FORECAST UPDATES

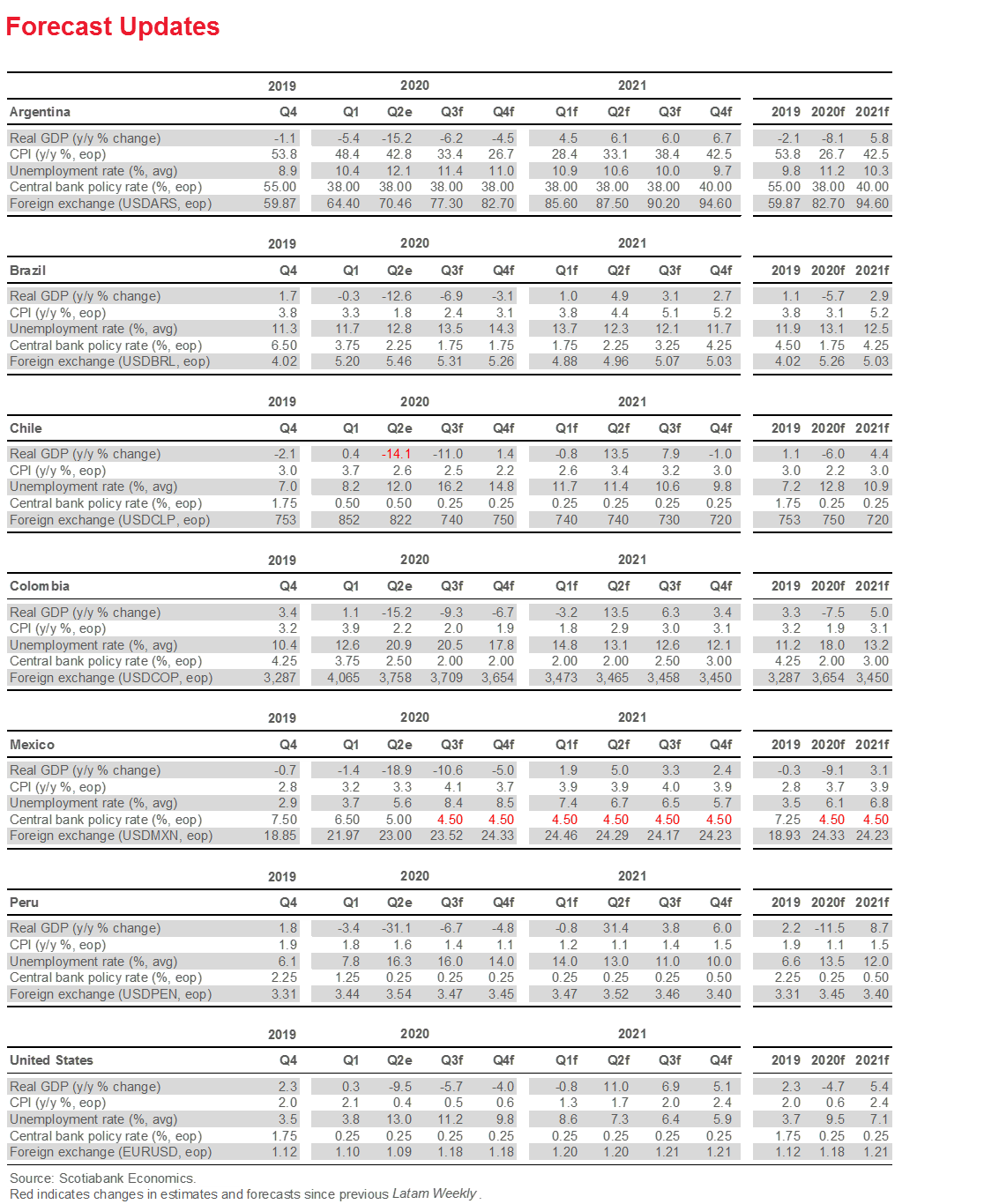

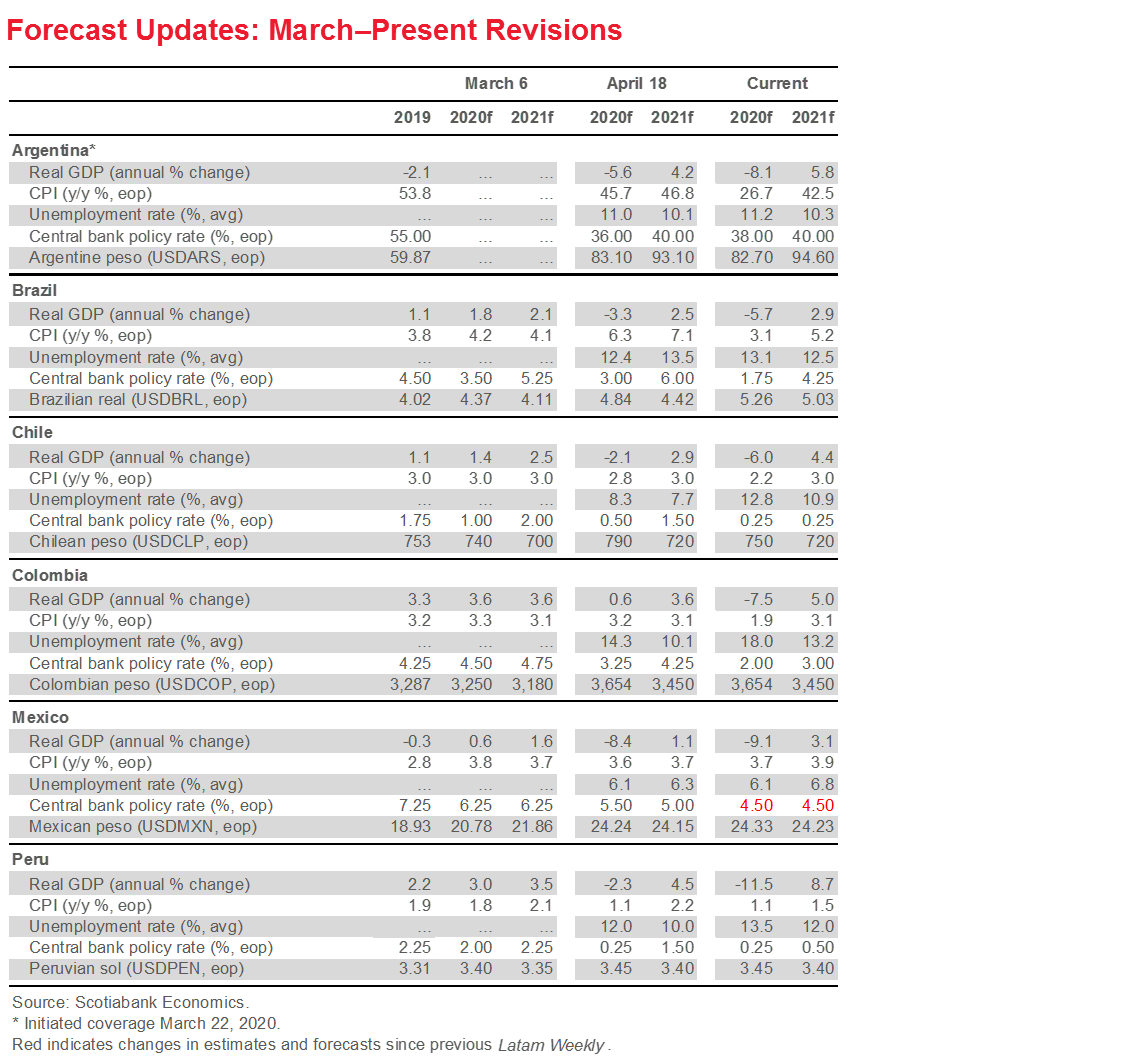

Our forecasts are unchanged aside from a revision in the Banco de Mexico’s terminal rate for this easing cycle from 4.75% to 4.50% to reflect its last monetary policy decision.

ECONOMIC OVERVIEW

Although pandemic control measures in Latam remain amongst the strongest in the world, the region is still one of the main global hotspots for COVID-19, with relatively poor indicators and new outbreaks. Nevertheless, the Latam-6 economies continue to rebound, but further progress on economic re-opening is going to get harder unless the pandemic is brought under control.

MARKETS REPORT

We make the case for a stronger Peruvian sol (PEN) based on our expectations of greater USD supply from the mining sector, reduced USD demand from Peruvian entities, and a central bank that could become more active in FX markets.

COUNTRY UPDATES

Concise analysis of recent developments and guides to the fortnight ahead in the Latam-6: Argentina, Brazil, Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

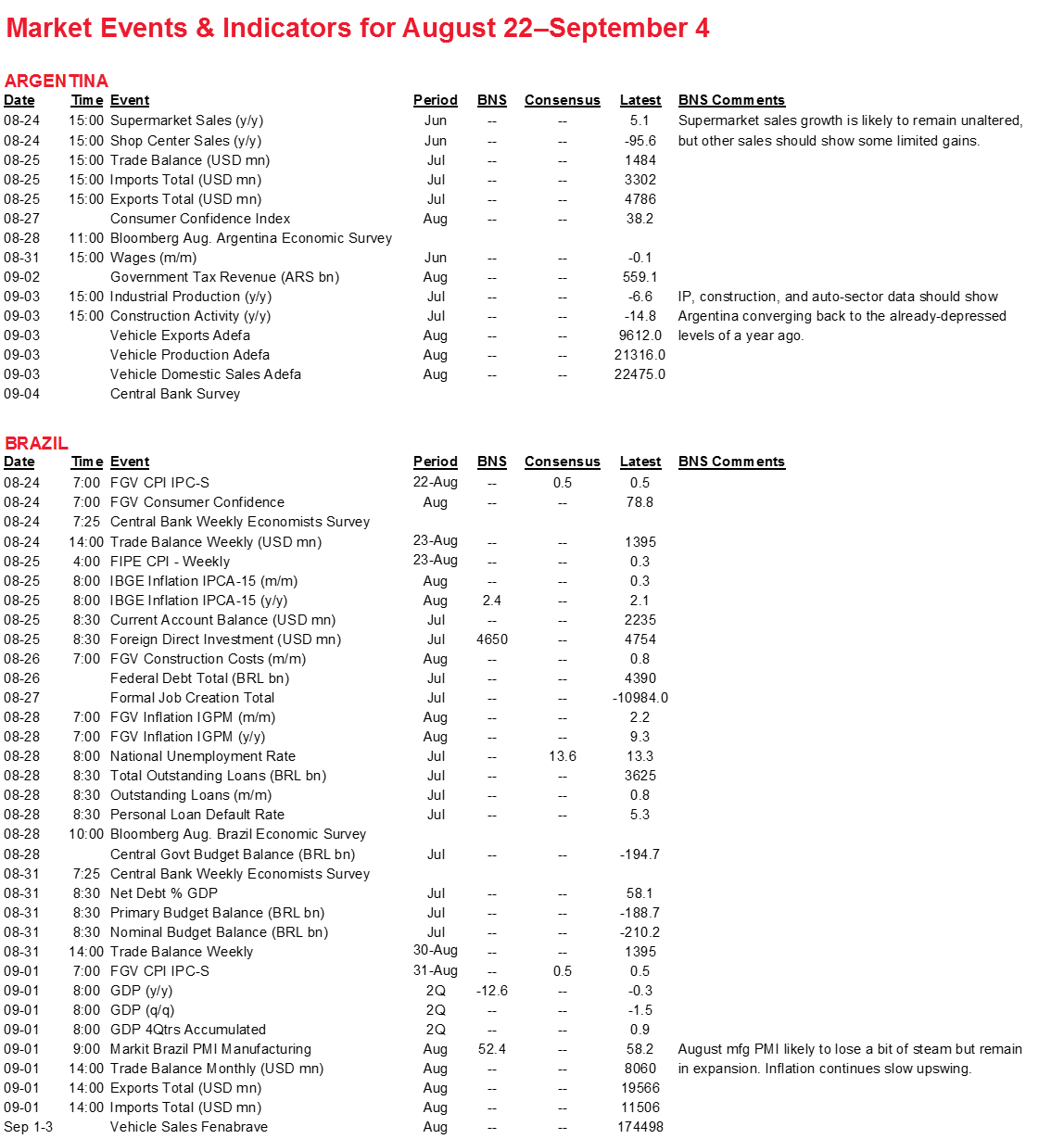

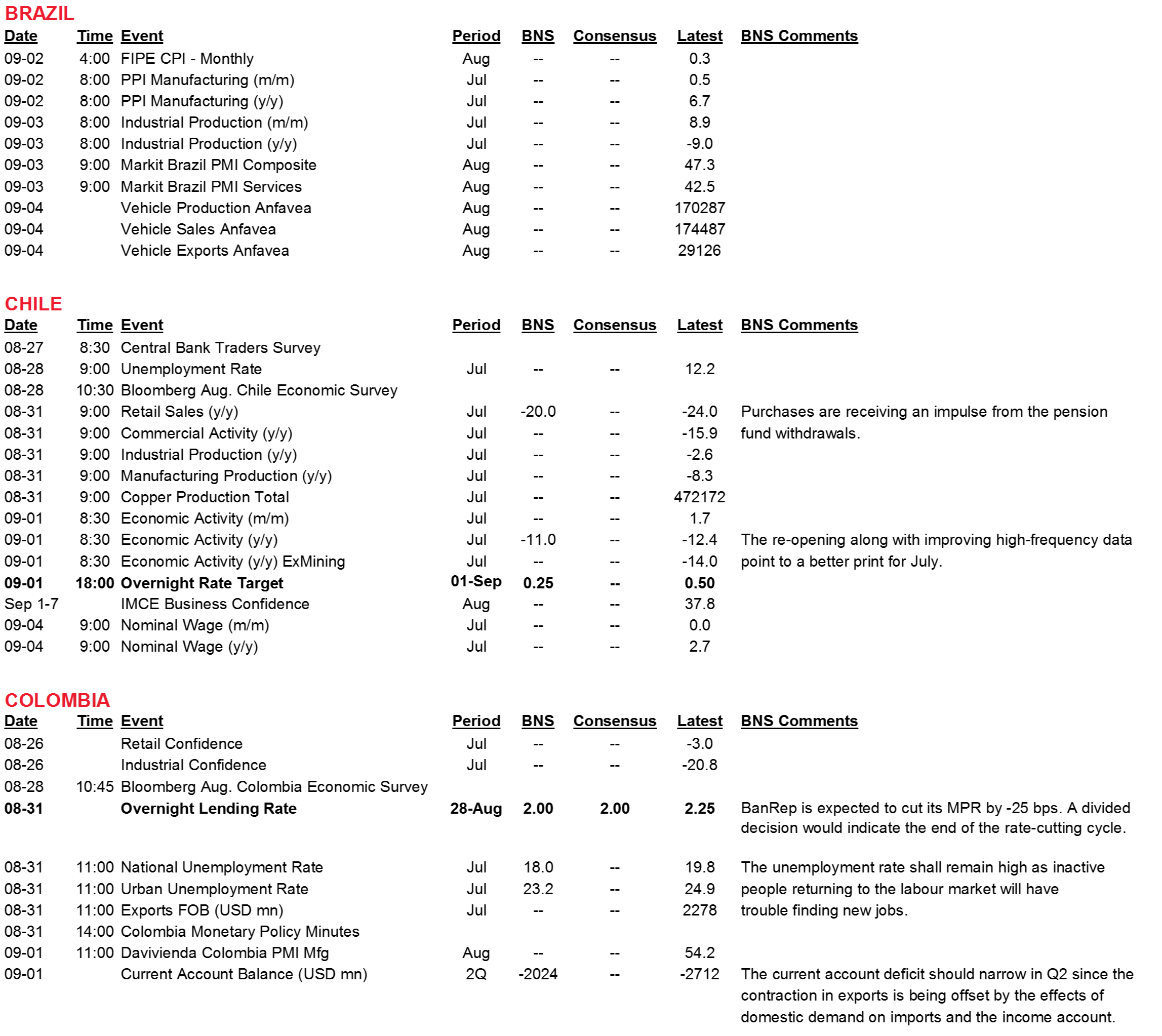

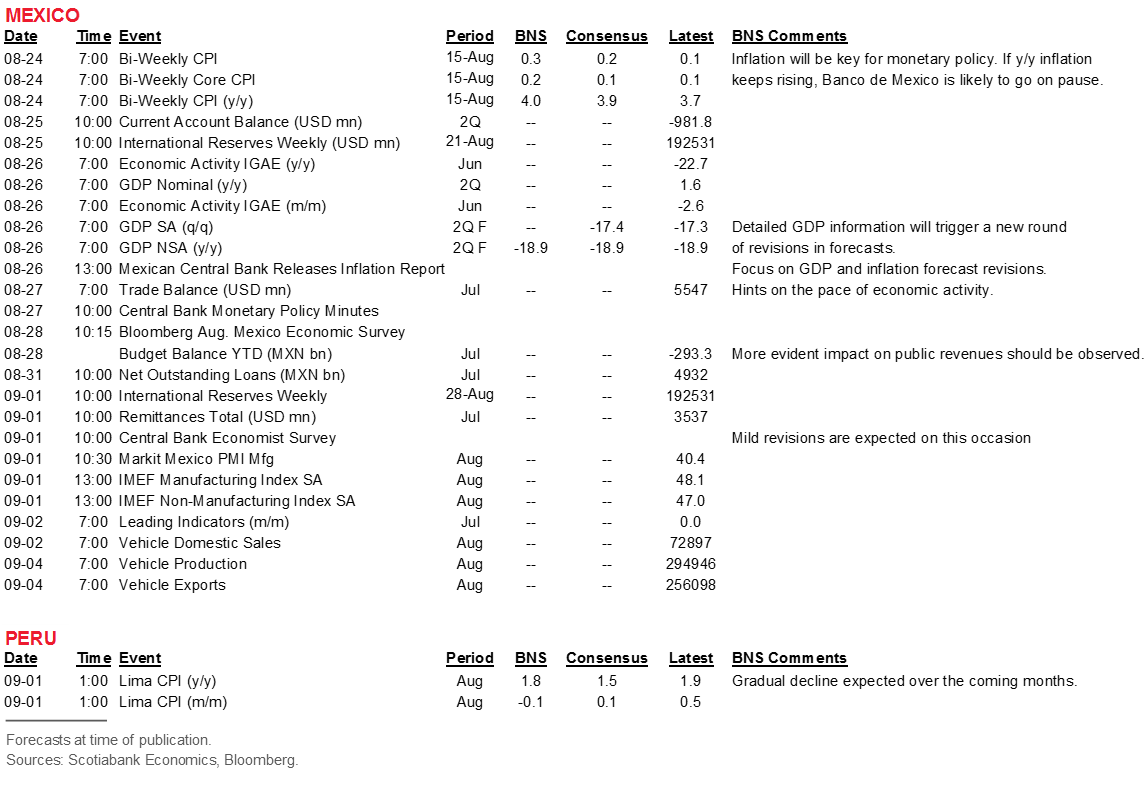

Risk calendar with selected highlights for the period August 22–September 4 across our six major Latam economies.

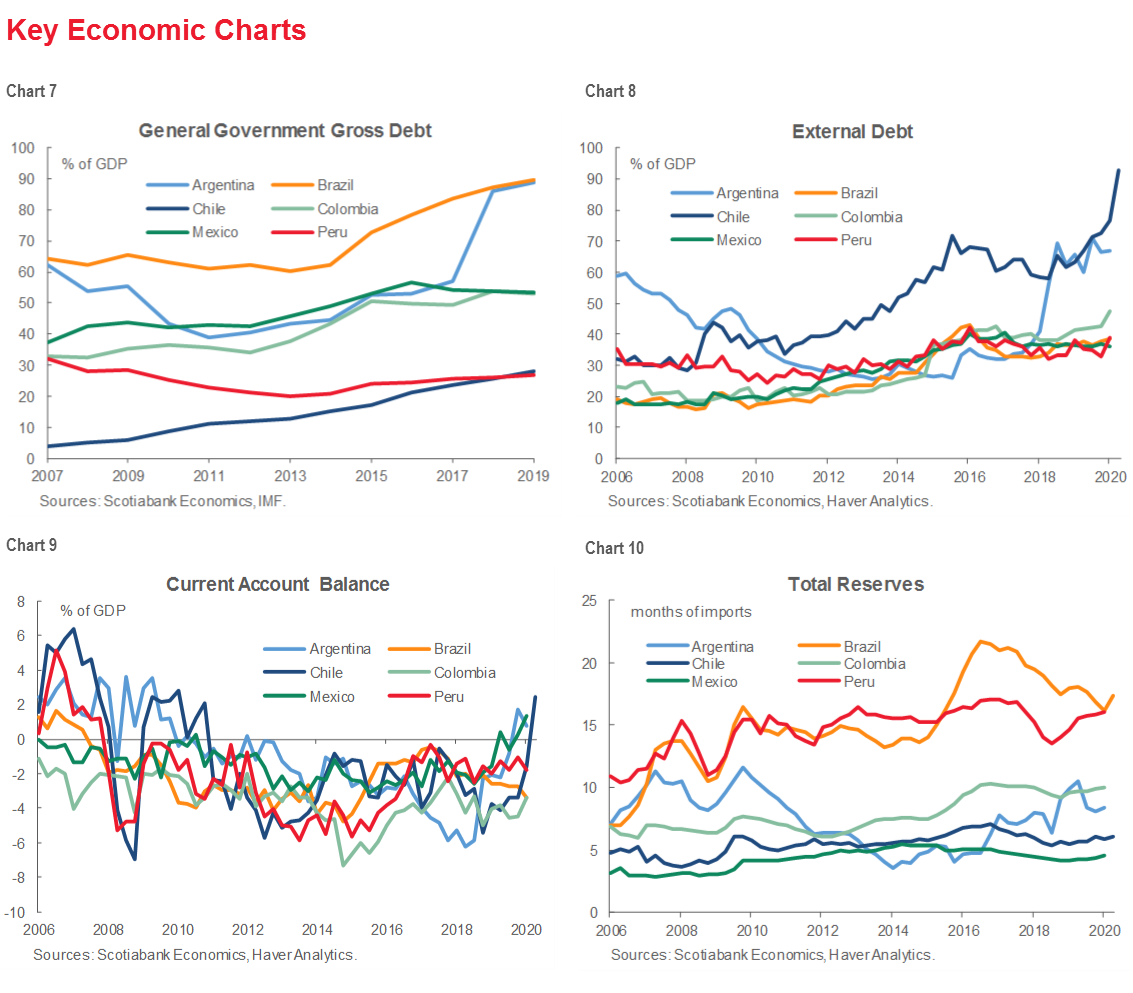

Economic Overview: Healthy Public, Healthy Economy

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

Thanks to our teams in Mexico City, Bogota, Lima, and Santiago for their excellent contributions to this section.

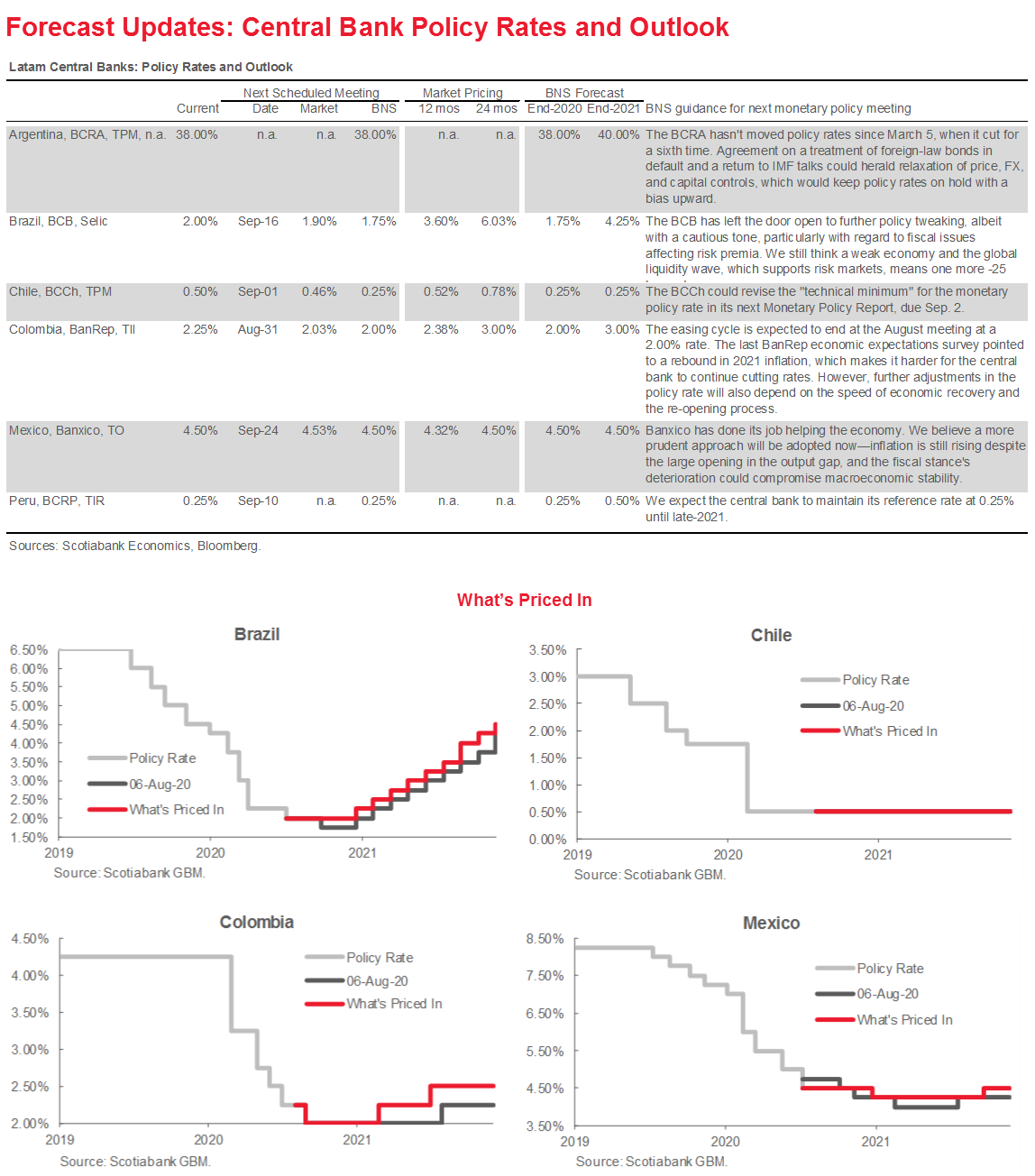

Central banks in Chile and Colombia are both expected to deliver a final -25 bps cut to their key monetary policy rates. Mexico’s Banxico will release both its Quarterly Inflation Report and the Minutes from its last monetary policy meeting.

Brazil, Chile, and Mexico will see a range of important data prints over the next fortnight that will be critical to our outlook going forward.

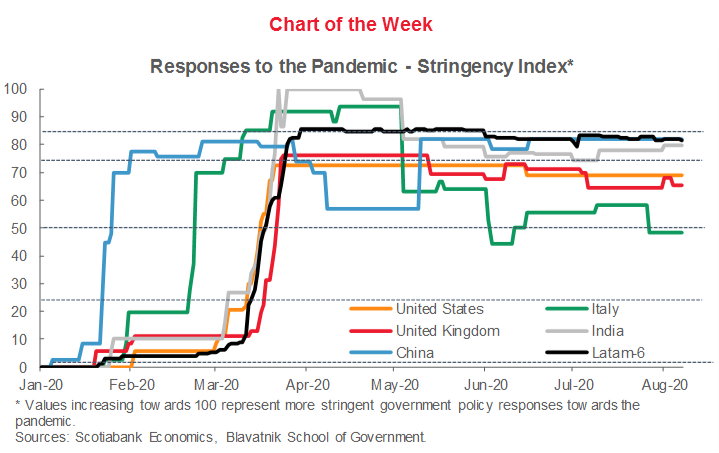

Latam is still a hotspot for the COVID-19 pandemic despite some of the most stringent control measures in the world. Research underscores the need to maintain these measures in order to ensure continued economic recovery.

MARKET MOVES AND FORECAST UPDATES: LOCAL STORIES

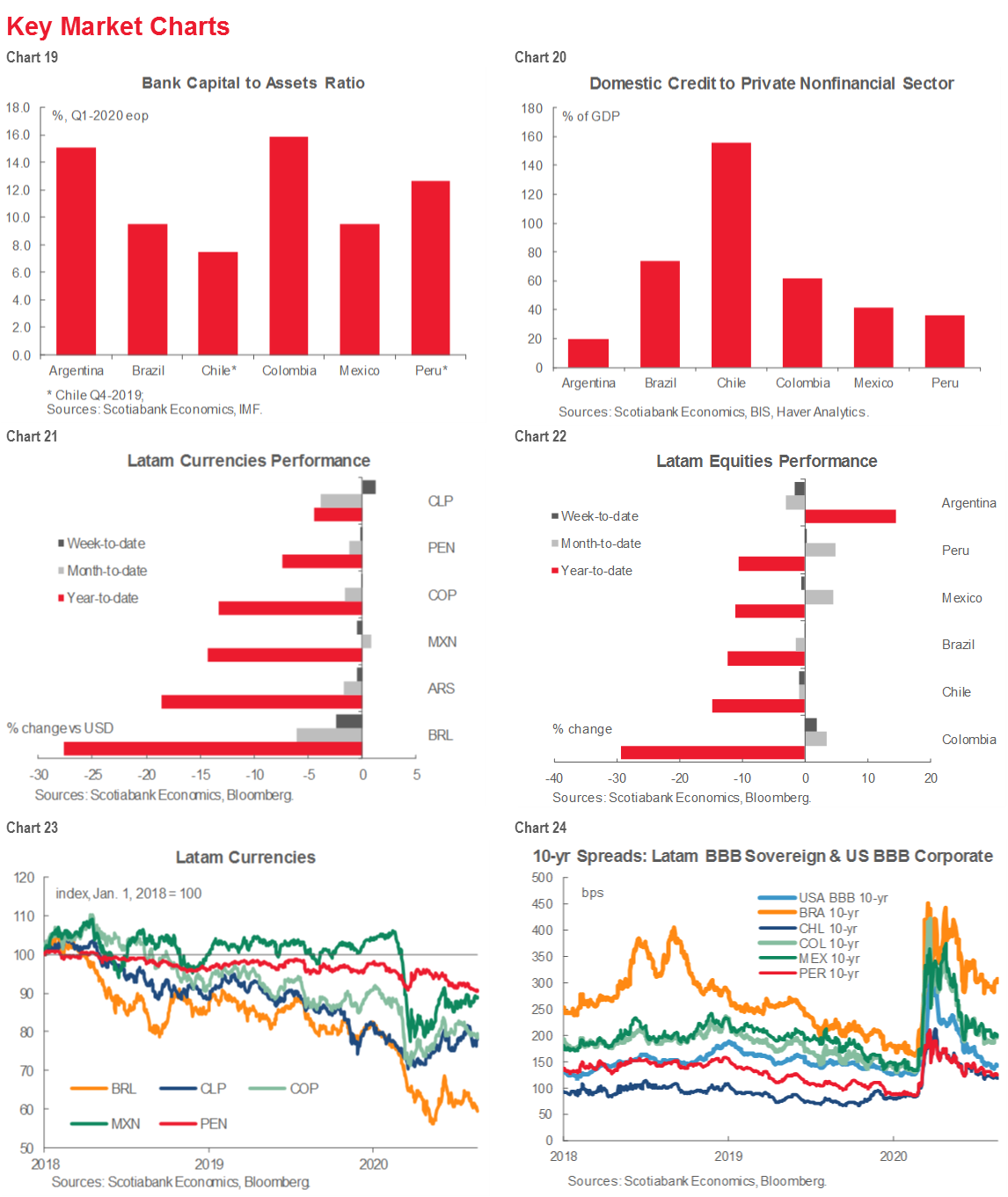

While the FOMC’s Minutes released on Wednesday, August 19 provided some mixed signals for risk assets, Latam markets over the last week responded mainly to local narratives (tables 1 and 2). The biggest story was the political schism in Brazil between the Executive and the Senate, which pushed the BRL down -3.5% on the week and nudged the sovereign curve marginally wider (see the Key Market Charts section). Argentina equities slid -4.5% on strong, but weaker than expected, growth numbers; meanwhile, Colombian equities advanced on better coincident indicators and soft inflation expectations that could spur further monetary easing.

FORTNIGHT AHEAD

I. Central banks

Chile. The BCCh monetary policy committee (MPC) meets on Tuesday, September 1 and our Chilean economists have a strong conviction call that the MPC will deliver a -25 bps cut from the central bank’s current “technical minimum” of 0.50% to 0.25% (see Forecast and Central Bank tables, pp. 2 to 4). The rate decision will be followed by the publication of the BCCh’s quarterly Monetary Policy Report on Wednesday, September 2, where we expect the BCCh to lay out its review of monetary policy and make the cases for a revision in its working floor for the nominal monetary policy rate.

Colombia. The BanRep’s next scheduled monetary policy decision falls on Monday, August 31 and our team in Bogota expects a last -25 bps cut from 2.25% to 2.00% (see Forecast and Central Bank tables, pp. 2 to 4). At its last monetary policy meeting on Friday, July 13, the Board of Directors delivered a -25 bps cut to 2.25%, in line with nearly every analyst’s expectations. At that time, the Board repeated its mantra of data-dependent gradualism, but retreated somewhat from its prior concerns about risks of disruptive capital flows even as it cut its growth outlook.

Mexico. Banxico’s Quarterly Inflation Report arrives on Wednesday, August 26. We will be particularly focused on any changes in the outlook for real GDP growth and inflation.

The Minutes from the Banco de Mexico’s monetary policy decision on Thursday, August 13 follow the next day on Thursday, August 27. At that meeting, the Governing Board cut the interbank rate by -50 bps from 5.00% to 4.50%, which was in line with market consensus, but went further than the -25 bps our team in CDMX expected in the context of rising headline inflation. In the event, the decision followed from a split 4–1 vote, where one member of the Board opted for a -25 bps cut. In light of this dissent, we expect the Bank to remain on hold at 4.50%, consistent with the post-meeting statement’s emphasis that the available room to maneuver will depend on the evolution of factors that affect the outlook for inflation and inflation expectations. Nevertheless, the Minutes will likely shed some light on which factors could drive any further cuts and how the Board is considering recent increases inflation. That said, forecast revisions in the Inflation Report will speak more loudly than any account of discussions in the Minutes.

II. Macro data

Brazil, Chile, and Mexico see the heaviest fortnight of data releases in our Market Events & Indicators risk calendar (see the back of this report):

- Brazil will see a spate of inflation readings at the beginning of this week that we expect to confirm an upswing, followed by credit data at the end of the week and Q2 GDP numbers on Tuesday, September 1 that are largely stale at this point. The August manufacturing PMI on the same day is expected to show some slowing in the recovery.

- Chile. Santiago sees a full slate of key data releases during the week of Monday, August 31, with prints for July on retail sales, industrial production, mining, wages, and the monthly GDP proxy.

- Mexico. Bi-weekly inflation on Monday, August 24 will be a key determinant of next steps by Banxico and our team in Mexico City expects the pace of price increases to edge upward, adding support to their view that Banxico is now on a long hold. Q2 GDP on Wednesday, August 26 will be combed over for detailed data that will underpin our next set of forecast revisions and provide detailed context for Banxico’s Quarterly Inflation Report.

Argentina will see the release of tier-2 activity data over the next two weeks, while Colombia prints July labour-market data on Monday, August 31, and Peru’s August inflation numbers follow on Tuesday, September 1. Our team in Lima expects a milder-than-consensus decline in the year-on-year headline in August, and expects 2020 inflation to be higher than the BCRP’s forecast. At present the Bloomberg consensus y/y and m/m medians are inconsistent with each other and don’t provide a clear benchmark.

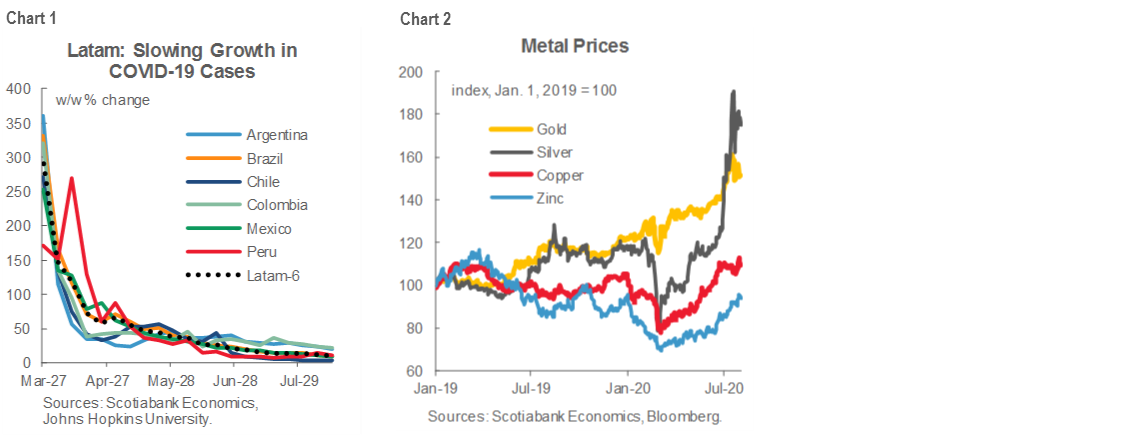

COVID-19: REBOUNDS ADVANCE, BUT IT’LL GET HARDER FROM HERE

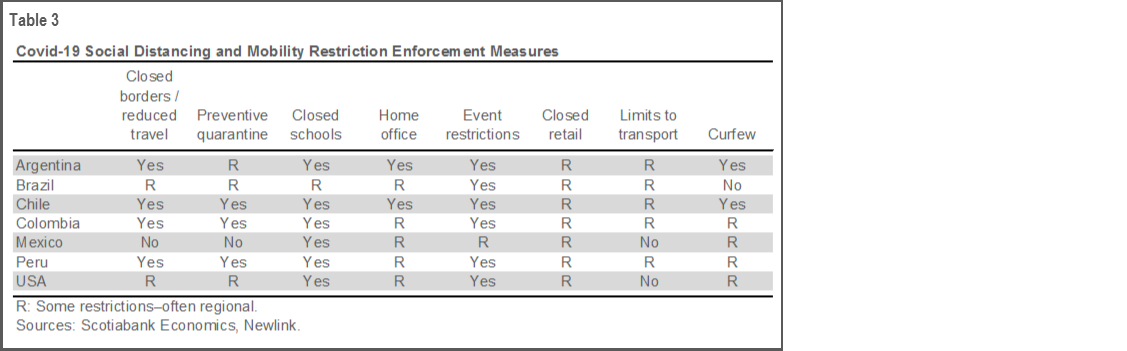

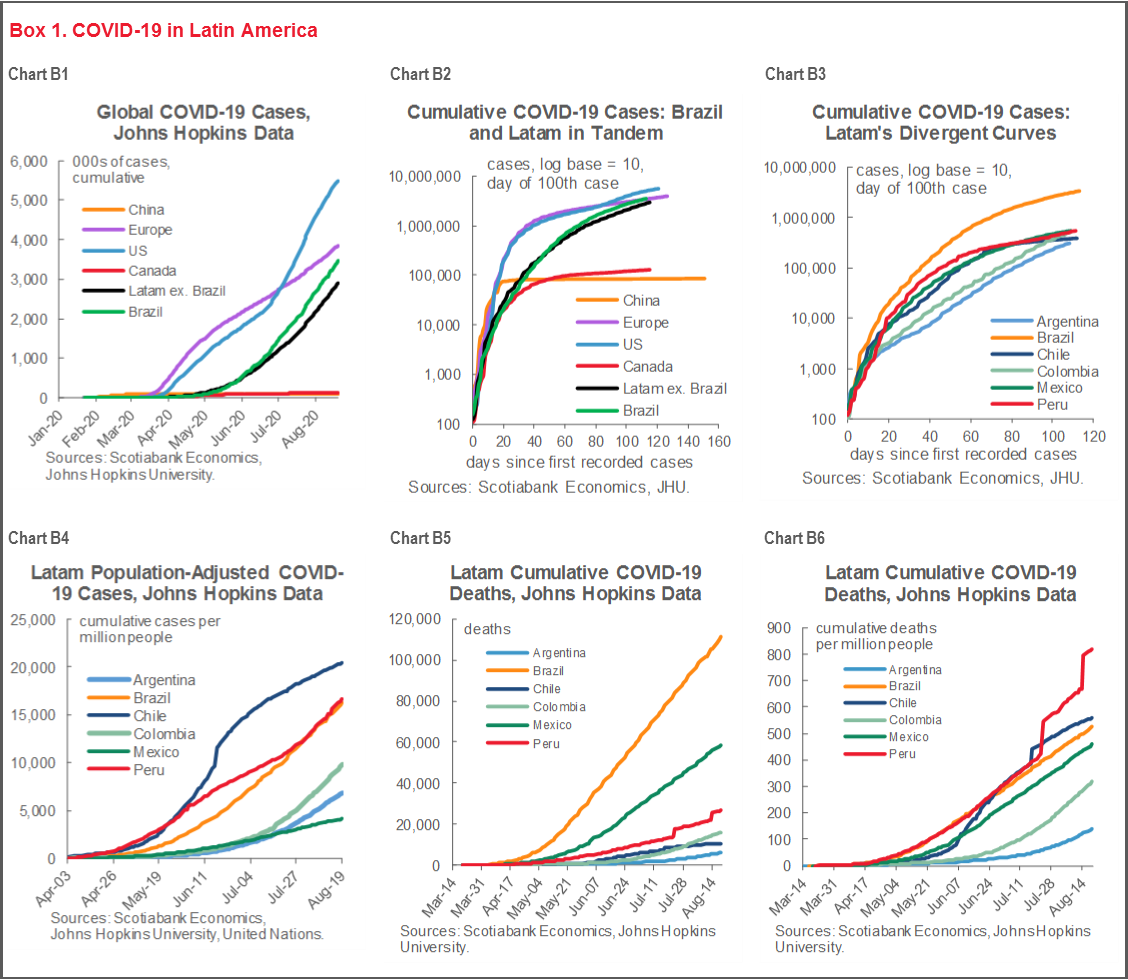

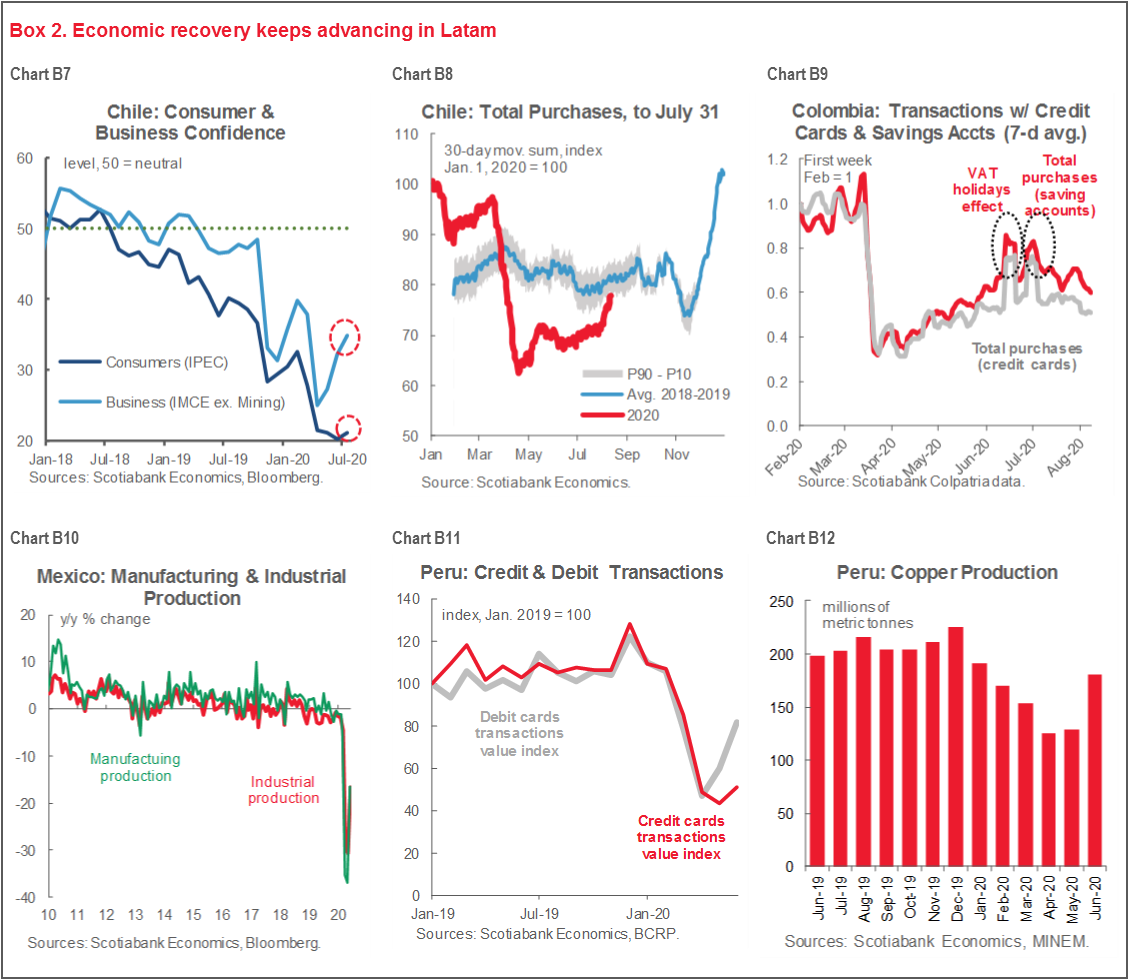

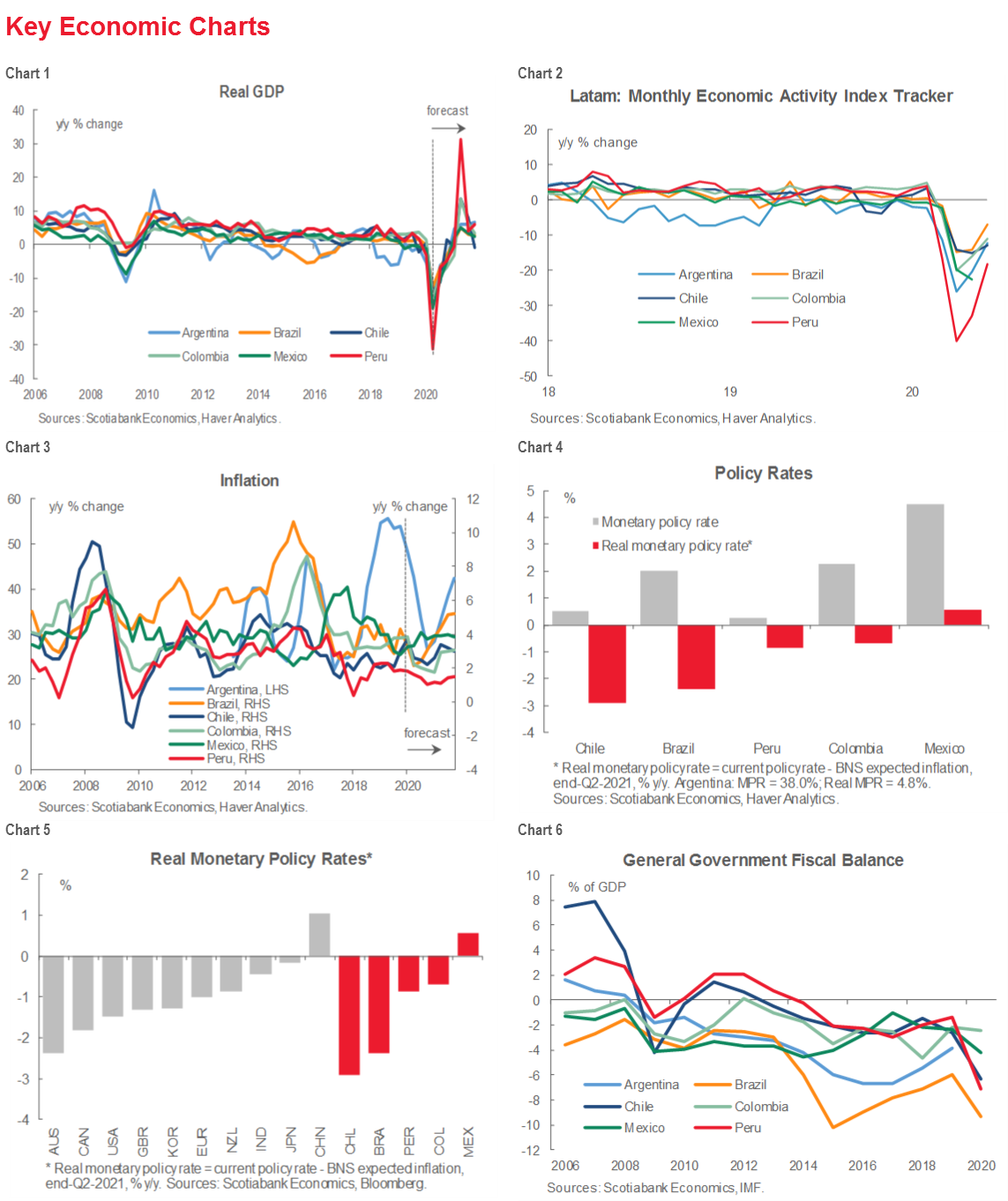

Latam’s COVID-19 numbers continue to tell a difficult story of a pandemic hotspot that isn’t easing (Box 1, charts B1 to B6) even though contagion growth rates are broadly down over the last few months (chart 1) and control measures remain amongst the most stringent in the world (see the Chart of the Week, p. 1, and table 3). Still, economic re-opening continues, and Latam economic indicators (Box 2, charts B7 to B12) paint a picture of progressive recovery supported by recovering commodities demand (chart 2). Just as in the US and Canada, where high-frequency data imply some slowing in the process of economic rehabilitation, further progress in Latam will be contingent on getting the pandemic under control.

Our “Useful References” below collects a bevy of recent research that underscores that public health and economic recovery are complements, not substitutes. Across pandemics past and present, concerted control measures lead to faster returns to business as usual. Latam’s COVID-19 fighters will need to stay the course.

USEFUL REFERENCES

McKinsey & Company, “COVID-19: Implications for Business,” August 20, 2020: https://www.mckinsey.com/business-functions/risk/our-insights/covid-19-implications-for-business?cid=other-soc-twi-mip-mck-oth---&sid=3611607906&linkId=97745216#

Joel Blit, Chuanmo Jin, and Mikal Skuterud, “Re-Opening and Re-Closing the Economy Strategically,” August 21, 2020: https://www.cdhowe.org/intelligence-memos/blit-jin-skuterud-%E2%80%93-re-opening-and-re-closing-economy-strategically

Sergio Correia, Stephan Luck, and Emil Verner, “Fight the Pandemic, Save the Economy: Lessons from the 1918 Flu,” March 27, 2020: https://libertystreeteconomics.newyorkfed.org/2020/03/fight-the-pandemic-save-the-economy-lessons-from-the-1918-flu.html

Austan Goolsbee and Chad Syverson, “Fear, Lockdown, and Diversion: Comparing Drivers of Pandemic Economic Decline 2020,” June 2020: https://www.nber.org/papers/w27432

Markets Report: The Case for a Stronger PEN

Tania Escobedo Jacob, Associate Director

212.225.6256 (New York)

Latam Macro Strategy

tania.escobedojacob@scotiabank.com

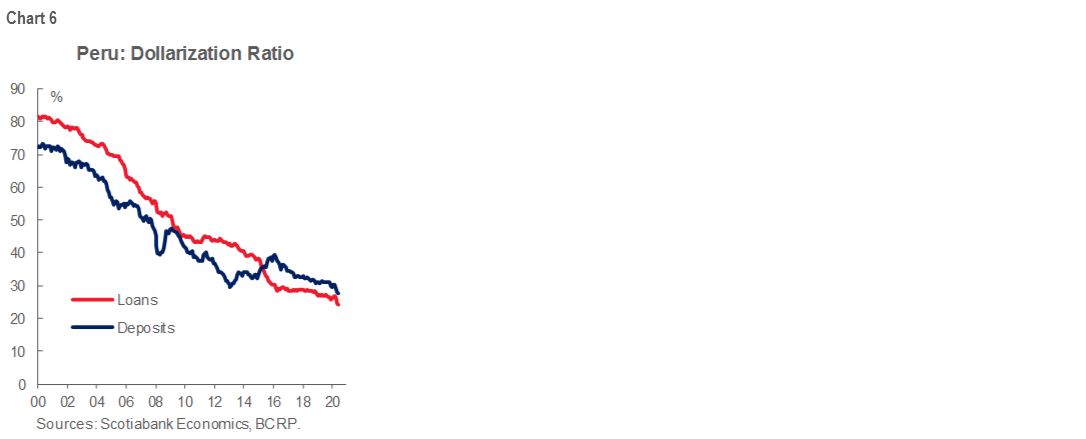

PEN has been among the worst performing currencies in the last four months and is currently fluctuating around its all-time low of 3.5847/USD.

We think the forces driving the move are local and identifiable, namely, 1) a decrease in USD supply from the mining sector, 2) an increase in USD demand from the local corporate sector, and, 3) a central bank relatively absent from FX markets.

In our view, these sources of distress in the local market will fade in the short term and we are keeping our target of 3.45 for USDPEN by year-end 2020.

IDENTIFYING AN OPPORTUNITY

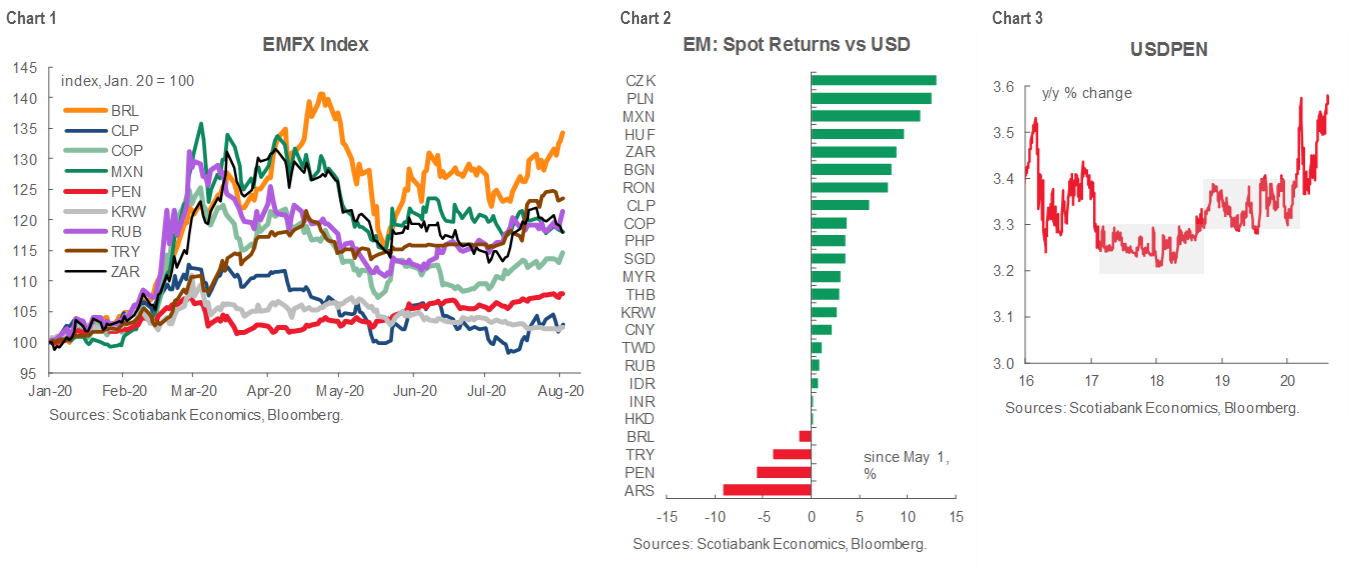

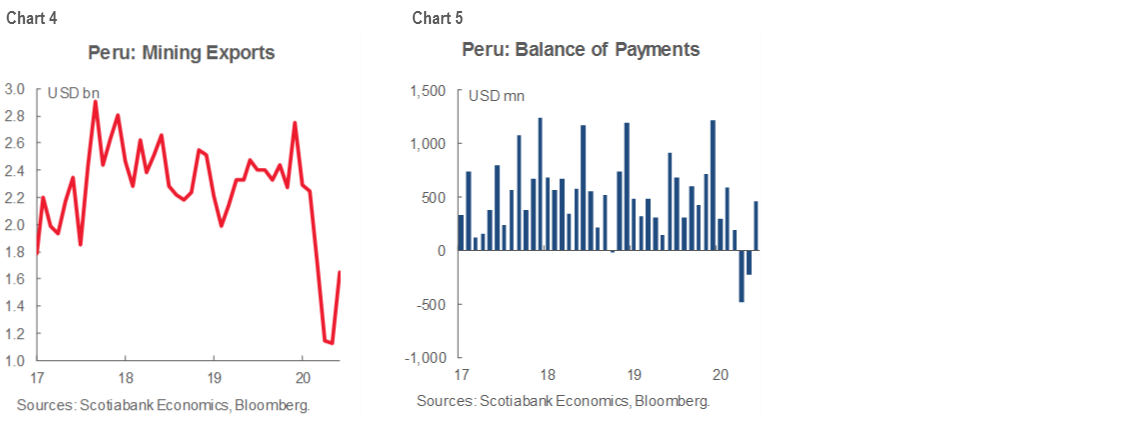

The Peruvian sol (PEN) has been among the most stable currencies in Latam in recent years. Throughout the worst of the financial turmoil that was triggered by the COVID-19 pandemic, PEN remained more resilient and performed better than its EM peers (chart 1). Starting in May, however, as other currencies began to recover, PEN decoupled from the region and started a depreciation trend that has left it as the second worst performer in the last four months, behind only ARS, which went through a dramatic debt restructuring process during this period (chart 2). PEN has moved away from the ranges it has seen in the last couple of years and is currently fluctuating around its all-time low of 3.5847/USD (chart 3).

Looking into the reasons that might explain the recent behaviour of PEN, we identified three specific disruptions in the supply-demand balance in the FX market that have put pressure on the currency and that are mostly driven by the implementation of local policies to respond to the COVID crisis. We describe those reasons below and why we think the pressure on the currency might fade in the short term.

A POSSIBLE TRINITY OF POINTS FOR APPRECIATION

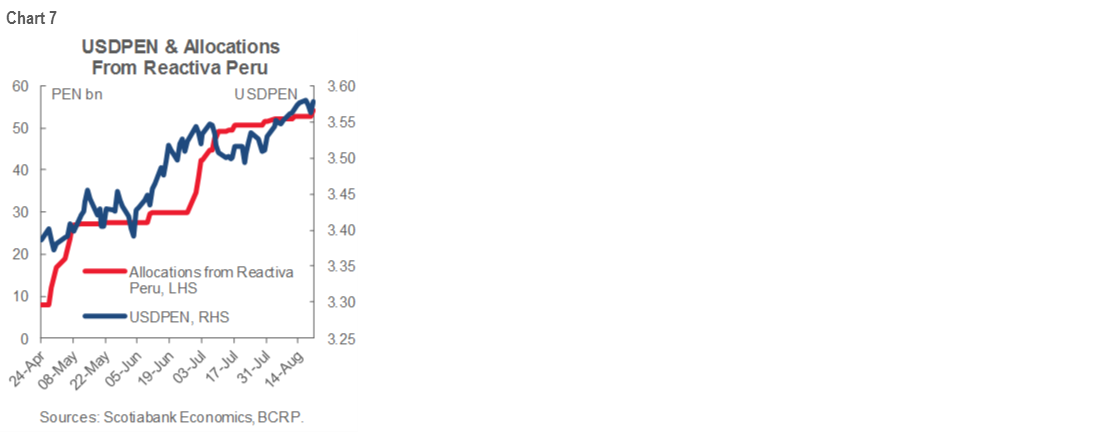

1. Decrease in USD supply as a result of the interruption of activities in the mining sector. The mining sector is the most important source of USD inflows in Peru, accounting for 60% of the total exports. From March 15, when the nationwide lockdown started, the mining industry reduced its activity significantly, resulting in a decrease of USD available in the market.

The Peruvian mining industry contracted by -42.3% y/y in April 2020, which marked the bottom of the cycle. But some sub-sectors such as the production of tin and iron stopped completely and others were working at minimum capacity—with zinc production falling by 86.3%, lead by 84.1%, silver by 73.6% and gold by 53.5%. The production of copper, which was the most resilient, fell by “only” 34.7%. As a result of this, we saw a deterioration in the balance of payments in March, April and May.

We are expecting a reversal of this effect and an increase in USD supply from the mining sector, which is gradually returning to full capacity and has also benefited from the strength of copper and gold prices. In line with the recovery of the mining sector, we also expect a turnaround in the trade balance which, after two consecutive months of deficit, went back to a small surplus in June that will likely consolidate in the coming months (chart 4 & 5).

2. Increase in USD demand from the local corporate sector. One of the flagship aid programs of the Peruvian government during the pandemic was the allocation of guaranteed PEN credits to local corporates to help them meet their short-term obligations despite the fall in income that would result from the collapse in consumption and economic activity. The program started with a target of PEN 30 bn and was extended to PEN 60 bn in credits. Given the high level of dollarization of the Peruvian economy (chart 6), a large portion of these loans in local currency hit the FX market to be exchanged for USD. According to the Central Bank, up until August 12, PEN 51 bn of the total amount had been delivered to commercial banks and, from that, about PEN 40 bn has reached Peruvian corporates. There is no official data on the exact volumes in the FX market, but our local trading desk estimates that about PEN 6 bn (15% of the allocated credits) were used to buy USD. That volume becomes more relevant if we consider that the COVID-19 crisis triggered a significant fall in the daily spot volume, which went from PEN 450 mn to about PEN 250 mn according to our estimates.

Going forward, we also think that this temporary distortion on the demand side will fade. Local banks seem to be struggling to allocate the remaining funds—probably because the number of corporates that can meet the stringent requirements for these credits already received their share, and the sense of urgency to get funds is lower as the economy starts to re-open. On the political side, we also think that the probability of an extension of the program is low as it has recently been criticized by the Congress and has gotten little popular support because it is seen as biased to help larger-sized corporations. From here, we think the government will likely focus any additional resources to help the lower income/informal sector of the population.

3. The central bank was less active in the FX market during the move towards USDPEN 3.58. The BCRP has been absent from the spot market since May and did not roll all its maturities of FX swaps during May, June and July, resulting in a net demand for USD, which did not help to tame the depreciation trend (table 1).

We think the BCRP will likely start to be more active in the FX market. Being a highly dollarized economy, a rapid weakening of the currency flows through into the real economy and popular perception very quickly. We think the central bank will try to prevent a move above 3.60 in USDPEN to avoid the negative economic impact, and the activity we have seen in the last couple of weeks seems to be going in that direction.

Another important consideration that serves as evidence that the disbalance is coming from local sources is the stability of the forward points (chart 7). The fact that PEN demand from offshore accounts has been resilient is consistent with our view that, once the local disruptions fade, we should see a rally in the currency.

Finally, the risk of Congress passing another bill allowing further withdrawals from the pension system is high and would probably result in additional USD supply from the liquidation of foreign assets, helping our case for a stronger PEN. We do not have data on the composition of the liquidations that resulted from the first bill on this matter, but we estimate that about PEN 25 bn were withdrawn from the system and that up to 50% of that liquidity might have come from sales of USD assets (from a broad comparison of the portfolio composition in February and July 2020). The new bill could result in withdrawals of about PEN 20 bn, in our view, (although there are estimates as high as PEN 60 bn) and—even with the central bank repo facility in place—we do see liquidation of USD-denominated assets hitting the market as a result of the new legislation.

CONCLUSION

As the sources of the local imbalance of supply and demand in the FX market dissipate, we expect USDPEN to start a downward trend to the 3.45 we project for year-end 2020 and, hence, think that there is value in PEN at current levels.

RISKS TO THE VIEW

If the fall in consumer and business confidence amid the deep economic contraction and the spike in political uncertainty turns into a more permanent increase in local demand for USD in Peru, we could see slower correction in USDPEN from potentially higher levels.

COUNTRY UPDATES

Argentina—Now for the Hard Part

Brett House, VP & Deputy Chief Economist

416.863.7463

brett.house@scotiabank.com

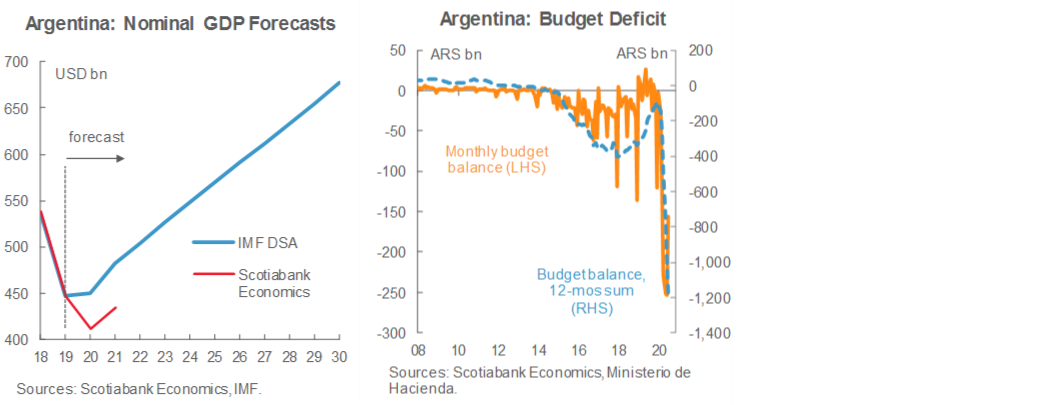

The next two weeks mark the end of the beginning for Argentina’s economic stabilization process. The extended deadline for expressions of commitment to join Argentina’s external debt swap falls at 5pm on Friday, August 28, with execution and settlement still planned for one week later on Friday, September 4. Given that three major bondholder groups and some smaller creditors are already on board, we see no doubt that participation will exceed the minimum thresholds that the authorities have set for the exchange to go forward. The domestic debt exchange will remain open until September 15. Despite all the challenges embodied in four months of negotiations with bondholders, the really tough steps to ensure Argentina’s solvency still lie ahead.

The IMF’s 2020 debt-sustainability analysis (DSA) laid out a need for between USD 55 bn and USD 85 bn in debt relief over the next decade and further work is required to obtain a financial framework under which these amounts would be adequate. The IMF staff’s technical note explained that, “The lower end of this cash-flow relief is associated with a scenario that assumes more advantageous funding conditions to meet payments due to the Fund and other official creditors.”. The external debt swap will provide about USD 42 bn in debt relief over the coming decade, while the domestic swap should add another USD 20 bn in relief, for a total of USD 62 bn—inside the bottom of the IMF DSA’s range, but the conditions consistent with this range haven’t yet been secured. Nominal GDP is coming in substantially below the DSA’s forecasts and federal deficits are substantially wider than the DSA expected (charts). Argentina is nowhere close to a return to international capital markets to make up the difference.

As a result, negotiations with the IMF will likely target financing even larger than roughly USD 44 bn (9.5% GDP) currently outstanding to the Fund. This would allow Argentina to roll over this entire amount, extend its grace period by about three years, and push principal payments now set to fall due from 2021 out beyond 2024. In return, IMF conditionalities are set to focus on reforms to the fiscal framework, price controls, capital controls, and monetary policy.

Looking at the next two weeks, retail sales numbers on Monday, August 24, will round out June’s monthly data prints. While supermarket sales growth is likely to hold at around 5% above year-ago levels, shopping-centre sales are a bit more of a wildcard: after a dismal May in which sales were down about 96% y/y, activity surely rose in June, but by how much is unclear since some quarantine measures were eased in June, some lifted, and then re-imposed, and some were simply extended through the month. July trade data out on Tuesday, August 25 isn’t likely to tell us much new on the export front, but import numbers could provide some early insight on the extent to which demand remained depressed as Q3 got under way. Industrial production and construction activity data for July, and auto-sector numbers for August, all due to be released on Thursday, September 3, account for about a quarter of GDP and should show monthly values converging back to just below 2019’s already-depressed levels.

Brazil—Political Hurdles to Fiscal Adjustments not Dead After All

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

At the start of the week, this commentary on Brazil was going to focus on how Bolsonaro’s rising popularity, the fast rebound in economic activity, and a seeming improvement of executive-legislative relations suggested that fiscal adjustment approvals would be a smooth process. On August 19, that view took a hit when President Bolsonaro’s veto to freeze public worker wages was overturned by the Senate. The veto was ultimately upheld by the Lower House the next day, but the standstill came close to costing Paulo Guedes’ adjustment plans close to 1% of GDP in 2021. More importantly, the more-arduous-than-expected battle highlighted the difficult politics of spending cuts.

Behavioural scientists use the concept of loss aversion to explain a type of human decision-making where preferences are not symmetric around an event. People give a greater priority to avoiding a loss over making a gain, even when these two represent a similar change in wellbeing. Essentially, people are unwilling of let go of what they perceive to be theirs, or their right.

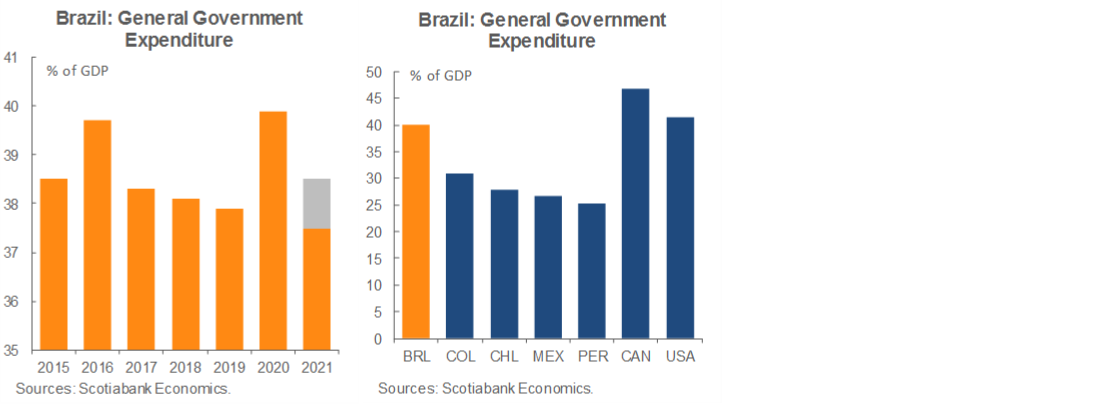

Loss aversion is one of the reasons why expenditure cuts are so difficult to implement—voters don’t like entitlement cuts. The Brazilian government spends a much higher share of GDP than what we see in most of the larger LATAM economies and is closer to the US or Canada in that regard than to its regional peers. In an economy where the government is already large, and which is struggling to kick-start growth, the solution to fiscal problems should focus on cutting public spending rather than increasing taxes. This is especially true in Brazil, where a large government hasn’t achieved particularly strong results in infrastructure quality, education, or growth.

This likely means a very tough political road ahead to bring the country’s fiscal stance back to a sustainable path. The pricing-in of this rough and uneven adjustment process is likely among the reasons for a relatively poor performance for the Bovespa (-12.3% YTD) and also why the BRL is the worst performing major global currency (-27.5% YTD), by a margin of 1.5:1 relative to the second worst performer.

Chile—GDP Falls -14.1% y/y in Q2-2020, Consumption Decreased the Most

Jorge Selaive, Chief Economist, Chile

56.2.2939.1092 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

On Tuesday, August 18, National Accounts data were released, showing a GDP contraction of -14.1% y/y in the second quarter of this year. This result was clearly influenced by the health crisis and quarantine caused by COVID-19, which prevented the normal mobility of people and the usual performance of productive activities. On the supply side, the most affected activities were personal services, commerce, construction, restaurants & hotels, manufacturing and business services. Mining was the only activity with positive figures for the quarter, although its momentum slowed from Q1. On the demand side, private consumption was the most affected, declining -22.4% y/y. Lower import demand and resilient mining exports helped net exports offset other drags on GDP.

The Q2 GDP data confirm our view that the Chilean economy will see a maximum contraction of -6% y/y in 2020 followed by an expansion of around 4.5% y/y in 2021. Although Q2 represented the bottom for GDP in this cycle, June economic activity showed positive seasonally adjusted growth of 0.8% m/m. For July, we anticipate a seasonally adjusted expansion of 5% m/m while, for August, the strong injection of liquidity provided by government aid to the middle class in conjunction with the withdrawal of funds from the AFPs should lead to further seasonally adjusted growth. According to our high-frequency indicators, total purchases with debit/credit cards show a significant/astonishing rebound up to August 12 after only USD 6.7 bn (out of around USD 20 bn) had been delivered by Pension Funds to pension members’ accounts. As expected, we observe strong heterogeneity: retailers and supermarkets are receiving most of the liquidity.

The calendar is full of tier-1 indicators coming out in the following weeks. On August 28 we will know the employment figures for July, and on August 31, sectoral data will be released. We estimate retail sales will show a drop of around -20% y/y in July, while August will reveal in its fullness the withdrawal of pension funds that will contribute "at least" 10 ppts to retail sales that month. Regarding the withdrawal of pension funds, up until August 18, more than 9 mn people have requested a withdrawal, and 7.2 mn have received part of their funds. In total, around USD 10 bn have been paid to pension fund contributors, and we anticipate more transfers in the following days. Finally, monthly GDP for July will be known on September 1, where we expect a contraction around -11% y/y. That same day, the central bank will hold its September meeting, where we expect some discussion about the revision of the technical minimum, currently at 0.5%.

Colombia—April was the Economic Bottom; the Recovery Now Depends on Regional Mandates

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@co.scotiabank.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@co.scotiabank.com

Colombian GDP contracted by -15.7% y/y in Q2-2020, the worst performance in recent history. Although the figure is very concerning, there were no surprises around the result. The COVID-19 / oil prices shock froze economic activity in the second quarter and put the handbrake on a solid recovery that started last year. However, “this time is a bit different” because the crisis was not triggered by a confidence shock or concern regarding policies. This crisis resulted from a very strong supply shock that was exacerbated by a demand shock due to the general lockdown in the economy.

That said, economic recovery is taking place as the government allows more sectors to open. The monthly economic indicator—ISE—has shown that the bottom for economic activity occurred in April when the quarantine measures blocked more than 30% of the economy. Since then, as lockdown measures were lifted, the economy has gained momentum. However, it is worth saying that although the current crisis does not have its origins in traditional sources, the duration of the lockdown measures is increasing permanent effects on the demand side, and it will make the recovery more difficult.

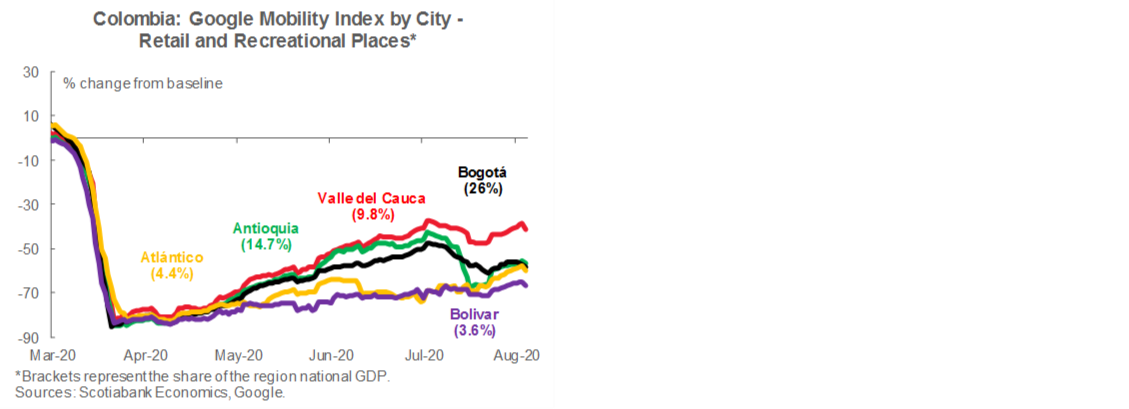

By the end of August, Colombia will have completed more than five months under isolation measures and—although Central Government Decrees have allowed the opening of somewhat more than 90% of economic activities—the execution of this unlocking is not the same across all regions. The implementation of those plans is the responsibility of regional government leaders. One special case is the capital city, Bogota, which since July 13 has implemented strict quarantines by neighborhood groups and now is considered the part of the country with the strictest measures and the highest economic cost. Unfortunately, Bogota is still far from showing a stabilization of the pandemic spread. That said, economic activity recovery in Colombia has been unequal by regions and the service sectors are the most affected. Employment has fallen -20% compared with pre-COVID levels, while labour income has fallen by -1.5% of GDP. Both are facts to keep an eye on since, if the demand weakens more, the production side of the economy has limited room to improve.

Extended quarantines in the capital cities are the main challenge for economic recovery. However, this week commercial flight pilot programs have begun, and it has been announced that in September activity would begin to normalize in Bogota, under an alternation scheme where some businesses and activities are open during the week and others on weekends. This will allow the majority of activities, including some social activities, to operate on a reduced schedule. This news constitutes more green shoots for the economy’s future.

All in all, our GDP forecast for 2020 remains at -7.5%, but positive surprises may arise if re-opening plans accelerate. This scenario is compatible with an expectation of a rate cut of 25 bps at the August 31 Monetary Policy Meeting. Further cuts could take place if economic recovery shows negative surprises, but it is not our base case scenario.

Over the next weeks, the macroeconomic calendar has the release of unemployment figures for July—the month when regional autonomy on lockdown measures started. Additionally, we expect the current account for Q2 (to be published on September 1) will narrow since a contraction in imports offset the plunge in exports in real terms according to the last GDP results, while other accounts such as remittances remained relatively strong.

Mexico—Is Banxico’s Job Done?

Mario Correa, Economic Research Director

52.55.5123.2683 (Mexico)

mcorrea@scotiacb.com.mx

In the most relevant event for financial markets, Banco de México recently cut its reference interest rate by -50 bps, as expected by most analysts, to 4.50%, but this time the decision was not unanimous, since one board member voted for a -25 bps reduction. Most of the press release was as expected, with the balance of risks for economic activity biased to the downside and no explicit bias for the balance of risks for inflation. There was, however, something new: “Going forward, available space [to cut again] will depend on the evolution of factors that affect inflation perspectives and its expectations, including the effect that the pandemic could have on both.” After this last cut, we believe the easing cycle has ended from the policy-making point of view, even though a new cut could take place if politics dominates. The following reasons lead us to this conclusion:

· Inflation behaviour. Despite the huge drop in demand and widening of the output gap, inflation is on the rise, affected by some factors—such as energy prices—outside the influence of monetary policy. Rising inflation is not comfortable for a central bank with a clear unequivocal mandate of price stability. Especially concerning is core inflation because it has not only remained stubbornly high above 3.5%, but is on the rise, reaching more than 3.8% y/y recently. It is true that the food-merchandise component explains a lot of core inflation’s recent rise for short-term factors, but in July the non-food merchandise also increased notably, +0.70%. It is likely that in the next couple of months, inflation will keep climbing in its y/y readings, even surpassing the 4.0% threshold of the acceptable range, making it advisable to adopt a more prudent stance and take a pause.

· Is not clear if the benefits of easing outweigh the risks. After a rapid reduction of 375 basis points in the reference rate, Banxico has done its job to provide some relief to households, firms and the government, and prevent a credit crunch in financial markets. The reference interest rate has now reached the same level at which the easing cycle that followed the global financial crisis of 2009 stopped for a long pause, after which there was some more easing in 2013 (see graph). At that time, core inflation was below 3% and descending, remaining below 3% and even close to 2% for a couple of years, while it is now rising and causing some concern.

· Real interest rates are now below neutral and rapidly approaching zero. As a consequence of the rapid reduction in the nominal reference rate, but also because inflation is rising, the real interest rate is falling rapidly (see graph), not only below the range Banco de México has defined as neutral, but hastily approaching zero. Many market participants have noted that high real interest rates in Mexico provide some relative attractiveness when compared to some similar markets, and hence there was space for easing the monetary stance. That space is closing.

· Public finances deterioration implies higher responsibility for Banxico. Macroeconomic stability, which is perhaps the main asset of the Mexican economy, is built on top of two pillars: fiscal discipline and monetary prudence. With the fiscal pillar weakening, the monetary pillar becomes more important, having to support a heavier burden. There are many concerning signals coming from public finances: the original primary balance target for 2020 was a surplus of 0.7% of GDP, in April this was changed to a deficit of -0.4% of GDP, and recently to a deficit of -0.6% of GDP. The primary balance is considered one of the best indicators of fiscal discipline, and it is loosening. The broadest definition of public debt—the balance for public sector borrowing requirements—which was not supposed to increase, will leap more than 10 percentage points of GDP, increasing to 55.4% of GDP in 2020 from 44.8% of GDP in 2019 according to the new estimates of Hacienda. If the public finances are weakening considerably, then macroeconomic stability will depend largely on the monetary policy as the last effective anchor, making the case for a more prudent approach and leaving the reference interest rate at its current low level for some time.

Turning to the other indicators recently released, formal jobs as measured by persons insured by the Mexican Social Security Institute (IMMS) fell by 3,907 in July, accumulating 1.118 million jobs lost in April-July. The open unemployment rate leapt to 5.5% in June from 4.2% in May, its highest level since 2011. These numbers reflect only partially the harsh reality of the labour market conditions in Mexico and the cloudy horizon for job recovery in the near future.

Industrial activity grew 17.9% real m/m in June using seasonally adjusted figures, which represents good news that reveals recovery is on its way. However, these figures should be taken cautiously, since we are still 17.5% below the level reached a year ago.

Consumer confidence improved slightly—to 34.4 points in July from 32.0 in June—but remained well below the threshold of 50 points, meaning consumers remain gloomy about the present situation and the next twelve months.

Finally, retail sales presented some improvement in June, growing 7.8% m/m, but remained 16.6% below the level reached twelve months ago. Wholesale sales grew 11.1% m/m, 12.8% below a year ago.

For the coming weeks, we will receive a great deal of new and relevant information. On the economic indicators front, we will have inflation for the first half of August, which will be a key input for coming monetary policy decisions. For the month of July, we will learn the unemployment rate, trade balance, public finances, and financial activity—all of which will help us form a better idea about the strength and pace of the economic recovery after the reopening of economic activities. For Q2, we will receive detailed figures of GDP and the balance of payments numbers. We will also have the quarterly report from Banco de México, where they will show their new forecasts for inflation and economic activity, their minutes of the last monetary policy decision, and the results of the latest survey among private sector economists. And finally, no later than September 8, the so-called “economic package”, defining the fiscal policy for 2021, will be released by Hacienda. This is one of the key ingredients used to revise the economic forecasts for the year ahead.

Peru—An Improving Economy, and a World of Concerns

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

Peruvian growth indicators released this week were mixed, but in general pointed to an improving economy, even as both COVID-19 contagion and political noise continue unabated.

GDP growth contracted -18% in June in y/y terms which, however, represented a 20% rebound in m/m terms. Early July-August figures are even more interesting. Electricity demand has gone from a -30% y/y contraction during the lockdown back to nearly pre-COVID-19 levels in mid-August. Cement demand, which was almost nil in April, was less than 5% off y/y levels in July. Fishing GDP will have another stellar month in July to match its 48% y/y growth of June, and copper output, down only -9% y/y in June, could well have recovered fully in July. Overall, our forecast is that GDP in July will be down -8% to -10% in y/y terms, halving the contraction that took place in June which, in turn, was well off the -40% contraction during April—the floor of the downturn.

Nevertheless, the rebound continues to leave the economy uncomfortably below pre-COVID-19 levels. One of the main factors hampering a stronger recovery has been the government itself. Public sector investment fell -50% y/y in July, a much too small improvement over -70% y/y contractions in April to June.

Employment also continues to be a concern. Unemployment in Lima rose to 16.4% in the May-July period (official unemployment data is given as a three-month rolling average). Despite a 34% m/m jump, jobs were still down 40% in y/y terms.

Meanwhile, the PEN has continued to weaken, in contrast to other regional currencies. The recent rise led the USDPEN rate to match its record high at 3.58. Given a weak USD globally, strong metal prices, and quiescent offshore capital flows, the cause is clearly domestic, and most likely linked to the tremendous increase in PEN liquidity. In Peru’s dual currency business environment, such a strong inflow of PEN liquidity has led to a net de-dollarization of business assets, leading many businesses to seek to return to equilibrium through the purchase of USD. It’s hard to tell when this process will end, and how high the PEN will go before it does.

Politics has remained as noisy as ever. Congress continued to push a law allowing for up to 100% of withdrawals for those who have been out of work due to or preceding the COVID-19 crisis. The issue could be voted on at any moment. The Bank Superintendent, which also oversees pension funds, has estimated that withdrawals could reach nearly 14% of assets under management.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | pirajaj@colptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including, Scotiabanc Inc.; Citadel Hill Advisors L.L.C.; The Bank of Nova Scotia Trust Company of New York; Scotiabank Europe plc; Scotiabank (Ireland) Limited; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Scotia Inverlat Casa de Bolsa S.A. de C.V., Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorised by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V., and Scotia Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.