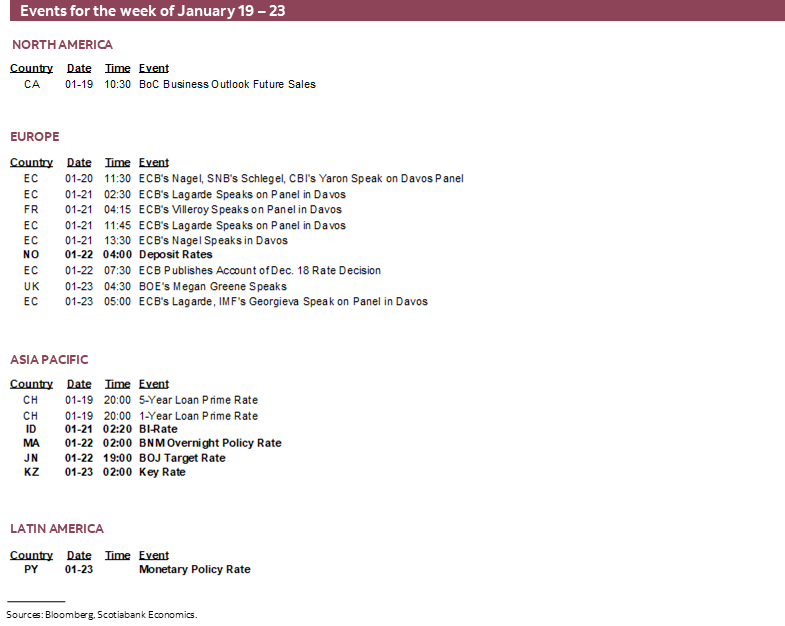

Next Week's Risk Dashboard

- SCOTUS IEEPA saga returns…

- …as Trump heads to Davos for his anniversary

- Bank of Canada Comment

- Canadian CPI preview

- BoC’s stale surveys

- Canada is likely to benefit from China deal

- Politics to constrain the BoJ

- BI, Negara, Norges to hold, Turkey to cut

- PMIs Aplenty

- Tracking Canadian holiday shopping

- US data catch-up continues

- UK Jobs, CPI and holiday spending

- Jobs Down Under

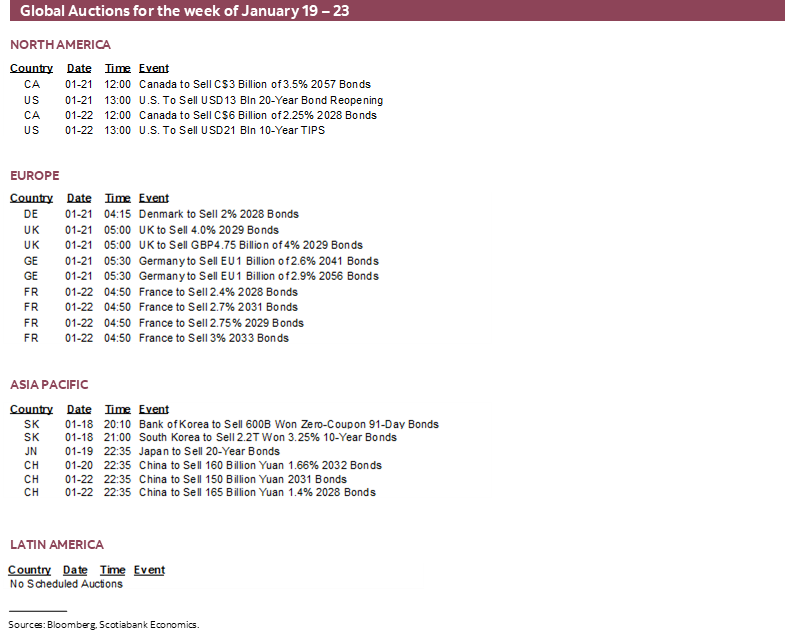

- Global macro

- US holiday Monday: MLR Jr Day

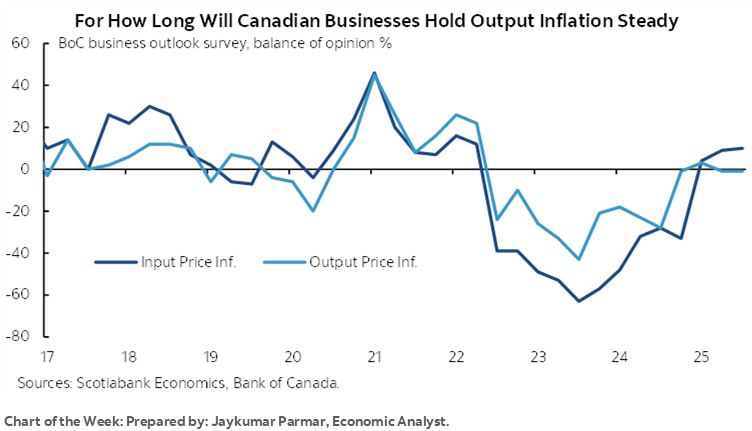

Chart of the Week

As earnings season progresses and broadens out, economists return to the task of dissecting a wave of central bank decisions and major economic indicators. The high drama surrounding when the US Supreme Court will issue its IEEPA tariff decision returns on Tuesday (10amET) after the US Martin Luther King Jr holiday with another round of case opinions that may or may not include tariffs. Will they reward or disappoint Trump on the first anniversary of his inauguration, or avoid the date altogether? My hunch is the latter, perhaps especially as he packs his bags for the annual Davos affair at the World Economic Forum.

But before we get to all of that I’ll take the opportunity ahead of another inflation report to refresh some arguments used in client meetings about the Bank of Canada.

BANK OF CANADA COMMENT—CUT, HOLD OR HIKE?

Canada’s economy continues to track little growth with another inflation report on tap for this coming week (see CPI preview later). Using estimates for the monthly accounts, Q4 GDP growth is tracking around -1.0% q/q SAAR. This is on the income/production basis, not expenditure-based GDP which can differ in either direction depending on things like inventory swings. We’ve conservatively estimated a contraction of around -½% for now. Strike activity dented hours worked as a GDP driver in Q4 as one consideration.

If the Q4 estimate is within spitting distance of reality, then it comes on the heels of the highly distorted Q3 2.6% q/q SAAR expenditure-based GDP print. Final Domestic Demand—which excludes volatile inventory and trade effects—was weak in Q3 and is tracking softly again in Q4.

So, cut, you say? Be careful on many counts. Here is a set of points to consider.

- you don't keep easing as the softness you at least partly thought would happen becomes reality.

- There are 12–24 mth lagging effects of rate movements that need to be given time to work. We're about 18 months into the period after the first cuts in the summer of 2024, it's still early for the last ones before they paused last March, and the effects of the added 50bps of cuts last September and October are still in their infancy.

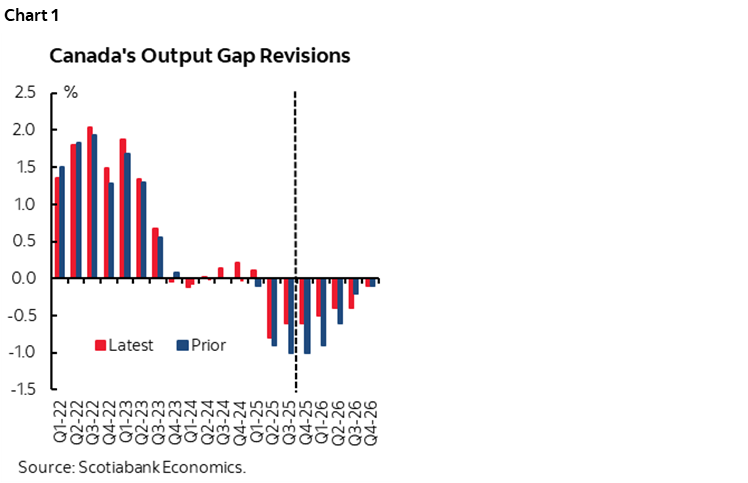

- GDP revisions going back years revised down the estimated amount of slack even after considering the net effects on potential through the GDP details (chart 1). We probably had net slack somewhere around -0.5 to -0.75% last Fall, down from prior estimates. As actual GDP growth is underperforming, the supply side is restrained by no population or labour force growth, underinvestment, and weak productivity.

- About 190k jobs were created over the past four months, and you wanna cut do you?

- Trend inflation is still tracking a little above target on headline, with trimmed mean and weighted median around 2¾% y/y. Volatile m/m SAAR core readings have been averaging around 2¼% m/m SAAR 3 mo MA.

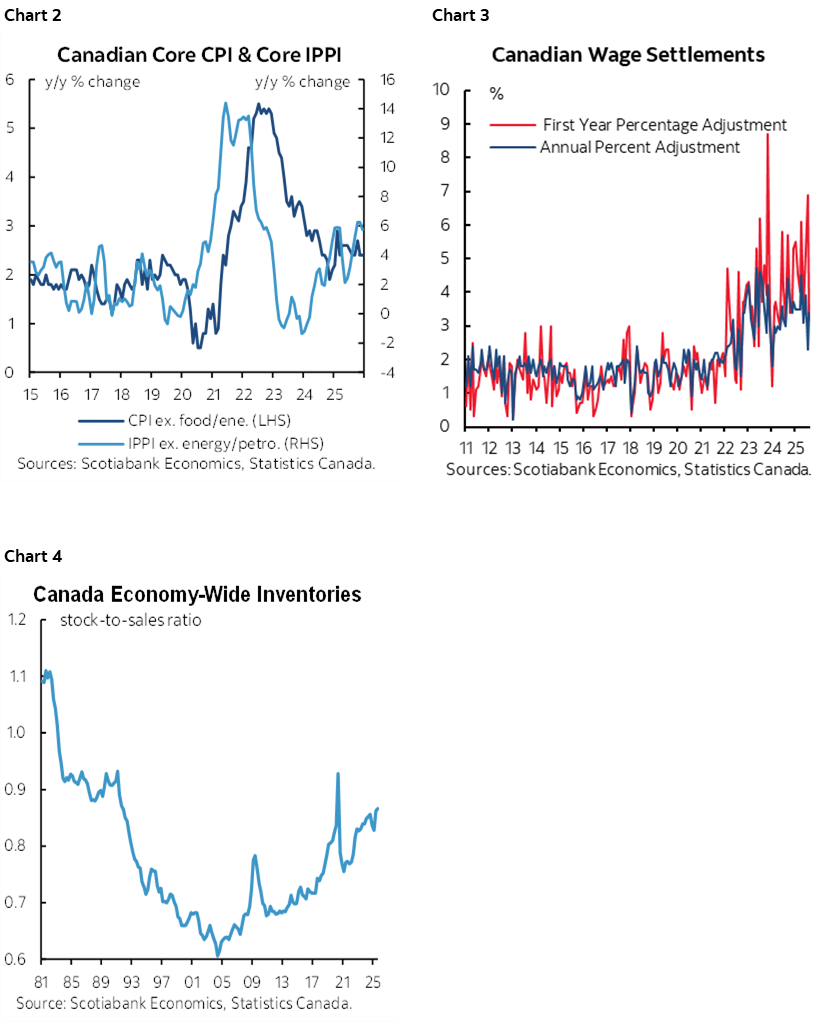

- Cost pressures point toward potentially material effects on inflation through multiple effects. The C$ has sharply depreciated over recent years which raises import prices, some of passes through to consumer prices with a lag. Producer prices are rising with some lagging pass through into inflation likely (chart 2). Wage growth remains in excess of productivity including wage settlements that govern about one-third of Canada’s workforce that is unionized (10% in the US), chart 3. Inventory buffers are high as companies pad stocks and migrate away from just-in-time deliveries given heightened border frictions to supply chains, but the costs will be passed on including to consumers (chart 4). There is little slack in the economy to mitigate these price pressures as previously noted.

- Monetary policy is passing the baton to fiscal (provies and feds).

- Financial stability considerations will be further informed in the Spring housing market. I’m more cautiously optimistic than others. Jobs are on a tear, real mortgage rates are very low, housing finance incentives have been added, there is pent-up demand that can capitalize upon softer prices in a market with relatively lean months’ supply, and Canada in my opinion has not fully absorbed prior waves of immigration in its overall housing market.

- The tariff effect is overstated. Around 90% of Canadian exports are CUSMA compliant and hence avoid tariffs. What does a floating, flexible currency do in response to a terms-of-trade shock which is what tariffs represent? Why it sinks, silly! From 1.20 in and out of the pandemic to two dimes north of that. If you're CUSMA/USMCA compliant then your export price competitiveness has improved and into a so far solid US economy that offers a strong income pull effect on Canadian exports. A 6% average effective tariff rate is a gift relative to what the Europeans and Japanese did to themselves, so Canada picks up some trade diversion too. The Canada-China agreements at the end of this past week offer medium-term upside (see separate section).

- I find the tariff debate to have parallels to the mortgage resets debate over the past 2–3 years. Lots of folks got in a flap over resets by failing to anticipate rate cuts and behavioural changes by borrowers and lenders, and by not accounting for the roughly 60% of households that don’t have a mortgage while an estimated 10–15% were among the more pressured. I'm proud that Scotiabank Economics argued against it on the sunnier side of the street, not dismissing legitimate challenges to some, but portraying it as more of a micro than a macro shock. To date, tariffs on Canada feel like the same thing.

- Could CUSMA/USMCA (I like CUSMA...) be torn up? I suppose, but it's not clear given how the mechanics and challenges would unfold. Trump's industrial/ag base is already getting increasingly agitated by the effects of his tariffs and other policies. A 16 year roll over is clearly out of the cards for CUSMA in this environment. 1-year-at-a-time reviews are possible up to 10 years at which point 2.5 administrations from here you have to decide if you're in or out. That's the middle ground, with uncertainty persisting but within the confines of an agreement that broadly stays intact. Higher tariffs are possible and I'm sure we'll hear a lot of threats yet especially whenever SCOTUS issues its IEEPA ruling.

- But there is also a path to a 'deal'. Higher N.A. content provisions could be offered. Maybe adjust or revamp the dispute panels. Maybe spend more on border security—which is already being done—and more on the flawed 'golden dome' concept. Maybe adjust dairy supports, partly depending upon the evolution of Quebec politics this year.

So with all that said, the policy rate in real terms is around zero to negative depending upon how you measure inflation (backward headline or core, forward expected and by which measure). The whole term structure out to 5s is low in real terms. Shock scenarios that crater CAD raise import price risk when cost pass through effects are already high via multiple channels.

So cut, you say. If the BoC were to do so after last Fall's insurance cuts, then Governor Macklem would risk renewed policy error. Markets are still leaning more toward up than down later this year, but in my opinion, they have backed too far away from this position. Tie all arguments back to inflation and its myriad drivers.

Still, most of our narrative is around a protracted pause with hikes up to 3% pencilled in (emphasis upon PENCIL) later down the road. More stock in the argument is placed in arguing against going toward a really negative policy rate. Emergency style easing. Throwing caution to the wind on inflation, Turkey style. The BoC is likely to set a very high bar against further easing as it would be of no use to offer just one cut, yet plumbing the negative depths of real rates would be a high risk venture.

CANADIAN INFLATION—REBOUND FROM THE CORE MELTDOWN?

Canada refreshes CPI inflation figures for December on Monday. Yes, Monday. An unusual day compared to past release dates, and when US clients with an interest in Canada are on holiday.

There may be market reactions, but it’s unlikely that the data will sway the BoC in any way ahead of the next policy decision on January 28th. See my Bank of Canada section for more on this perspective.

Headline CPI is expected to drop by -0.4% m/m in seasonally unadjusted terms which should leave the year-over-year rate unchanged at 2.2%. In seasonally adjusted terms, CPI would translate to about +0.2% m/m.

Here are some drivers of the estimate:

- in terms of the year-over-year rate, the year-ago comp will shift lower than it was in November which would raise the y/y rate from 2.2% to 2.6% before considering other points.

- December is a seasonal down month for overall prices in Canada. This could account for 0.1–0.2% m/m of the estimated 0.4% m/m CPI drop.

- gas prices fell more than seasonally normal. They were down by enough to shave probably 0.2–0.3 ppts off of CPI.

- there were unusually large price adjustments in several categories the prior month that on net may revert lower in the implied estimations. Categories like communications and tuition and rent were examples.

- Seasonal adjustment factors have tended to be middle of the pack in recent years when comparing like months of December over time. The absence of any outlier SA factor adjust is expected to continue.

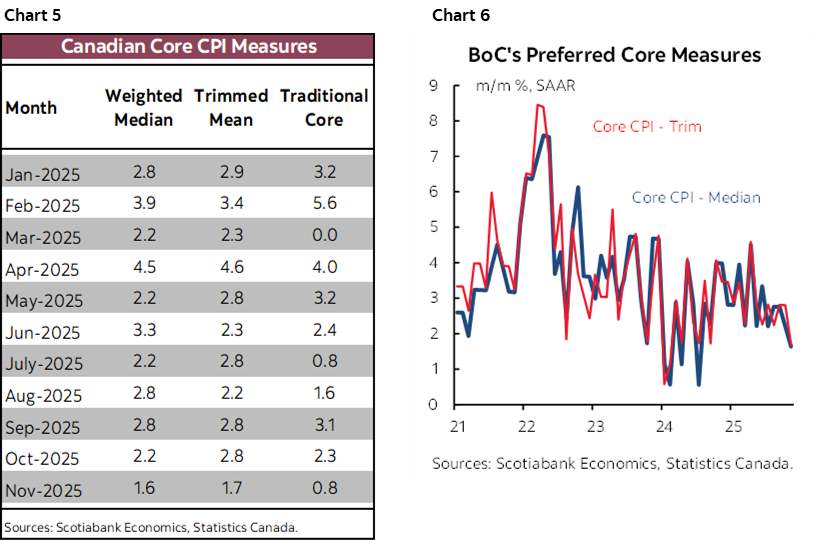

Key will be the core measures of inflation. As charts 5–6 show, they trailed off rather sharply in November with weighted median and trimmed mean CPI rising by about 1¾% m/m SAAR and traditional core CPI ex-food and energy at 0.8%. These abrupt slow downs were unusual compared to the trend and may be vulnerable to a spike higher this time.

Producer prices will follow up CPI when they get updated on Wednesday for the same month of December. Recall the prior chart showing that soaring producer prices tend to presage upward pressure on CPI inflation.

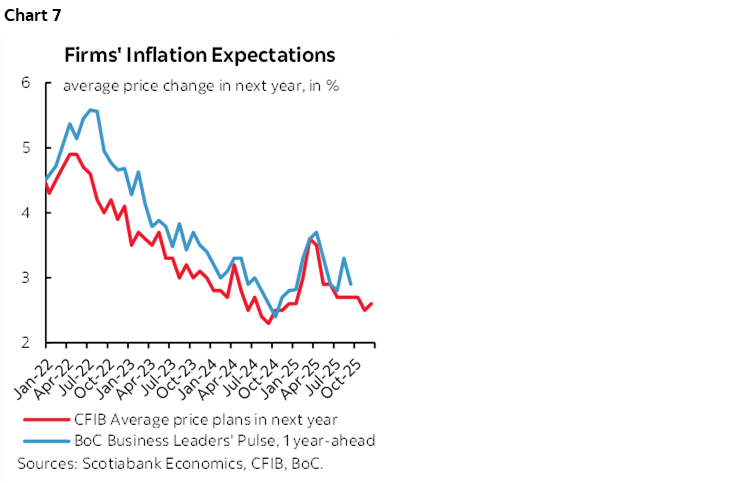

The Bank of Canada’s quarterly consumer and business surveys will also inform measures of inflation expectations. The surveys greatly lag behind, however, so they tend to be treated as stale on delivery. The Business Outlook Survey was likely sampled over the month of November but a fresher leading indicator suggests its measure of inflation expectations may decline again (chart 7). The Business Leaders’ Pulse survey is conducted online and spans the October to December period. The consumer survey is also sampled over the first few weeks of November with limited follow-up calls into early December.

CANADA LIKELY TO BENEFIT FROM CHINA DEAL

Initial impressions about the Canada-China announcements were offered here, but I’ll follow up with a few other points.

One concern is whether allowing Chinese e-vehicles into Canada would negate the other advantages of the trade arrangements. That’s unlikely because of the modest volumes, the differences in the products, and the relative weights of the various sectors in the Canadian economy. I’ll unbundle each of those points.

Canada produces 1.4 million vehicles annually. It buys 1.9 million vehicles. China’s e-vehicle import quota of 49k to start and maybe 70k in future starts off at 2½% – 3½% of these measures and rises to 3½% to 5% several years from now. Canada saw this level of Chinese e-vehicle imports before in 2023 and it didn’t kill off the auto industry.

And it won’t. Over 90% of Canadian assembled vehicle production heads to the US. The overwhelming majority of it is CUSMA/USMCA compliant. The US has barriers against Chinese e-vehicle imports. Canada’s auto production is not vulnerable to Chinese e-vehicle imports.

Why might it not beyond the limited volumes? Half of these cars are to be priced under C$35k (US$25k). Perhaps the chassis, wheels, roof, axle and doors are options. If the battery alone is at least $5–10k and assuming a budget battery doesn’t burn your house down, then there isn’t much left for the rest of the car. As for the other half, we’re talking numbers that would represent around 2–3% of Canadian sales and production. There may not be much product overlap with what’s built in Canada. A dealer network is largely absent in Canada. Brand recognition is limited if not entirely non-existent for the companies like BYD, Chery, Li Auto, NIO and XPeng.

On Canadian sensitivities to US-relations and responses, note that President Trump shared encouraging support for the announced deal between Canada and China. Further, the US has a choice. They have chosen to discourage e-vehicles as the Trump administration emphasizes gas combustion engines that are likely to continue to dwindle as a share of global auto production.

Trade negotiations also involve trade-offs by their very nature. The entire auto industry in Canada including production of assembled vehicles, parts and auto wholesalers equals about 1½% of GDP. Crop production is the same, so don’t scoff at opening up opportunity there. Energy is 7½% of GDP of which oil and gas extraction including pipelines is 4% (chart 8).

There are multiplier effects on each of these sectors once the exposures of capitals goods makers, finance companies and others are added. Those multiplier effects also need to consider the subsidies and other supports that the industries enjoy on a relative basis, and their commitment to honouring the agreements they sign in exchange for such supports.

Many of these affected sectors are in Ontario that stands to benefit from stronger performances in sectors like energy and agriculture and may pick up Chinese investment in its own auto sector.

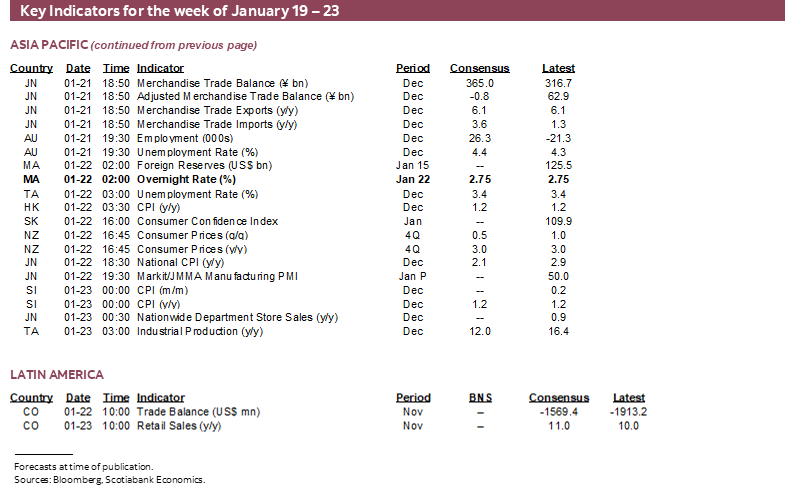

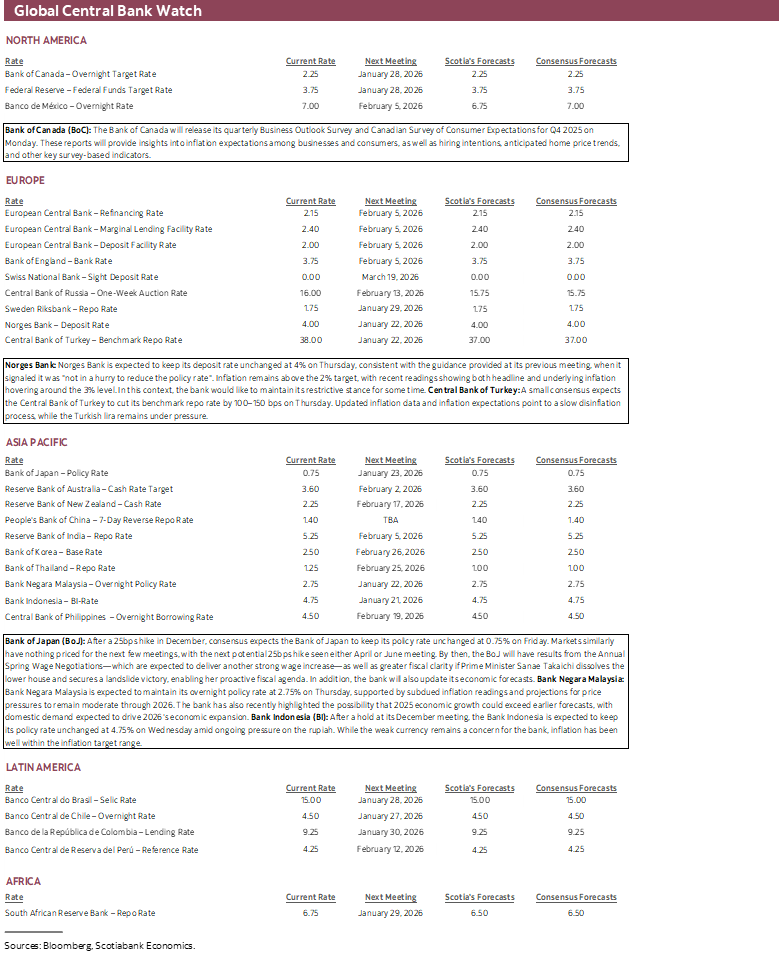

GLOBAL CENTRAL BANKS—POLITICS TO CONSTRAIN THE BOJ

Five central banks will weigh in with decisions this week. One of them may matter to global markets. Most are expected to be on hold with only one easing policy. See the central bank table for more on some of them.

Each of Bank Indonesia (Wednesday), Bank Negara Malaysia (Thursday) and Norges Bank (Thursday) are expected to remain on hold. Turkey’s central bank is expected to cut again (Thursday).

The one that may matter is the Bank of Japan. It hiked in December and tends to act in measured, gradual ways such that no one expects a policy rate change at this meeting. Guidance may matter more. The BoJ issues new forecasts this time and when coupled with Governor Ueda’s comments they might inform the path forward with markets pricing the next hike by Summer.

There’s just one problem. Prime Minister Takaichi is widely expected to dissolve the lower house and call a snap election for as soon as February 8th or 15th. Her aim is the build on the momentum since becoming PM in October to try to secure a single-party majority for the Labour Democratic Party. A disciple of the late former PM Shinzo Abe, Takaichi promotes aggressive fiscal stimulus which puts upward pressure on yields given Japan’s heavy indebtedness.

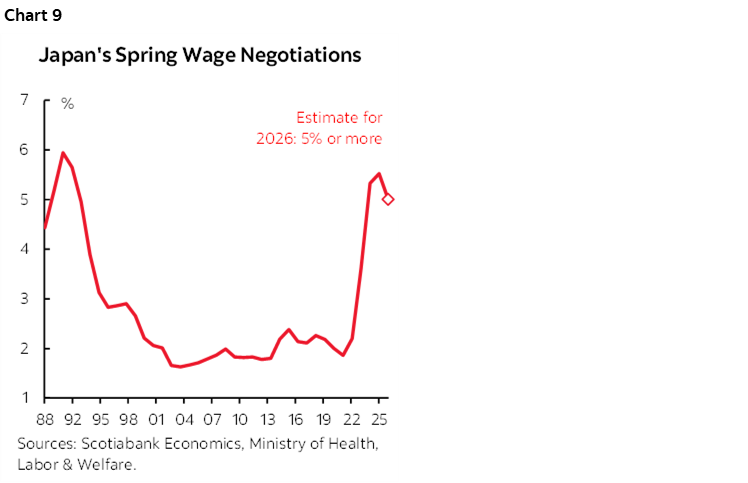

The Bank of Japan will stay out of the politics for now, but mindful toward other developments like a weakening yen and associated pass through to inflation and the upcoming round of Shunto spring wage negotiations that look to extend the pattern of strong gains for less than 20% of Japanese workers (chart 9).

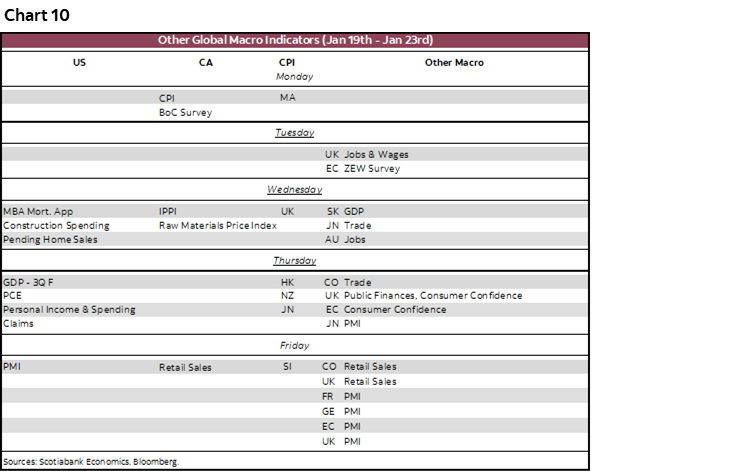

GLOBAL MACRO—NEW YEAR NORMALCY RETURNS

Global indicator releases pick up this week as distance from the holiday period grows (chart 10). Key will be a round of purchasing managers’ indices for January, several US macro readings, Canadian retail sales covering the whole holiday period, and job market figures for the UK and Australia.

PMIs Aplenty

Australia and Japan will kick off the round of PMIs on Thursday evening with the Eurozone, UK, US and India releasing into Friday morning. A reading above 50 signals growth and most of the regions have been hovering just above that with India’s more rapid growth an exception.

Canadian Holiday Shopping

Canada also updates retail sales for the last two months of 2025 and hence enveloping the holiday period. Statcan previously guided that November sales jumped higher by over 1% m/m SA in nominal terms. The first estimate of sales in December might get a lift from higher auto sales based on Desrosiers estimates.

US Catch-Up Continues

A wave of US macro reports will continue to catch up from the shutdown’s interruptions. Key ones may be difficult to read.

For instance, the Fed’s preferred inflation reading will be updated with October and November estimates on Thursday. Because data wasn’t collected in October, they have guided that the October estimate will be an average of the September and November price levels by applying linear interpolation. This means that the m/m rates for both individual months are unlikely to be meaningful. At best, we’ll be able to figure out the average m/m SA change in core prices in both months.

Other US releases will include:

- Spending and incomes (December): Spending is likely to benefit from the solid 0.4% rise in the key retail sales control group onto which higher services spending is added. Income growth is expected to be buoyant at 0.4% m/m. The net effect could mean little change to the saving rate of 4%.

- Q3 GDP revision (Thursday): The initial estimate of 4.3% q/q SAAR was well above consensus but widely viewed as suffering from questionable data quality. Most estimates expect no material revision, which is not the same as saying there is no scope for surprise. There often is even when data quality isn’t suspect.

- Q3 core PCE revision (Thursday): We can’t tell the direction of revision risk given that the initial estimate was based on known Q3 PCE data at the time and we don’t have October-onward data which would include monthly revisions. It’s possible that producer price figures that were revised higher for September could add some upside.

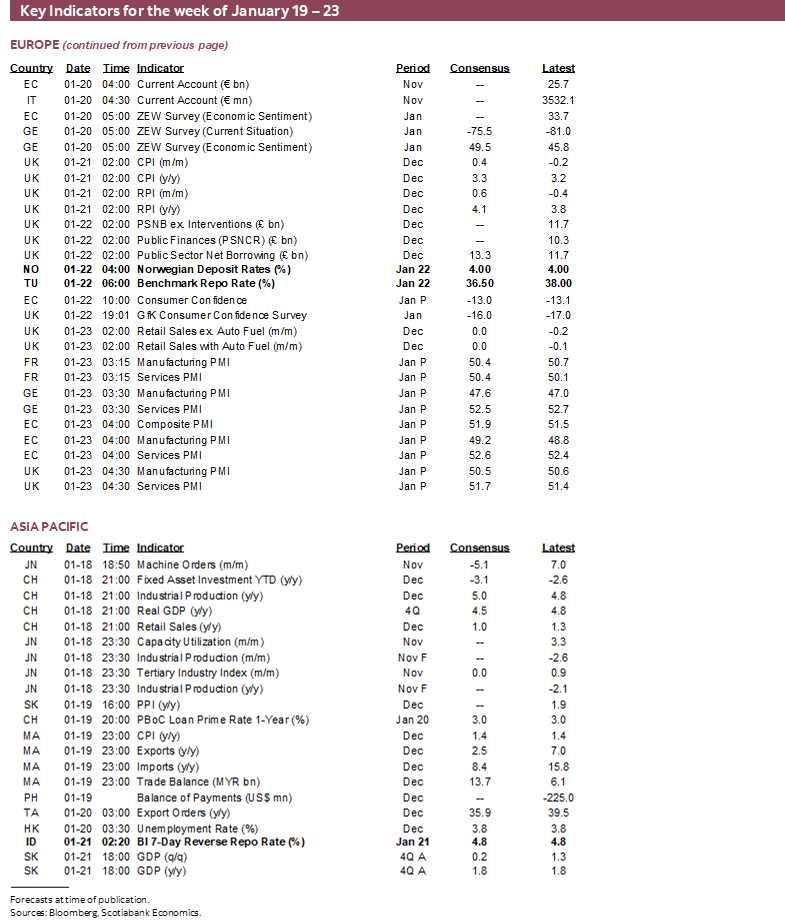

UK Jobs, CPI, and Holiday Spending

The UK job market’s performance is poised for an update on Tuesday following this past week’s strong GDP and other data. Payrolls in December and total employment in November will combine with updated figures for jobless claims during December and November’s wage growth. Wages have been running fairly hot at just beneath 5% y/y. The unemployment rate of 5% has been close to estimates of its equilibrium rate.

The UK also updates CPI (Wednesday) and producer prices (Wednesday) and retail sales (Friday). Core inflation is expected to remain near 3 ¼% y/y with retail sales holding unchanged to end the year.

Jobs Down Under

Australia updates job market readings for December (Wednesday). November was a set back (-21k) with full-time jobs taking a hit (-57k) along an otherwise solid trend. Most expect a rebound this time.

Other global readings will include CPI figures from Japan (Thursday) and New Zealand for Q4 (Thursday), South Korean GDP (Wednesday), and economic activity readings for November from Mexico (Friday) and Colombia (Friday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.