- The Fed sounded more optimistic again…

- ...through small statement changes…

- ...and in Powell’s press conference

- No policy changes were hinted at…

- ...but remarks were consistent with our taper expectations

- The Fed’s goal of a fully inclusive job market is too lofty…

- ...with the policy tools at its disposal…

- ….and is unlikely to be achieved...

- ...without courting materially higher inflation risk

Markets paid relatively little heed to Fed communications on balance, but the aftermath saw a small bid to the US dollar and slight temporary upward pressure on the 10-year Treasury yield as stock selling marginally intensified from 2pmET onward.

Why? The Fed…dare one say…sounded optimistic as it reinforced the generally more upbeat stance at the December meeting! Good heavens who spiked the water coolers over at the Eccles Building?! Big pharma did, that’s who. The Fed’s more upbeat stance cannot be characterized as strident and there was nary a whisper of a pending taper, but, like golf, monetary policy is a game played one stroke at a time and today’s swing added to some of the optimism.

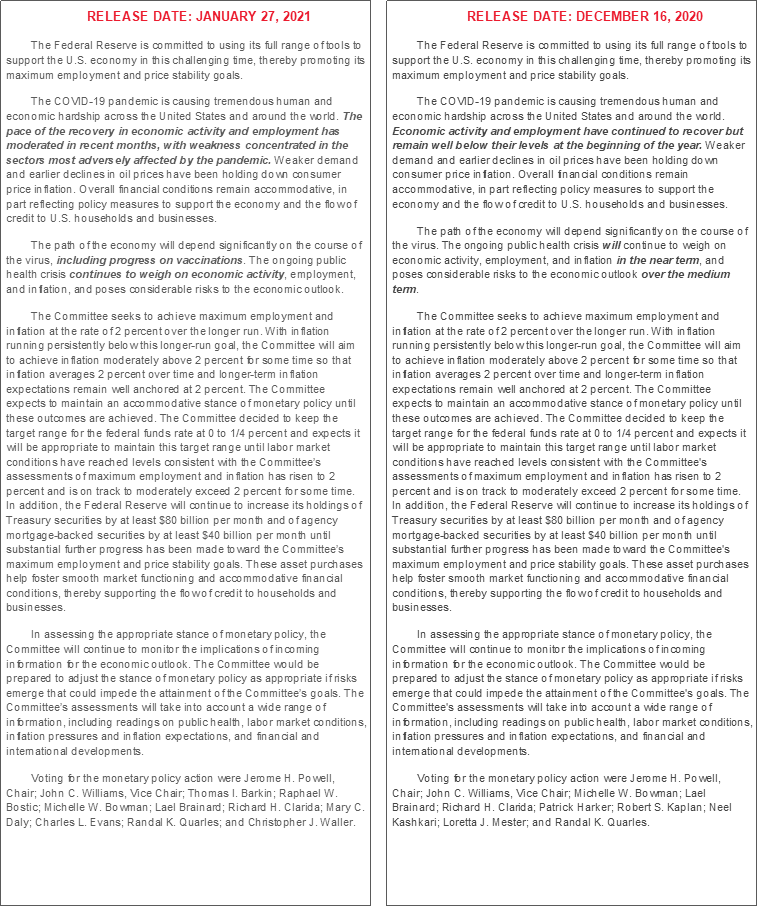

First off, four changes in the statement generally hinted at a bit more optimism on balance, but not evenly so. The changes included the following that are also highlighted in the accompanying statement comparison.

- The second paragraph noted that “the pace of the recovery in economic activity and employment has moderated in recent months” which is just a truism compared to the initial burst of activity and hence not terribly meaningful.

- Also in the second paragraph, the Fed hinted at how it is more encouraged by a narrowing breadth of the pandemic’s shock effect on the American economy by stating “with weakness concentrated in the sectors most adversely affected by the pandemic.” Chair Powell reinforced this interpretation of what this statement change meant during the press conference when he emphasized improvements elsewhere in the economy in terms of housing, business investment and manufacturing. The Fed is still concerned about pandemic effects, but sees areas of the economy to celebrate.

- The statement finally codified reference to vaccines in the third paragraph after passing on the chance to do so in the December statement following vaccine developments since November.

- That same third paragraph involved three subtle changes. One was that they changed the tense in reference to how covid-19 is impacting the economy by dropping “will continue to weigh on economic activity” in favour of “continues to weigh on economic activity.” Second, they dropped reference to how COVID-19 poses risks “over the medium term. Third, they also eliminated “in the near-term” from that same sentence. When probed about these changes during the press conference, Powell confirmed that “we dropped in the medium-term because the risks are in the nearer term.”

This somewhat more optimistic slant was bolstered by several remarks in the press conference. For example, Chair Powell said “we need to finish the job” and “it’s within our power to do that this year” in reference to the collective abilities of all policymakers. He also repeated reference to how the pandemic “had a much smaller effect than expected” on the economy as “people just got on with their lives” even as COVID-19 cases picked up over the summer. Then when the larger wave hit starting in the Fall, Powell observed that the impact on nonfarm payrolls in December involved a more concentrated effect on the most directly impacted sectors like bars and restaurants, while elsewhere “it’s not having an effect.” He also used trading floors as an example of how the ability to adjust to work-from-home dynamics has been much better than initially feared.

The press conference added discussions on several other important matters.

When to Taper

On tapering the present flow of purchasing US$80B/month of Treasuries and $40B/month of MBS, Powell said “The whole focus on exit is premature, if I may say,” and that “We think it’s premature to think of tapering. We want more progress. It’s too early to focus on dates. We’ll communicate clearly to the public well in advance of when we think we will do a gradual taper.” He also went on to say that “We think our stance is just right” and that “We think we’re in the right place.”

This was expected as Powell wouldn’t wish to risk a taper tantrum at this juncture and will only reveal the Fed’s intentions much closer to the point of possible action. Such references to tapering are likely to heat up over 2021H1 before gradually beginning to taper purchases early next year. That, in turn, could easily drive more volatility around higher yields than we presently show in our Treasury curve forecasts.

Will Facilities Slated to Expire in March be Extended?

When asked about potentially extending several facilities that are slated to expire at the end of March, Powell only said that “We're going to continue to monitor conditions. If emergency conditions persist then our emergency facilities will continue. I have not had meetings or discussions with Treasury on that.” In my view, emergency conditions have passed quite some time ago and while there may be a case for allowing the facilities to expire, their underutilization may pose little downside to extending them other than tying up Treasury capital that may be put to better uses by that time.

Is More Fiscal Stimulus Needed Without Sparking an Inflation Problem?

This was kind of a rookie style of questioning as Fed Chairs are well versed in ducking the sights of newly elected members of Congress. Still, when questioned about whether further fiscal stimulus is required following passage of the US$900 billion package at the end of December, Powell deferred to Congress, as is customary, but emphasized how “We’re a long way from a full recovery” and “the economy is a long way” from dual mandate goals.

How Will the Fed Know it has Crossed the Inflation Rubicon?

Related to the prior question was that when asked how the FOMC will assess whether a pick-up in inflation is durable or transitory, Powell remarked that “we’re going to be patient if we see small and likely transient effects on inflation” and that the Fed doesn’t expect to see “troubling” inflation given its belief that the Philips curve remains flat and inflation persistence remains low across the world. He argued this is because of changing demographics, advancing technology and globalization. He also repeated that the Fed views inflation that is too low to be a bigger and more difficult problem to address than inflation that is too high.

In my view, the issue is likely to turn from when the Fed sustainably hits its inflation and full employment goals and more toward the suitability of maintaining emergency levels of stimulus after the passing of emergency pandemic considerations. You can still maintain highly stimulative policy with a bloated balance sheet and a policy rate below the FOMC’s estimate of the neutral rate while nevertheless moving away from extreme emergency levels of stimulus as we have at present. If downside risk to the dual mandate continues to diminish, then that should merit experimenting with gradual removal of policy stimulus before fully achieving all dual mandate goals.

Is Fed Policy Driving Bubbles?

Yes of course, there are bubbles everywhere and Fed policy is exclusively to blame so Powell apologized profusely.... When are journalists going to stop asking a Fed chair about bubbles and the Fed’s role? They’ll never get the ‘gotcha’ quota to boost the reporter’s career. They sure didn’t today and with good supporting points for why not.

When probed on whether monetary policy is driving bubbles that could spark fallout if they burst, Powell said their focus is principally on the economy and dual mandate shortfalls, while emphasizing that their financial stability framework looks at a variety of readings that portray overall stability risks as “moderate.” He also emphasized that the financial system is resilient to shocks including to banks, nonbanks and money market funds. Last, he noted that valuations were principally driven by vaccines and fiscal policy but that monetary policy does play a role; this is where I found his argument became weak, since one might expect functioning financial markets to need fewer monetary policy supports if the other drivers of the outlook have improved. When asked if monetary policy would be used to address asset value imbalances, Powell said that they don’t theoretically rule it out but it’s not something they’ve ever don or would do versus relying on macroprudential tools.

The Fed’s Full Employment Goal Dominates—But Sounds Unattainable as Defined

Powell bluntly remarked that “I’m more concerned about people losing their jobs and careers than I am about higher inflation.” That continues to tilt the policy emphasis more toward the full employment half of the dual mandate than inflation.

Powell observed that there are still 9 million out of work with policy supports and that “Fully defeating the pandemic and getting back to a place where it's safe to resume normal activities is still the goal and needed.” His line of commentary implied that getting all nine million jobs back will be a starting point to achieving full employment.

I say starting point because of his ongoing characterization of full employment (note that we’ve heard the same from the BoC). “When we say full employment is a broad and inclusive goal, we'll look at different demographic groups and not say we're at maximum employment until we are there across all pockets” in terms of women, different racial groups etc. That sent a shiver down my spine to be honest. Of course that’s not because I wouldn’t very much like to see such an outcome and I share Powell’s enthusiasm for addressing such shortfalls in the American labour market. It’s just that when I hear monetary policy makers say it, I get pretty nervous about the risks they may be courting through the blunt tools they have at their disposal, assuming they truly believe what they say.

The heart of the matter involves what can be achieved over a reasonable time frame and whether monetary policy is the right tool to do so without courting greater risk than reward. Over fifteen years ago I led a Canadian diversity study that sought to quantify the economic cost to not addressing labour underutilization across various groups in society and made policy recommendations like sharply raising immigration rates, spending on daycare and early childhood education, reforming municipal funding through infrastructure bonds, 3Ps and Tax Incremental Financing, eliminating mandatory retirement in the 60% of provinces that still foolishly had it, improving foreign certification of workers, offering more flexible maternity leave including phased mat/pat leaves, tax reforms to lessen disincentives to second earners that disproportionately impact the decision for a second household earner to join the workforce. This study was done before the so-called ‘woke’ era that now dominates.

Where are we today? While there has been some progress, we’re still largely just talking about the same things but in a more ‘woke’ context with fancier slogans. But in the 15–20 years since that and prior work, I would say not say there has been anywhere near enough progress to merit thinking that we have everyone with equal choices to matter enough to monetary policy makers which is my point. Targeting a fully inclusive workforce is like turning a slow-moving ship that encounters a lot of hardwired resistance in society along with the constraints of the political and business cycles and the net effects upon productivity, inflation and overall costs and benefits. If central banks sit on super easy monetary policy "until all pockets" of underutilized labour are fully employed as Powell just said, then we'll still be at numbers like ¼%, $80B and $40B until we’re all pushing up tulips. Hellloooo inflation!

That leads to my final point. The Fed’s goals should arguably not be so slanted toward such an extreme definition of full employment as leaving no stone unturned in the recovery. That’s probably an unrealistic goal as not even every one of the nine million still unemployed Americans who had jobs just before the pandemic are likely to return to the workforce in full within a reasonable time horizon versus, say, exiting through early retirement or embracing different flex choices. Who knows what fraction of that nine million will ultimately return, but the inflationary consequences that could stem from the actions of the other 143 million employed Americans may be the bigger risk to the price stability half of the Fed’s dual mandate. While Powell’s inflation arguments are good ones, he neglects to mention that we’ve never seen monetary policy shift toward achieving such a strict measure of full employment which may change historical relationships between an altered definition of full employment and inflation risk. Even more unattainable will be absorbing all other potential workforce entrants and then fully employing every nook and cranny of the labour force that was underutilized before the pandemic. Easy money won’t achieve that and perhaps should not even try given the mixed risks.

At the end of the day, I don’t think the Fed will truly seek to achieve such a strict measure of full employment. They will tighten long before then. The argument to maintain stimulative monetary policy for that long is very likely a political ruse. The Fed routinely gets grilled by members of Congress about its alleged role in driving everything that's wrong in society and what the Fed can do about it. It’s easier than, say, members of Congress questioning themselves. Saying that the Fed is in tune with such pressures is good politics that keeps at bay potential politicized changes to its mandates and powers that could come at a high price to its independence.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.