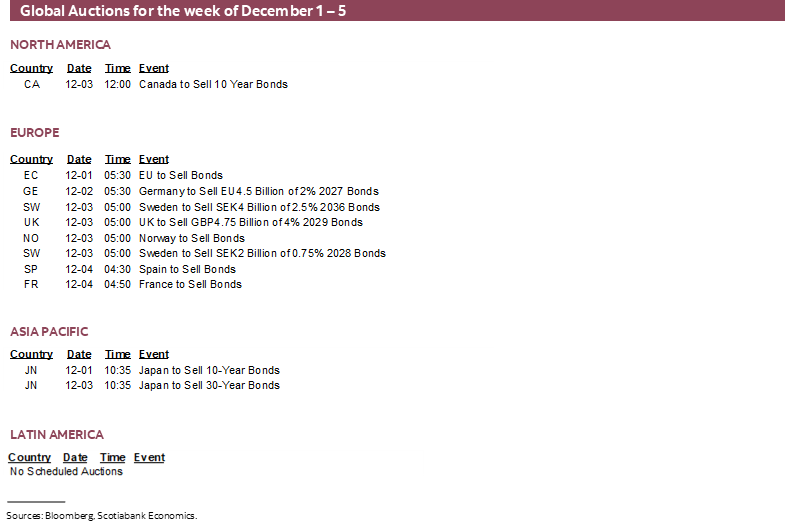

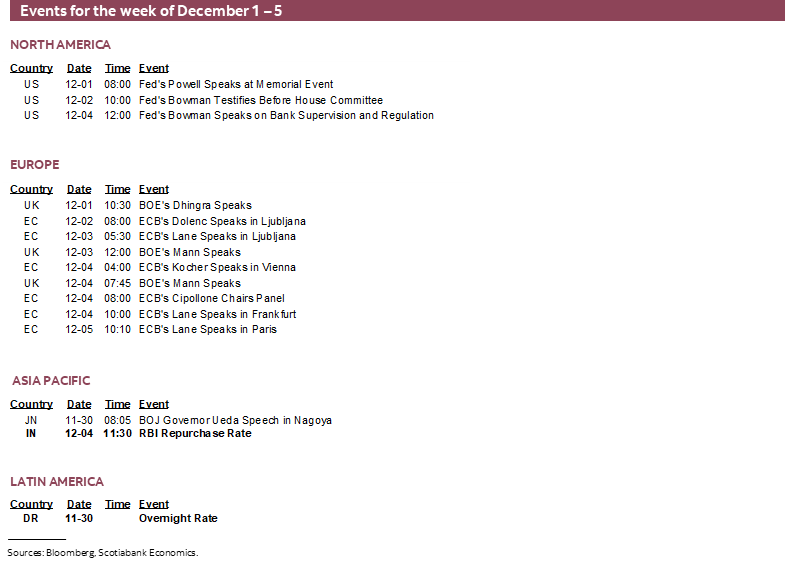

Next Week's Risk Dashboard

- Comment on CAD stablecoin

- Canadian jobs update won’t matter to the BoC

- Canadian banks wrap up FY25 earnings…

- …in a strong year for shareholder returns

- Holiday shopping results usually beat, discounts are similar

- USTR’s USMCA hearings kick off

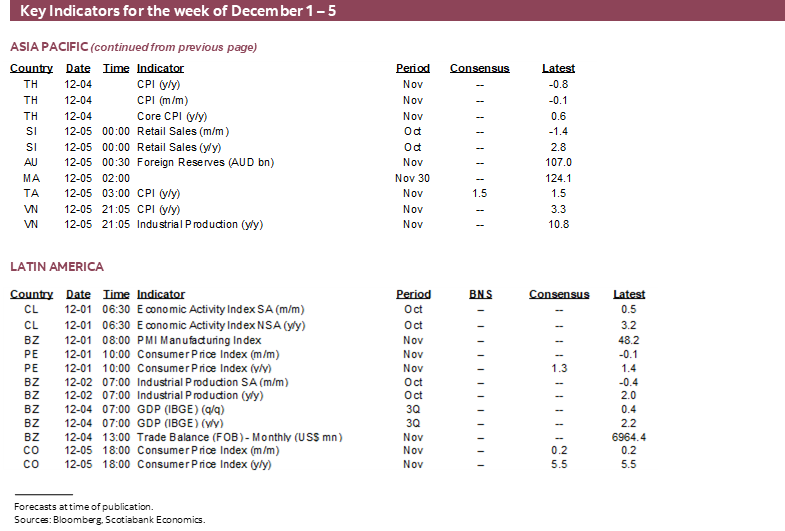

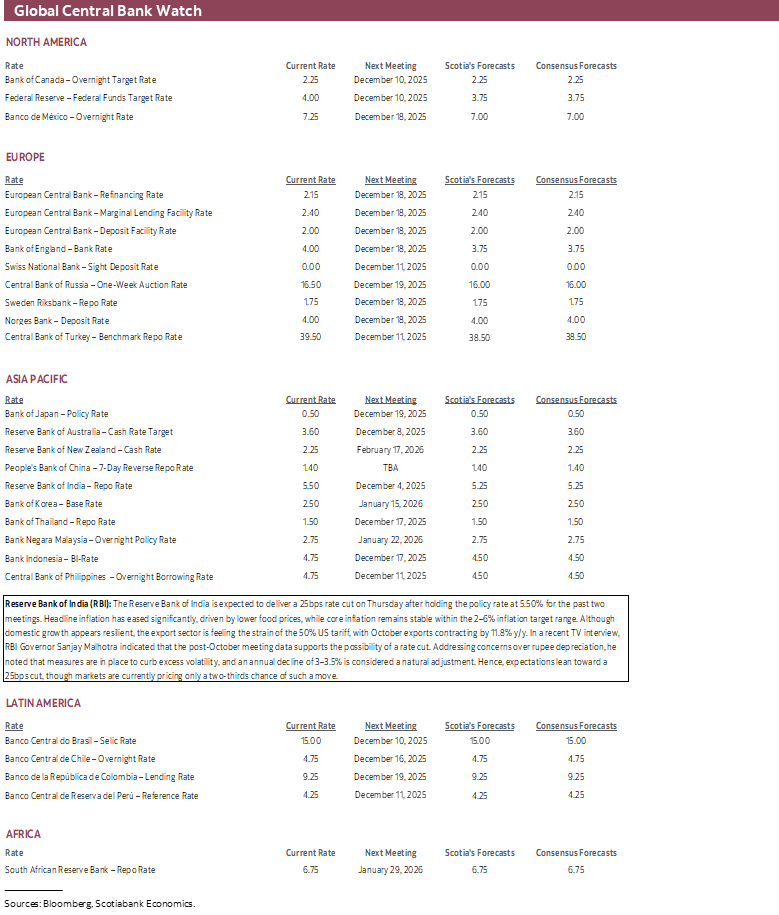

- RBI might ease this week

- Global macro readings

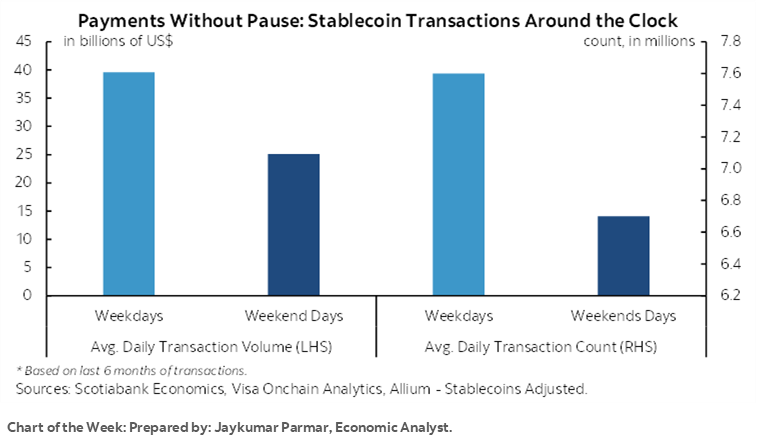

Chart of the Week

This coming one may as well be labelled Canada Week. There will be some other things going on, but the global calendar is looking pretty light.

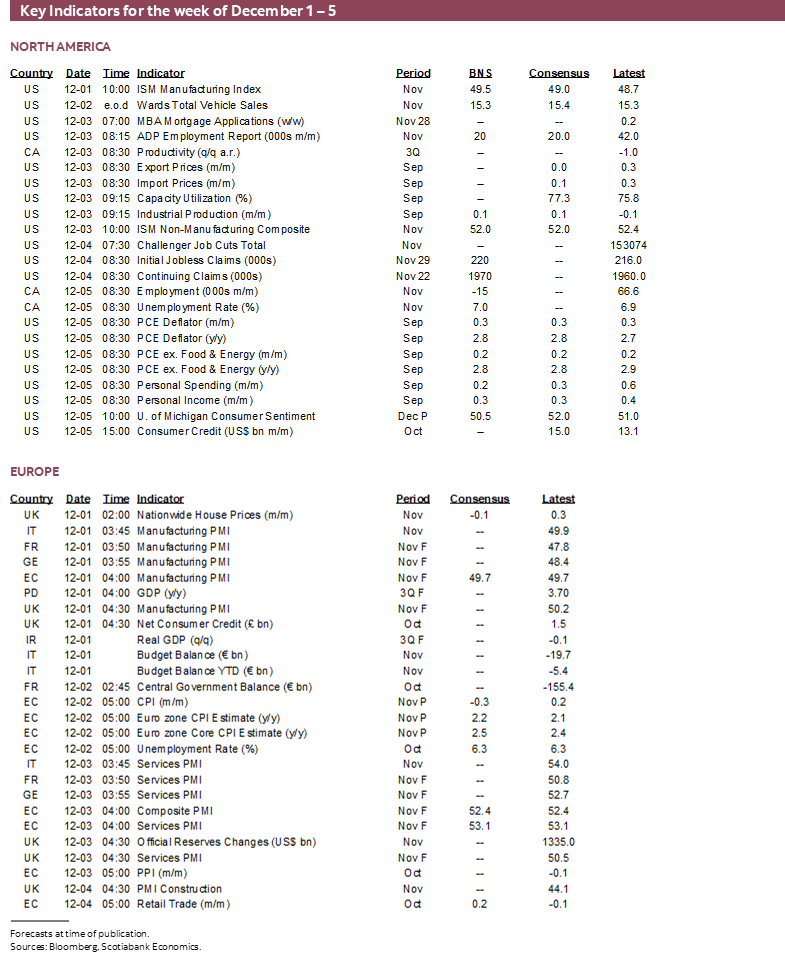

The US will continue to catch up on releases delayed by the record-long government shutdown by the Trump administration, but key releases like GDP, inflation and nonfarm will have to wait longer yet—until after the December 9th–10th FOMC meeting. Also watch for indications of the strength of the US holiday shopping season as Americans return and probably sick of turkey leftovers notwithstanding the 40% rise in turkey prices within CPI since 2019! There will be an active calendar elsewhere but there are no major releases that would affect global markets. Only one central bank (the RBI) will make a decision.

As for Canada, it’s becoming an exciting place to watch. With each passing week, month and quarter, the federal government’s energetic policy framework is becoming less distributive, more growth-oriented with the players changing accordingly. Inreasingly out the window is the self-defeating guilt of having a large factor endowment of natural resources the world wants. It’s about time and it shouldn’t matter what dear reader’s political stripe may be in welcoming such a pivot.

This week brings more action. Banks wrap up the fiscal year with Q4 and full-year earnings that may validate a rather lucrative year for shareholders. Friday’s jobs report will seek to extend the explosive job growth of the prior two months.

CUSMA/USMCA hearings are also approaching. These are the US Trade Representative’s delayed hearings that were to have been conducted in November. They will be conducted from Wednesday through Friday starting at 9amET each day. Friday brings the deadline for submissions and then additional committee hearings occur the following week (here). Rebuttals can be submitted the following week. The USMCA Environment Committee Meeting with reps from each government occurs on December 11th and will be immediately followed by a virtual public session.

No decisions or key guidance are expected out of these hearings that, if anything, are likely to make clear that the agreement has broad support among businesses. What happens afterward remains up in the air. Will PM Carney visit Washington soon as suggested? How will SCOTUS rule on IEEPA tariffs and exactly when? What outcome will arrive when the formal review hits next July?

Personally, I remain cautiously optimistic. Canada has been securing the lowest effective tariff rate of all of America’s major trading partners. The intertwined nature of supply chains in the two countries is likely what should be credited.

Also in the spirit of Canada week, I’ll kick it off with a special topic. Canada is quickly moving toward meaningful regulatory changes governing the financial sector. One example is stablecoin legislation. There is opportunity here. There are also risks aplenty. What follows expresses concern that we’re getting a tad carried away with some of the theories concerning the bounty to be had from adopting Canadian stablecoin.

CANADIAN STABLECOIN COMMENT

As Canada finally considers the path forward for stablecoin legislation, a key issue is whether other market participants should anticipate broader Canadian financial market repercussions. Colour me skeptical with thanks to Jay Parmar for research assistance. Pursuing CAD stablecoin legislation should be driven more by the desire to foster payments innovation and concomitant efficiency benefits and less by any other motives.

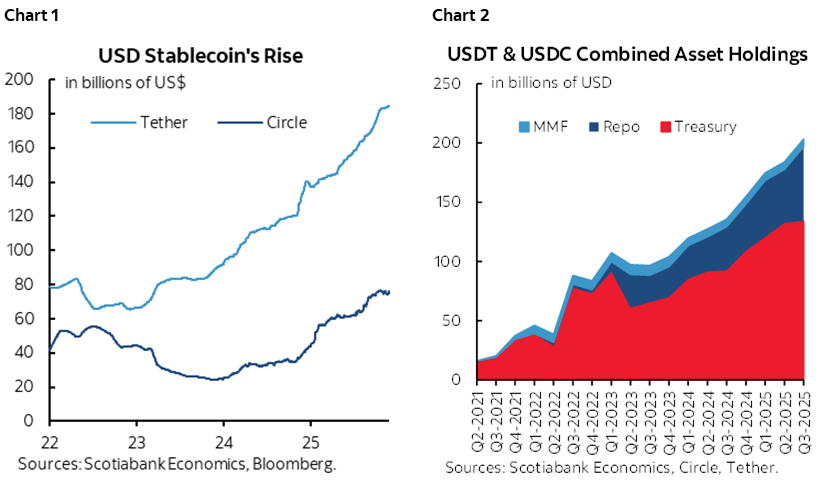

Stablecoin’s Rise

Stablecoin—cybercurrency tokens backed by relatively stable fiat money like the USD on a pegged 1–for–1 basis—has taken off in the United States. Several issuers are in the market but the biggest is Tether—incorporated in El Salvador—that has seen its market capitalization soar to about US$185B now (chart 1). Tokens issued on the liability side are invested in the asset side primarily in short duration fixed income assets like US T-bills and short-term maturity Treasuries alongside increasingly important other investments in assets like repurchase agreements and money market mutual funds (chart 2). Bitcoin is a rising share of investments as well and currently sits at just under 6% of reserves. So is gold.

It is this investment focus in select asset markets and possible spillover effects that attract some interest when paired to the benefits of stablecoins. The latter benefits include speed, transparency, low cost, round the clock availability, and the perception that it offers a way around regimes marked by high inflation and more unstable currencies.

Rating Agency Warnings

Ratings agencies are upping the ante in terms of warning about the risks. S&P very recently lowered the odds on the ability of Tether to maintain its 1–for–1 peg to the USD to the lowest number on a one to five scale (here). Part of the concern is the rising focus upon other investments that may include rising counterparty risk as well as gaps in disclosure. Circle’s peg is viewed as much more stable because its investments remain focused in liquidity Treasury securities.

Needless to say, any inability to defend the peg to the dollar would strike to the very heart of the stablecoin business model in the cyber world’s version of a bad Jenga outcome. A run could result with ripple effects across cybercurrencies in general and other asset markets. A run could spark redemptions of stablecoin holdings including Treasuries and a liquidity crisis. Stablecoin’s lack of access to the Fed’s discount window—which should likely stay that way—limits its ability to tap into supports barring the creation of a new facility. This site has some interesting features on stablecoin pegs and different regulatory regimes. This BoC piece offers an overview of the stability risks potentially emanating from stablecoin and the example of the run on TerraUSD in 2022.

This isn’t the stuff of the ERM or the trade that ‘broke’ the Bank of England or other famous currency imbalances and broken pegs like the Thai baht’s collapse into the Asian financial crisis as stablecoin’s potential challenges are more concentrated in a modest part of the financial system.

So far, that is. Longer run blue-sky projections commonly foresee thirteen-figure Treasury portfolios at stablecoins by the end of the decade which would raise their share of the Treasury market from being de minimis now toward being rather substantial.

Policymakers—like US Treasury Secretary Bessent—argue that stablecoin supports the dollar’s status as the preeminent reserve currency. Stablecoin’s rise and peg to the USD create complementary support for the dollar. Of course, policies that undermine that reserve currency status over time—like unsustainable fiscal policies—could backfire on stablecoin as well. So could brewing imbalances in stablecoin finances.

Growth Through Payments Innovation

There is nevertheless enormous potential for stablecoin to rise within payments systems by taking a rising share of the booming market for cross-border payments. No doubt there are efficiencies for payments intermediaries, exporters and importers and a broad variety of cross-border investors. Lower liquidity premia are one channel through which their rise could benefit multiple markets. So is 24–7 management. A pegged exchange rate to fiat money provides some certainty as long as the issuer of the tokens is stable.

But can stablecoin offer untold fortunes to investors in other asset classes should Canada enact supporting legislation for CAD stablecoin?

The Canadian Stablecoin Investment Thesis

A popular thesis in Canada is that given the nod provided by the recent Federal Budget, eventually enacting legislation here by improving upon the best aspects of the US Genuis Act could spark gains in Canadian asset classes such as government bonds in a way that could further widen the negative rate spread to the US. Canada could have advantages like more centralized regulation under the BoC rather than the plethora of US financial regulators alongside the requirement that reserves would have to be held at a financial institution.

In addition to the prior points, here are some reasons to be skeptical:

- Canadian stablecoin legislation doesn’t necessarily mean CAD stablecoin would take off. You want stable fiat money backing in order to combine the best of cybercurrencies with the best of fiat money. A strong reserve currency offers this benefit. Canada’s approach to seek higher reserves in a separate trust with greater oversight than in the US could lend credibility although there remains much uncertainty over how legislation may take shape at this early stage. Here is a good, brief summary of key parts of the proposed Stablecoin Act ((“Bill C-15”).

- Offshore holdings of Canadian dollars as a share of total Canadian dollars in circulation are very tiny in relation to the large foreign holdings of USD. This limits the appeal of CAD denominated stablecoin.

- It’s doubtful that the nation’s overall savings would rise as opposed to changes—big or small—in the way households and businesses save and transact including through stablecoin issuers. In essence, stablecoin’s rise could displace other investors. As one illustration, the US personal saving rate has been little changed during stablecoin’s rise while the nation’s savings have deteriorated through a rising current account deficit and sustained large fiscal deficits as corporate profits have risen. It may therefore be unlikely to see stablecoin drive a significant net inflow of added savings into Canadian markets overall. The rise of a new class of intermediary need not expand the overall market on its own within the context of the likely further growth in overall financial intermediation. A vulnerability could be saving through bank current accounts, personal chequing accounts and personal savings deposits with less risk to term deposits. Using other vehicles for cross-border payments would be the most vulnerable.

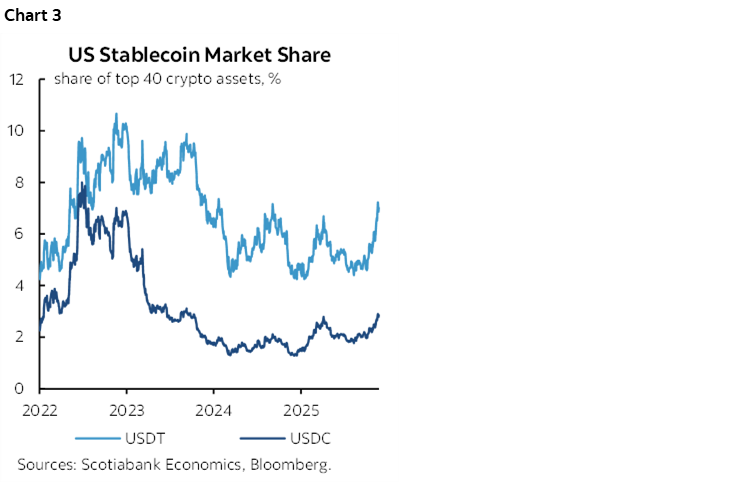

- Further, while recently gaining market share as traditional cybercurrencies fell, over time stablecoin is merely growing roughly in lock step to the overall cybercurrency market despite the benefits of stablecoin over cybercurrencies not backed by fiat money (chart 3). That suggests it may be sought more as just another cybercurrency and less for its advantages over other cybercurrencies.

- The matched maturity bias of stablecoin issuers investing in short-dated government securities puts them in the domain of central banks where they rule the roost. If central banks are uncomfortable with where short-term rates are trading relative to monetary policy goals, then they have a large and sophisticated toolkit of options for bringing markets back into alignment with their guidance on the policy rate. Overnight repo, term repo, cash bills management, receiver general auctions, adjusting borrowing terms at the BoC’s window or establishing new facilities are all among the various tools the BoC can apply to ensure proper transmission of monetary policy in relation to the central bank’s goals. Fear over the potential impact that USD stablecoin could have on independent monetary policy in Canada may therefore be exaggerated.

- If the Canadian front-end were distorted by stablecoin issuers, then governments could be tempted to shorten up the debt management strategies by issuing more in t-bills and shorter-dated bonds. More demand that lifts prices and depresses yields and more supply that depresses prices and raises yields could cancel each other in terms of yield curve effects. This could result in undesirable effects such as shortening the weighted average maturity of government debt while increasing and compressing refi risk.

- Liquidity is of paramount importance to flighty investors in short-dated liabilities and assets. Nothing beats the liquidity of the USD and US Treasuries especially when transacting across a broad variety of markets.

This is only intended as a short note injecting caution into some of the enthusiasm over stablecoin. It’s not intended to address myriad other opportunities and risks of which there may be plenty if the legislation sets a prudent framework. The only intent is to resist viewing the rise of a different form of financial intermediary as offering manna from heaven across asset classes.

Canada has been susceptible to other such investment theses in the past given the shock appeal in a more modest marketplace and economy. In the 1990s I wrote a piece that argued against the thesis that the Canada Pension Plan’s reforms would drive outperformance of the TSX. Those reforms were a success, but unaccompanied by any clear benefit to the TSX not least of which in relation to the S&P500.

CANADIAN JOBS—THE ODDS VERSUS LOGIC

Canada created 127,000 jobs over the past two months in a trade war unjustly inflicted upon it by the Trump administration. Make sense? I wouldn’t blame the doubters. We’ll see if it continues in November’s numbers at the end of the coming week.

That said, with the BoC clearly signalling it is on an extended hold and on the back of two very strong reports, the only outcome of this update may be to drive market volatility but little by way of implications for monetary policy.

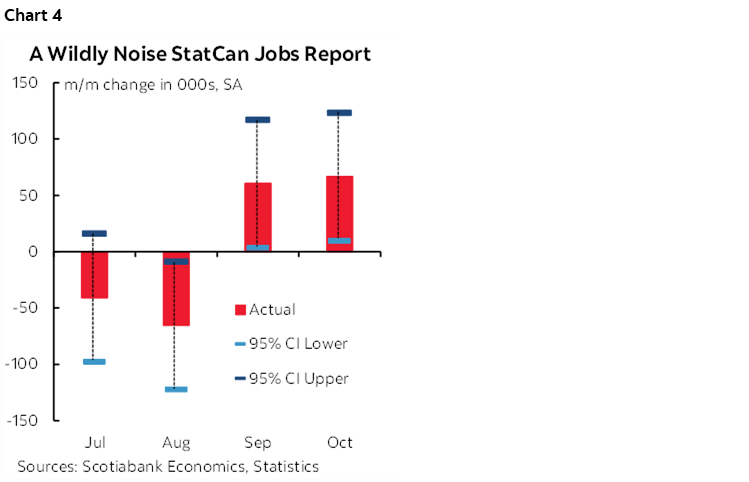

Sometimes you stand a decent chance at forecasting what the small sample used for the household Labour Force Survey spits out within a 95% confidence band of +/- 57,000. Chart 4 shows the bands around the recently estimated monthly changes in employment. More often than that you may find it more rewarding getting next season’s fishing tackle ready to hit the waters.

My guess? A dip of 15k. An unemployment rate somewhere around 7%. Here is some loose logic.

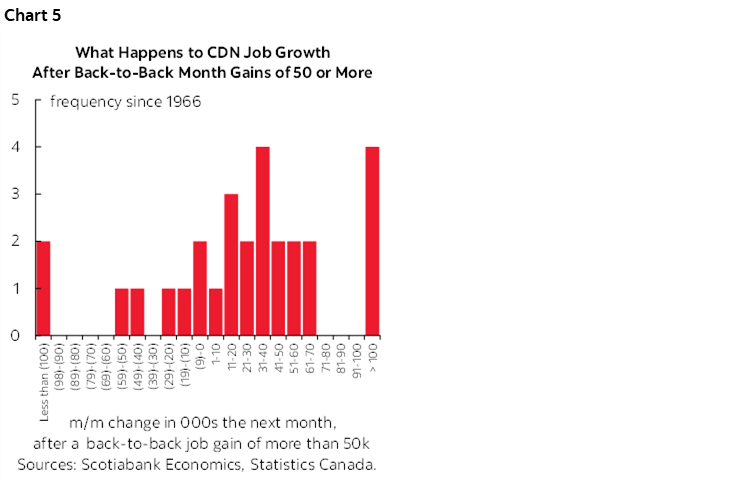

- If you’re one to play the odds by way of past experiences, then chart 5 shows what happens to the next month’s job tally after back-to-back monthly gains of at least 50k per month. The next month has been up twenty times and down eight times.

- Why does such trend persistence exist? One reason could be that the trend indicates information by way of business hiring attitudes. Another is the sampling persistence argument; the survey selects fixed panels of household respondents and rotates out one month at a time by dropping the first month in the sample and adding in the latest extension. This methodology can create some trend persistence that may or may not be representative of actual conditions.

- Then again, only one of these times (when the next month was up after two large prior monthly gains) was a month of November. That was in 2020 when hiring was soaring back over the prior months.

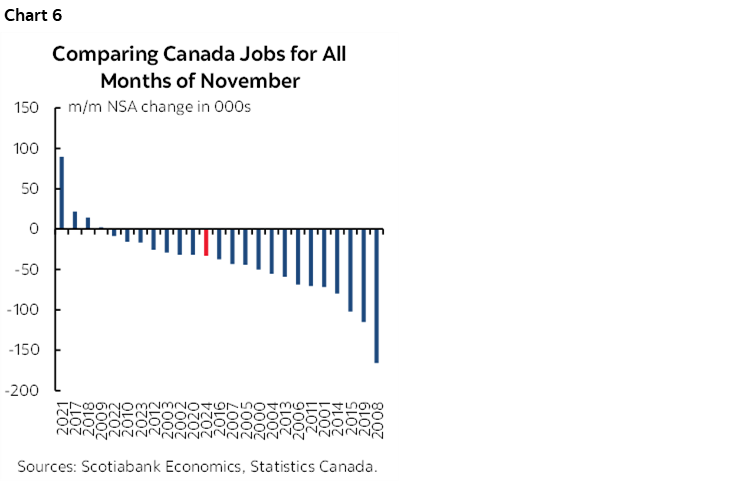

- And yet, November is normally a seasonal down month for hiring (chart 6). I’ve estimated a small decline this time.

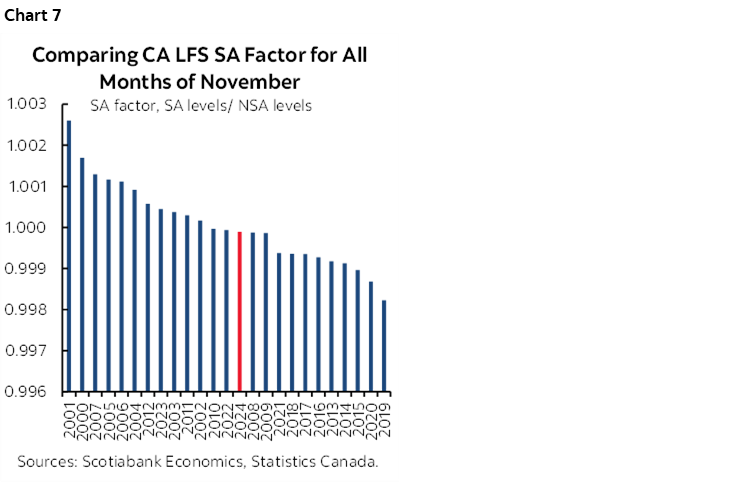

- Seasonal adjustment factors can be all over the map for November (chart 7). I don’t have strong reason to assume anything other than around 1.0.

- surveys of seasonal hiring show a pick-up in y/y terms but are still relatively softer than prior years (here).

- no, the Blue Jays didn’t prop up October’s jobs. Ergo, there isn’t a meaningful reversal of any such effect that is expected for November.

- job postings are running at about the long-run average. It’s unclear how many are truly ‘live’.

- A CFIB survey is pointing toward reductions in full-time staff over the next quarter or so among small businesses.

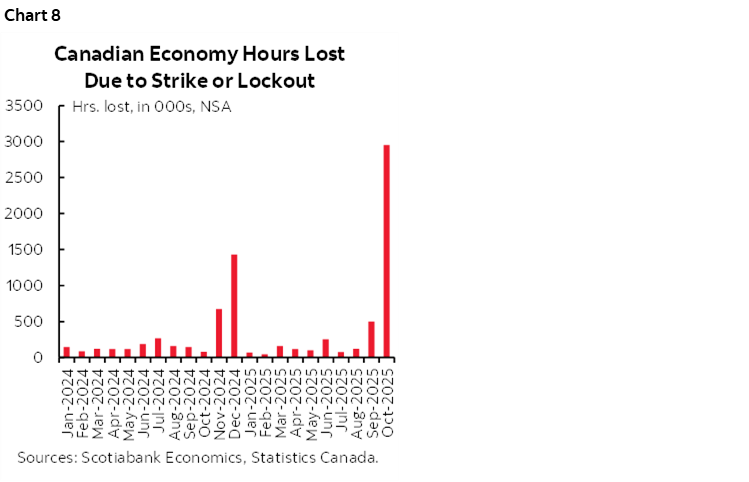

Also watch for a potential gain in hours worked as strikes ended (chart 8). There may also be a moderation if not reversal from the prior month’s wage surge.

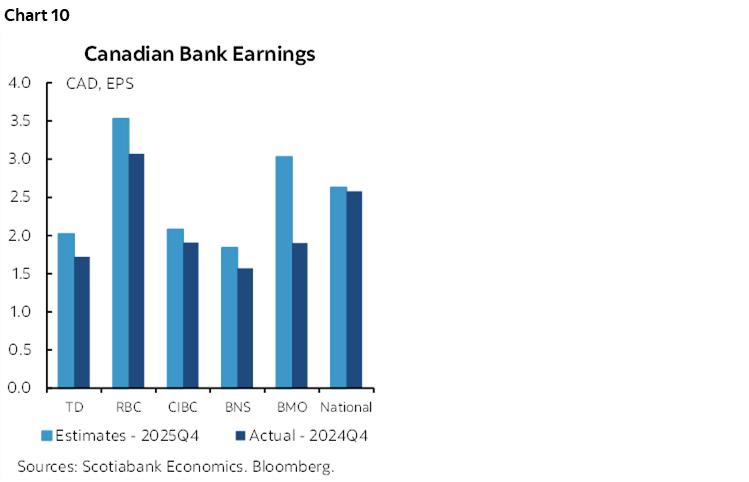

CANADIAN BANK EARNINGS—VALIDATING A STRONG YEAR FOR SHARE PRICES?

Full-year and Q4 results arrive starting on Tuesday with the banks on an October 31st fiscal year-end.

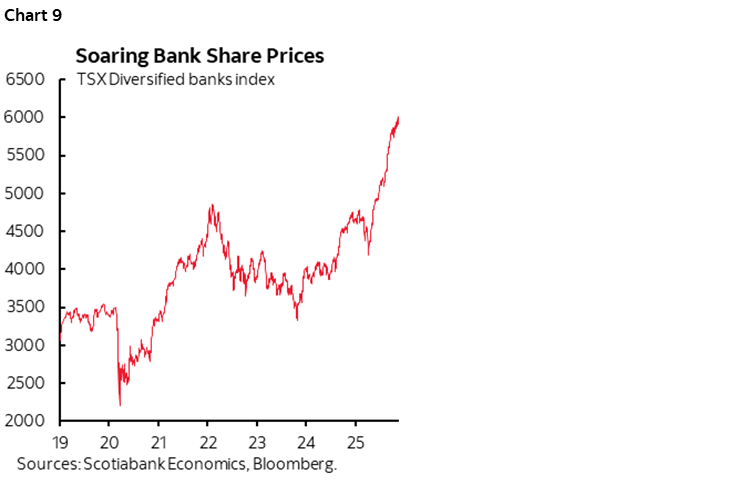

Canadian bank share prices have performed rather well this year with a gain of over 30% in the TSX diversified banks subindex (chart 9). Thank you, dear clients for the joint effort. You’re welcome, dear pensioner, dear passive TSX index holder (21% of the index), and dear active investor who spotted value coming into the year. And Happy Holidays too. The banks’ C$657 billion of collective market capitalization is up from just under $500 billion at the start of the year for an addition of over $150 billion. They are world class with a reach well beyond their immediate borders. A banking system known for its resilience, its stability, innovation, investment and good jobs—nearly 450,000 of them around the world including over 300,000 in Canada.

BNS (my employer) kicks off the parade on Tuesday. It will be followed by National and RBC (Wednesday), then BMO/CIBC/TD on Thursday and finally Laurentian Bank on Friday.

The strongest performer this year (TD) has done so as it rebounded from prior missteps before regulators. The rest of the pack saw a very tight range of common equity gains within the 21–24% range and one particularly rate sensitive and leveraged bank clocked in a touch above.

Analysts’ EPS expectations are shown in chart 10 compared to the same quarter last year since the numbers are not seasonally adjusted. Now bring on the results.

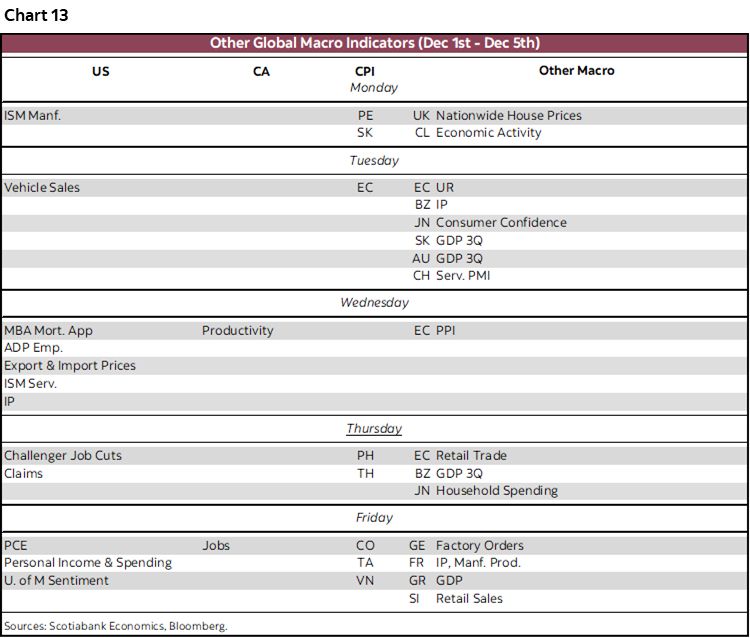

GLOBAL MACRO

Several second- and third-tier US macro reports will combine with CPI and GDP readings across a bunch of economies and one central bank decision (RBI).

More US Data

More US data releases are on tap but we’ll still have to wait a couple of weeks before major ones start to arrive like GDP, inflation and nonfarm.

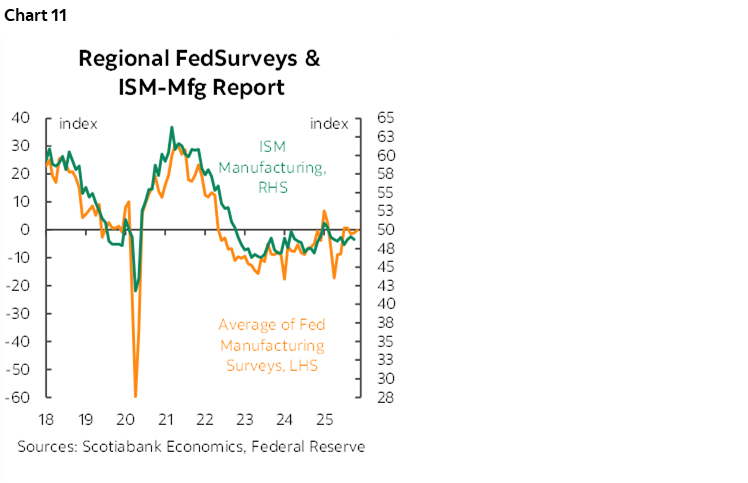

- ISM-mfrg November (Monday): Mild improvement is expected partly based on the average improvement across regional manufacturing surveys (chart 11).

- Vehicle sales November (Tuesday): Little change from the prior month’s 15.3 million annualized pace is expected according to industry guidance.

- ADP private payrolls November (Wednesday): The weekly moving average across ADP reference weeks suggests a weak tone to this reading with possible downward revision risk to the prior month.

- Import/export prices September (Wednesday): Import prices were on the rise in August as more tariffs bit and perhaps provided cover for price hikes.

- Industrial production September (Wednesday): ISM-manufacturing’s production subindex suggests little trend growth in overall factory output and September is somewhat between key seasons for utilities.

- ISM-services November (Wednesday): We’ll probably see moderate growth being signalled by a reading just above 50 again.

- Challenger layoffs November (Thursday): After they spiked in October, another less elevated reading is expected for November based on individual announcements to date and WARN data of advance layoff notices.

- Continuing jobless claims (Thursday): They remain elevated and trending up since September as a warning sign that the unemployment rate is edging higher.

- PCE inflation September (Friday): Headline is expected to be up by 0.3% m/m SA with core up 0.2%. This is based on what we know about CPI for that month and the producer price components that matter. There may be added risk from the methodological differences between CPI and PCE.

- Personal income and spending September (Friday): Income growth has been on a solid trend that is expected to continue while spending growth is likely to be tepid partly based on the weak retail sales control group measure for the same month.

- UMich consumer sentiment December (Friday): This reading is at the lowest level since mid-2022. Another decline wouldn’t surprise me.

Reserve Bank of India—Time to Strike?

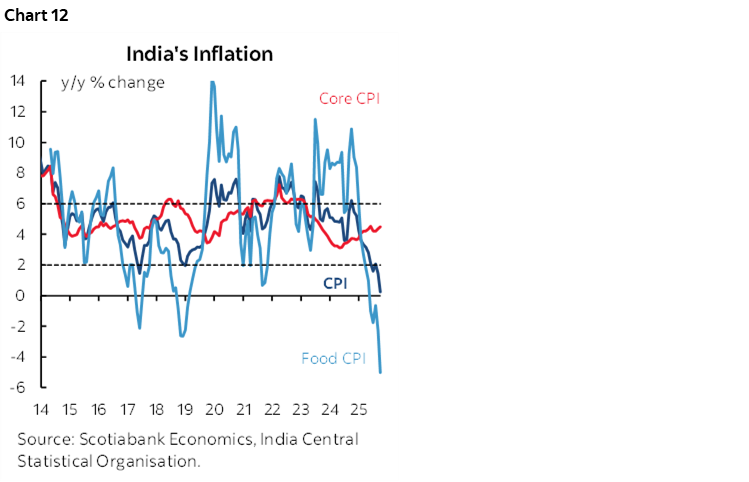

A cut by the Reserve Bank of India on Thursday is about 70% priced. Part of why it’s not fully priced is because the RBI has been in a holding pattern of late. Headline inflation has been sharply ebbing while core inflation is within the headline range (chart 12). Governor Malhotra sounds open to easing after holding to evaluate the effects of tariffs and tax cuts. He bluntly stated at the last decision on October 1st that the outlook “opened up policy space for further supporting growth.” They may still opt to wait a little longer or choose to strike now given that the rupee has been relatively well behaved since the prior decision.

Other Global Readings

Chart 13 summarizes the rest.

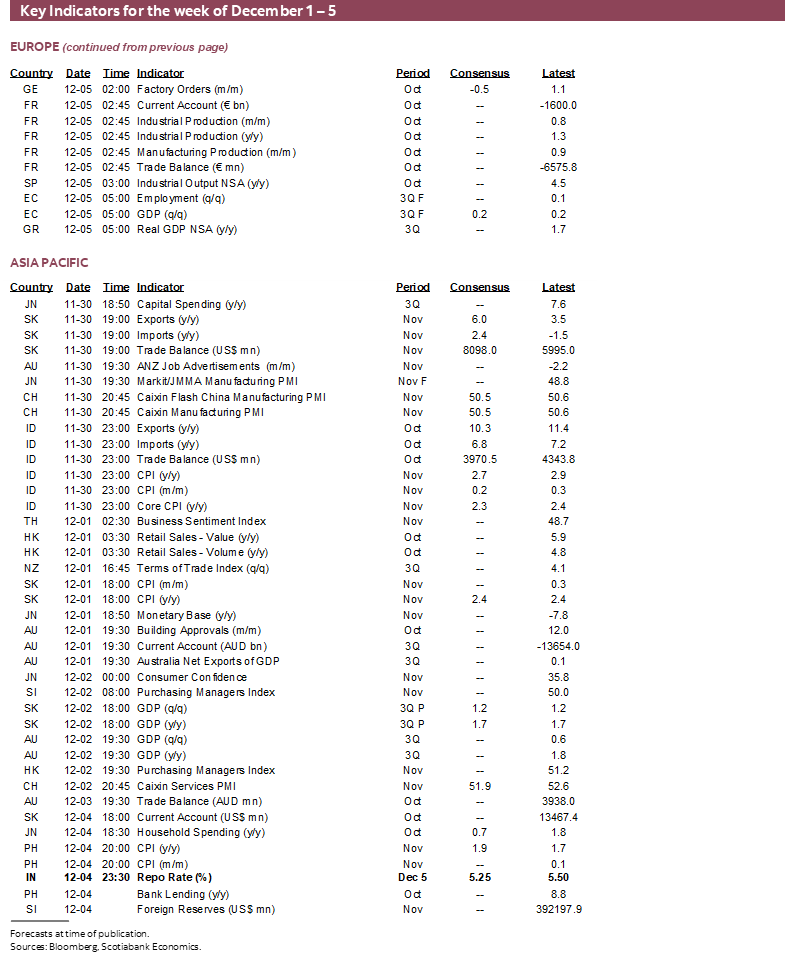

CPI inflation reports will include the Eurozone add-up that should offer little scope for surprise after the major countries released. Readings from several LatAm (Colombia, Peru, Chile) and Asia-Pacific countries (South Korea, Thailand, Philippines, Taiwan) are all due out plus readings from Sweden and Switzerland.

GDP figures are likely to showcase another solid reading for Australia (Q3 ~ ½ q/q SA, Tuesday), a pick-up in South Korea to over 1% q/q SA (Tuesday), little if any growth in Brazil (Thursday), and Chile updates its monthly GDP proxy for October (Wednesday).

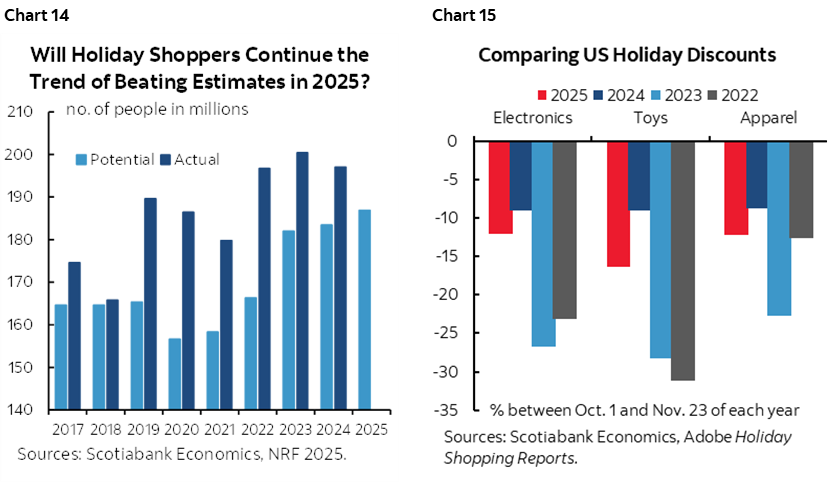

And finally watch for rolling results from the holiday shopping season in the US and Canada. Credit card companies are among the earliest to offer assessments along with measures of online sales. The National Retail Federation’s forecasts are usually too conservative (chart 14). What may help this year is evidence that discounting over the prolonged sales season is no worse and maybe better than in prior years (chart 15).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.