Next Week's Risk Dashboard

- Three ways the FOMC can handle December’s unique risks

- Forget the minutes: here’s a vote-weighted round up of FOMC leanings

- Eat, Shop, Drop — Tracking Holiday Sales

- Canadian GDP: stall speed won’t surprise the BoC

- US to continue catching up key releases

- Eurozone CPI won’t sway the ECB’s coming hold

- BoJ bets may hang on Tokyo CPI

- UK Budget: Pay Up!

- RBNZ — could this be the last cut?

- BoK to hold on FX and housing stability concerns

- Global macro

Chart of the Week

The shutdown’s aftermath may result in near paralysis among Fed policymakers at the December 9th–10th FOMC meeting because both the October and November nonfarm payroll reports won’t be released until December 16th. That will rob them of what may be critical information necessary to make a fully informed decision and perhaps restrain their confidence in providing a new Summary of Economic Projections. That’s especially true in the wake of a September payrolls report that suspiciously averted disaster only due to a record high seasonal adjustment factor that hopefully reflects pure motives amid leadership uncertainty at the BLS (here). While the Committee’s data dependency is overly extreme—versus a more forward-looking perspective—this is the reality that we’re faced with.

It will be imperative for the FOMC to be flexible through this period. If, for instance, the readings bomb and the Fed sits on its hands until the next formal meeting on January 27th–28th, then the potential for serious market turmoil during the intervening period would be real. Market confidence and uncertainty could be major risks as FOMC officials split town for the holidays. Compounding this possibility would be uncertainty toward year-end funding conditions, appetite for US dollars, and the risk of combining such uncertainty with deteriorating data. Put simply, the Committee could be left whistling by the graveyard until the next formal a month-and-a-half later. Why chance it?

To counter this uncertainty, the FOMC should be willing to show flexibility in three possible ways in addition to cutting in December.

- One is to insert an off-calendar meeting after receiving the data should circumstances warrant doing so. That would not be unprecedented but the two meetings in March 2020 were delivered under truly exigent circumstances. The holiday calendar would be a complicating factor since the following week has just two-and-a-half trading days before shutting for Christmas. This is a low probability scenario.

- A second way would be the unprecedented step of delaying the December 9th–10th FOMC meeting until after the data, but not for too long. Perhaps wait for the thick blanket of fog to lift before heading out on the road. This option could also run into the constraints around the holiday calendar.

- A third way could be openness toward signalling less of a gradual pace of easing that currently implies no serious tolerance toward upsizing. Weak payrolls could merit catching up by conveying openness toward a bigger move than -25bps at the end of January and doing so through communications in advance. Insert a holiday speech soon after the data if needed and make it a Merry Christmas indeed as markets would ease on the guidance. This could be the most palatable and most likely option.

At the moment, our base case does not assume such options being pursued, but the fragile market environment may require such flexibility.

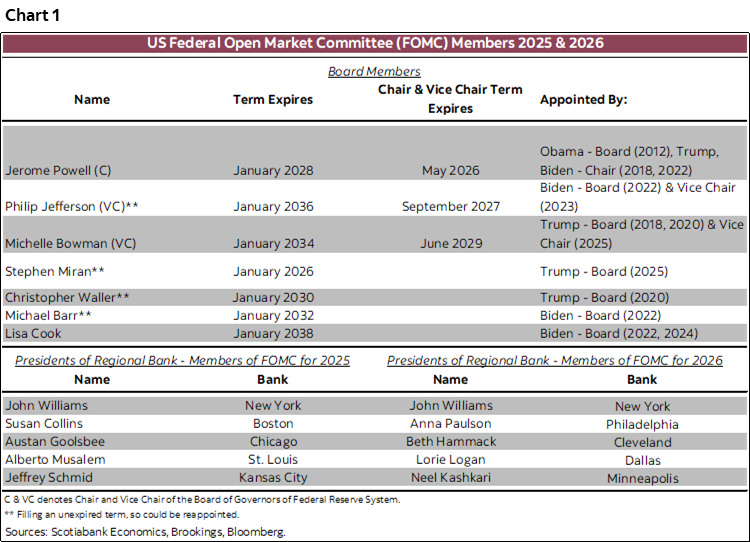

SURVEYING VOTE-WEIGHTED FOMC OPINIONS

What will the Federal Reserve’s Open Market Committee do on December 10th? I still think they cut –25bps but it’s uncertain. More uncertain than it perhaps should be given the extreme dependency of the Committee on recent backward-looking data.

And yet based on a review of recent comments by FOMC members, I figure that if held today, the vote could be 8–1–2 in favour of -25bps, -50bps and a hold in that order plus one present member who appears to be highly undecided. This provides a vote-weighted perspective that may be subject to change but that nevertheless leans against the “many”—not majority—of Committee members who leaned against a cut in December as expressed in the FOMC minutes that do not weight views toward present voting members. Easing in December could be easier to deliver than in January when the regional Presidents arguable rotate in more neutral-hawkish fashion (chart 1).

The minutes would be far more useful if they were less egalitarian. A simple adjustment could be to insert language like “Among voting Committee members….” as distinct from the overall Committee’s views. Given votes to only some on the overall Committee but issuing minutes that fail to differentiate views according to voting status is awkward democracy that doesn’t serve markets well.

Jerome H. Powell, Board of Governors, Chair — Vote -25bps

Has not pre-committed to December while stating that “a further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it.” Still, he has tended to express concern about downside risks to jobs while expressing a central base case inflation scenario that sees only a temporary acceleration he’s prepared to look through.

John C. Williams, New York, Vice Chair — Vote -25bps

Will vote with Chair Powell and FOMC consensus. Just said there is room for a near-term rate cut. Has previously said the December decision is “really a balancing act” while cautioning that “inflation is high, and it’s not showing signs of coming down right now,” while the economy “is showing some resilience” but cautioned that the rub may lie in weakening conditions for lower- and moderate-income households that could dampen the outlook for consumption.

Michael S. Barr, Board of Governors — Vote -25bps

Balanced in his comments, likely to vote with the consensus. On inflation, said “We made a lot of progress on that, but we still have some more work to do.” On jobs, said “We have to pay careful attention to making sure that the labour market is solid.” Post nonfarm, he said the job market is “kind of cooling” and “in balance at a pretty low level of net new job creation” while stating “I am concerned that we’re seeing inflation still at around 3%.”

Michelle W. Bowman, Board of Governors — Vote -25bps

Has not commented on monetary policy in quite some time as she has focused on her new supervisory role but broadly viewed as dovish and a possible candidate to replace Chair Powell and highly likely to support a further 25bps cut in December.

Susan M. Collins, Boston — Vote Hold

Appears to lean in favour of an extended hold. “It will likely be appropriate to keep policy rates at the current level for some time to balance the inflation and employment risks in this highly uncertain environment.”

Lisa D. Cook, Board of Governors — Vote -25bps

Likely to support additional easing. She did not comment on monetary policy in her post-nonfarm remarks but previously said: “I believe that the downside risks to employment are greater than the upside risks to inflation. Looking ahead, policy is not on a predetermined path. We are at a moment when risks to both sides of the dual mandate are elevated. Every meeting, including December’s, is a live meeting.”

Austan D. Goolsbee, Chicago — Not Committing

Leaning hawkish but open to treating December as ‘live’: “I’m not decided going into the December meeting. I am nervous about the inflation side of the ledger, where you’ve seen inflation above the target for four and a half years and it’s trending the wrong way.” And on data gaps that may be filled in by the meeting, he said: “I have some concerns, and I lean more to the, ‘When it’s foggy, let’s just be a little careful and slow down.”

Philip N. Jefferson, Board of Governors — Vote -25bps

Appears to lean dovishly and likely to support a further cut in December: “I see the balance of risks in the economy as having shifted in recent months with increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently.”

Stephen I. Miran, Board of Governors — Vote -50bps

Need I say more? Would likely advocate for -50bps as he has unsuccessfully at the prior two meetings.

Alberto G. Musalem, St. Louis — Vote -25bps

Unclear but likely to support gradual easing including -25bps in December but cautious thereafter: “We need to proceed and tread with caution, because I think there’s limited room for further easing without monetary policy becoming overly accommodative. We need to continue to lean against above target-inflation while providing some support to the labuor market.”

Jeffrey R. Schmid, Kansas City — Vote Hold

Voted to hold rates in October. Likely to vote for another hold in December. Recently stated “My view is that with inflation still too high, monetary policy should lean against demand growth to allow the space for supply to expand and relieve price pressures in the economy. Cuts could have longer-lasting effects on inflation as our commitment to our 2% objective increasingly comes into question. “This was my rationale for dissenting against the rate cut at the last meeting and one that continues to guide my thoughts as I head into the meeting in December.”

Christopher J. Waller, Board of Governors — Vote -25bps

Waller is among the most dovish on the Committee and his recent views largely pre-committed himself to advocating a 25bps cut on December 4th: “With underlying inflation close to the FOMC’s target and evidence of a weak labour market, I support cutting the committee’s policy rate by another 25 basis points at our December meeting,” he said in a speech delivered at the Society of Professional Economists Annual Dinner. “My focus is on the labour market, and after months of weakening, it is unlikely that the September jobs report later this week or any other data in the next few weeks would change my view that another cut is in order.” On that, while one can agree or disagree with his views, I think his stance against extreme data dependency in favour of looking forward is probably among the most sensible on the FOMC.

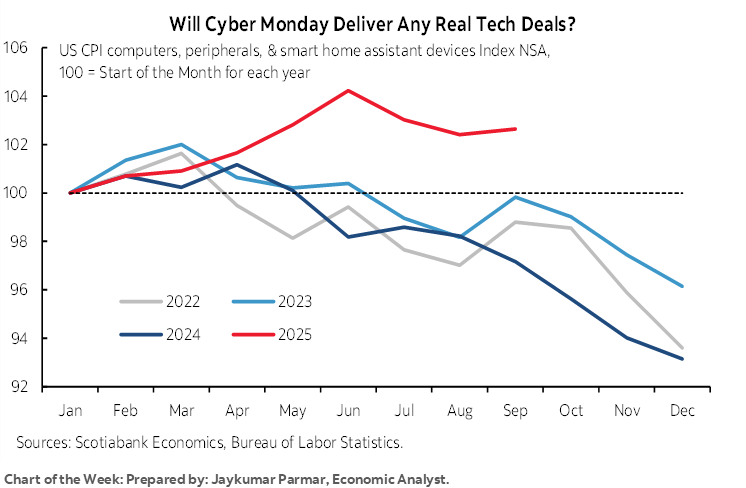

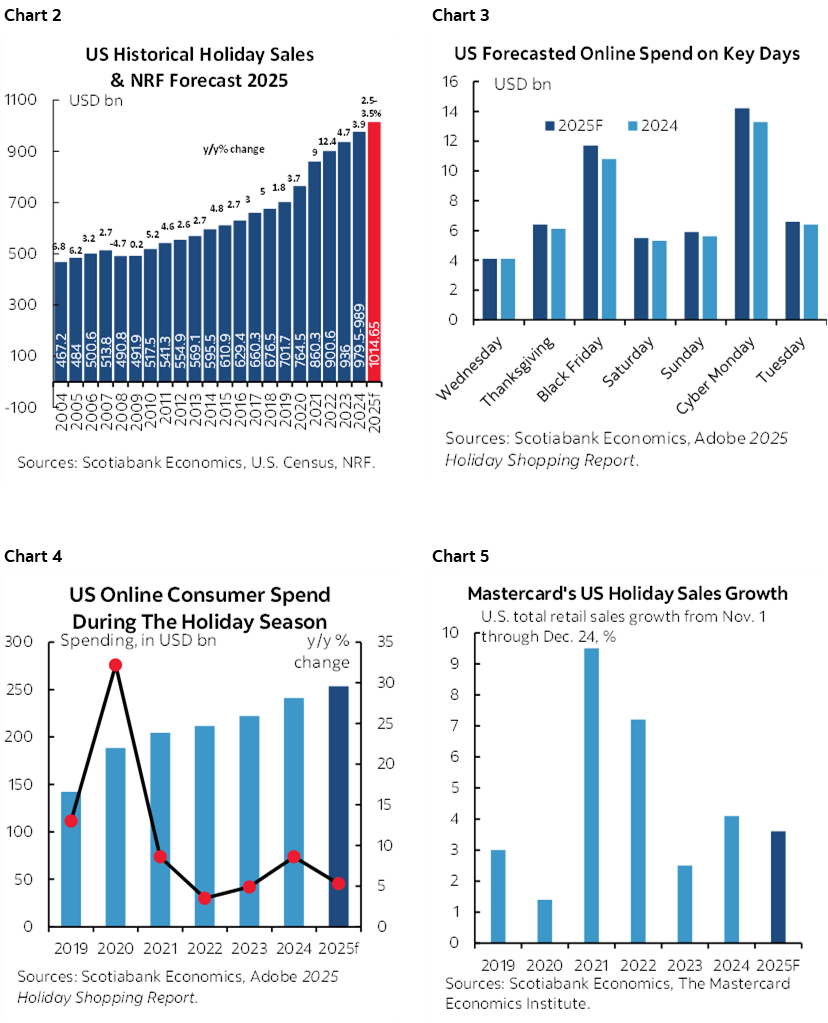

TRACKING US HOLIDAY SALES

American Thanksgiving is on Thursday. Markets will be shut and that will be followed by an early close on Friday at 1pmET for stocks and 2pmET for bonds, that is for those who don’t book off a long weekend.

Black Friday and Cyber Monday sales may provide an indication of how strong the holiday shopping season may be, but its effects are more prolonged and spread out than in years past. Forecasts are mixed from various groups (charts 2–5). Markets will monitor readings like credit card transactions, TSA flight data, hotel bookings, and guidance from key retailers for an advance sense of the key start of the holiday shopping season before the hard data.

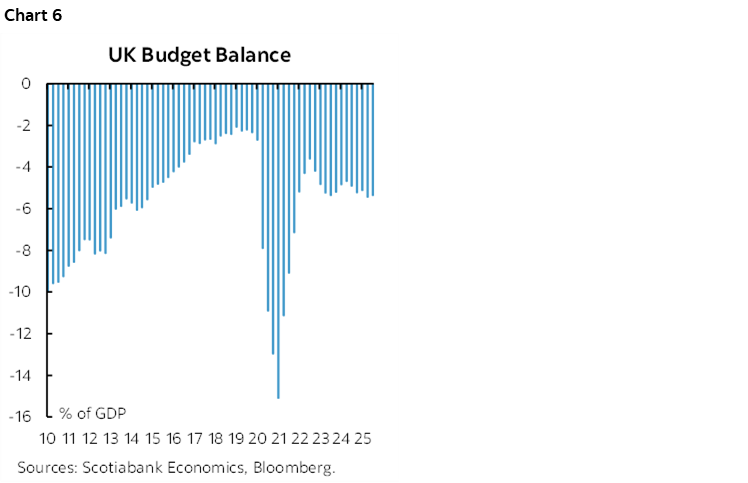

UK BUDGET—I’M THE TAX (WO)MAN

You think the lead up to Canada’s Federal budget was long? That Canada has a persistent residual inflation problem? That Canadian taxes are high? Let’s just say the former colony has much in common with the former mothership!

The Starmer administration delivers its second budget on Wednesday. The Chancellor of the Exchequer—Rachel Reeves—will deliver it. The first Budget was hardly a smashing success. The 10-year gilt yield jumped by 15bps on delivery. Sterling depreciated by about 1%. The FTSE100 fell by over 1%. The lack of a credible roadmap for the fiscal deficit, an additional £70 billion of annual spending, inflation concerns and a broken pledge that raised taxes on wealthier individuals and businesses wasn’t well received.

Perhaps much has been learned. Perhaps not.

The fiscal deficit to GDP ratio is well over 5% which is slightly wider than this time last year (chart 6). No progress has been made to date toward reining in the deficit ratio. Debt-to-GDP has risen to about 94%.

Fervent speculation points to other possible ways of raising tax revenues such as adjusting the personal allowance, possibly freezing tax brackets such that income growth over time moves more earners into higher brackets and hence paying more taxes, and possibly raising taxes on investment income. Possible changes to pension rules are in the cards as well. Will Reeves implement a so-called ‘mansion tax’ on home sales above £1½ million? If so, then we share rather different definitions of ‘mansion’—especially in the London real estate market.

The market balance to be struck must lie between deficit restraint, expenditure restraint with a line-up of open hands outside of Reeves’ door, limited ‘soak the rich’ taxes that may harm growth and drive more of London’s wealthier individuals away after April’s changes that abolished non-domiciles, and not rocking the pension world given its status as large holders of gilts with memories of 2022.

If policies materially harm growth, then the gilts front-end may quickly look to how the Bank of England responds not only insofar as December’s expected cut is concerned but also beyond.

I can almost hear the lyrics blasting out of Range Rovers now. “There’s one for you, nineteen for me…..be thankful I don’t take it all….declare the pennies on your eyes…’cause I’m the taxman.”

CENTRAL BANKS—A PAIR OF WARM-UPS

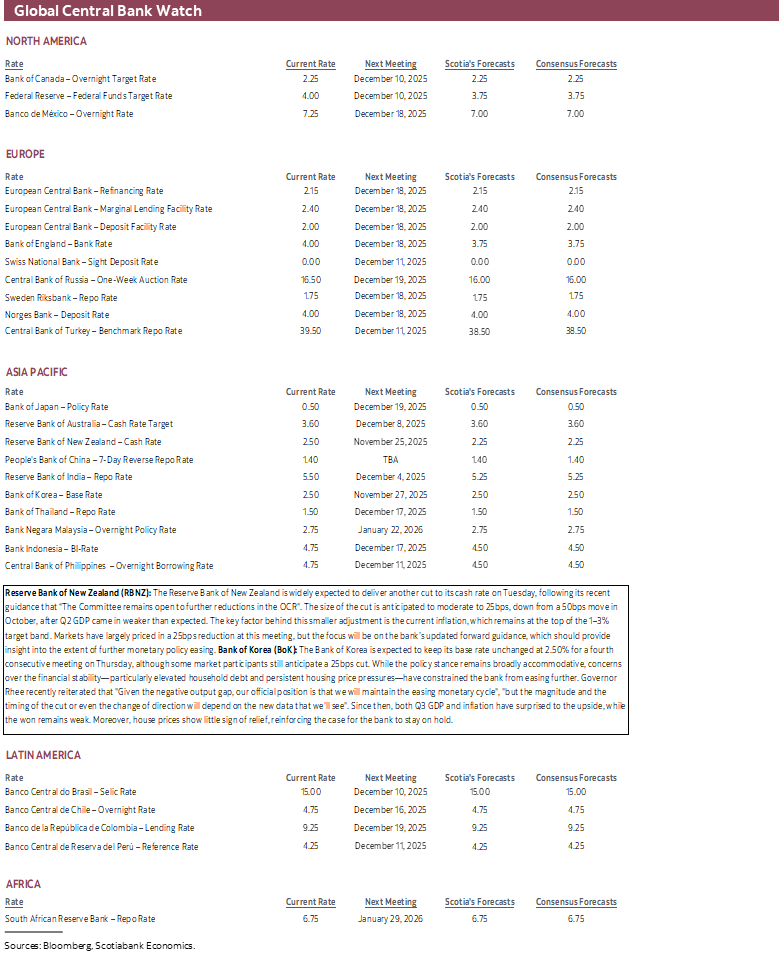

Only two regional central banks weigh in with decisions this week. They’ll be a warm-up for the deluge of decisions by global central banks in December before year-end festivities largely grind their calendars to a halt.

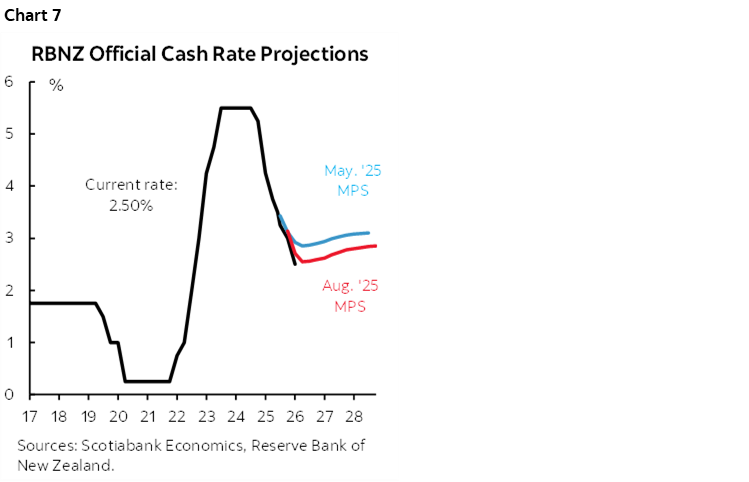

RBNZ—Downsizing, Not Disappointing

Tuesday’s decision is widely expected to deliver a -25bps cut, bringing the official cash rate down to 2.25%. That would downsize the pace from the prior 50bps cut in October that doubled expectations, albeit that the year-to-date path has been an erratic mixture of holds, 50s and one 25. Markets are priced for a quarter point and RBNZ is unlikely to desire a shock in the current environment. The bias at the October meeting was open to further easing: “The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2% target.”

Readings since that meeting have been somewhat mixed. Inflation picked up with total CPI up 1% q/q SA nonannualized in Q3. The unemployment rate edged higher to 5.3% with no job growth in Q3.

As for the forward bias, the RBNZ will publish an updated Monetary Policy Statement including projections with this decision that may inform market pricing that is on the fence between a hold after this meeting and one more quarter point cut (chart 7).

BoK—A Solid Case for Continuing to Hold

The Bank of Korea has been on hold since having last cut its base rate back in May. Some believe it could cut by another 25bps on Thursday, but a hold would be easier to defend.

Guidance offered with the last decision back on October 22nd sounded open to further easing on fears that growth would soften given global trade turmoil. A small majority of Board members indicated openness to resuming policy easing.

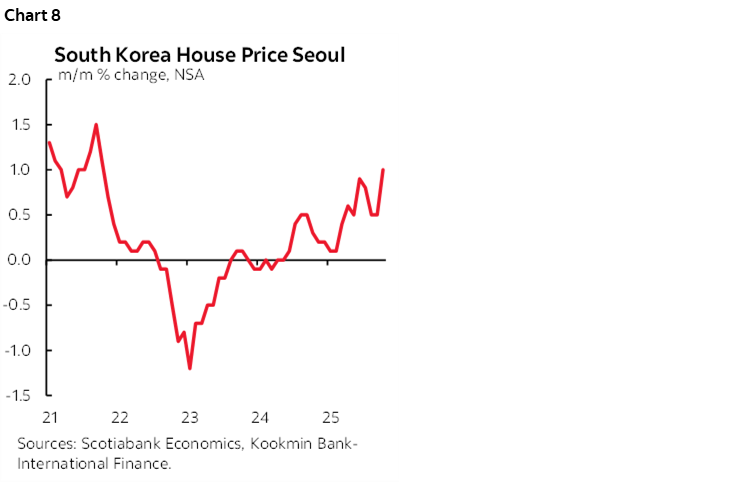

Since then, Q3 GDP came in stronger than expected at 1.2% q/q SA nonannualized (1.0% consensus). So did CPI inflation during October that climbed to 2.4% y/y (2.1% prior) with CPI ex-food and energy up 2.2% (2.0% prior). Financial stability considerations have weighed heavily on BoK’s policy bias particularly toward housing. Seoul’s house prices surged by 1.0% m/m SA in October for the biggest monthly gain since October 2021 (chart 8). In addition, the won has been sharply depreciating since July and is now down by over 7% to the USD and among the weakest performers.

GLOBAL MACRO—BETTER LATE THAN NEVER

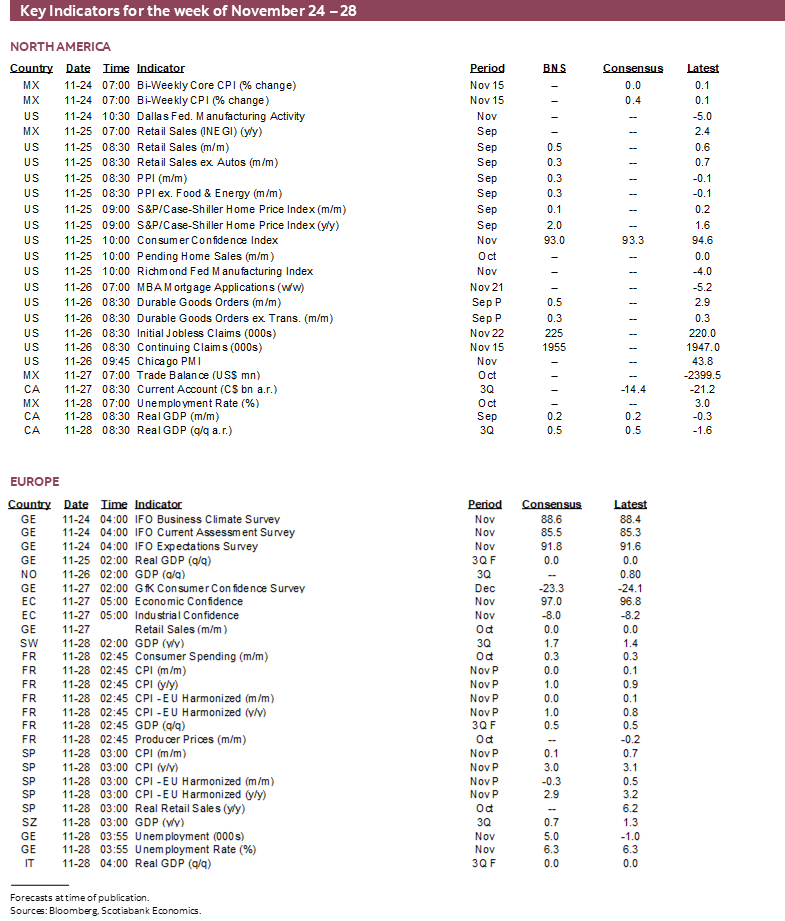

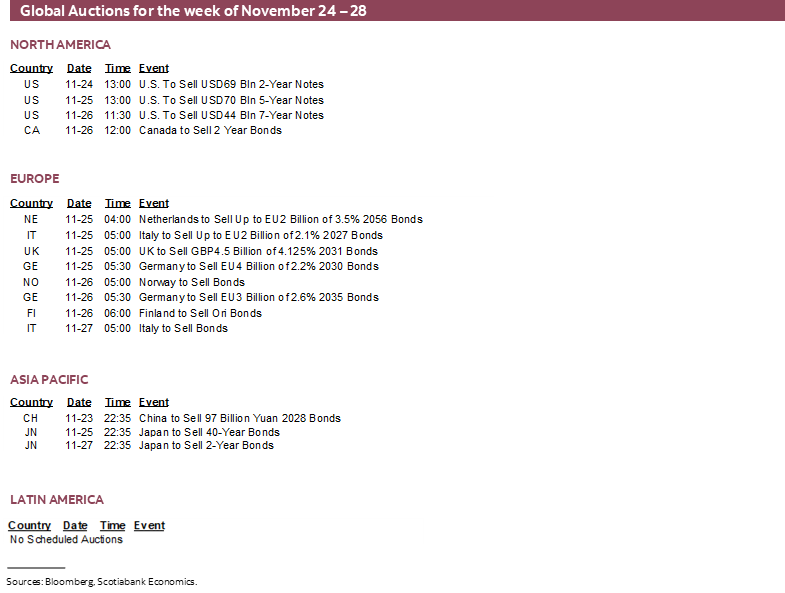

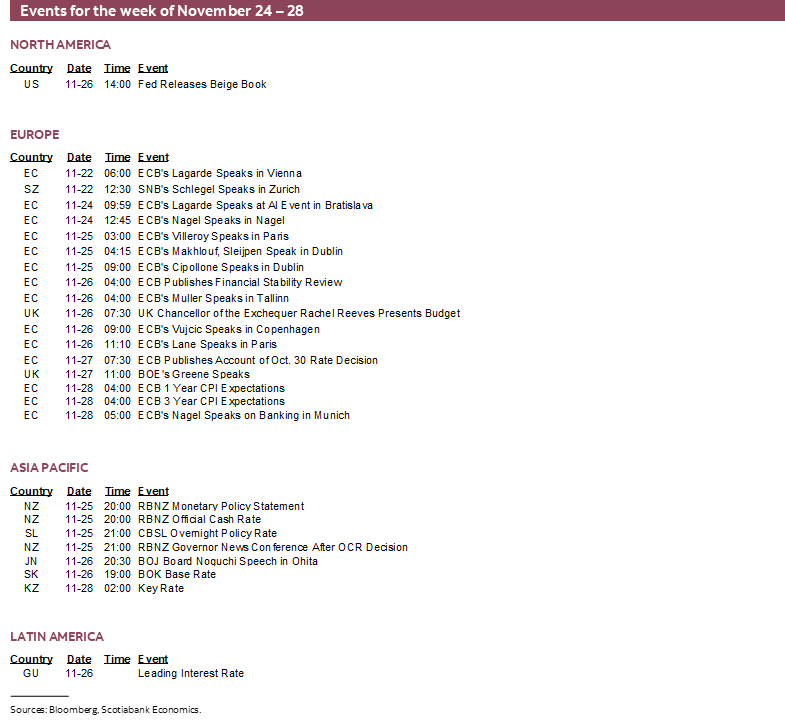

See the accompanying tables for the indicators that are due out over the coming week with the caveat that they reflect what is known as of Friday November 21st. The US list may evolve further but the major releases are probably already lined up. Highlights of the key releases follow by market.

Canada’s Economy—Strrrriiiiike!

On Friday, Canada will report GDP for Q3, plus detailed figures for the month of September, and the preliminary estimate for October sans details.

Q3 growth is likely to land around ½% q/q SAAR on an expenditure-accounts basis that fully accounts for net trade and inventory effects. That’s basically stall speed. Our ability to estimate Q3 growth is limited by virtue of the fact that we’re still missing trade figures from August and September due to the US government shutdown and its effects on Statistics Canada. Inventory figures are also incomplete. Therefore, one should treat the estimates with wider brackets than normal and with higher revision risk than normal once Statcan more fully assesses the trade picture.

Still, anything around that reading wouldn’t surprise the BoC. It forecast 0.5% Q3 growth in the October MPR.

As for the monthlies, Statcan had previously guided that September would be tracking at about 0.1% m/m SA. I’ve bumped that up a bit to 0.2% given data since that guidance was provided.

As for October, it was just the Blue Jays who were throwing strikes. Hours worked fell in each of September and October by 0.2% m/m SA partly because of the Canada Post strike from about late-September to mid-October, and the Alberta teachers strike. Both of those strikes carried direct and indirect effects. It will be important to assess growth independent of estimated impacts.

US—Catching Up

With nonfarm out of the way, next up are several other catch-up releases over the coming week. More may be added, so keep tabs on the various schedules (here, here and here).

Here is the line-up as at the point of publication:

- Retail sales (September, Tuesday): Total sales are roughly estimated to rise by about ½% m/m SA. Among the drivers are expected to be the 2% m/m SA rise in new vehicle sales and higher gasoline prices. Another decent gain in nominal core sales is also anticipated. Key, however, will be converting to inflation-adjusted sales that may be little changed net of price effects.

- US PPI (September, Tuesday): The producer price index will be the final piece of the puzzle to firm up expectations for the Fed’s preferred inflation gauges—PCE and core PCE. Several of its components flow through to PCE along with the weighted contributions from core CPI that equalled 0.22% m/m SA in September. Core PPI may be more likely to swing the core PCE estimate up to 0.3% than down to 0.1%.

- S&P house prices (September, Tuesday): House price inflation is clearly cooling. Tuesday’s updates of repeat-home sales prices in September and the FHFA house price index are likely to extend the pattern. The S&P repeat measure is only up by about 1 ½% y/y from a recent peak of about 7½% in early 2024 and this is way down from the low rate-fuelled boom when prices were up by about 21% y/y in early 2022. Calling disinflation in housing is hardly a brave call at this point.

- Regional manufacturing surveys (November, Monday, Tuesday): Regional manufacturing surveys take on somewhat greater importance absent harder data due to the government shutdown. We already know that the NY Fed’s measure accelerated in November. Monday’s Dallas Fed measure and Tuesday’s Richmond Fed reading will further our understanding of manufacturing conditions.

- Consumer confidence (November, Tuesday): This measure is more skewed toward job markets than the UofM sentiment gauge. It may be that a further weakening of confidence lies in store with job markets looking shakier.

- Pending home sales (October, Tuesday): Sales that have been inked but not yet closed—have been on a generally flat path throughout the past couple of years. October’s reading will inform where completed existing home sales are going into year-end.

- Durable goods orders (September, Wednesday): Expect a surge for the headline reading given that Boeing plane orders jumped from 26 in August to 96 in September. Core orders (ex-plans and defence) are also likely to post a mild gain with AI-related investments assisting.

- Beige Book (Wednesday): The book of anecdotes has generally revealed softening conditions through recent editions. Expect material emphasis on labour market conditions.

- Claims (Wednesday): Data will catch up to the week of November 22nd for initial claims and the prior week for continuing claims.

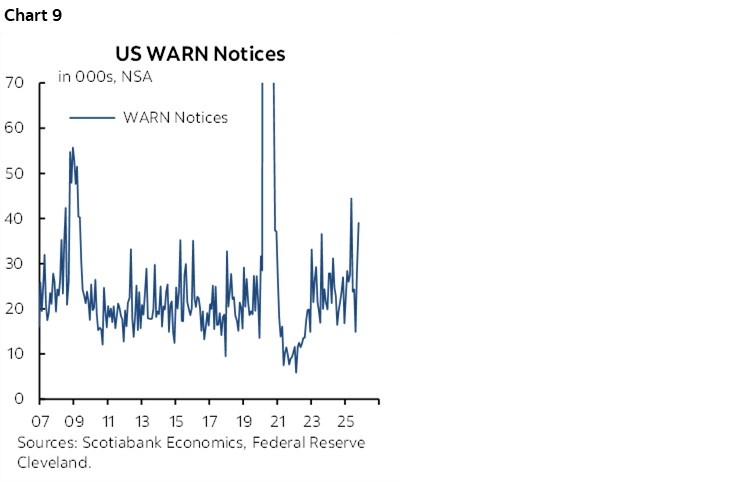

- Advance Layoff Notices: Friday will bring out fresh estimates of WARN Act advance layoff notices that may further inform coming Challenger layoff readings. They have been on an upward trend (chart 9).

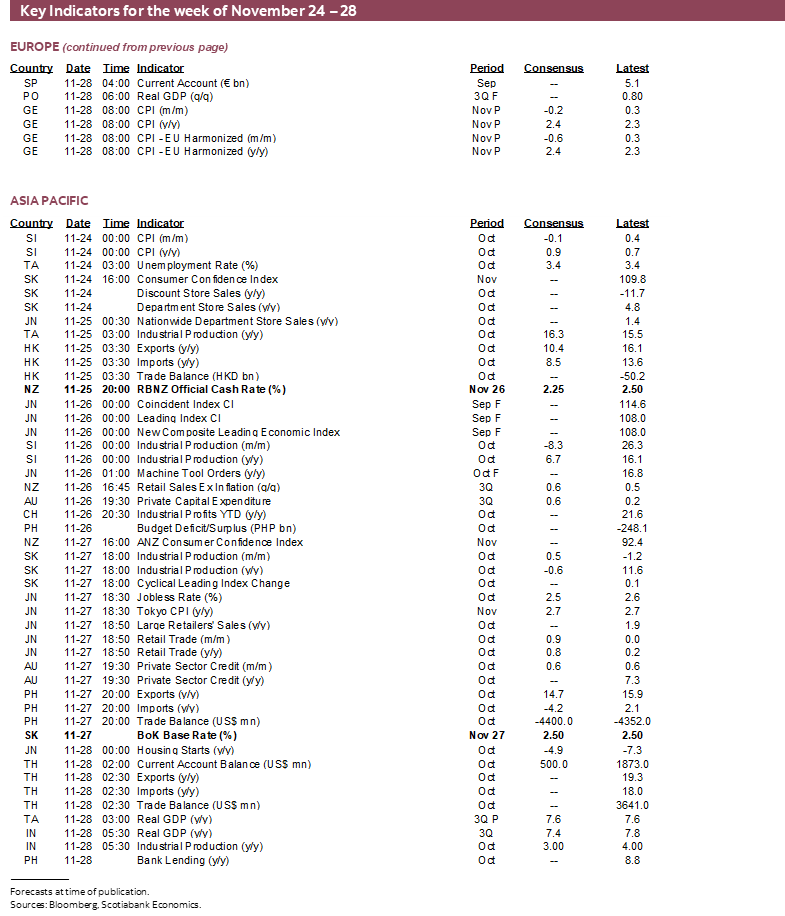

Europe—Nearly Meaningless CPI

Most of the focus in terms of releases will be on Friday’s Eurozone CPI inflation readings. The eurozone add-up arrives the following week, but Germany, France, Italy and Spain release on Friday. Markets and forecasters are in broad agreement that the ECB will stay on hold on December 18th with core inflation running at 2.4% y/y. Fresh data is unlikely change anything in the nearer term.

Asia-Pacific—BoJ Bets Hanging on CPI

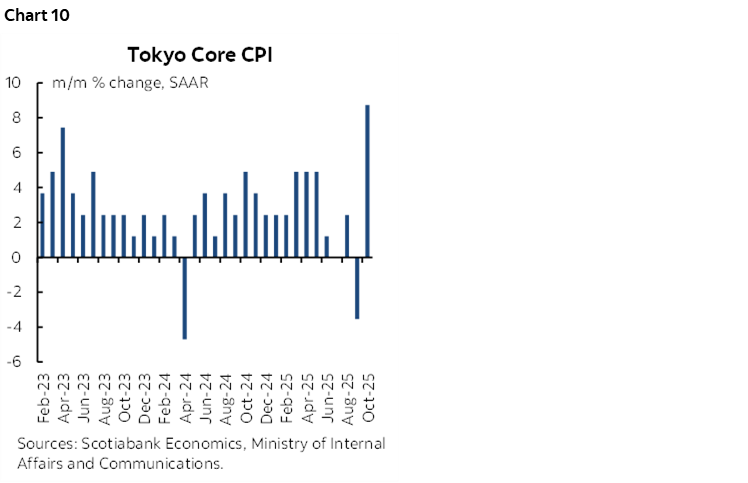

Most of the focus will be upon Tokyo CPI for November on Thursday. Core CPI has been running at about 2.8% y/y with markets assigning material odds to a Bank of Japan hike in January. Core inflation has been volatile in m/m terms for several months such that after the spike (chart 10).

Place the reading in the context of two drivers of higher Japanese yields. One was recent remarks by a BoJ Board member—Junko Koeda— who expressed openness to a rate hike next month. That’s not priced amid wider expectations for a hike in January.

Further, there was a Bloomberg article about new PM Sanae Takaichi’s plans to apply about ¥18 trillion (about $110B) of fiscal stimulus which exceeds prior plans under the previous administration.

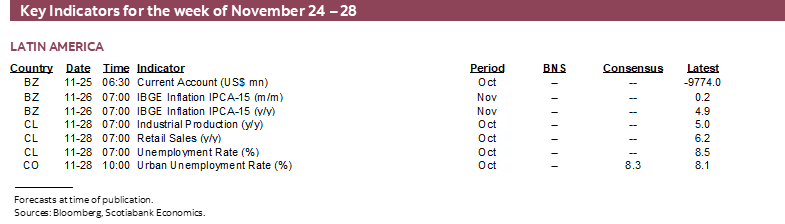

Latin America—Waiting for Chile’s Run-Off

The final full week of campaigning before the Chilean Presidential run-off vote on December 4th will see little by way of other developments this week given a light docket.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.