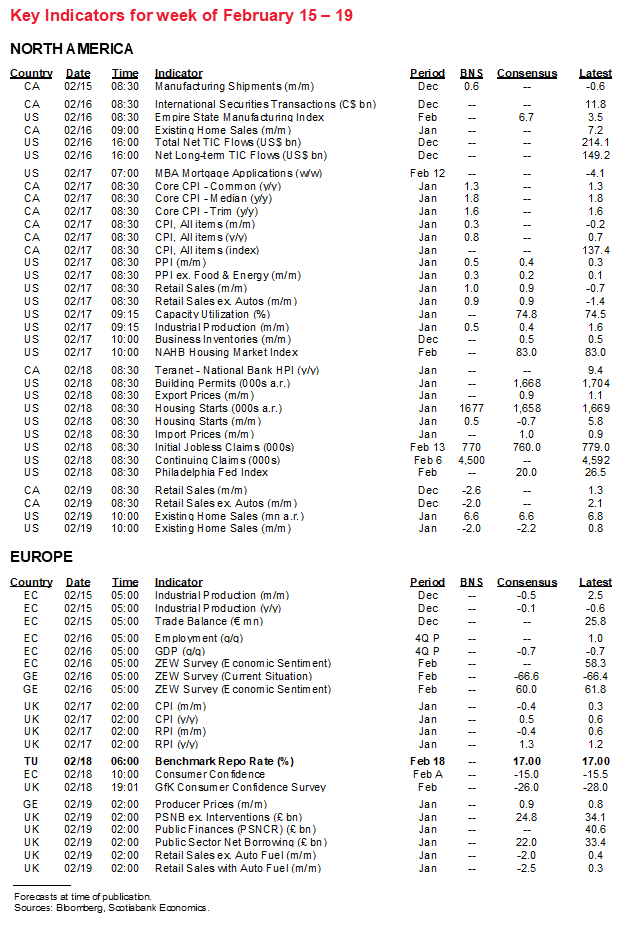

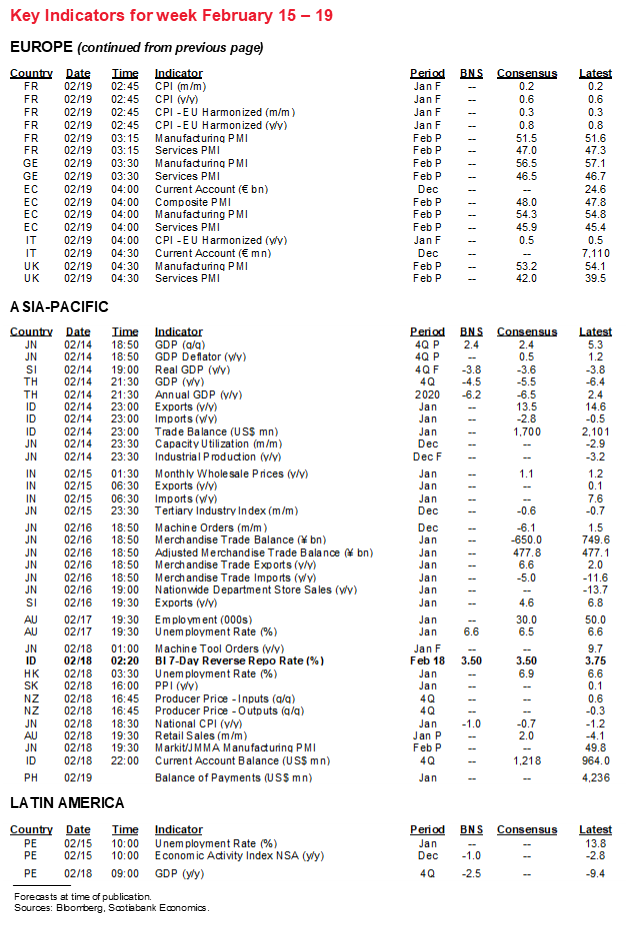

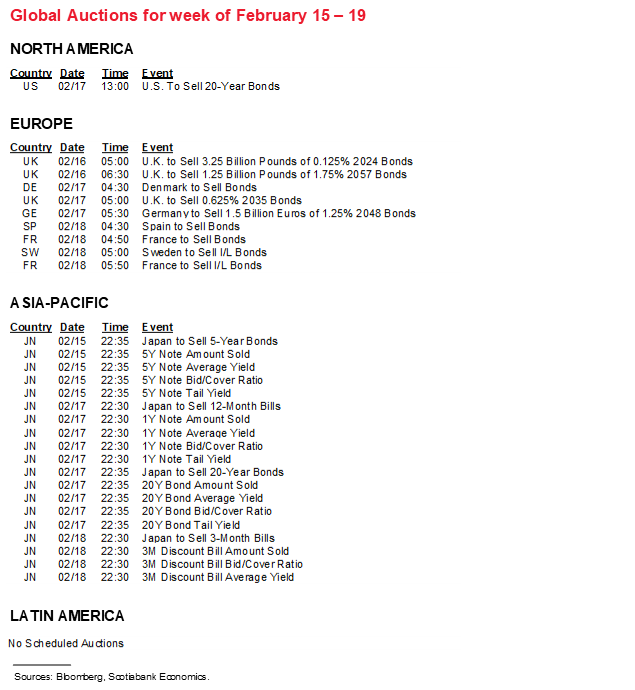

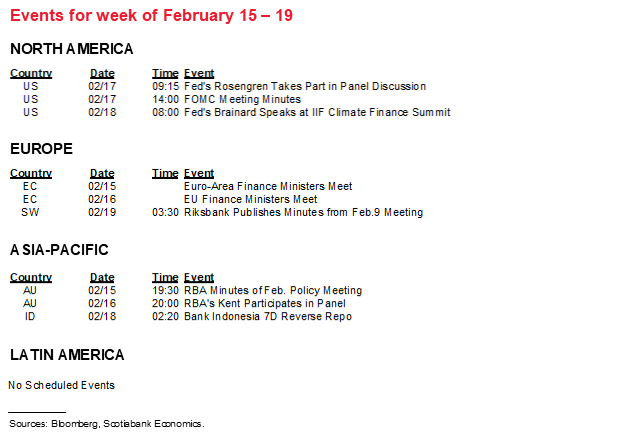

Next Week's Risk Dashboard

• Vaccine tracking

• CBs: FOMC minutes, Turkey, BI

• PMIs: US, Eurozone, UK, Australia, Japan

• Inflation: Canada, UK, Japan, Sweden

• GDP: Eurozone, Japan, Colombia, Peru, Thailand

• Jobs: Australia

• NF election

Chart of the Week

1. CENTRAL BANKS—PLEASE DEFINE “SUBSTANTIAL”

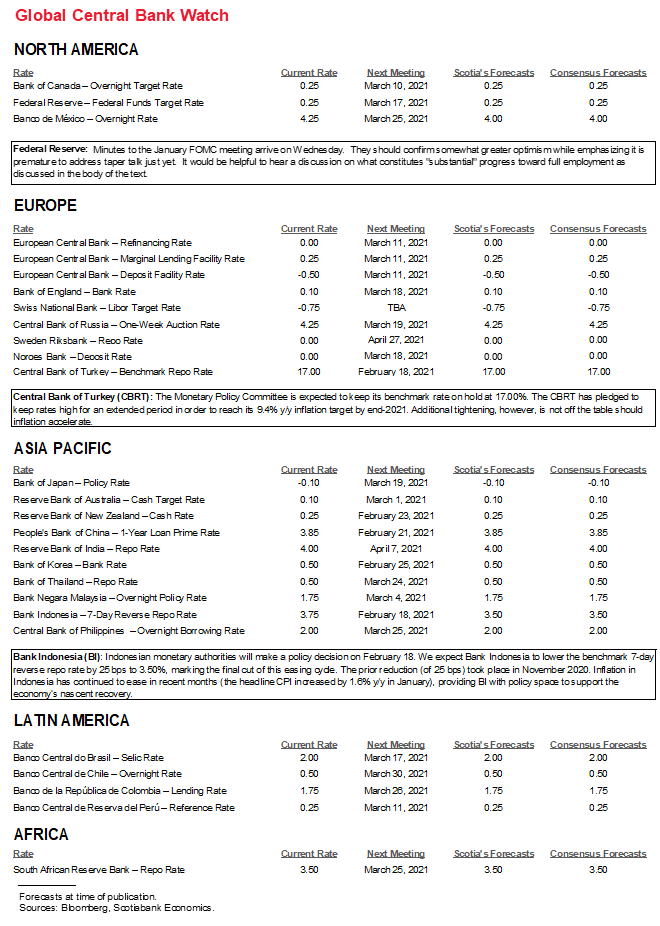

None of the central bank developments are likely to be terribly influential at the global macro level over the coming week, but there may be interesting developments nonetheless. The Fed releases minutes to the January 26th–27th FOMC meeting on Wednesday, while central banks in Turkey and Indonesia will deliver decisions.

Recall that the FOMC meeting delivered another upgrade to the Fed’s optimism (recap here). The bigger upgrade was at the prior meeting in December when the FOMC issued forecast upgrades that it let do most of the talking. January’s meeting nevertheless delivered small statement changes that sounded a bit more optimistic yet. Expect the minutes to repeat that it’s premature to talk about tapering just yet and that the Fed will be patient in assessing progress toward full employment and its “moderate” overshoot of 2% inflation for “some time.” The minutes may be stale in terms of references to fiscal policy and vaccines amid upgraded expectations perhaps since the January FOMC.

What I would like to see is the broader FOMC consensus weighing in on how to interpret full employment and what constitutes “substantial” progress toward the goal given this is the qualifier attached to continuing Treasury and MBS purchases at the current rate of US$80 billion and US$40 billion per month, respectively. That’s unlikely, but it flags a discussion worth having.

Is meaningful progress a substantial down payment toward recovering all or what ballpark fraction of the 9.9 million payroll positions and 8.7 million jobs in the household survey that have yet to be recovered from the pandemic? We forecast all of this to be achieved when the unemployment rate drops back down toward 3 ½% by the end of next year. Does it also mean that the FOMC wants to see the 4.3 million people out of the workforce brought back in? Even further to that, does it also want to see the 1½ million who are working part-time and would prefer full-time work actually securing full-time work? If so, that could take somewhat longer as indicated by the broader U-6 measure of unemployment (chart 1).

Or does the committee’s definition really go as broadly as Chair Powell suggested in the press conference following the January meeting when he said the following:

“When we say full employment is a broad and inclusive goal, we'll look at different demographic groups and not say we're at maximum employment until we are there across all pockets” in terms of women, different racial groups etc.

The more extreme the definition of full employment becomes, the greater the potential risk over time to inflation and hence tilting the balance of risks on the dual mandate in a different direction from present. Since the election, Chair Powell has put increased emphasis upon achieving a fully inclusive definition of full employment and spoken as if referencing how monetary policy will remain highly stimulative until fully equal labour market outcomes are experienced. Bear in mind that Chair Powell’s term is up for renewal next February, Vice Chair Quarles’ term is up this September, Vice Chair Clarida’s term is up the following month and there remains a vacant Governor position. All three of the Fed’s most senior roles are Republicans and are mismatched to the diversity and inclusion agenda that is strongly driving appointments in the Biden administration. I’m inclined to believe that Powell’s comments that imply an extreme definition of full employment are not to be taken literally, as opposed to treating them as being sensitive to the political climate that may shape the very top of the FOMC for years to come, but I’d like to see a fuller discussion on “substantial” across the FOMC. That could, for example, take the form of indicating acceptance toward one of these approaches using the language employed to denote frequency of citation in the minutes (none, one, a couple, a few, some, several, many, most, all but one, generally all).

For more on rates views including the Fed, please see the US-Canada Rates Outlook 2021–22: So Long Emergency, Hello Inflation piece here.

Turkey’s central bank is expected to hold its one-week repo rate at 17% on Thursday with a small minority expecting a hike. Inflation has risen to 15% y/y, but much of this reflected the lagging effects of the lira’s lengthy depreciation that was due to political challenges, often involving the central bank that previously eased under government direction, as well as the effects of sanctions. Back in 2014 it took about two liras to buy one USD before long-term depreciation drove that up to about 8½ at the peak last November. The return of tighter monetary policy that raised the policy rate from 8% last August to 17% by year-end has succeeded in turning the currency around somewhat to about 7-to-one. An evaluation period spent monitoring inflation and currency markets will likely mean a pause for some time.

Bank Indonesia has the opposite currency problem. It fears that if it cuts the 3.75% seven-day reverse repo rate on Thursday that it might stoke currency instability and potential balance of payments challenges. The currency, however, has been relatively stable for several months compared to the volatility through much of last year. That might allow the central bank to return to easing in order to address low inflation that entered the new year at about 1½% y/y on a headline and core CPI basis in line with the expectations of most economists.

2. REDOING THE PESSIMISTIC VACCINE NARRATIVE

Even the laggards are picking up the pace on vaccine deliveries, so the pessimism being spearheaded by the popular press has been excessive. Watch for further developments on vaccine take-up and covid-19 case counts over the coming week and beyond.

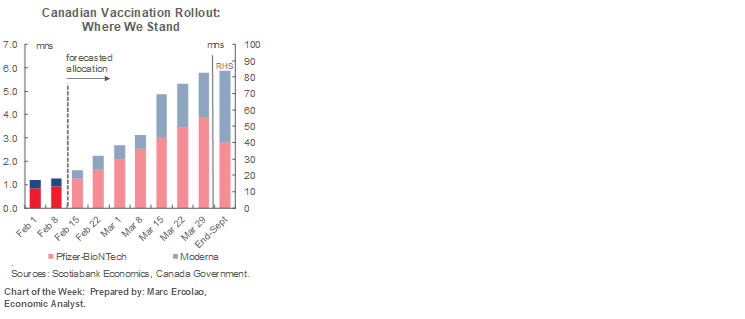

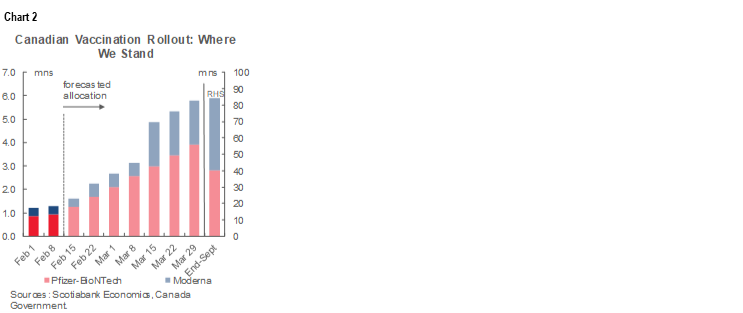

Enter Canada. The country may be arriving at the anticipated inflection point. Revised company guidance involves four million doses to be delivered to Canada by Pfizer by the end of March; being a two shot regimen and after adjusting for the 20% extra derived from withdrawing six instead of five doses per vial with the same efficacy, that translates into 2.4 million inoculations. Revised company guidance points to 84 million doses to be delivered to Canada between now and the end of September from Moderna and Pfizer combined (chart 2). If Health Canada moves toward approving the Oxford/AstraZeneca and Johnson and Johnson vaccines, then add another 20 million doses (10 million inoculations) and 38 million doses (and inoculations, being a one-shot vaccine) respectively. Let alone what would happen if the other vaccine candidates are approved.

In a country with 38 million people, just the Moderna and Pfizer supply will take care of the whole population. Presumably overshoots through supply from other vaccine makers would be either stored for second rounds, shared with other countries or redirected.

There remain plenty of risks. For one, we need vaccines and the sooner the better if mutations really spark a third wave soon, but thus far the case evidence remains pointed in the other direction and is being outpaced by doses administered so if that crossover point is maintained then net momentum has shifted more favourably (chart 3).

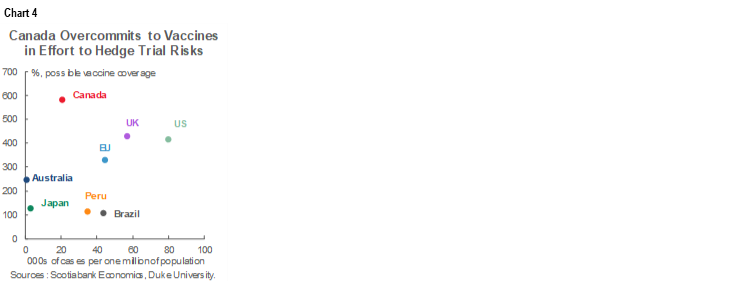

Whatever the outcome, let’s be fair here, folks. The Trudeau administration is taking much more heat than it deserves. Early on, Canada signed more contracts with companies for more doses than anyone else and certainly when scaled to the case counts (chart 4). Canada was ahead of most others which drew charges from other (particularly less developed) countries that Canada was unfairly securing this supply ahead of others who were less organized. Perhaps the others were just less well organized in advance and should answer to their own electorates for why that was the case, why they often continue to advise against wearing masks, etc. etc.

Second, we're getting to the point that was always expected to follow the temporary interruption partly owing to Pfizer's Belgian plant retooling that was necessary to scale up production. Canada regressed on its vaccine supply during that period and is on the cusp of catching up. Then factor in challenges stemming from a possible home bias for big pharma serving their own markets first while nonetheless in a tough spot navigating how to urgently supply enough vaccine to nearly 8 billion people around the world, decades of Canadian drug policy that were less favourable to drug innovation, not to mention Canada’s constitutional division of powers that grants much control over health spending and policies to the Provinces—that are often difficult to coordinate on any number of topics.

The point is that if we even come anywhere close to getting this kind of supply and rolling it out, then there has been far too much pessimism on Canada's vaccine issues and the outlook and far too little optimism which would be a disservice to more balanced debate over trying to time changes in the macroeconomic and overall policy environment.

In fact, consider that in the US, $2.3T++ of fiscal stimulus within two bills likely to pass within three months of one another will hit the economy over the summer just as a majority of Americans will be inoculated, given current distribution plans. In Canada, ditto on the vaccines but maybe a few months later, and then add imported benefits of US fiscal stimulus (through US consumption into the trade account) plus the pending Federal budget in Canada. All that the ministerial letters said was no "permanent" increase in spending, whereas the C$70–100 billion of added spending guided in the Fall statement was limited to three years (ergo, not permanent).

The next risk to the outlook to consider is whether people will take the bait in terms of behaviour. There are two reasons why they probably will.

1. The first one involves using our eyes. What you or I may think to be irrational behaviour isn't what matters. The reality is that people do hit the beaches, bars, gyms and restaurants the minute they can even if it is perceived to be irrational, which may be much less the case after getting vaccines. What I’m getting at here is to use the Warren Buffet approach when he hit a homerun on Amex. You know what the sentiment is, you can hear what analysts are telling you, now go to the check out counters and count the number of times people whip out their Amex cards with your own eyes, then buy it, and ride it to a fortune. It’s the same thing here: don’t impugn behavioural sensibilities because you disagree with them; such a normative filter has no place when forecasting the economy.

2. Second, never underestimate the power of consumers to spend everything they earn, or most of it. Betting against that is a main reason why consensus spends so much time revising up their forecasts during expansions with this one likely being no different. Sure, it may be a while—if ever—before we get line-ups at buffets, packed cruise ships, or people boasting about their airline status. Maybe that stuff will never be the same, but they'll spend it on other things while, at the same time, diverting what they are saving from not spending on transportation to the office, etc. etc. toward... Hey, let's rebuild the deck, buy that flashy tv, or re-shingle the roof. The macroeconomics is likely to restore consumption momentum which is the best remedy of all toward healing the tragic pain so many continue to experience.

3. WHAT PMIS SAY ABOUT NEAR-TERM GROWTH

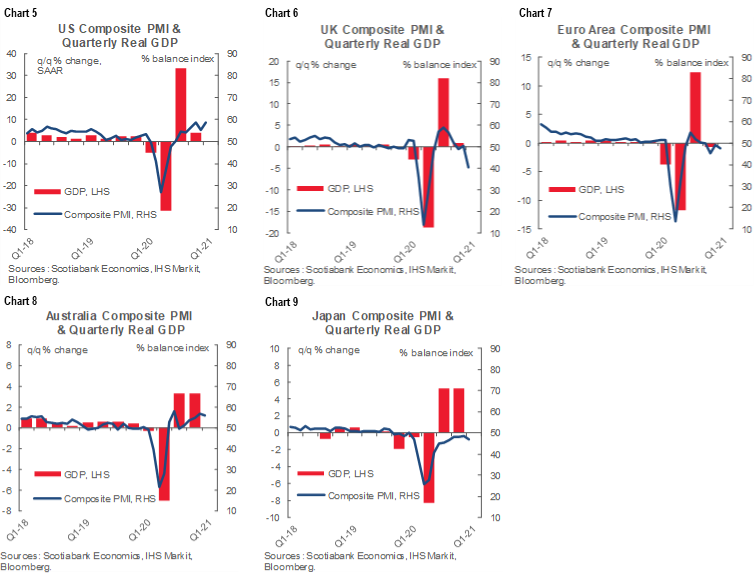

Going into a long weekend, I always say, What’s a month without another batch of global purchasing managers’ indices? Hmph. Well, ok, maybe that’s a wee bit of an exaggeration, but it’s still worth paying attention to the fact that the US, Eurozone, UK, Australia and Japan will offer February updates for these early readings of how GDP growth is tracking. Note the connections in charts 5–9 between the PMIs and GDP growth for why they matter to markets and forecasters tracking the current evolution of risks to the forecasts.

4. OTHER RELEASES

Canada and Japan (Wednesday) plus the UK and Sweden (Thursday) will offer up inflation reports for January. Canada is the closest to the central bank’s inflation target using the operational ‘core’ measure with little change expected next week; headline inflation is expected to edge slightly higher to 0.8% y/y with average core remaining near 1.6%. The UK is next with core inflation expected to be little changed from the 1.4% y/y rate set the prior month. Sweden’s inflation is expected to jump toward 1.6% in a marked pick-up driven primarily by year-ago base effects. Japan remains in deflation.

Four sets of Q4 GDP numbers will be released including Japan (+10.1% q/q SAAR), Thailand (3 ¼% q/q SAAR) and Colombia (+<6% q/q) to kick off the week, followed by Peru on Thursday that is likely to show a continued ~3% y/y contraction.

Other US releases will focus upon industrial and household readings. In addition to Friday’s Markit PMIs, the Philly Fed (Thursday) and Empire (Tuesday) readings will inform ISM-manufacturing expectations. Industrial output during January is due out on Wednesday. A 2% gain in vehicle sales and a rise in gasoline prices are among the contributing drivers behind expectations for a gain in retail sales on Wednesday. Existing home sales, housing starts, weekly claims and producer prices round out the hits.

Canada will also update retail sales (Friday) with earlier Statistics Canada guidance pointed toward a 2.6% m/m drop for December but watch the January guidance for fresher information. Monday should offer a better start to the week, however, as manufacturing sales are expected to rise by 0.6% m/m based on earlier guidance. Canada also updates existing home sales for January on Tuesday. Newfoundland and Labrador heads to the polls on Saturday, or rather, some of them will after COVID-19 resulted in the postponement of voting in about half of the districts. It’s one for the incumbent Liberals to lose (chart 10).

Miscellaneous international releases will offer up Australian jobs for January (Wednesday), German investor sentiment (Tuesday) and UK retail sales (Friday).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.