Policy stayed on hold as expected

Dissenters returned

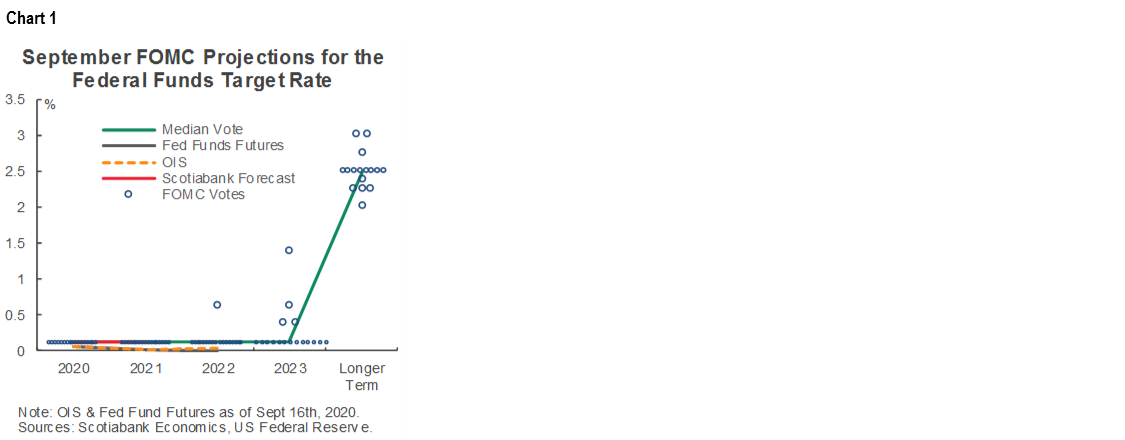

About one-quarter of FOMC members expect a first hike in 2023

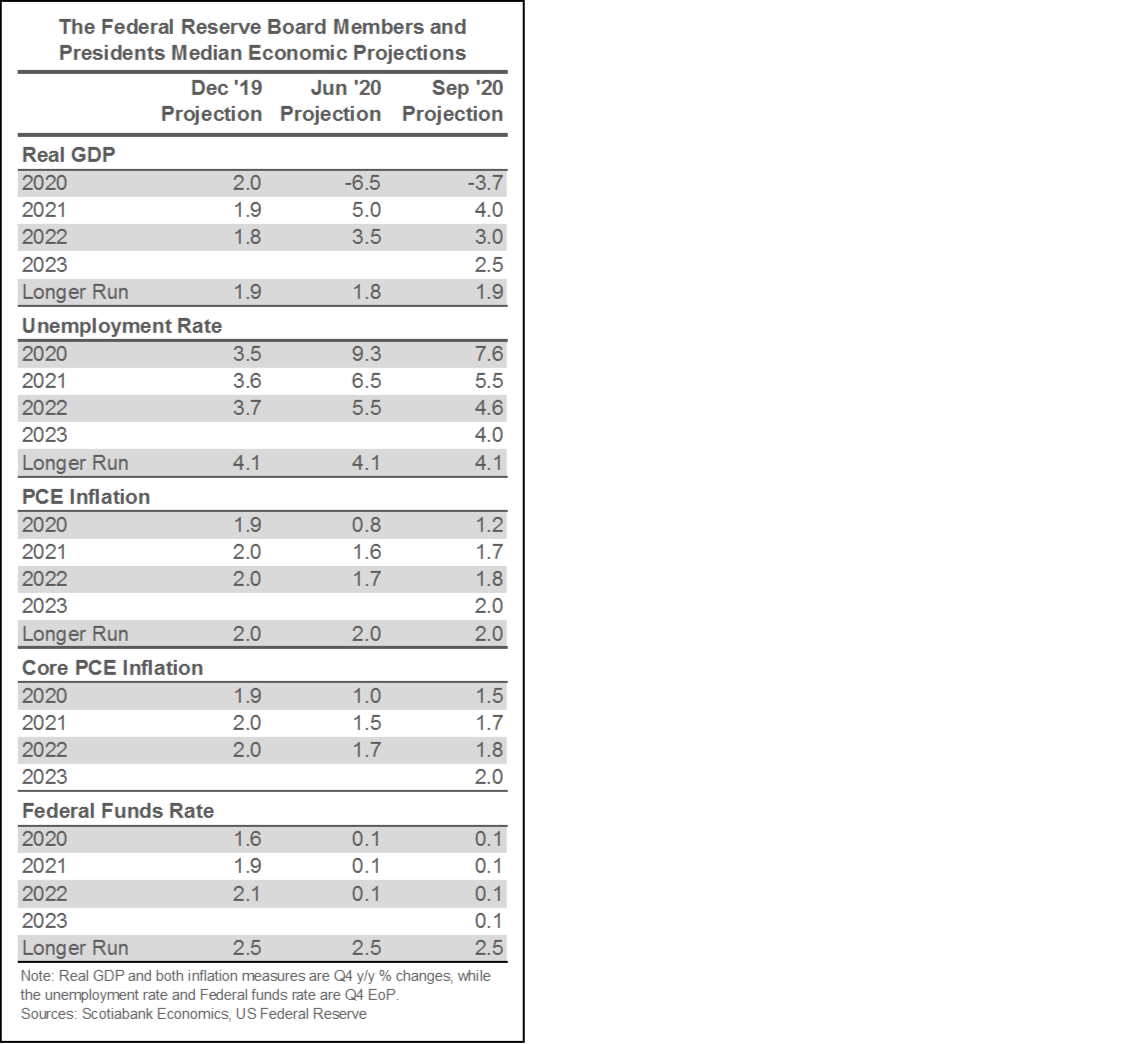

Positive forecast revisions to growth and inflation

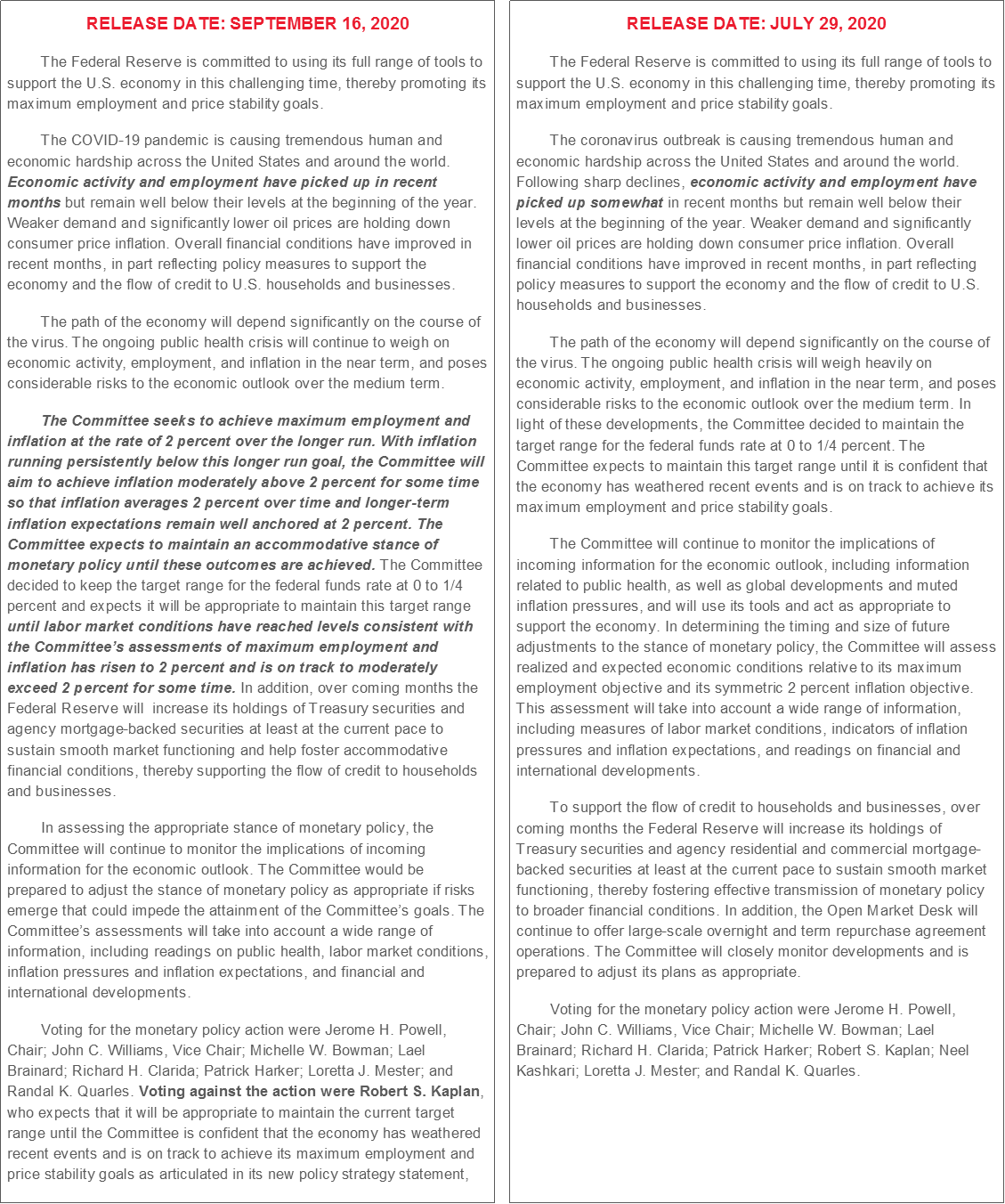

Statement codified longer-run goals

If having the kids back in school across many regions already has you thinking that late August seems so long ago, then apparently the FOMC agrees. While all policy instruments were left unchanged as expected, the airtight consensus that emerged on August 27th–28th when Chair Powell released the revised Statement on Longer-Run Goals and Monetary Policy Strategy at the annual Jackson Hole symposium sprang a little bit of a leak today. It still generally holds, just a touch less so.

Stocks lost some ground once the dust had settled following the statement and press conference that lasted just over an hour. The S&P500 initially gained ½% following the statement but then closed down by ½%. The USD appreciated a touch on a DXY basis. The US 10 year Treasury yield rose 2.5bps. It isn’t clear this was all due to the Fed reaction as the Information Technology sector turned lower starting toward the beginning of the press conference and led the S&P lower.

There were several ways in which a little less cohesion at the fringes and other changes injected somewhat more uncertainty toward the Fed’s commitments.

a) Dissenters return: There has not been a dissenting vote on the FOMC since the March 15th meeting when Loretta Mester preferred a 50bps cut instead of a full percentage point. This time there were two. Neel Kashkari dissented because he appears to prefer remaining on hold until 2% inflation has been achieved on a sustained basis instead of language describing a moderate overshoot for some time. Dallas President Kaplan dissented because he wishes to have greater policy rate flexibility beyond the point at which the goals laid out in the new policy strategy statement have been achieved. Their first speeches following today’s communications may further elaborate including Rosengren on September 23rd.

b) Dots: The revised dot plot (chart 1) shows continued unanimous agreement toward no rate change this year or next and slightly more agreement toward no rate change in 2022 as only one now forecasts a hike that year instead of two back in the June projections. The insertion of 2023 forecasts for the first time shows four out of 17 FOMC members forecasting hikes for a not inconsequential almost one-quarter of the committee. So much for “We’re not even thinking about thinking about raising rates” at least in the minds of these participants. The long run rate projection and the dispersion around it was unchanged.

c) Forecast revisions: Each of the growth and inflation projections were revised upward as shown in the accompanying summary table. The pace of contraction this year was reined in and Chair Powell acknowledged during the press conference that the recovery has proceeded faster than anticipated thus far.

d) Statement language changes: It wasn’t certain that the Fed would codify the changes to its longer run goals in today’s statement, but it was probable that they would and they did so. The statement openly refers to aiming to hit inflation “moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent.”

e) Purchase guidance: The statement itself could have gone more aggressive on the motives behind Treasury and MBS buying and did not. It is still primarily about sustaining smooth market functioning and helping to foster accommodative financial conditions. Powell’s press conference nevertheless did note that buying $120B of Treasuries (US$80B) and MBS (US$40B) per month is driven by broader motives than market repair.

Nevertheless, because we are just under seven weeks away from the Presidential election, it may be difficult to fully evaluate FOMC communications including openness to policy alterations in either direction. History tends to indicate that—barring exigent circumstances—the Fed stays out of things this close to an election, let alone this election! The next FOMC statement won’t be delivered until after the election on November 5th and even that one may be a quiet affair until some time passes.

Other core messages included noting that despite progress through a quicker than expected recovery, there is still a lot of spare capacity and half of all lost payroll positions remain unemployed. Powell observed that three-quarters of household spending has been recovered, housing has returned to its level at the start of the year and there are some signs of progress in business investment. He once again repeated that the virus remains a dominant uncertainty and was fairly direct in calling for further fiscal stimulus while evading questions regarding its optimal composition that are best left for Congress. Powell observed that the Fed is not out of ammo, but nevertheless repeated that there are limits to monetary policy such as the power to lend but not grant and that fiscal policy may be more effective.

COMPLEMENTARY MATTERS

Several complementary lines of questioning in the press conference may be of added usefulness.

When probed about financial stability concerns, Powell noted they have been around throughout the post-GFC period but never really materialized, that they are paying attention but that monetary policy is not the first line of defence as opposed to regulations, supervision, stress testing, high capital/liquidity requirements and macrpru tools.

I thought one of the better questions was whether the FOMC truly believed its ability to engineer higher inflation when its core PCE forecast only hits and never crosses 2% even by 2023. Powell was somewhat evasive when he said it will simply take some time to get above 2%. Of course, sensible people wouldn’t really hold anyone to macro forecasts that far out so we’ll cross that bridge when we get to it. Nevertheless, markets are priced for basically one outcome here and that is little inflation and no hikes for years to come so pick your tail.

Powell implied that FOMC members likely do incorporate expectations for fiscal stimulus in their committee forecasts because he said that failure to reach agreement over an additional stimulus package would “certainly be a downside risk” and that individual FOMC members have done what they think is appropriate. Translation? The next forecasts in December could downgrade expectations if no deal is struck.

When questioned about incorporating income inequality and housing affordability considerations into what the Fed does, Powell answered that they are doing constant research on such matters and how they affect the recovery but that monetary policy “can’t get at those things through our tools. Our tools and broad and can’t target particular groups.”

I liked Powell’s response when asked if we don’t get a vaccine until well into 2021 (or later..) what does that do to the economy? He noted that social distancing, mask wearing, cheap and rapid testing etc could still open up areas of the economy and a lot of workforces across the country.

Powell refused to address a question about stress tests saying he had nothing to offer today.

Powell was asked what is wrong with the design or function of the Main Street Lending Program given its trivial size. He offered a multi-part answer:

- Firms are not indicating credit constraints as the main problem, so maybe its usefulness was overstated;

- Some lenders are concerned about the underwriting expectations and feel they should underwrite the loans as they would others;

- It’s a facility for companies that don’t have access to alternative borrowing and otherwise why would we need it? Many do face alternatives;

- many businesses are still shut down and can’t service a loan so they need fiscal support instead;

- Powell would not comment on allegations that Treasury is saying to banks they should target zero losses in the mainstreet programs while Boston Fed President Rosengren said it should be up to Congress to decide that.

When asked about targeting assistance to commercial real estate, Powell rightly noted their powers are only indirect. The Fed cannot target particular sectors directly, but their facilities take CRE securities and the Main Street facility helps them pay their rent while CMBS spreads have tightened. Further, he noted that covenants often prohibit taking on more debt which is an impediment to providing more direct support.

Please see the accompanying statement comparison. The original statement can be found here and the original forecasts can be found here.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.