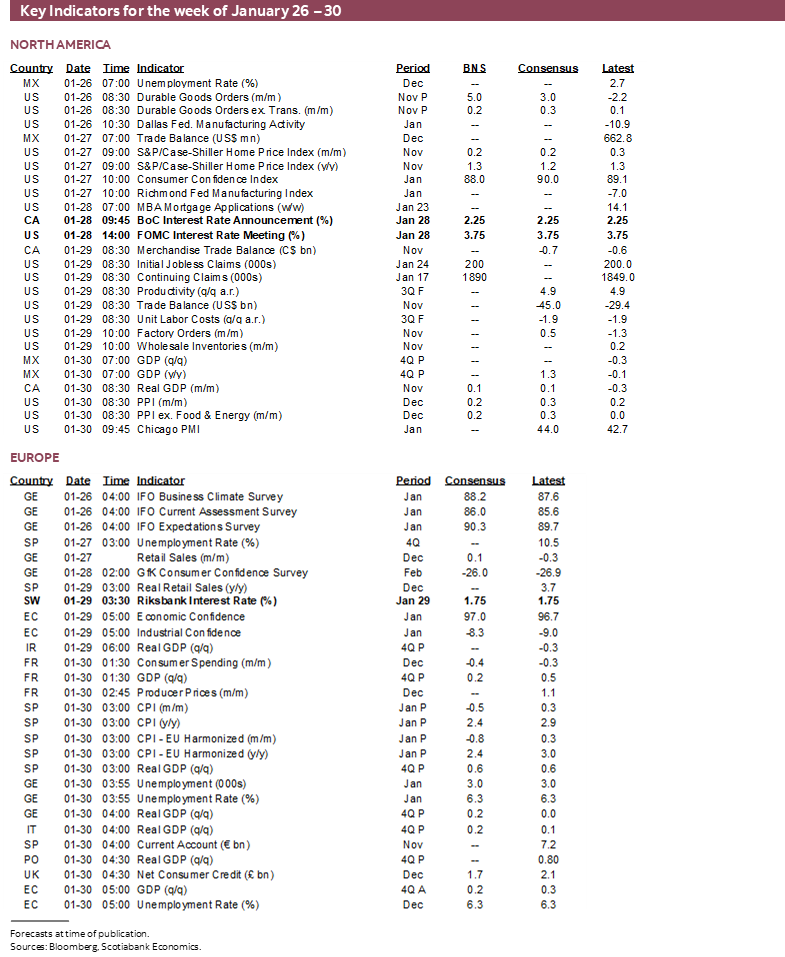

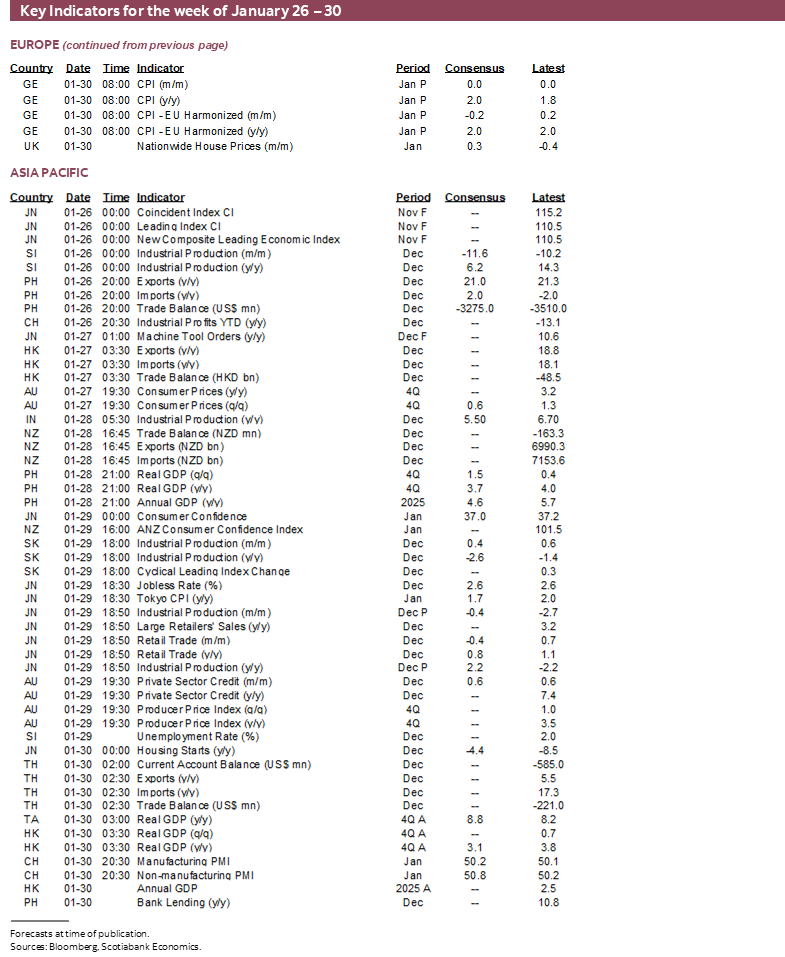

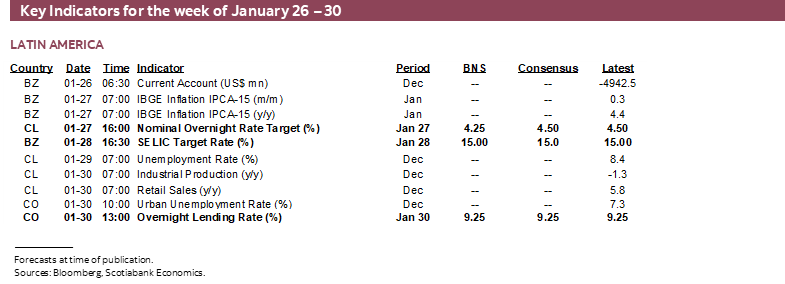

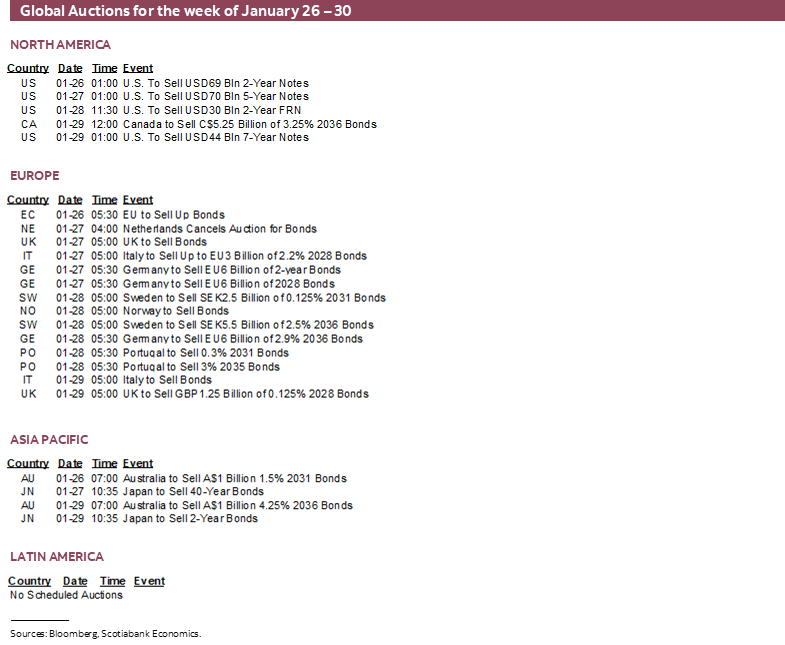

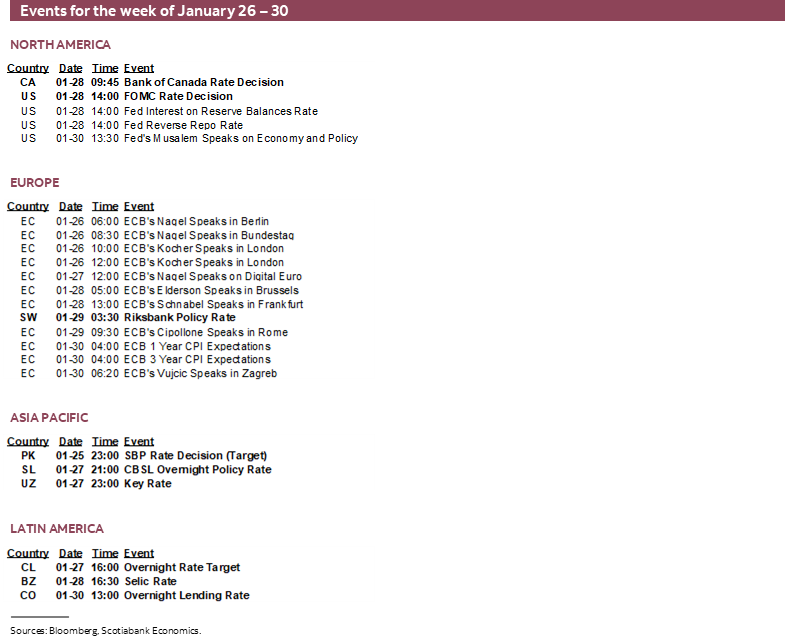

Next Week's Risk Dashboard

- Why USMCA risk is no excuse against investing in Canada

- Canada continues to invest more in the US than vice versa

- BoC Preview — All Talk, No Action

- FOMC preview — A Long Yawn

- BanRep — Whiplash!

- BCCh — Cut Risk?

- BSB — Still Holding

- Riksbank — Next Move Up, Eventually

- SARB — There’s Gold in those Inflation Figures!

- Earnings — Still Magnificent?

- GDP: Canada, Mexico, Eurozone

- China PMIs still marginally expanding?

- Aussie CPI to inform RBA hike pricing

- Eurozone CPI — Little interest, with ECB on a long hold

- Random risk: Fed Chair? Iran assault?

Chart of the Week

Clearly the push over the years toward cancelling meetings if there isn’t much to say or achieve isn’t a philosophy that has resonated across global central banks. There will be seven central bank decisions issued within our coverage universe this week and not much is expected out of most of them by way of concrete actions.

The market influences of central banks may therefore be supplanted by US tech earnings and the fundamentals calendar that emphasizes a wave of global GDP and inflation readings and Chinese PMIs.

Random developments like whenever the nominee for Federal Reserve Chair is announced and whether tensions flare in Iran as the US sends naval forces must be evaluated as information arrives.

The same applies to whether Congress can pass 12 annual appropriations bills by Friday in order to avoid yet another government shutdown.

Before turning to the coming week there are two important Canadian investment themes to explore.

A PAIR OF CANADIAN INVESTMENT MYTHS

Is Canada really living rent free in America’s attic with nothing to offer back? It’s important to address false impressions that could impair the tone of Canada-US trade negotiations.

Is it an unattractive place to invest in solely deserving to have investment diverted from Canada to the US by companies seeking to serve the US market? Again, an important question insofar as addressing whether large opportunities are being seized.

These questions will be examined one at a time.

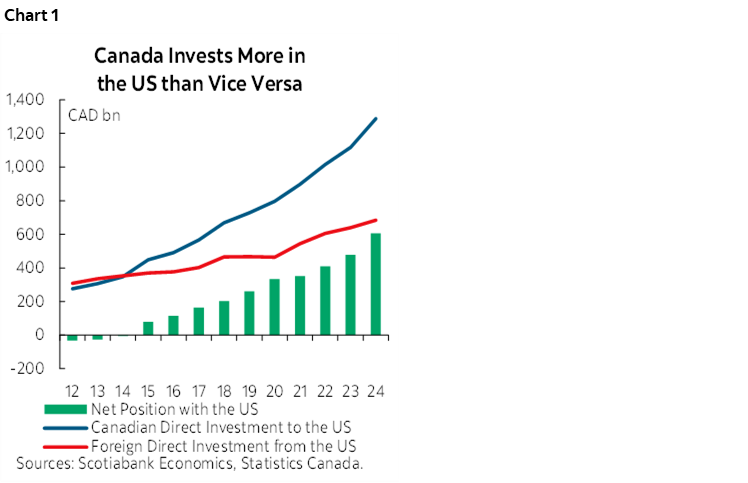

Charts 1–4 should clear the air on the first question. Canadian companies invest more in physical capacity—plant, structures, and equipment—in the US than vice versa and the margin by which it is doing so is rising by the year (chart 1). This investment in the US creates jobs and opportunities for Americans and income returns for Canadians in a win-win scenario.

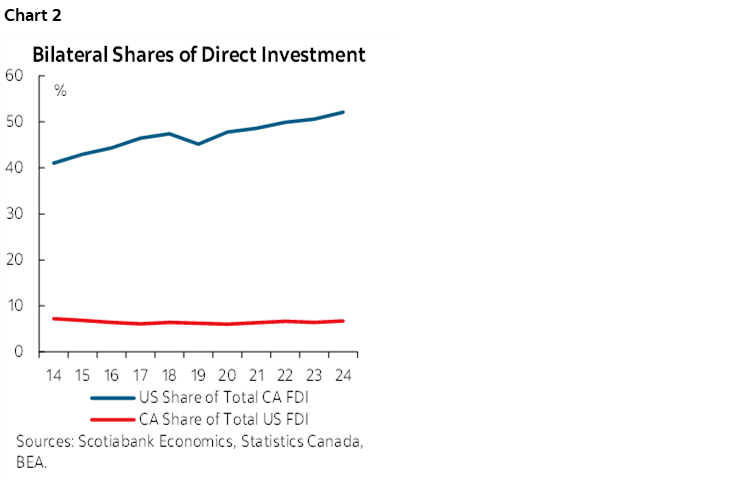

Chart 2 shows that the US is a rising share of Canadian global direct investment with over half being bound for the states. The Canadian share of what US companies invest in Canada has changed little over the years and is less than 7%.

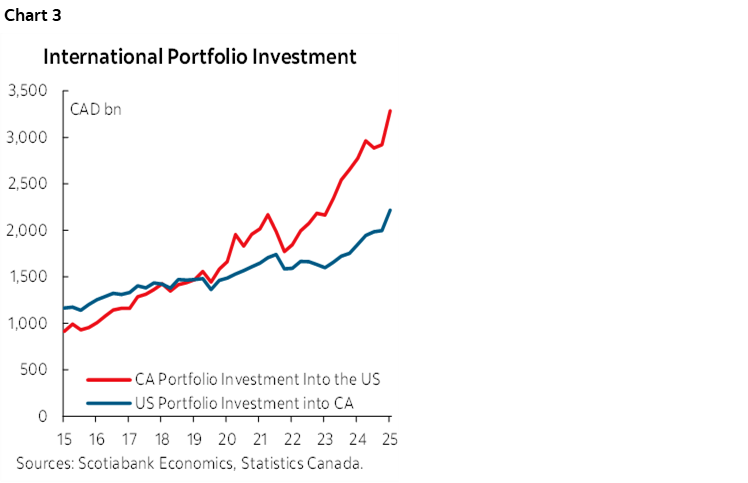

Further, Canadian investors put more money into US stocks, bonds and money market instruments than vice versa and the gap is growing (chart 3).

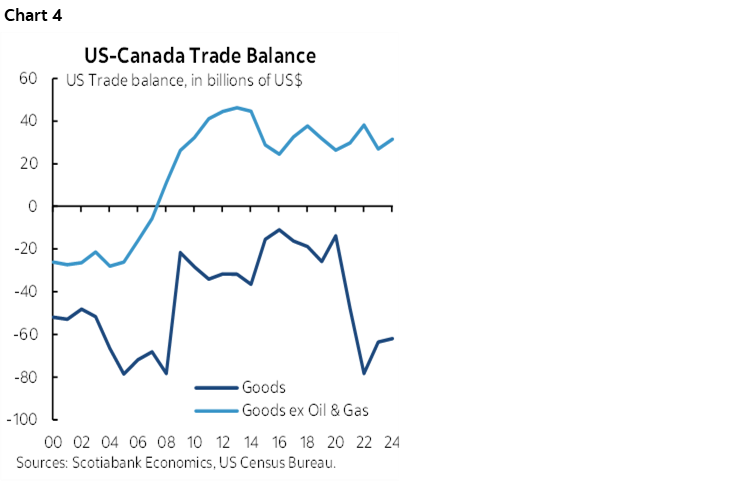

Canada also exports more to the US than it imports but only after including energy. After excluding oil and gas—that the US needs from Canada—the result is a persistent Canadian trade deficit with the US (chart 4). Canadian trade with the US accounts for one-quarter of Canadian GDP. Exports are 36% of Canadian GDP of which 67% now go to the US, equaling about 24% of Canadian GDP that is reliant upon gross exports to the US. 59% of imports come from the US and imports are 41% of GDP is imports, therefore 24% of GDP is imports. This highlights the co-dependence of the two nations as trading partners rather than falsely portraying one as holding all the cards.

Canada should be broadcasting these points stateside. By investing more in the US than vice versa and importing from the US than vice versa excluding energy, Canadians are making strong contributions to the performance of the US economy. No mooches here. Paying their rent. Canada is no newcomer to investing the US as other countries may be with recent pledges; it has been there longer than many other actors, so don’t rock the boat.

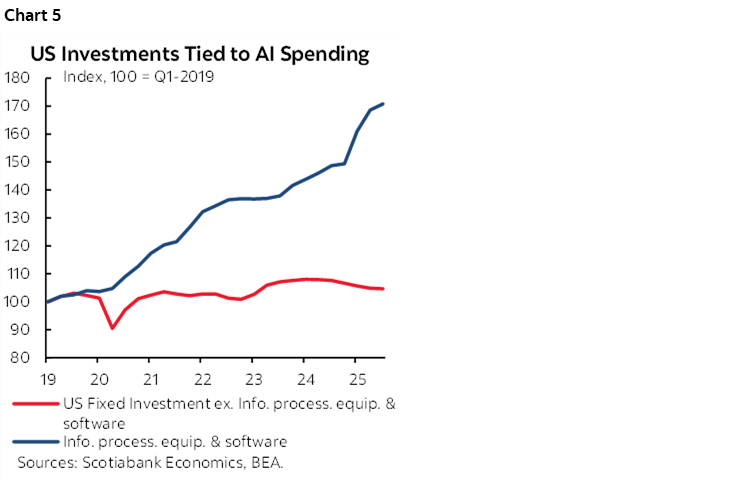

Such investment is vital to the US economy. Take AI-related investment out of the picture, and investment within the US economy is contracting (chart 5).

On the second question regarding whether Canada is an attractive place to invest for purposes of serving the US market, I’ll start by turning it right around. Why aren’t you doing so?

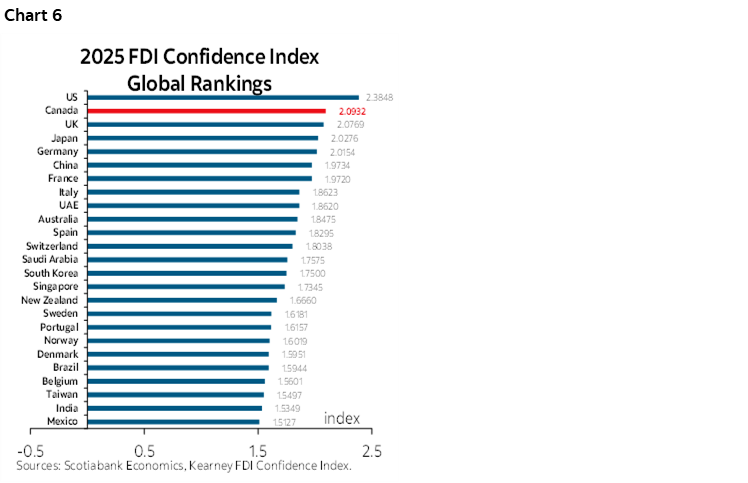

International comparisons of the attractiveness of various markets for foreign direct investment position Canada at #2 in the world (chart 6).

The average effective tariff rate being imposed on Canada by the US is about 6%. Take the handful of the most affected sectors out of the numbers and the average effective tariff rate drops to around half that.

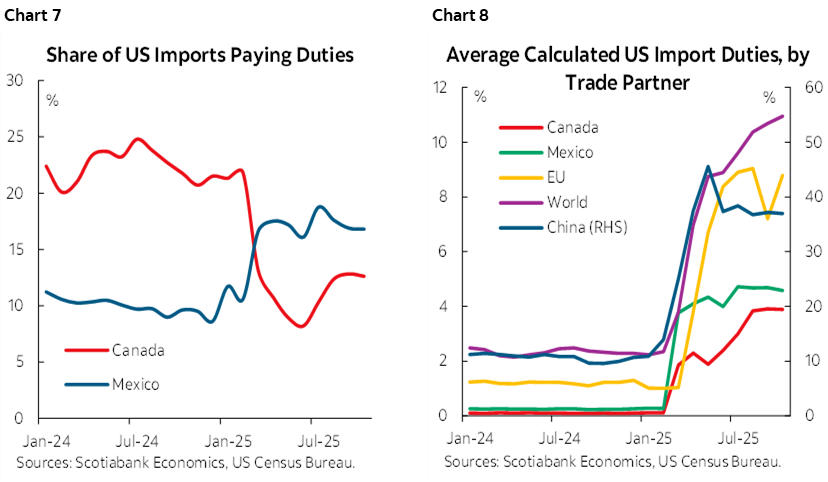

If you’re CUSMA/USMCA compliant, then you’re not paying tariffs. Around 90% of Canadian exports are compliant (chart 7). Taking into account the share of trade that is CUSMA-compliant reveals a still very low effective tariff rate on US imports from Canada (chart 8). That’s also true relative to the rest of America’s trade partners which implies the potential for trade diversion in Canada’s favour.

The Canadian dollar has plunged in value from about $1.20 USDCAD (or 83 cents US) to about 1.37 now (or just under 73 cents US). This has insulated the country against harsher trade realities. China has borne the brunt of the revaluation of the US trade deficit in part because the yuan’s dirty managed peg to the dollar. This also lessens China’s appetite for investing abroad—such as in US Treasuries—as it generates fewer foreign currency receipts to reinvest. Canada’s trade balance with the US is not appreciably different from where it was in the pre-pandemic period before the temporary post-pandemic US recovery drove US imports higher.

Now pair the arguments. #2 FDI destination in the world. CAD has offset a modest tariff shock and then some and especially relative to others. So why aren’t you investing in Canada?

One possibility is feared tariffs, but they’d have to be huge to offset the CAD argument, and CAD would likely depreciate further as an offset; it’s like a game of trade whack-a-mole. Some industries may not invest because imported inputs are more expensive with a weaker currency. I don’t find the argument that the CUSMA/USMCA agreement will be torn up to resonate; hubris aside, that hasn’t been the US attitude to date and the vast majority of US industries that testified at USTR hearings strongly supported the USMCA deal. These are what I think are the probabilities for various scenarios:

- tear it up (very low): A six-month letter of notice to withdraw would likely need to be passed by Congress which is not assured. If it were, then challenges could go to the Supreme Court, risking failure. The domestic lobby in the US is strongly supportive of USMCA.

- Roll it over (very low): Triggering the provision to merely extend for another 16 years is very unlikely in this environment.

- Annual reviews (40–50%): The USMCA/CUSMA agreement affords the opportunity to conduct annual reviews up to ten years max at which point parties need to decide if they’re in or out. That’s 2.5 administrations from now in the US. This scenario would drive persistent uncertainty, but without fundamentally jeopardizing the agreement.

- A deal (40–50%): There is a reasonable path to a deal perhaps before the midterms that combines security and trade issues.

For most companies, however, the decision not to invest is one that should be challenged by shareholders pressuring their boards and in turn pressuring management. At a minimum, present the cold hard math behind refusal to invest. Then be held accountable in what may simply be yet another excuse not to invest.

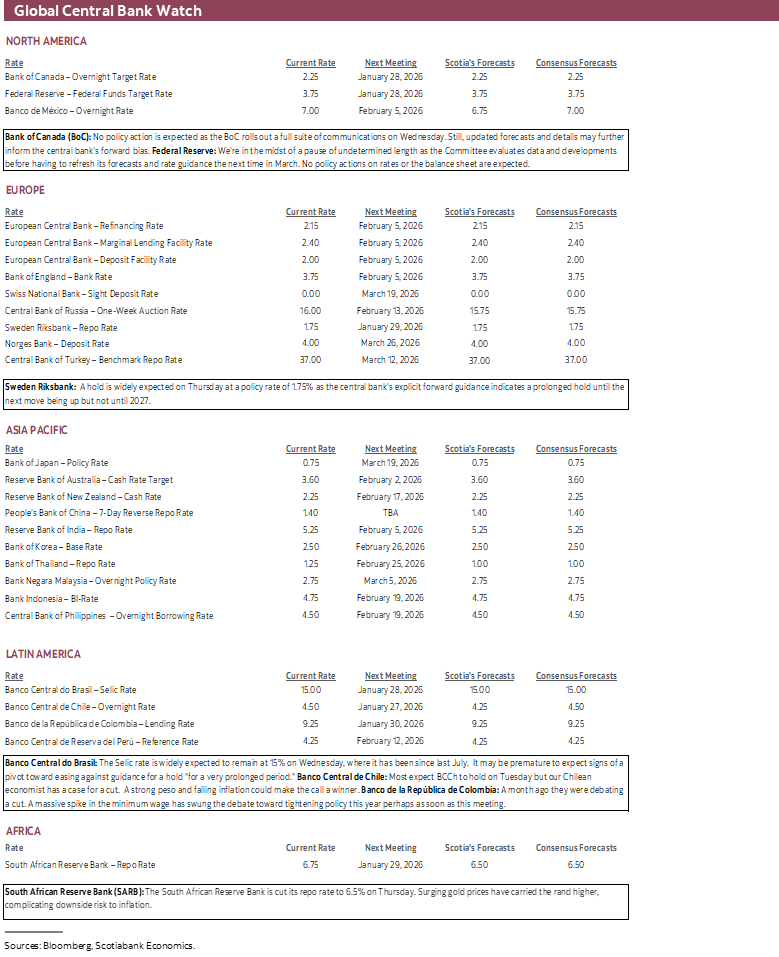

BANK OF CANADA—ALL TALK, NO ACTION

The Bank of Canada will fire off everything it has by way of communication tools on Wednesday—and do nothing. Nothing by way of immediate actions, that is, but they may help to further inform key questions concerning their forward bias as it feeds into cut, hold, hike debates. Markets continue to price the next move to be up but not until late year and we continue to forecast 50bps of hikes late this year.

The statement will be here and lands at 9:45amET along with Governor Macklem’s written opening remarks to his press conference (to be here at that time) and the Monetary Policy Report (to be here) that includes full forecast updates. He and SDG Rogers will deliver a press conference at 10:30amET for around 45 minutes plus or minus; I recommend running multiple feeds (such as CPAC with translations) since the various outlets frequently have a/v and translation (if needed) issues.

No policy rate change is expected from the present 2¼%. No balance sheet changes are expected as we’re in between phases with the BoC having already pivoted last year toward expanding its assets first through repo then through the late-year decision to purchase bills and a long way off from returning to drive gross purchases of GoC bonds. That latter step likely won’t come until well into next year and it will be in the regular conduct of monetary policy (ie: not QE) as currency in circulation and settlement balances rise on the liability side to be invested in a cleaner balance sheet more dominated by GoC bonds like the days of old. CORRA is smack dab on top of the overnight rate, so there is also no reason to be addressing funding conditions. It seems everything is just tickety-boo at 234 Wellington Street in Ottawa.

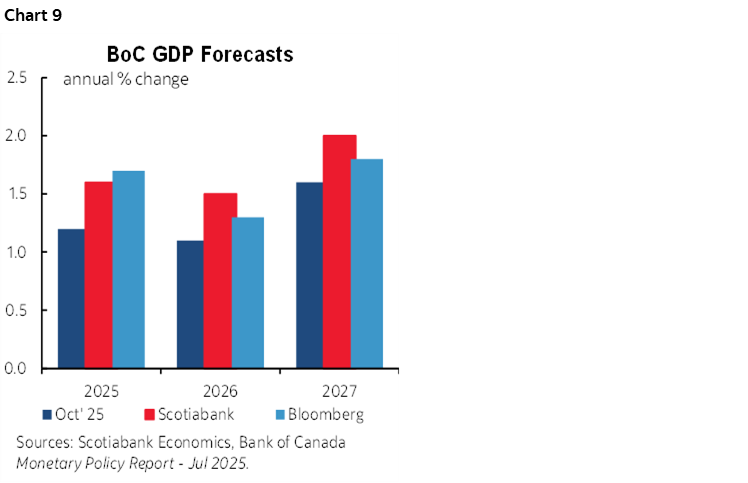

Or is it? The numbers will do more of the talking this time. They may have to raise their GDP forecasts at a minimum for 2025 given tracking to date, and we are a little higher than their October 2025 forecasts for 2026 and 2027 (chart 9).

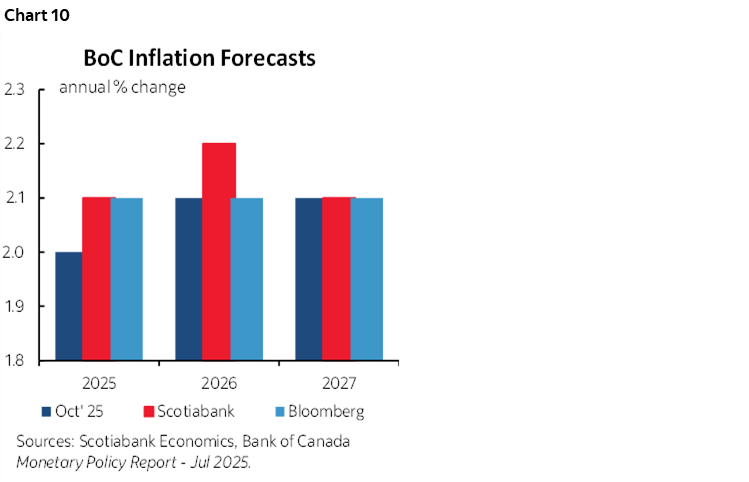

Our present January forecasts are slightly higher than the BoC’s October 2025 forecasts for inflation in 2025 and 2026 and the same in 2027 (chart 10). In my opinion, BoC forecasts represent a combination of best efforts and adjustment to the messages they choose to deliver when they choose to do so.

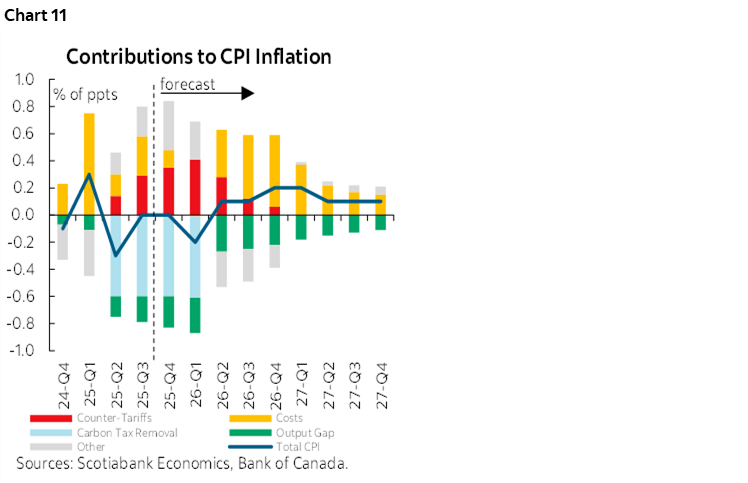

Key is will they repeat chart 11 in unaltered format and hence leave their own inflation outlook unchanged at 2.2% y/y by 2026Q4 (2.3% using the average of trimmed mean and weighted median CPI) and then 2.1% by 2027Q4 (2.1% core)? That alone would reinforce the impression they’re not really open to further easing and, if anything, slightly more concerned about upside risk to their 2% target. They would have to suddenly indicate they are worried about materially undershooting the 2% inflation target over the medium term in order to have markets think they are open to further easing. This is improbable.

One uncertainty here—beyond how they project actual GDP from a higher post-revision starting point last Fall—is whether they adjust potential GDP. Some of the GDP components that were revised higher point to a need to also revise higher the level of potential GDP (the economy’s supply side) as at last Fall. Their prior estimate for the economy’s noninflationary speed limit (ie: the rate of growth of potential GDP) was for 1% in 2026 and 1.3% in 2027. Our estimates are higher by ¼% to ½% per year. Having said that, potential GDP is an unobservable construct with a wide margin of reasonable estimates.

The April MPR is the more likely context in which to revisit potential. Ditto for the neutral policy rate range (presently 2.25–3.25%). It’s possible that the BoC just continues to talk through changes in output gap estimates as they did in the December statement despite knowing the GDP revisions, although that’s tougher for them to do now as they present an updated forecast round.

They also need to more formally incorporate federal budget effects that they have not done yet.

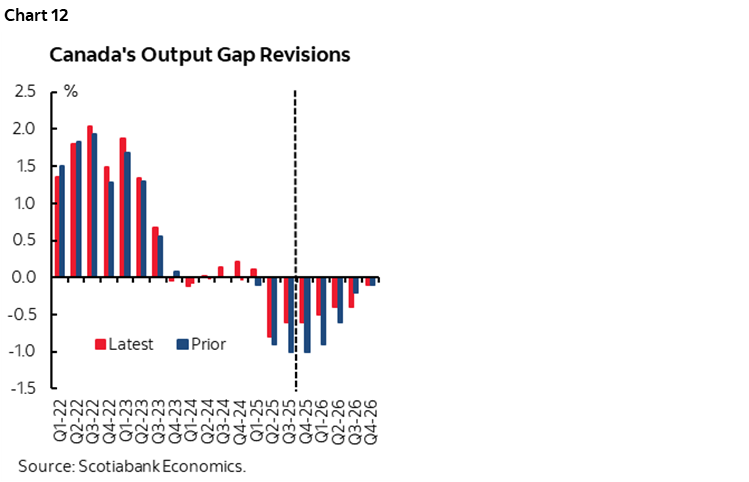

Or will they alter the aforementioned chart and underlying calculations by lowering the drag on inflation from less estimated slack due to recent GDP revisions? Chart 12 shows our estimated reduction in the output gap on the heels of last Fall’s GDP revisions stretching back years in time.

If they do that, then I doubt they’d have confidence to offset the impact of less slack on higher inflation than previously estimated by reducing their estimate of the sum total of cost pressures on inflation. Recall some of the examples:

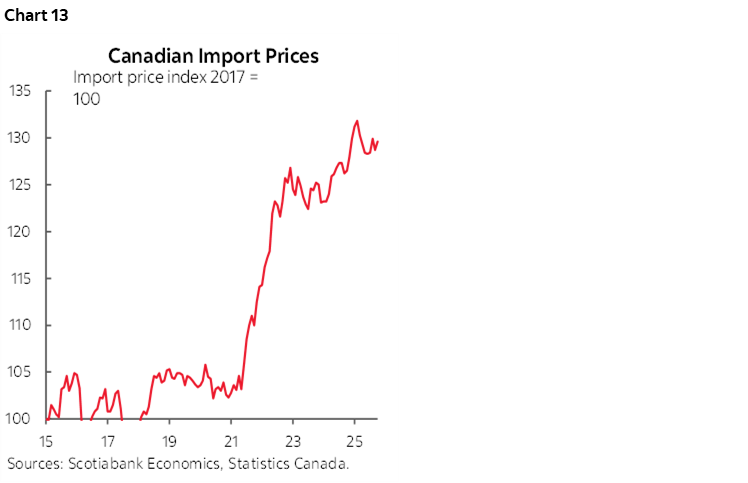

- CAD has depreciated by nearly two dimes since its pandemic peak. The lagging effects on import prices are still evolving and threatening further pass through (chart 13).

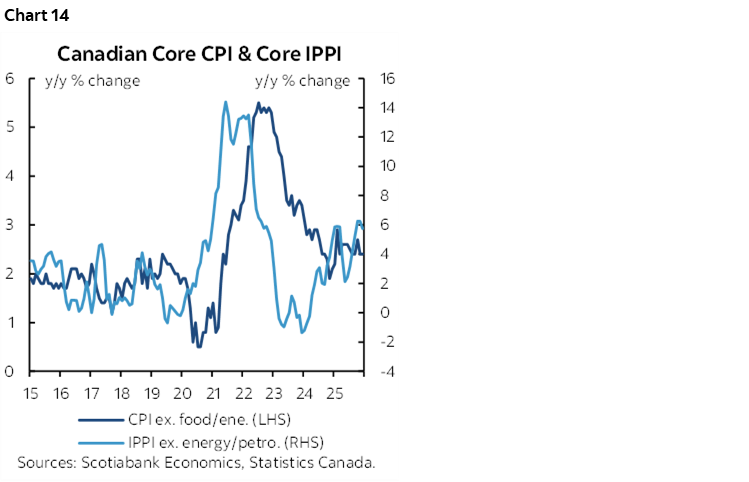

- producer prices continue to soar and lagging effects point toward upside risk to underlying core inflation (chart 14). This reinforces the prior point but also adds to it.

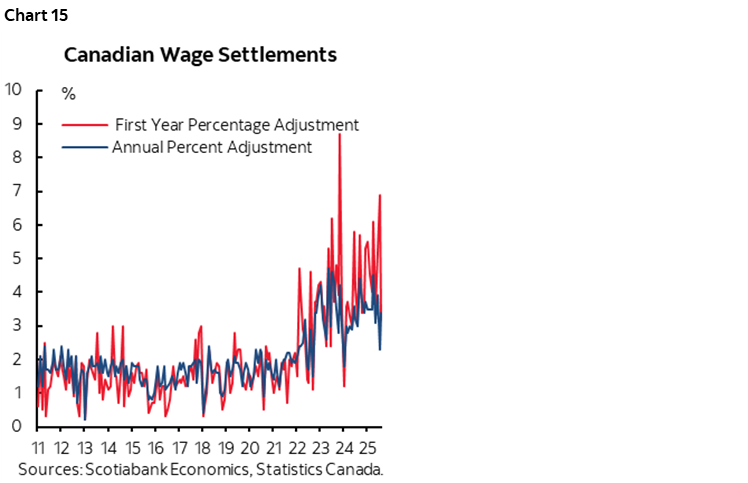

- wages continue to grow faster than inflation. This remains the case for wage settlements for about one-third of Canadian workers that are unionized (10% in the US). The 3–4 year contract periods containing revenge wages or make-up pay point to persistent wage inflation over coming years (chart 15). Moribund labour productivity trends are well established. Wage growth exceeding productivity squeezes company margins, restricting revenues while pumping up compensation. Shareholders are likely to press for sharing the incidence effects through higher prices.

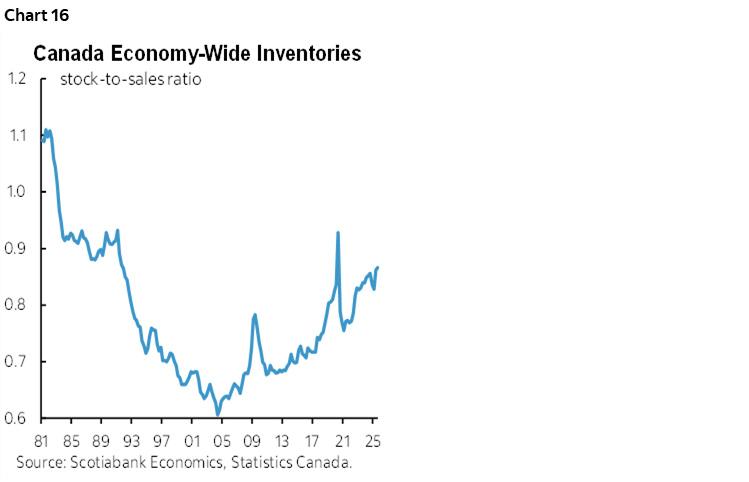

- inventories relative to sales are high (chart 16). It’s a changed world for just-in-time as companies pad their buffers given greater border frictions and business interruptions. Financing and storage costs need to be passed on including to consumers.

- supply chains are evolving. They require partial or complete reinvention with associated costs to establish new supplier relationships, new capacity, new workers etc etc.

As for statement changes, the bulk of the emphasis will be placed upon incorporating references to updated forecasts which lessens the usefulness of comparing this one to the December statement that was recapped here. Key will be whether this sentence remains largely or entirely intact:

“If inflation and economic activity evolve broadly in line with the October projection, Governing Council sees the current policy rate at about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment.”

If so, then the BoC is kicking off the new year with the same long-pause guidance. A slightly more dovish or hawkish spin or qualifier could be impactful to markets but is not expected.

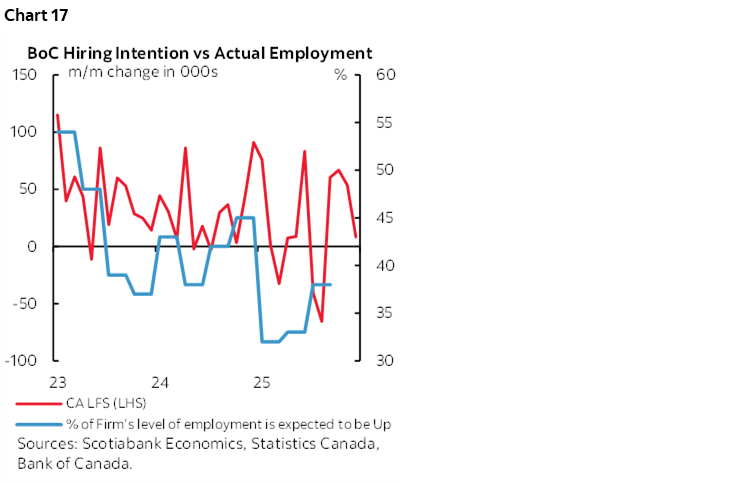

One reason for not expecting a more dovish spin is that the BoC has kind of blown it on jobs. The December statement placed excessive emphasis upon hiring intentions through soft data, yet hiring intentions perform poorly as a predictor of actual job growth (chart 17). Canada has generated nearly 200k jobs in the past four months. Had that been the US, they’d be up by around 1¾ million and clearly they are not.

As for trade negotiations with the US, please see the earlier section for my views. At this point, the BoC has no further information to go by which adds to long pause arguments. When we get closer to developments, headline risk will flare but I find dovish voices are being extraordinarily premature in assuming only the worse outcome while assuming it will only be a demand shock absent supply side offsets that could complicate the BoC’s ability to act.

Also toward the list of top cautions is the impact of massive tech investments in the AI boom. Hopefully I’m not the only one shuddering at the thought of drawing parallels between the pictures in this article (available in full for terminal subscribers) and the SPV flow charts that confused many in financial markets into the GFC—until it was too late.

FEDERAL RESERVE—A LONG YAWN

Nothing is expected from this meeting. Absolutely nothing. Markets are priced for no policy rate change. No one within consensus expects a change. They are fresh off projections including an updated ‘dot plot’ in the December 10th communications and it’s too soon to contemplate material changes before the next round in March. They just heaped an extra US$40B per month into the ample reserves framework. They are not going to be comfortable to pre-commit to what they have in mind for the next decision on March 18th by which point they’ll have a tonne of additional data and perhaps further information on other policy developments.

Relatively minor things to watch for include statement tweaks, the tone of Chair Powell’s press conference and dissenters.

The statement may upgrade the reference to the economy expanding at a “moderate” pace to something stronger. Watch for continued reference to a higher unemployment rate but strike “through September.”

Powell’s press conference may sound more neutral than justified, for now. On inflation, he is likely to repeat his view that inflation risk may be temporary over coming months, but that opinions vary on the Committee. On jobs, he may flag deteriorating payrolls but point to a broader suite of data and include references to offsets on immigration policy and its effects on the unemployment rate.

Powell is likely to emphasize that on balance, the Committee thinks policy is well situated for now.

The voting status of the regional Presidents rotates with this meeting, but two or a maximum of three—all Governors—may dissent in favour of a rate cut. Governor Miran is sure to do so and may be joined by Governor Bowman given her recent remarks and perhaps Governor Waller. Cleveland’s Hammack votes this time and is a relative hawk who prefers a lengthy rate hold. Philly’s Paulson has indicated she prefers holding. Dallas President Logan has been warning for some time not to count inflation risk as down and out, and Minneapolis Fed President Kashkari has cautioned that inflation is still too high and “another price bump” could arrive.

What has changed is growing evidence that the US consumer cycle is maturing. Inflation-adjusted personal disposable income growth has crawled to a halt. Real consumption growth is tracking 2¾% q/q in Q4 after 3½% growth in Q3 but this is at the expense of the saving rate that at 3½% is the lowest since October 2022 and barely positive in real terms. The wealth effect on consumption has diminished as real house prices have fallen and most American households own negligible amounts of equities.

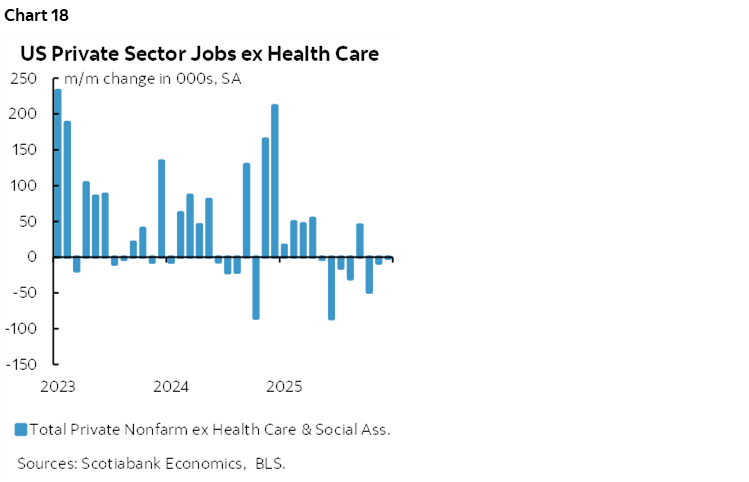

With inflation now at 2.8% y/y, the Committee won’t have confidence they have won the battle. They should have more concern about the jobs picture; chart 18 shows that private nonfarm payrolls excluding one upbeat sector (healthcare) have been trending lower.

BSB—STILL HOLDING

Banco Central do Brasil is widely expected to stay on hold at a Selic rate of 15% on Wednesday. It has been parked at this rate since last July. This holding pattern followed 450bps of rate hikes to a new all-time high for the policy rate. The December statement continued to emphasize that “maintaining the interest rate at its current level for a very prolonged period is appropriate to ensure the convergence of inflation to the target.” Markets will watch for hints of a future shift toward easing but it’s premature to expect that at this meeting.

BCCH—CUT RISK?

Consensus expects Banco Central de Chile to extend its hold on Tuesday but our Chilean economist—Jorge Selaive—expects a 25bps cut down to 4¼%.

The easing pattern slowed over 2025 with rate cuts spread out by 5–7 months between the two cuts followed 625bps of cuts starting in mid-2023. Having cut in late 2025, consensus may be thinking another one now may be too soon.

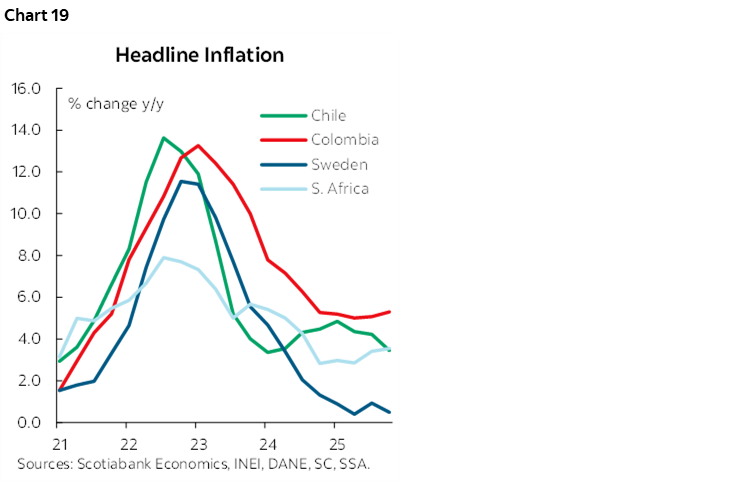

Doves can point to the appreciating Chilean peso. CLP has rallied by just under 10% to the dollar since October. Inflation has fallen back to 3½% with core at 2.8% compared to the inflation target of around 3% (chart 19, along with inflation readings for others to follow). BCCh expects inflation to drop further to 3% over 2026H1.

BANREP—WHIPLASH

The last time that Colombia’s central bank delivered a rate hike was in April 2023. It could restart a tightening campaign on Friday.

BanRep is widely expected to raise its overnight lending rate, but opinions are varied on how much it will go up. Most expect 50bps to 9.75%, with minority opinions in favour of 25 or 75.

Why hike? Clearly a lot changed since the December 19th decision when four voted for a hold and three wanted to cut.

A 23% minimum wage hike will do that. The leftist government of President Gustavo Petro announced this raise on December 29th—ten days after BanRep’s meeting. In total, the minimum wage has been raised by 42% in three years. Spend it quickly, as most economists immediately raised their inflation outlooks and pivoted toward expecting the central bank to lean against the measure. About one in two workers in Colombia work at the minimum wage or less and will see a major boost to their spending power until prices adjust.

RIKSBANK—PROTRACTED HOLDING PATTERN

Sweden’s central bank is widely expected to remain on hold on Thursday at a policy rate of 1.75%.

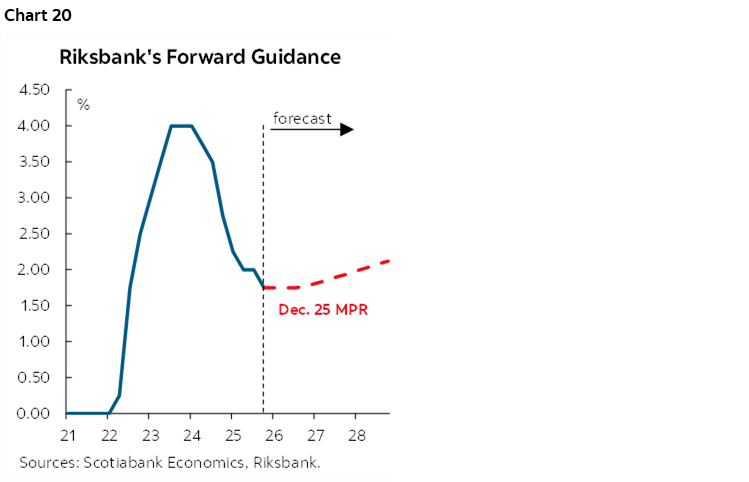

The central bank publishes explicit forward rate guidance and its December projection indicated a prolonged hold at 1.75% until the next move being up but not until 2027 (chart 20).

SARB—THERE’S GOLD IN THOSE INFLATION FIGURES!

The South African Reserve Bank is expected to cut its repo rate by 25bps to 6.5% on Thursday.

SARB Thursday. This would extend the easing cycle that has been in place since September 2024.

The appreciating rand lends room for monetary easing. Up 7% since November, the rand has been benefiting from surging gold prices that are closing in on US$5,000/oz.

The currency’s rise contributed to recent comments by the central bank in favour of possibly hitting the 3% inflation target this year. At 3.6% y/y with core CPI at 3.3%, they don’t have far to go. By extension, a further unwinding of the restrictive policy stance may be sensible.

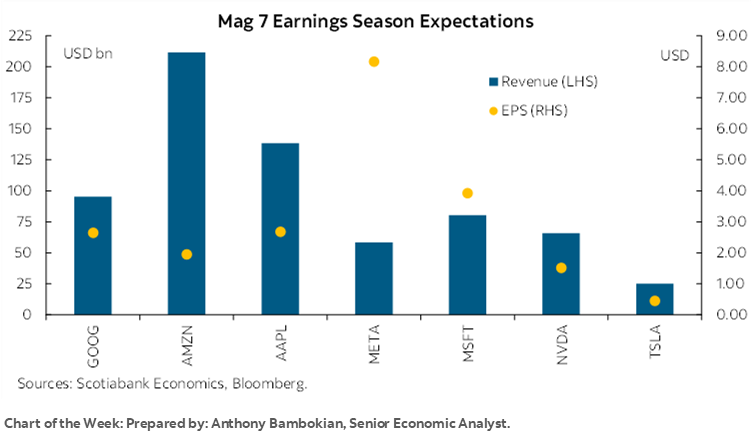

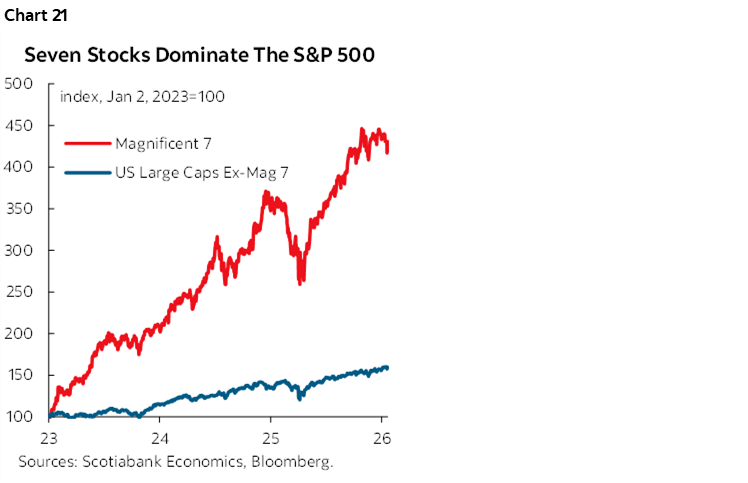

EARNINGS—STILL MAGNIFICENT?

About one-hundred S&P 500 firms release quarterly earnings this week as the season accelerates.

The main emphasis will be upon the tech darlings, aka the Magnificent Seven (chart 21). Meta Platforms, Tesla and Microsoft all release on Wednesday followed by Apple on Thursday. Alphabet and Nvidia are later. We already know Intel’s results as markets were unimpressed by guidance.

Earnings from Canadian companies will include names like Rogers (Thursday) and CN (Friday).

GLOBAL MACRO READINGS

A substantial line-up of global macroeconomic indicators also lies in store in a highly active week.

Canadian GDP is expected to post modest growth of around 0.1% m/m SA in November but December may face downside risk given a drop in hours worked (Friday). December was an usually cold and snowy start to winter compared to recent years including these folks who flagged it as the second coldest month of December in two decades. There have also been lost hours worked—and hence GDP—effects stemming from labour strife. These effects could temper interpretations of the data.

Several countries and regions will update Q4 GDP figures. They will include the eurozone, Germany, France, Italy and Spain on Friday, plus Mexico (Friday) and some Asia-Pacific economies like HK, Philippines, and Taiwan, and Sweden.

China updates the state’s purchasing managers indices but not until next Friday evening; they’ve been barely hovering in expansion territory up to December after a wave of more upbeat January readings across the world at the end of this past week.

Job market conditions in Mexico (Monday) and Chile (Thursday) will be refreshed.

Whether market pricing that is leaning toward the RBA hiking rates as soon as its February 3rd meeting makes sense of not may be further information by a batch of inflation readings. Tuesday brings out Q4 CPI including underlying measures and the December spot measure, while Thursday reveals producer price inflation in Q4.

Friday also starts to bring out readings for Eurozone CPI inflation in January. Germany and Spain will release ahead of the other countries and Eurozone tally the following week.

And that’s enough. Other indicators will be covered in regular daily notes throughout the week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.