

Or is it premature to be moving toward a different leg of the monetary policy cycle? Chart 1 gives the market’s answer.

It shows that several central banks including the BoJ, the Antipodeans, the BoC and the odd Scandie and LatAm central bank are up against markets that are pricing policy tightening over the coming year.

Others, like the ECB, SNB and RBI are priced to be done with their easing campaigns.

Modest easing is priced for the Federal Reserve, the BoE, and a few others. The only central bank for which material easing is priced is the one that went the other way from most others toward a tighter stance—Brazil’s central bank.

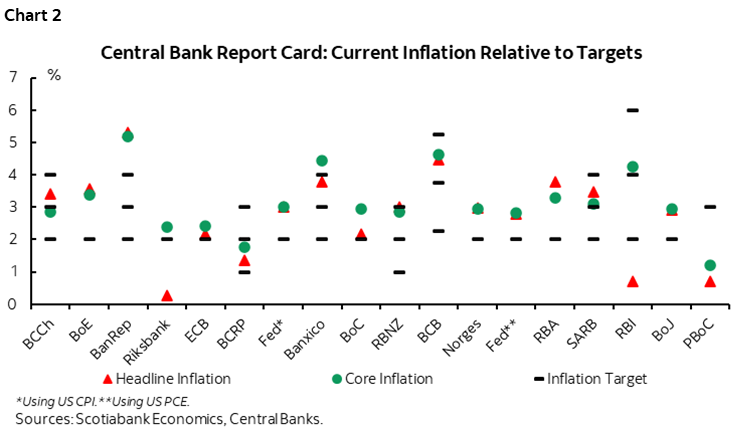

Some of this variation reflects varying performances on inflation. Chart 2 may look like it should be under a Christmas tree, but provides a look at where inflation stands in relation to targets for each of the central banks. Of course, central banks can be partly data dependent, but also have to have an eye on the future.

Clearly in most cases it’s too soon to be moving toward tightening, but it’s a legitimate point of debate in forward-looking markets. Enter this week’s dirty dozen. That’s how many global central banks will deliver policy decisions after this past week’s decisions led by the Fed and BoC. They’re clearing the decks before going radio silent and their words could set the stage for 2026. The list includes the BoJ, ECB, BoE, Riksbank, Norges, Banxico, Chile, Colombia, Thailand, Indonesia, Taiwan, and my least favourite, Russia. Their decisions follow this past week’s actions by the Federal Reserve (here) and Bank of Canada (here). Also go here for a Canadian rates outlook for 2026–27.

We might even hear who President Trump chooses to nominate for the Fed Chair in the wake of a WSJ interview that portrayed it as let’s say photo finish between the two Kevins—Warsh and Hassett. Markets may be more welcoming toward Warsh in my opinion.

Also be on guard for multiple key readings on the global economy. Two US payroll reports, US CPI, and US retail sales will catch up from the backlog created by the Trump administration’s government shutdown. Canadian CPI will be one of two before the next BoC decision and retail sales will inform tracking of consumer spending. Before the BoE decides what to do, UK markets will take down a tonne of key data.

CENTRAL BANKS—CLEARING THE DECKS

A dirty dozen of global central banks will weigh in with updated decisions this week before the central bank calendar slips into holiday mode. After this week we won’t hear from major central banks until at least mid-January so here’s your chance to get your fill of them now! Here are previews in chronological order with most of the focus upon the majors.

Before turning to them, however, someone tell me what “Good money and your central bank” means. It’s the title of BoC Governor Macklem’s speech on Tuesday with a full press conference. Maybe inflation control and preserving the value of money? Stablecoin perhaps? And yet not much is expected in terms of policy guidance compared to this past week’s communications (recap here).

BCCh — After the Vote

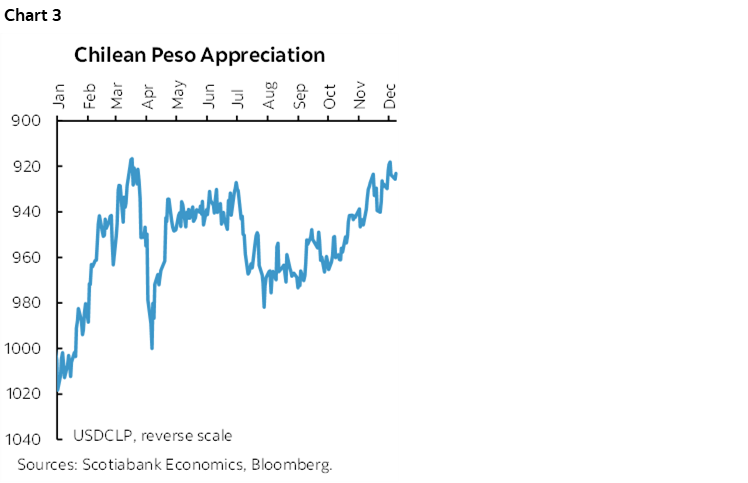

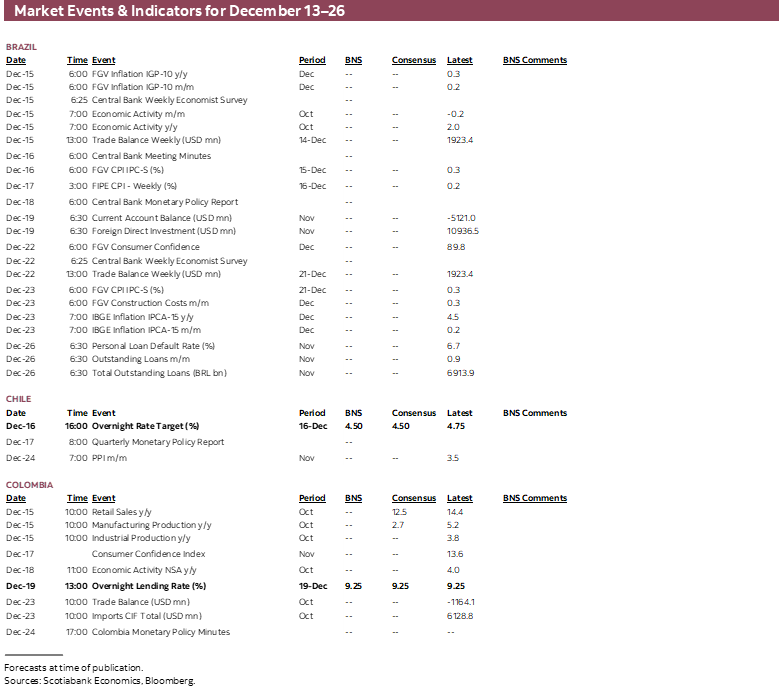

Chile’s central bank is expected to cut its overnight rate by 25bps on Tuesday after markets close. The catch is that the decision lands after the run-off vote on Sunday (see section later in this note). Inflation at 3.4% y/y is approaching the 3% target. The last time it provided explicit guidance was in September when they signalled a cut this week and then two more over 2026–27. The October 28th statement still sounded concerned about inflation risk and repeated the data dependent bias. The Chilean peso has also been appreciating to the dollar (chart 3).

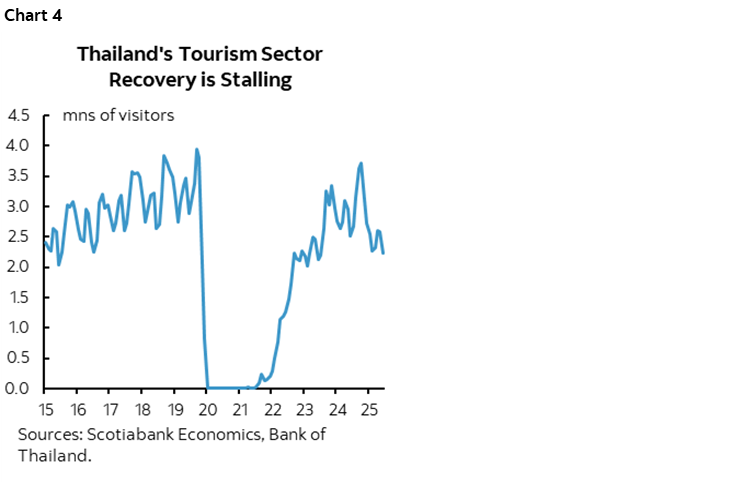

BoT — Maybe You Shouldn’t Have Surprised

Thailand’s central bank is expected to cut its benchmark rate by 25bps to 1.25% on Wednesday. The last cut was in August and it passed on expectations for a cut in October. The economy contracted by -0.6% q/q nonannualized in Q3 which was double the pace expected by consensus, and broad CPI prices are falling by -0.5% y/y with core inflation only at 0.7%. Tourism remains soft (chart 4).

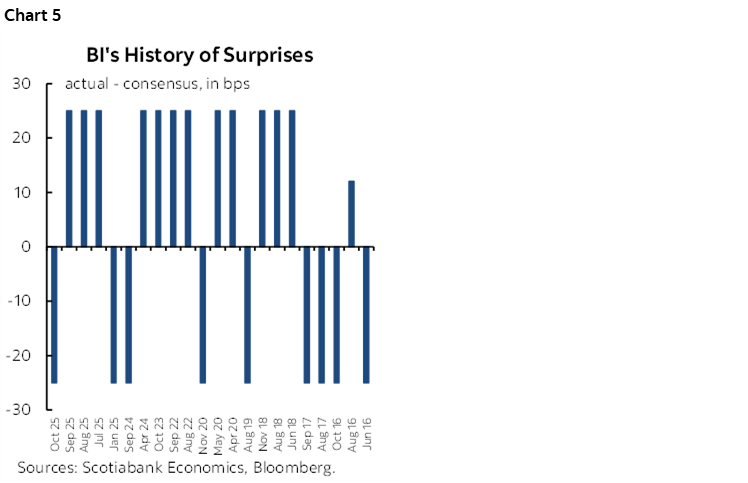

BI — Stable Enough?

Wednesday’s decision is expected to be a bit of a toss up. A majority of forecasters expect Indonesia’s central bank to hold at 4.75% but a solid minority expects a 25bps cut. Inflation eased a touch to 2.7% after the last decision.

Governor Warjiyo kept rate cuts speculation alive when he flagged low inflation, a focus on raising growth and room for further easing at the last decision in November. He also remarked that rupiah stability remained a key objective; since that decision, the rupiah has indeed been little changed to the dollar.

Bear in mind, however, that this central bank absolutely loves surprising markets (chart 5).

BoJ — Hike to Save JGBs

The Bank of Japan is widely expected to raise its target rate by 25bps to 0.75% on Thursday night (ET). Governor Ueda’s press conference will be closely scrutinized for openness toward further tightening in 2026.

Markets moved toward pricing a hike at this meeting fairly suddenly. As recently as late November there was basically nothing priced. That all started to change late in the month and the first several days of December. Why?

Governor Ueda fed speculation when he said on December 1st that the BoJ “will consider the pros and cons of raising the policy interest rate and make decisions as appropriate.”

Further, Japan’s new Prime Minister—Takaichi Sanae—advanced a supplementary budget bill that has just passed the Lower House and is headed to the Upper House. The bill applied ¥18.3 trillion (US$118B) of additional stimulus measures including subsidies for electricity and gas, as well as further spending on AI and shipbuilding.

What’s more, the government is now targeting further tax cuts such as investment incentives.

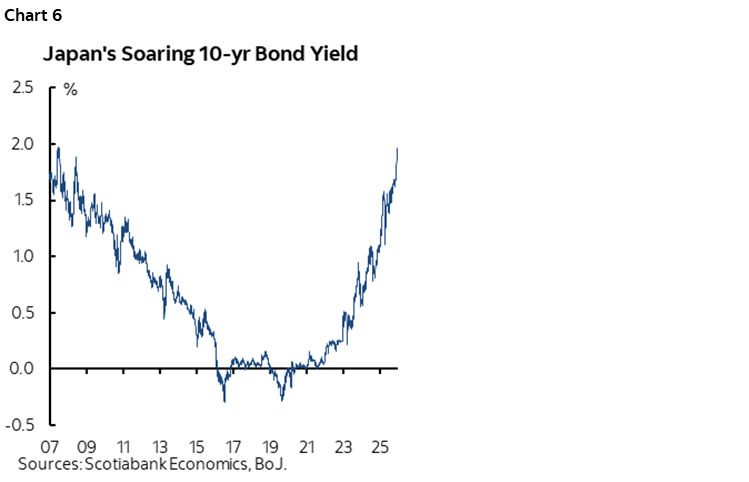

Monetary tightening can substitute for fiscal easing. Monetary tightening can perhaps seek to rein in the rapid rise of term yields, such as the 10-year JGB that has risen by about half a point since late summer to nearly 2%. To most other markets that would be low, but Japan last saw yields this high just before the Global Financial Crisis (chart 6). The rapid JGBs surge and BoJ tightening have been steadily killing off the carry trade (borrowing cheaply in yen and investing elsewhere).

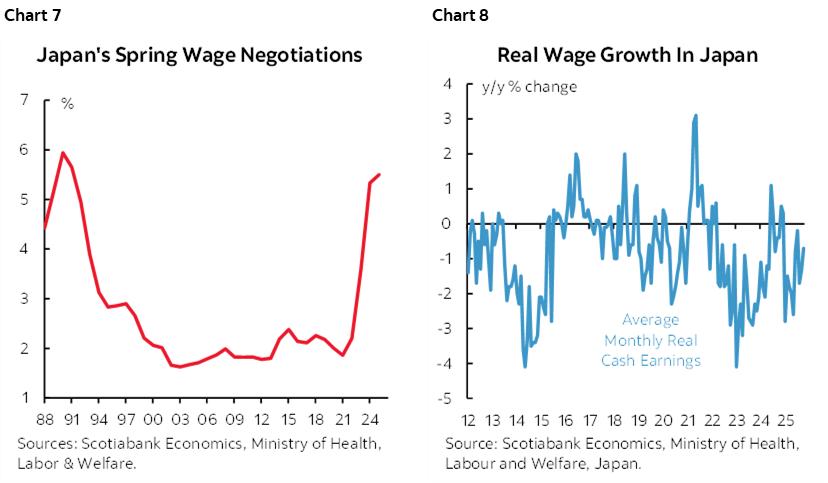

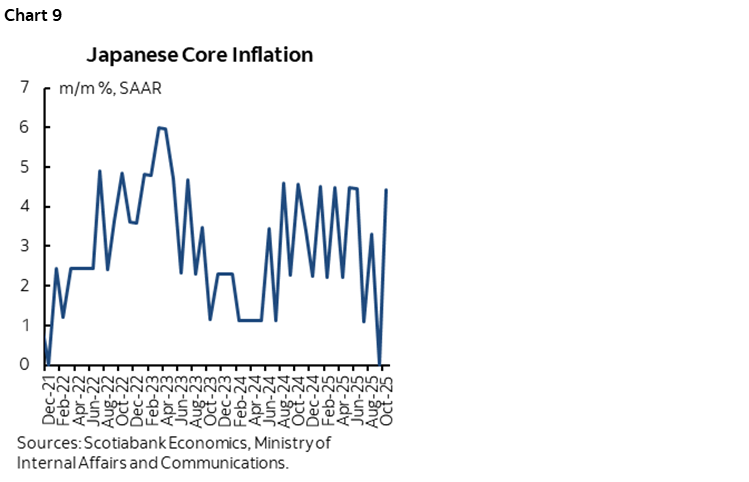

There is more to the picture. The annual Spring ‘Shunto’ wage negotiations are coming up. The Japanese Trade Union Confederation (Rengo) is demanding wage hikes of 5% or more overall and 6% or more for small- and medium-sized companies. If granted by businesses, then this would be the fourth consecutive year of large pay gains that affect under a fifth of Japanese workers (chart 7). There is as yet little evidence of spillover into aggregate real wage growth (chart 8).

Further, the past eighteen months or so has generally witnessed solid core inflation. Recent months have been more erratic (chart 9). Pass through effects of yen depreciation could give way to lagging upside to core inflation as the yen has depreciated by over 9% to the dollar since April.

Yen depreciation has been part of why Japan’s economy has been fairly resilient to US tariffs as Governor Ueda put it. He might have overstated his case. GDP contracted by 2.3% q/q SAAR in Q3 as investment and exports fell.

No forecast update is expected with this meeting. The last update on October 29th signalled that core CPI would rise by 1.8% next year and 2% in 2027. The January 22nd – 23rd 2026 meeting may unveil a higher core inflation reading partly backed by yen depreciation and fiscal impulses.

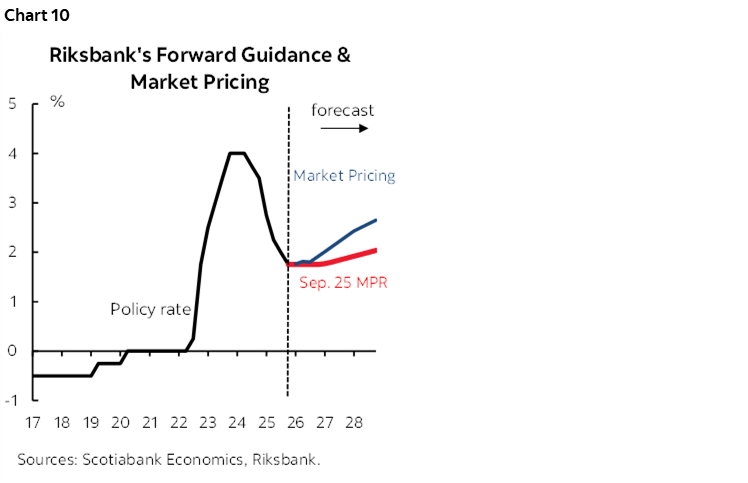

Riksbank — What’s the Worst Thing that Can Happen to a Forecast?

It’s the bias that will count in Thursday’s communications from Sweden’s central bank. No action is expected on the policy rate itself that is expected to stay parked at 1.75% and is priced accordingly.

They will, however, publish a fresh outlook along with updated and explicit forward rate guidance. Chart 10 shows that they signalled in the prior projection in September that cutting was probably over and the next move would eventually turn higher. Markets are well ahead of them as conditions give way to 2027. That’s a long, long way off from here and so much could change over that time, but whether the Riksbank will choose to lean against hike pricing that has already raised the two-year Swedish government bond yield by almost 40bps since late October will be the key.

You see, the worst thing that can happen to a forecast for an eventual move is that folks believe it too early, markets getting ahead of themselves, and the whole house of cards tumbles leaving the family fighting over who ate the last Swedish berry.

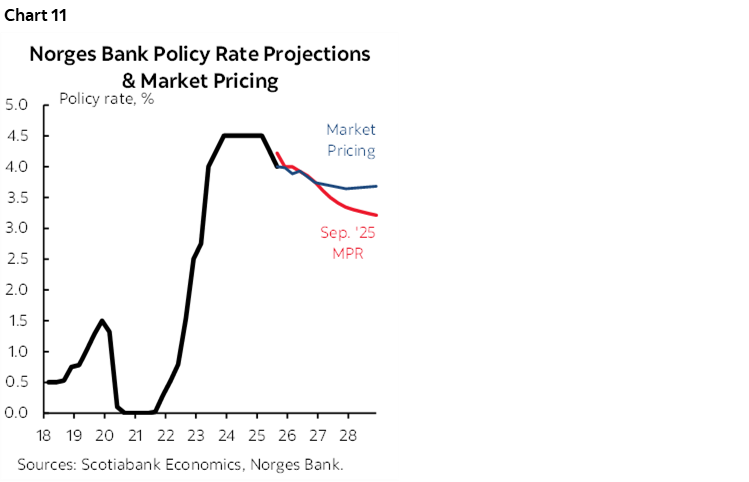

Norges Bank — Markets Don’t Believe You

Neighbouring Norges Bank faces a somewhat different dilemma to that which hangs over the Riksbank. Markets don’t believe the prior published rate path showing significant further easing ahead (chart 11). Markets are about 50bps above the forward rate path over the medium-term. Norway’s 2-year yield has jumped by about 50bps since August.

Why? Inflation. CPI surprised higher in the November reading at 3% y/y (2.7% consensus) with underlying inflation at 3%. There has been a persistent sideways trend in Norwegian underlying inflation throughout the year that has stayed around 3% y/y.

The near-term gulf between markets and Norges is not wide. The prior policy statement noted “a restrictive monetary policy is still needed. Inflation is still too high.” The question is whether to adjust the forward rate path in the direction of giving a nod to markets, or to dig in and expect similarly disinflationary forces to eventually emerge as they’ve previously argued.

This is more about whether prior forward guidance that indicated a bias toward one cut per year over the next three years is still appropriate. Norges may well emphasize that policy is unlikely to have to remain restrictive throughout the horizon with the deposit rate presently at 4% and hence meaningful above estimates for the neutral policy rate bracketed around 2½% on a nominal basis or around ½% in real terms (here).

BoE — Cutting Into Neutral

The Bank of England is widely expected to cut Bank Rate by 25bps to 3.75% on Thursday (7amET). Markets are mostly priced for a cut. No forecasts will be updated with this one after fresh forecasts were shared at the November 6th decision and with the next ones due in February. Expect dissenting voices amid comments indicating divisions on the Monetary Policy Committee.

The oscillating pattern of cuts and holds in keeping with the ‘gradual’ easing mantra was broken when the BoE held for two straight meetings in September and November. The cumulative 125bps of cuts since mid-2024 has brought the BoE closer toward estimates of nominal neutral that could be liberally estimated between 2–4%.

BoE guidance and data drove cut pricing higher for this meeting starting in October. At its last decision, the BoE said if they’re satisfied with further disinflation progress, then “Bank Rate is likely to continue on a gradual downward path.” They noted that “the risk from greater inflation persistence has become less pronounced recently, and the risk to medium-term inflation from weaker demand more apparent.”

Data since then has buttressed the case for easing. CPI eased to 3.6% y/y in October (from 3.8%) and services inflation also eased but remains high at 4.5% y/y. Monthly core inflation readings have also eased including a string of core CPI m/m seasonally unadjusted readings that have been more seasonally normal.

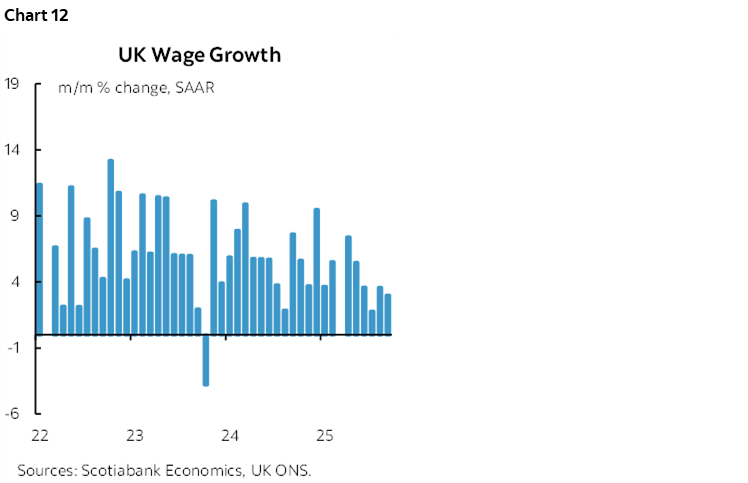

Wage growth is also ebbing (chart 12). The Starmer/Reeves Autumn budget was also more restrained than feared going in as witnessed by a relatively benign reaction in gilts.

A restrictive monetary policy stance and easing capital rules for banks likely has room for modest further easing in 2026.

ECB — Let’s Not Get Carried Away Here

The ECB’s 8:15amET statement next Thursday and President Lagarde’s press conference starting 30 minutes later are likely to be all about the reasons not to expect much from them for a while. No policy rate change is expected as 2% is pretty much spot on reasonable estimates for the neutral rate. Nothing is priced in markets pretty much throughout next year.

The statement is likely to repeat that inflation “remains close” to the 2% medium-term target. Key is how upgraded growth projections may filter through to this inflation guidance.

Recall that this past week President Lagarde said “In the last projection exercises, we have upgraded our projections. My suspicion is that we might do that again in December.”

Having said that, don’t get too carried away. Their prior projections in September pointed to 1.2% growth this year, 1.0% in 2026 and then 1.3% in 2027. They are only marginally lower than the private sector consensus for each year. It’s not like the ECB is going to wave a magic wand that whooshes away all that ails Europe.

Topics that may come up could include ECB Board Member Schnabel?)’s speculation that the next policy rate move is likely to be up. Expect Lagarde to bat that away as highly premature. French President Macron’s plea for more of a growth focus in the ECB’s mandate is also (hopefully) going to be batted away; Lagarde did so this past week but was perhaps being diplomatically reserved in the strength of her rebuttal.

CBCT — Long Pause

Taiwan’s central bank is widely expected to hold its benchmark rate at 2% on Thursday. The policy rate hasn’t budged since March 2024 with the New Taiwan Dollar operating under a managed float with interventions to maintain stability to the USD. Inflation is running at just 1.2% y/y with core at 1.7% so there is no real pressure to tighten, while easing could destabilize the currency when it has already been sliding since July. Flip the channel to something more interesting.

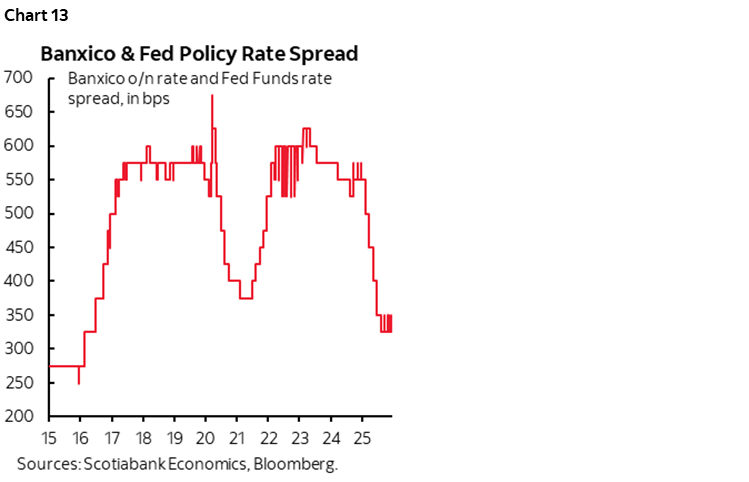

Banxico — Less Dovish If Not Downright Hawkish

Another quarter-point overnight rate cut is expected to be delivered by Mexico’s central bank on Thursday. That would mean 425bps of cumulative easing since early 2024. Key is the signal on how much further to go, if at all.

One case for halting in its tracks is that core inflation has been on the rise throughout much of this year. It’s running at 4.4% y/y, up from 3.7% in February.

Another case is uncertainty over the forward path for the fed funds rate. The present policy rate spread is 350bps and has narrowed by 225bps since early 2024. That’s a narrower spread than it was at any point since 2016 (chart 13).

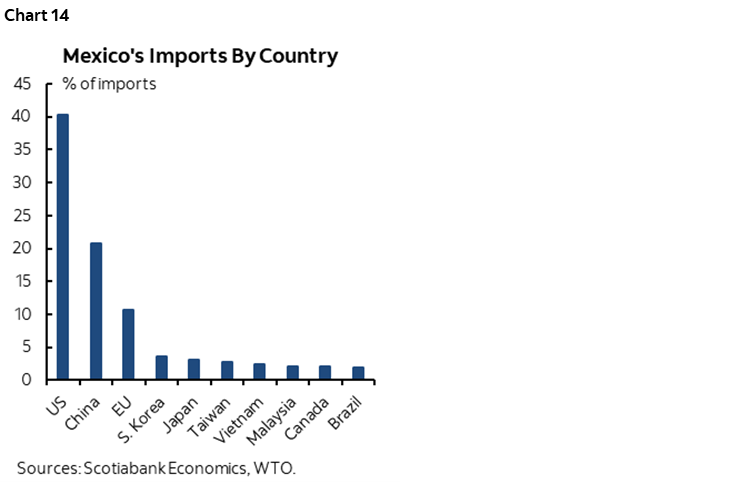

Trade negotiations with the US are an obvious risk but carry demand and supply side considerations. Mexico’s steep tariffs applied against Asian imports—particularly from China with rates up to 50%—could pose substantial pass-through risk given high import propensities (chart 14).

Even before this announcement, Banxico’s Deputy Governor Jonathan Heath said “nobody believes” that the central bank will achieve its 3% inflation target as the midpoint of a 2–4% target range. Heath warned “We must do everything we can, and continue doing so permanently, to bring inflation down to 3%.” To date, Heath’s dissenting voice has been on the right side of the debate. With MXN appreciating by about 15% to the dollar ever since April, his colleagues may counterbalance the debate.

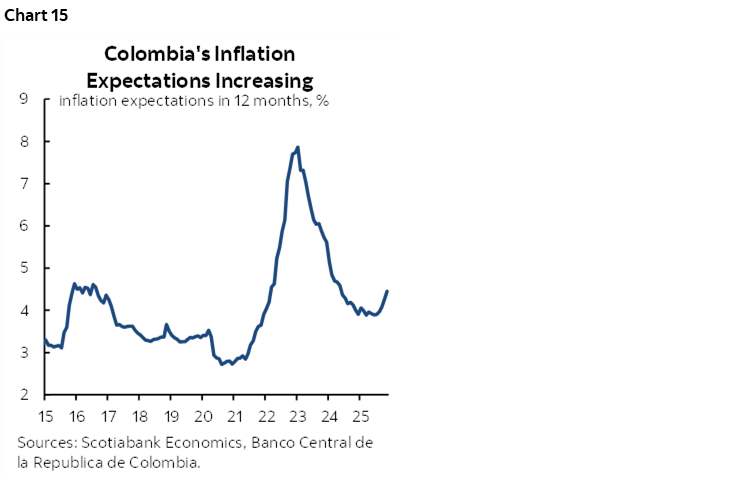

BanRep — Inflation Doesn’t Need COP Weakening

Colombia’s central bank is widely expected to stay on hold at an overnight rate of 9.25%. It has been on hold since April. Inflation expectations are back on the rise again (chart 15). Core inflation has stopped falling and is at 5.2% y/y.

COP was appreciating strongly since April but has recently lost some ground partly as US President Trump and Colombian President Petro increasingly lock horns. Trump warned Petro “will be next” after Venezuela. Petro’s remarks that drug consumption is not illegal and instead reflects societal and emotional factors doesn’t help tensions with the US over its own drug problems. The Colcap stock index has treated much of this as mere theater, rising to new highs in December.

Russia — Happy New Year, Not!

Friday’s decision by Russia’s central bank is expected to deliver another cut with the median consensus estimate at -50bps down to 16% but some forecasting a bigger 100bps key rate cut. Inflation is falling and at 6.6% y/y with core at 6.1% from the nearly 10% peak in March.

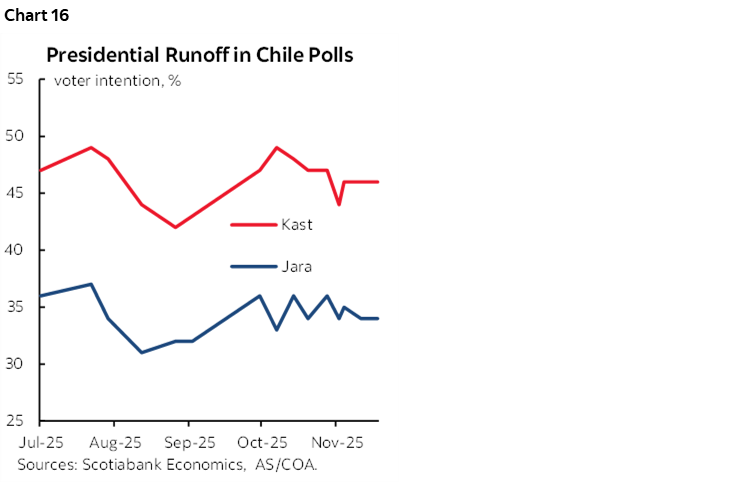

CHILE’S ELECTION—STOCKS AND CLP COULD GET A BOOST

The final run-off vote for Chile’s election will be held on Sunday. It’s a classic right-versus-left contest as José Antonio Kast goes up against the communist candidate, Jeannette Jara.

Kast is widely expected to win after his performance in the first-round back on November 16th. Markets would welcome such an outcome at the start of the week. The Chilean peso has appreciated by about 2% to the dollar and the Chilean S&P/CLX IPSA exchange has gained almost 8% since that election on expectations for a market-friendlier right of center government to emerge. Kast had won about 70% of right-leaning votes in the first round and other centre-right candidates have been throwing their support behind Kast.

Like elsewhere, crime and immigration are key election issues. Polls show a sizeable lead for Kast over Jara (chart 16).

GLOBAL MACRO—FILLING IN SOME BLANKS

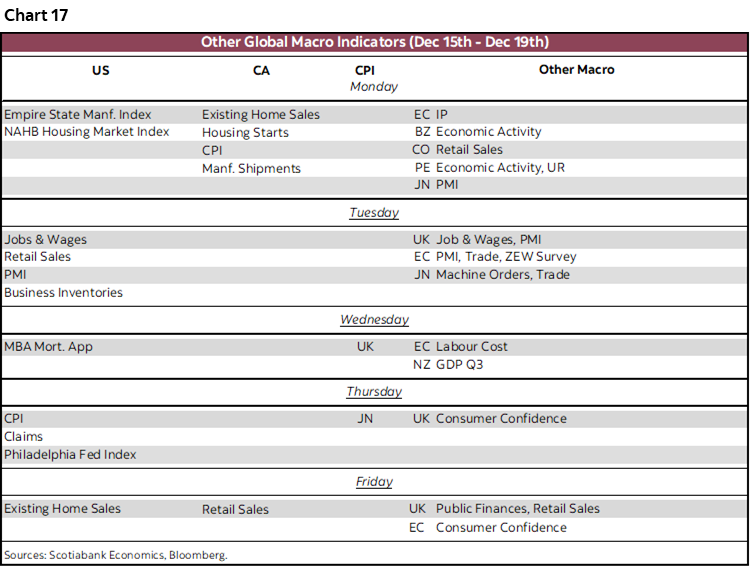

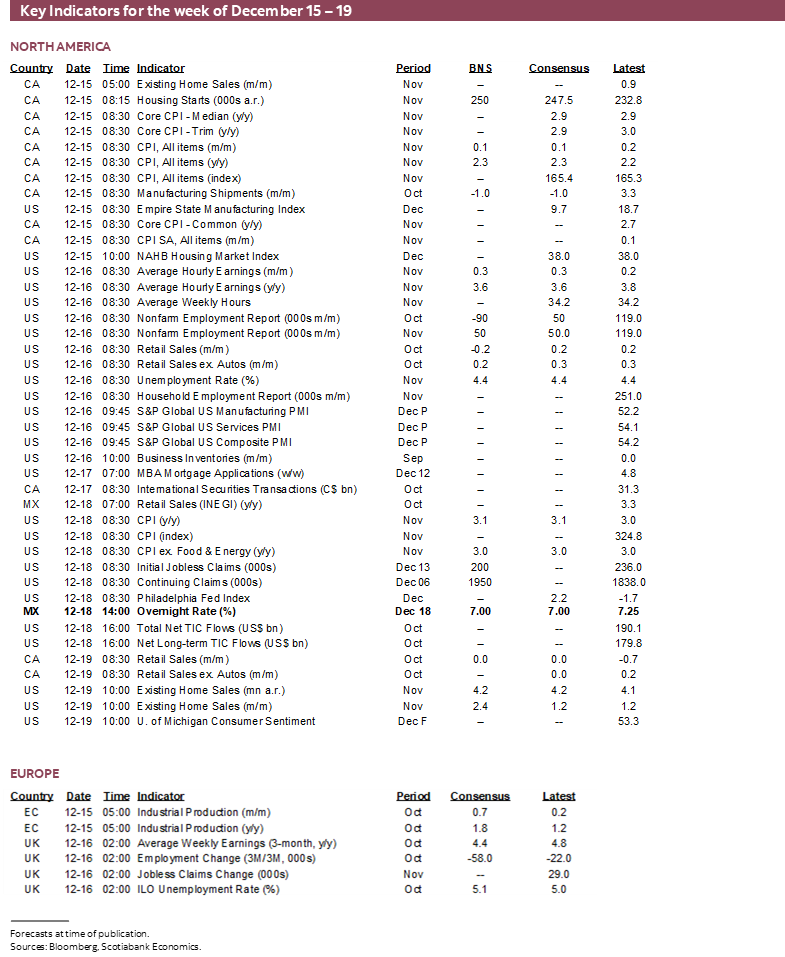

With the Fed and Bank of Canada out of the way until their next decisions on January 28th the focus now returns to tracking key data. Chart 17 provides highlights by day.

US — Obstructed Vision

High data risk driven by low conviction over the estimates will hit markets on Tuesday and Thursday.

Nonfarm payrolls for October and November will arrive on Tuesday alongside the household survey for November (October’s was cancelled). The BLS also refreshes CPI estimates for November (Thursday) after previously guiding that October’s release was cancelled because the government shutdown prevented data collection.

How much faith can you have in November estimates for month-over-month changes without October data? Not much if any!

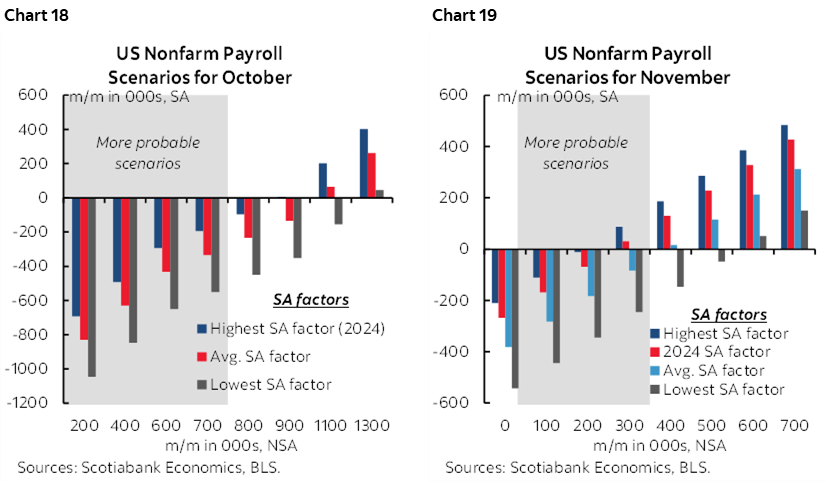

I figure October payrolls could be down (-90k estimate) and November could rebound a touch (+50k) but wouldn’t advise betting the Toronto Blue Jays payroll on it. Scenarios for seasonal adjustments and seasonally unadjusted payrolls slant toward a drop in October and a small gain in November (charts 18, 19).

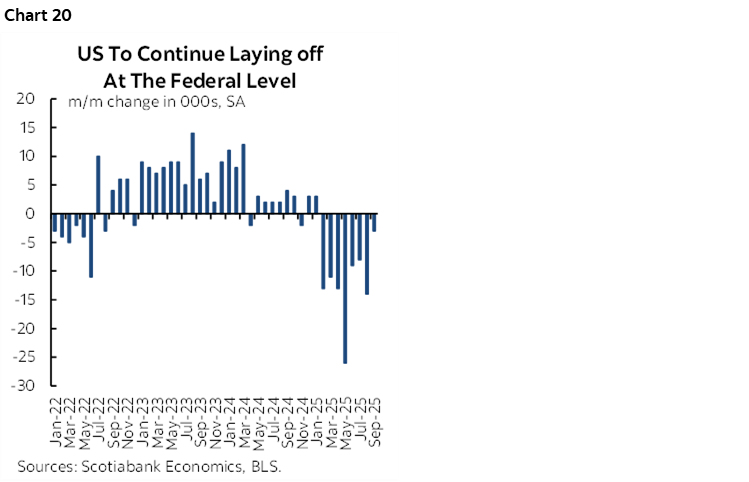

The government shutdown over October 1st through November 12th could have impeded related activity and private sector hiring through the reference periods. The expiration of DOGE layoff packages in September could drive October payrolls lower as those who didn’t already jump ship would now fall off payrolls (chart 20).

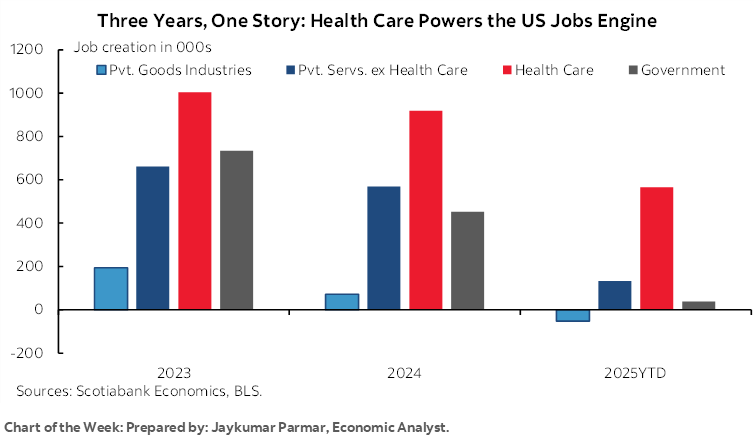

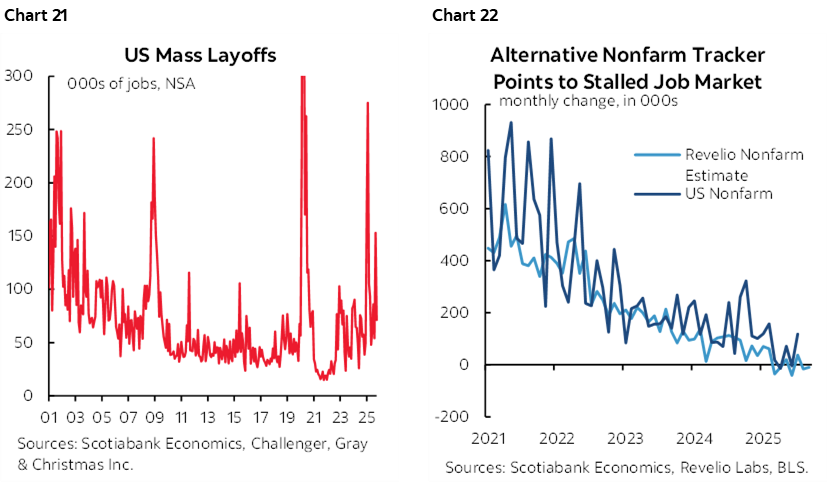

I still don’t trust the September payrolls report that was driven higher by the highest SA factor on record for like months of September and without explanation from the BLS. Further, October saw a surge in mass layoffs (chart 21). Alternative nonfarm trackers like Revelio’s point to a stalled job market (chart 22). Other advance readings like consumer confidence jobs plentiful and ISM-employment subindices are subdued. ADP private payrolls were up somewhat in October and fell in November but can be highly misleading for private nonfarm payrolls. Remember to strip out health care from the headline reading given its role as a distorting upside relative to the rest of the labour market as Jay Parmar’s chart of the week on the cover shows.

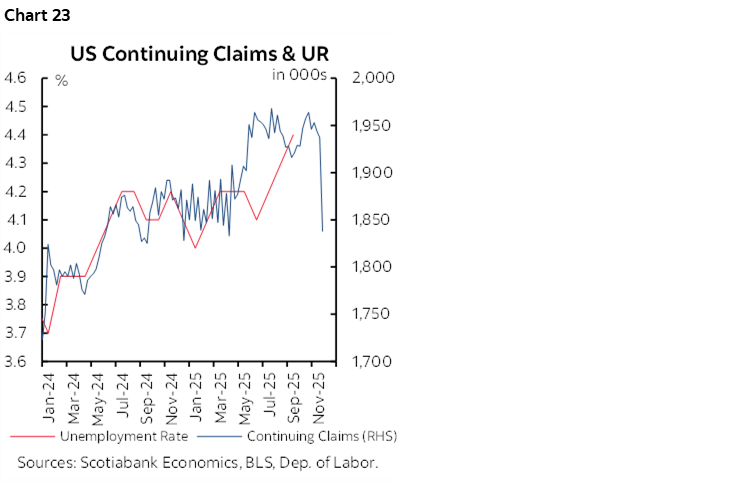

As for the unemployment rate, we won’t get it for October, but November’s could be flat to higher based on correlations with continuing claims (chart 23).

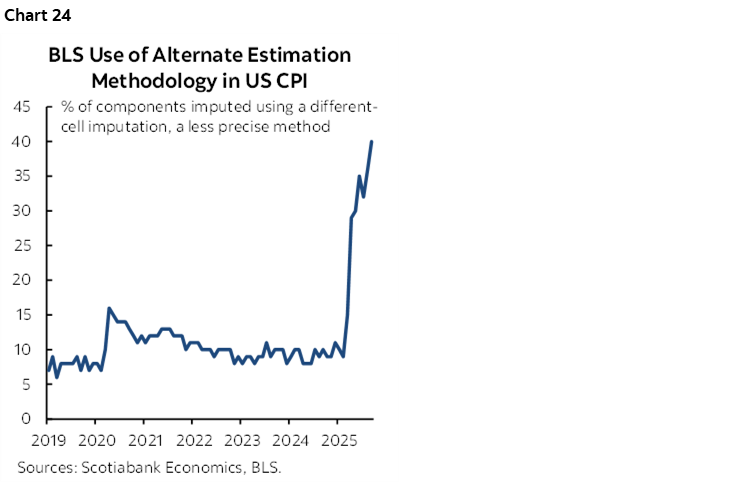

As for CPI in November, I figure it will be up by around 3.1% y/y with core up 3% y/y. No estimates for month-over-month are feasible absent October data. Uncertainty and faith in the estimates were already low given a record 40% of the CPI basket that is estimated using imputed methods due to budget cuts and other issues (chart 24).

Also on Tuesday will be retail sales during October. The headline could be soft given what we know about the drop in auto sales following the expiration of EV credits in September and gasoline prices, but core sales could post a mild gain.

Canada — One of Two before Next BoC

CPI for November (Monday) and retail sales for October with November guidance (Friday) will add a little local flare to Canadian markets possibly in addition to any market impactful comments from Governor Macklem on Tuesday.

Still, this is one of two inflation readings before the next BoC decision on January 28th and with the BoC signalling it is on an extended hold there may be little by way of policy and market implications stemming from the reading. The two combined could inform market pricing for policy tightening to begin arriving later next year.

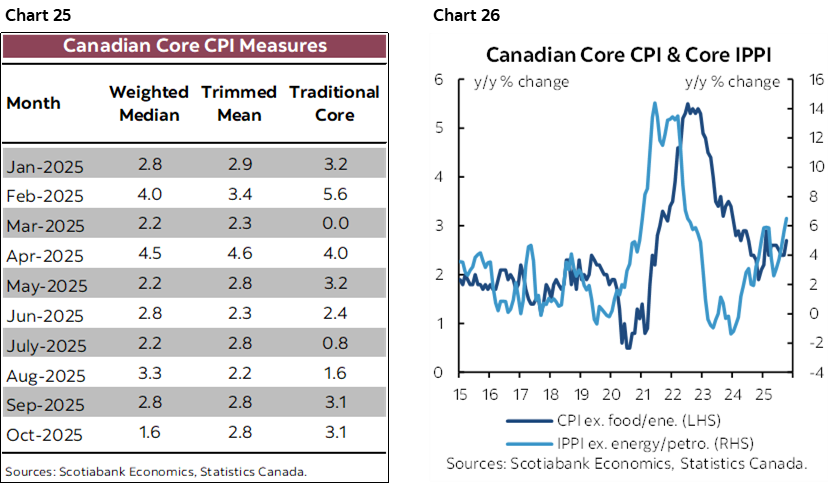

The year-over-year inflation rate could bump up a tick to 2.3% based upon a mild seasonally unadjusted gain of 0.1% m/m and base effects. Key, however, will be whether mixed and partial progress on underlying core measures continues (chart 25). Among the warning signs is chart 26 that shows how rising producer prices—measured as the industrial products price index—tends to lead core CPI inflation pressures.

Retail sales were previously guided to have been “relatively unchanged” in October in dollar terms. Volumes and other details will matter, but so will the first estimate for November.

Global PMIs

A wave of purchasing managers’ indices for December land toward the start of the week. They will inform developments across supply chains including orders, production, hiring and pricing decisions.

Japan updates the Q4 Tankan Survey Sunday evening. Then Australia and Japan report PMIs on Monday evening followed by the UK, Australia, India and US into Tuesday morning.

UK — CPI & Jobs Could Influence the BoE

UK markets also receive fresher readings on jobs and wages on Tuesday, CPI for November on Wednesday and retail sales for November on Friday. The pre-BoE data for labour markets and inflation may be influential to the tight balance between hawks and doves on the BoE’s MPC.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.