ECONOMIC OVERVIEW

- Markets just had one of their best weeks in a while, as key risk events fell short of what was feared, seeing sizable gains in global equity benchmarks, alongside a massive rally in rates markets—not just in the US, but also in Latam—and a broadly weaker USD. There’s still a lot of lost ground left to recover in markets, and risks abound, but at least next week should be quiet—outside of Latam, at least.

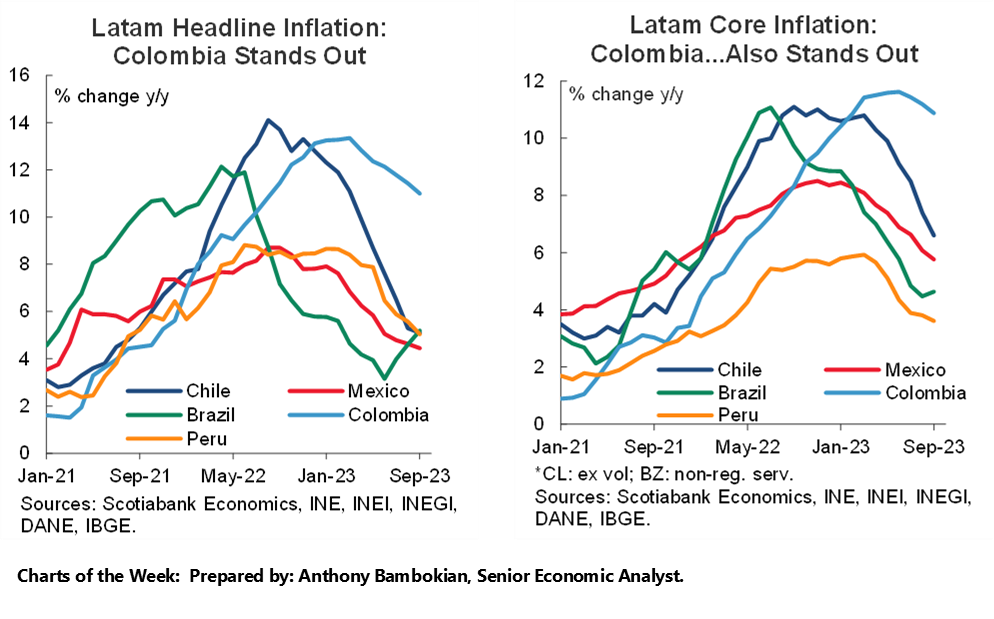

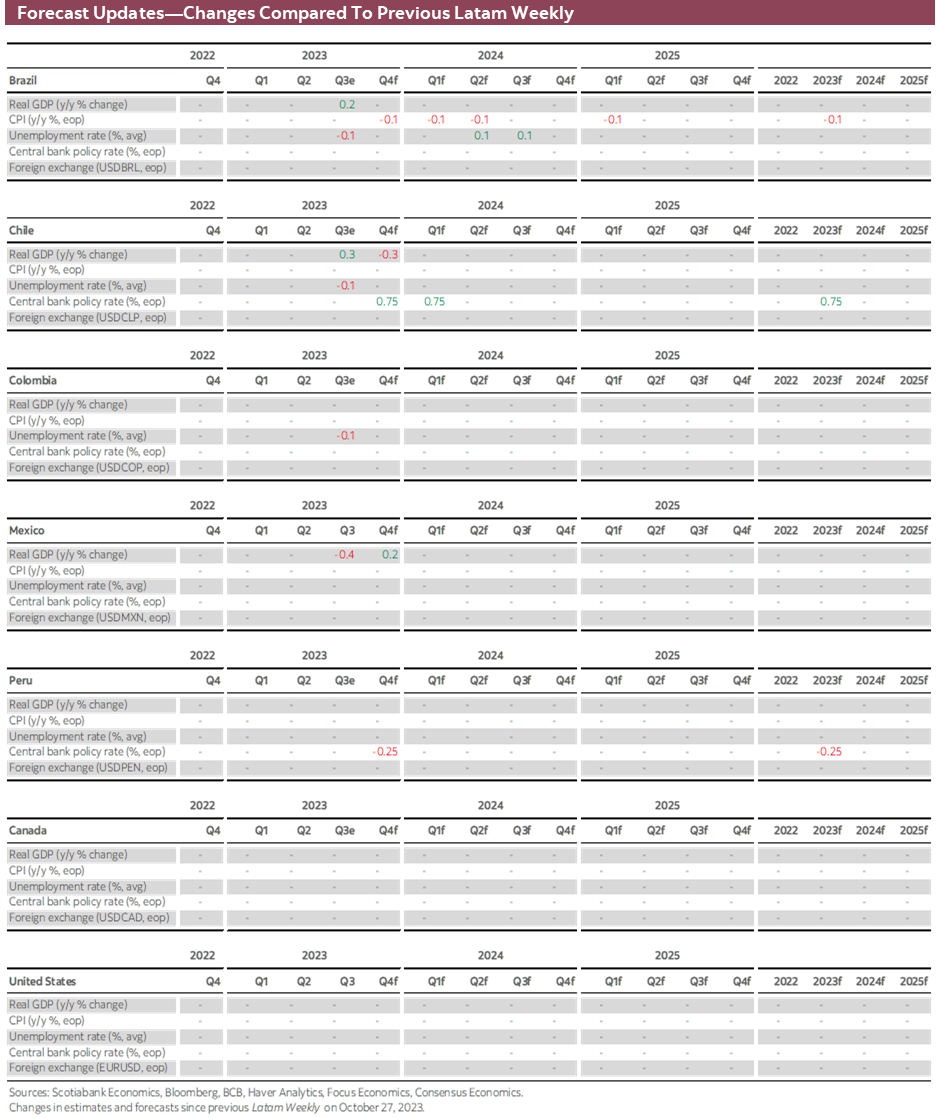

- Chile, Colombia, Mexico, and Brazil all publish October inflation data over the coming days. But, maybe these releases will not be as impactful as they normally would be. Central banks from each of these countries will have one additional prices print between now and their last meeting of the year, in December.

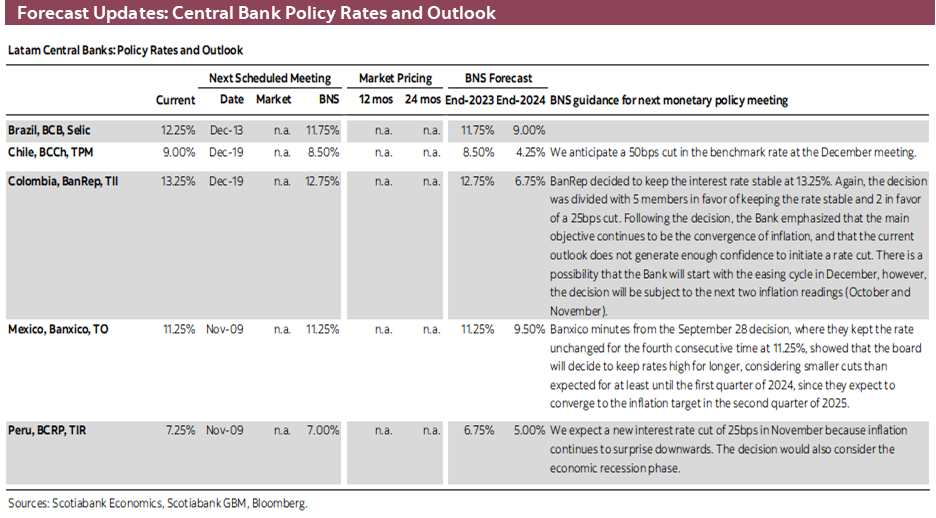

- Peru’s central bank is the last in the region to decide on policy in this late-Oct/early-Nov meetings round. It will also have inflation data at hand, which came out a few days ago and greatly undershot expectations. Our team expects a 25bps cut next week, to be followed by an equal-sized reduction in December.

- Banxico’s rate announcement should again be a mostly uneventful placeholder. Not enough has changed in inflation or economic activity terms since the bank’s latest meeting in September that would warrant a guidance change. In today’s report, our Mexico economists focus on next year's elections and two key things that markets may pay attention to most closely: energy supply and fiscal policy.

- Our economists in Colombia set aside a discussion of next week’s CPI data and instead give their take on last week’s regional elections. Overall, political power shifted towards the centre-right and Petro-adjacent candidates performed poorly. We’ll see now how this shift impacts reforms discussions.

- Chilean year-on-year inflation is seen little changed by our team in Santiago as base effects mask a normalisation of month-on-month price increases. We’ll also watch developments on the constitutional re-write front, as President Boric may in the next few days call the December 17th referendum on the final text.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

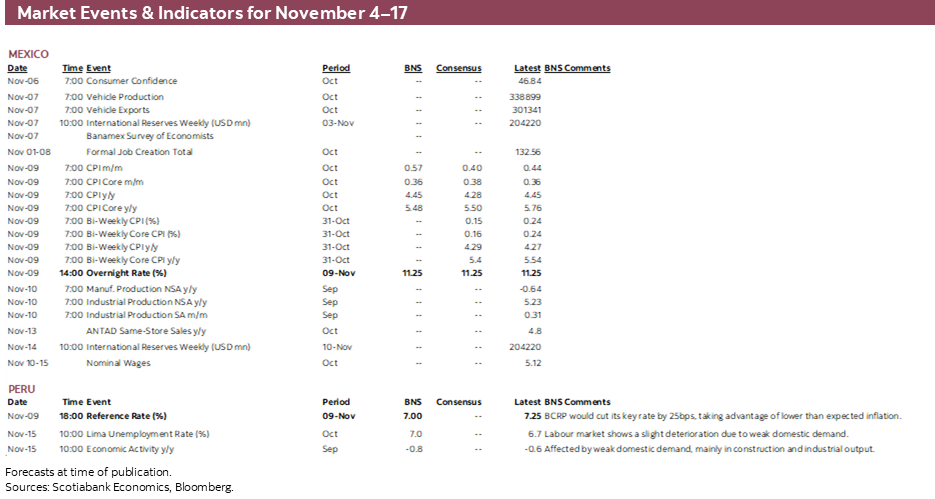

MARKET EVENTS & INDICATORS

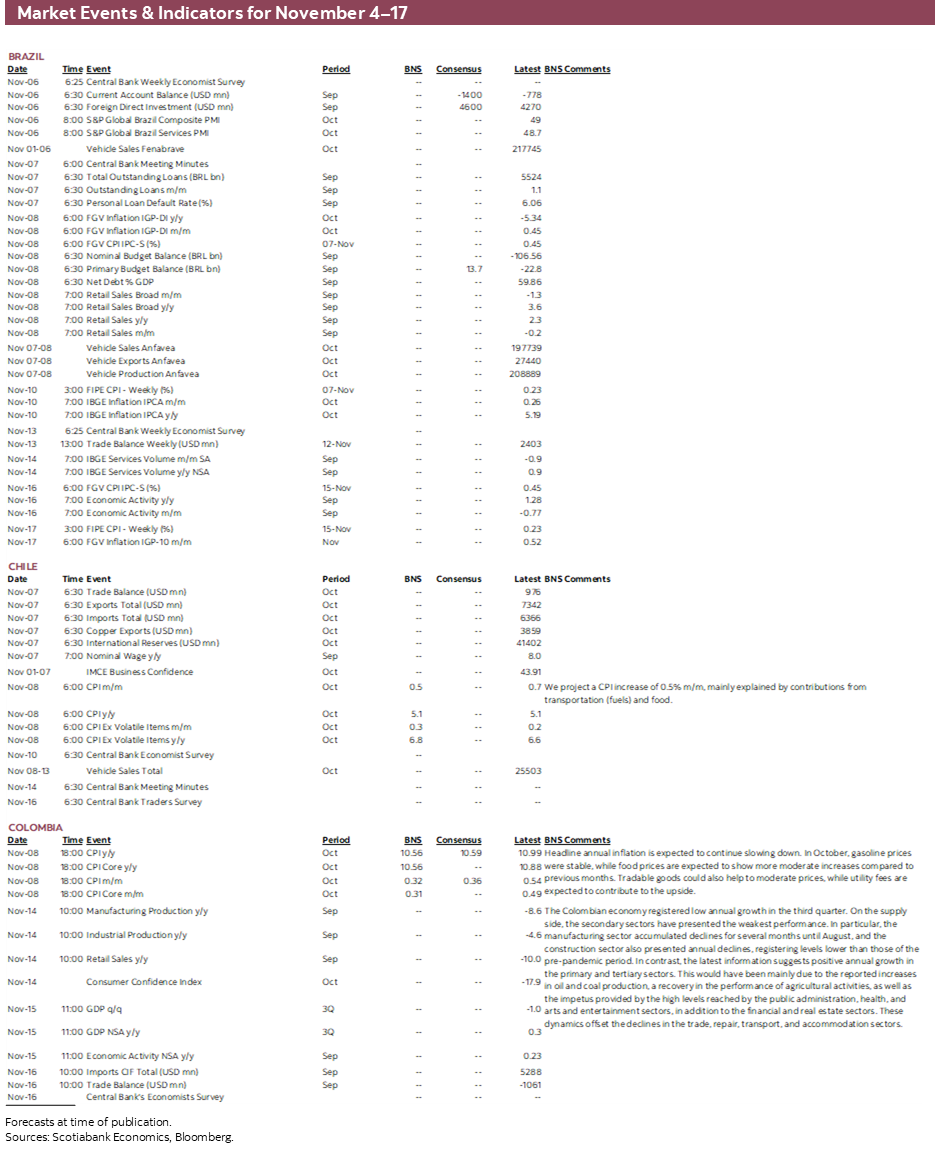

- A comprehensive risk calendar with selected highlights for the period November 4–17 across the Pacific Alliance countries and Brazil.

Charts of the Week

ECONOMIC OVERVIEW: REGIONAL INFLATION; BCRP, BANXICO

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Markets just had one of their best weeks in a while, as key risk events fell short of what was feared, seeing sizable gains in global equity benchmarks, alongside a massive rally in rates markets—not just in the US, but also in Latam—and a broadly weaker USD. There’s still a lot of lost ground left to recover in markets, and risks abound, but at least next week should be quiet—outside of Latam, at least.

- Chile, Colombia, Mexico, and Brazil all publish October inflation data over the coming days. But, maybe these releases will not be as impactful as they normally would be. Central banks from each of these countries will have one additional prices print between now and their last meeting of the year, in December.

- Peru’s central bank is the last in the region to decide on policy in this late-Oct/early-Nov meetings round. It will also have inflation data at hand, which came out a few days ago and greatly undershot expectations. Our team expects a 25bps cut next week, to be followed by an equal-sized reduction in December.

- Banxico’s rate announcement should again be a mostly uneventful placeholder. Not enough has changed in inflation or economic activity terms since the bank’s latest meeting in September that would warrant a guidance change. In today’s report, our Mexico economists focus on next year’s elections and two key things that markets may pay attention to most closely: energy supply and fiscal policy.

- Our economists in Colombia set aside a discussion of next week’s CPI data and instead give their take on last week’s regional elections. Overall, political power shifted towards the centre-right and Petro-adjacent candidates performed poorly. We’ll see now how this shift impacts reforms discussions.

- Chilean year-on-year inflation is seen little changed by our team in Santiago as base effects mask a normalisation of month-on-month price increases. We’ll also watch developments on the constitutional re-write front, as President Boric may in the next few days call the December 17th referendum on the final text.

Global markets have started the month strongly. The S&P500 is, at writing, on track for its greatest one-week gain in a year, above 5%. The Bloomberg dollar index’s ~1.2% decline is its largest since July. And, US 10s and 30s are tracking a 25-30bps+ fall in yields since Friday. There is still a lot of wood to chop, however. US 30yr yields remain around 85–90bps higher than their Q2-23 close—and broad UST liquidity remains very poor, as poor as during the regional banking crisis in March. The S&P500 is still about 5% below its close peak in late-July, and the Bloomberg dollar index is still in the range held since late-September.

High-risk events this week that had markets trading anxiously did not surprise, and in some cases delivered much more benign outcomes than expected. Specifically, the BoJ’s minor adjustment to YCC policy, an on-hold Fed that acknowledged the impact of the months-long surge in yields, a UST refunding announcement with smaller long-end supply than feared, and even a cautious BoE as well as markets better internalizing Middle East risks all helped support the risk mood in recent days.

Latam assets were no strangers to the positive mood outside of the region. Market-specific events may have resulted in an underperformance of some local bourses that failed to make much of the S&P 500’s gain since Friday—which was capitalized on more clearly by Mexican indices (BMV +5%). For instance, Chile’s IPSA is just barely managing to stay flat on the week, dragged by a 6/7% drop in SQM, the biggest name in the main index (firm-specific risks).

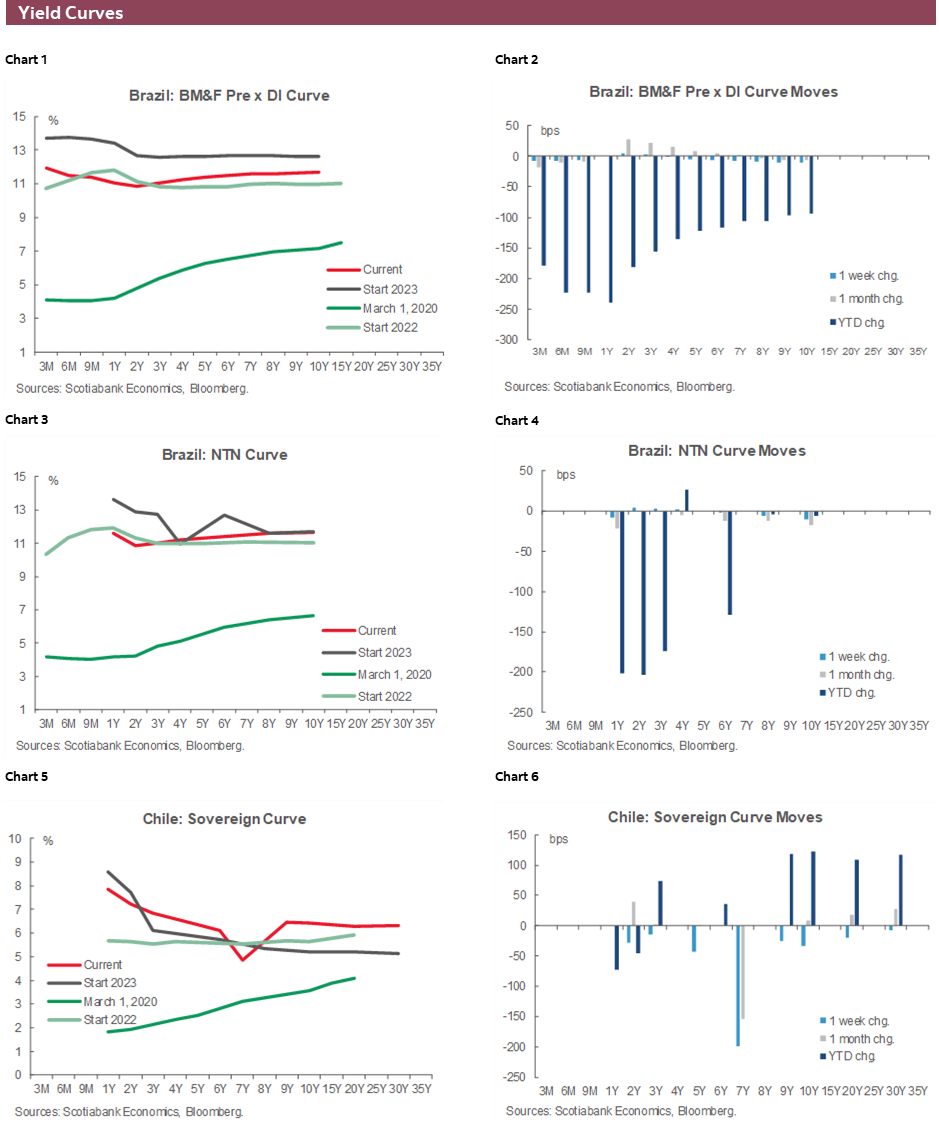

Long-end local rates markets also caught on to the UST positive mood in USTs—and then some in Colombia—but Brazil debt lagged its peers on fiscal concerns. Lula floating the possibility of not meeting Fin Min Haddad’s fiscal targets also meant the BRL underperformed in the region, but the real still rose above 2.5% on the week. This was far from the CLP’s near-6% gain which alongside the MXN (+4.5%), COP (+3.2%), and PEN (+3.0%) were four of the five best performing expanded major currencies this week.

Next week, the ex-Latam calendar is relatively quiet. In the US, the data slate is limited to Friday’s U Mich survey results; Thursday’s weekly jobless claims may be overlooked ahead of Fed Chairman Powell’s address that afternoon. Maybe US shutdown risks will be a bigger source of anxiety for markets as the current government funding extension lapses the following week. The BoJ’s October meeting summary of opinions due Friday is also a risk for long-end rates, while Chinese international trade and CPI could influence high-beta assets and commodities. The RBA’s decision and UK GDP round out the offshore week.

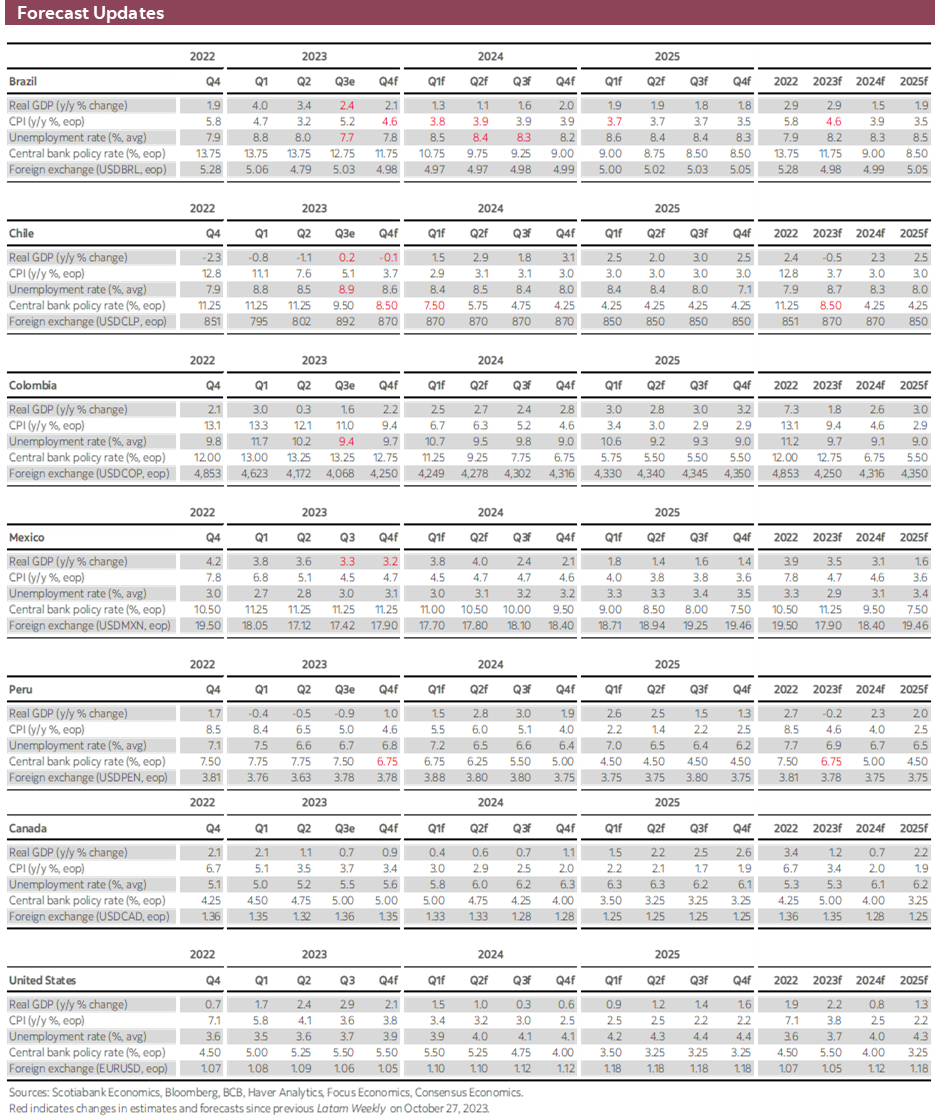

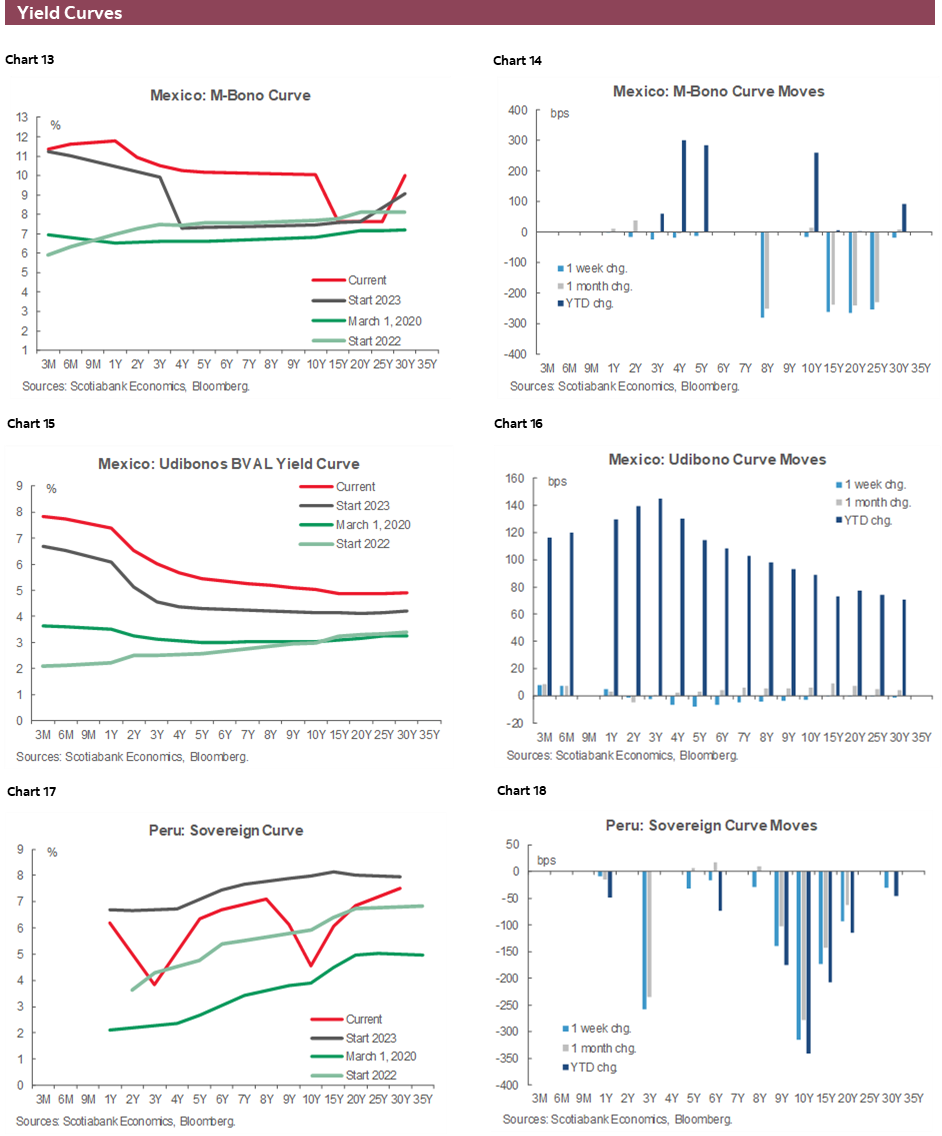

Chile, Colombia, Mexico, and Brazil will follow Peru next week with the release of October inflation data, while Peru’s BCRP will be the last in the region (just a few hours after Banxico) to decide on policy in this late-October/early-November announcements cycle. Peru’s CPI significantly missed to the downside (see our write up here) in data released on November 1st, which further reinforces the widely-shared view that the BCRP will cut 25bps again next week, to 7.00%. In today’s report, our team in Lima preview the bank’s decision, and change their call to a December cut from previously seeing a rate hold—which they now see in January.

Staying on the topic of central banks, Banxico’s rate announcement should again be a mostly uneventful placeholder. Partly because of this, our Mexico economists focus on next year’s elections and two key things that markets may pay attention to most closely: energy supply and fiscal policy. Back to Banxico, not enough has changed since the bank’s latest meeting in late-September to change their guidance. On the inflation front, data have been mixed or in-line. Meanwhile, economic activity remains strong with no signs of slowing rapidly—and remittances growing in September at their fastest pace since early-year (11.4% y/y) point to consumption strength continuing. So, Banxico’s announcement may be a bit of a dud, but depending on the bank’s hawkishness there may be more who push out their forecast for the first rate cut to Q2-24 instead of late-Q1. Inflation data published the morning of the announcement will not change expectations for Banxico, but economists expect a 0.2–0.3% slowdown in year-on-year headline and core inflation, with the latter only falling to the mid-5s.

Alike our team in Mexico, our economists in Colombia set aside a discussion of next week’s CPI data and instead give their take on last week’s regional elections. Overall, political power shifted towards the centre-right and Petro-adjacent candidates performed poorly. We’ll see now how this shift translates into political processes, namely reforms (health, pension, and labour). As for CPI data, it will continue to show double-digit inflation in both headline and core terms, standing as a clear reason for why BanRep may choose not to cut rates this year and instead wait until early-2023. Nevertheless, next week’s October data and November CPI data out on December 7th could tilt the decision either way; for now, the team maintains their December cut call. Note that Colombian markets are closed on Monday.

Chile’s inflation is seen little changed by our team in Santiago, at 5.1% y/y for headline and even rising a bit in the ex-volatiles basket to 6.8% from 6.6%. On the other hand, the 0.5% m/m rise in the headline basket (after 0.7% m/m in September) would mark a return to below historical averages. We’ll also watch developments on the constitutional re-write front, as President Boric may in the next few days call the December 17th referendum on the final text that was approved in late-October by the Constitutional Council. The latest polls see around half of Chileans are opposed to the proposal.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Call for Plebiscite and Inflation in October

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

WITH THE TEXT IN HAND, PRESIDENT BORIC SHOULD CALL FOR A PLEBISCITE IN THE NEXT FEW DAYS

On Monday, October 30th, the Constitutional Council approved the proposed new Constitution, with no supporting votes from any of the left-wing councilors. It will be submitted to a citizens’ referendum on December 17th in a mandatory vote.

Surveys reveal that the percentage of citizens who would vote against the constitutional proposal is higher than the segment of the population that wants to vote in favour. In the last Cadem poll (October 29th), the favourable share sat 34% of voters, compared to 51% of those polled who were opposed. As we have reiterated on other occasions in Scotiabank Economics (see our Latam Daily), our baseline scenario is that the new Constitution will be approved.

CORE M/M CPI INFLATION WILL RETURN TO BELOW ITS HISTORICAL AVERAGE

On Wednesday, November 8th, the statistical agency (INE) will release the October CPI, for which we project an increase of 0.5% m/m (5.1% y/y), in line with surveys. At the core (ex-volatile) level, we project a CPI of 0.3% m/m (6.8% y/y), explained by increases of the same magnitude in both goods and services. On the other hand, inflation of volatile items would stand at 0.9% m/m (2.3% y/y). By divisions, we project that the main positive impacts would come from transportation (0.17 ppts), food (0.11 ppts) and housing (0.09 ppts). By products, we highlight increases in gasoline, tourist packages and new cars.

Colombia—The Economic Side of Regional Elections and Monetary Policy Perspectives

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

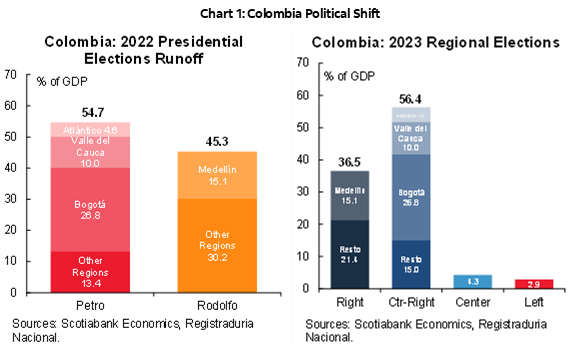

On Sunday, October 29th, Colombia’s elections reflected a change in the political sentiment among regions. It is worth noting that turnout was slightly lower vs previous elections, with 59.2% (~23 million voters) vs the 60.7% in 2019. However, the good news is that the election process was as usual: a broadly peaceful day, and a very fast count in which just two hours after ballots closed, we had most of the winners defined. President Petro highlighted that the election process reflects people’s sentiments and that that decision must be respected.

Now, the main question is if recent elections will materially impact the governability and how results may influence reform discussions and Government economic policy plans. In this piece, we will analyze some facts from Sunday’s vote, not only on the political front but in the economic scenario.

- Colombia doesn’t show radical changes in the political wing. Instead, most of the regions were tilted to the center-right.

Out of the 33 regions (including Bogotá as an independent region), only 3 voted for a leftist government, 4 voted for the center, 13 for center-right, and 13 for right. However, let’s make the same calculation using GDP. The center-right new governments represent 56,4% of Colombia’s GDP. In comparison, the far-right option represents 36.5% of GDP. Former results showed a strong contrast versus the runoff of presidential elections, in which President Petro received the support of 16 regions (including Bogotá), which accounted for 54.7% of GDP (chart 1).

It is worth noting that this change in the political side could be influenced by the deterioration in security, which benefited some elected leaders that showed a hard line in that regard during the campaign. However, in center-right options, businessmen dominated; it was the case of Barranquilla (Atlántico) and Cali (Valle del Cauca), which is good news for potential new real investments that could prevent Colombia from a deeper deceleration. It is worth noting that regions in which the right and center-right wings won are the most representative of manufacturing-related activities.

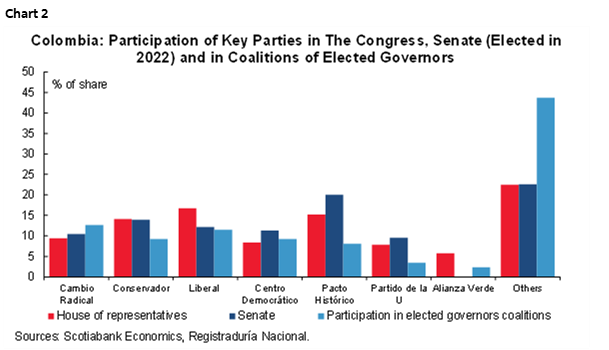

- Elections were characterized by coalitions. In the case of Governors for the 32 departments, 17 leaders formed alliances with different parties. When we add up the participation of traditional parties in those coalitions, it is noticeable that parties that initially were part of the Government’s coalition (Liberal, Conservador, de La U), lost steam compared to the opposition party Cambio Radical, which got a better participation (chart 2). Despite this, in our opinion, is not going to have immediate effects in Congress, it could motivate the increase of dialogues between the opposition and Government’s party since both have incentives to deliver results for the next four years; in the case of the Central Government, the incentive is delivering results for the country and in the case of Cambio Radical results for regions.

- What could happen with the Reform discussion? Traditional parties affirmed their relevance across regions, especially the opposition party Cambio Radical. In the 2022 Congress elections, the Government’s Party achieved relevant individual relevance; however, in regions, this relevance vanished, which increased the importance of negotiation. For now, there are three key reforms in the pipeline: Health, Pension, and Labour Reform. This week Health Reform resumed discussion, and despite around more than 40% of the initiative was approved before elections, parties are calling for negotiation more ahead of the rest of the pending debates. We don’t discard the possibility of the Government having a still very decent chance of passing a reform. However, the bill’s final approval could point to a very vanished initiative versus the initial proposal.

That said, the political front should not mean for now an increment in political risk premiums in Colombia; the result continued demonstrating that check and balances are still in place and that not only does the Government’s party has the incentive to negotiate, but also traditional parties need to deliver the result in regions and to achieve this, they need to negotiate a budget with the Government.

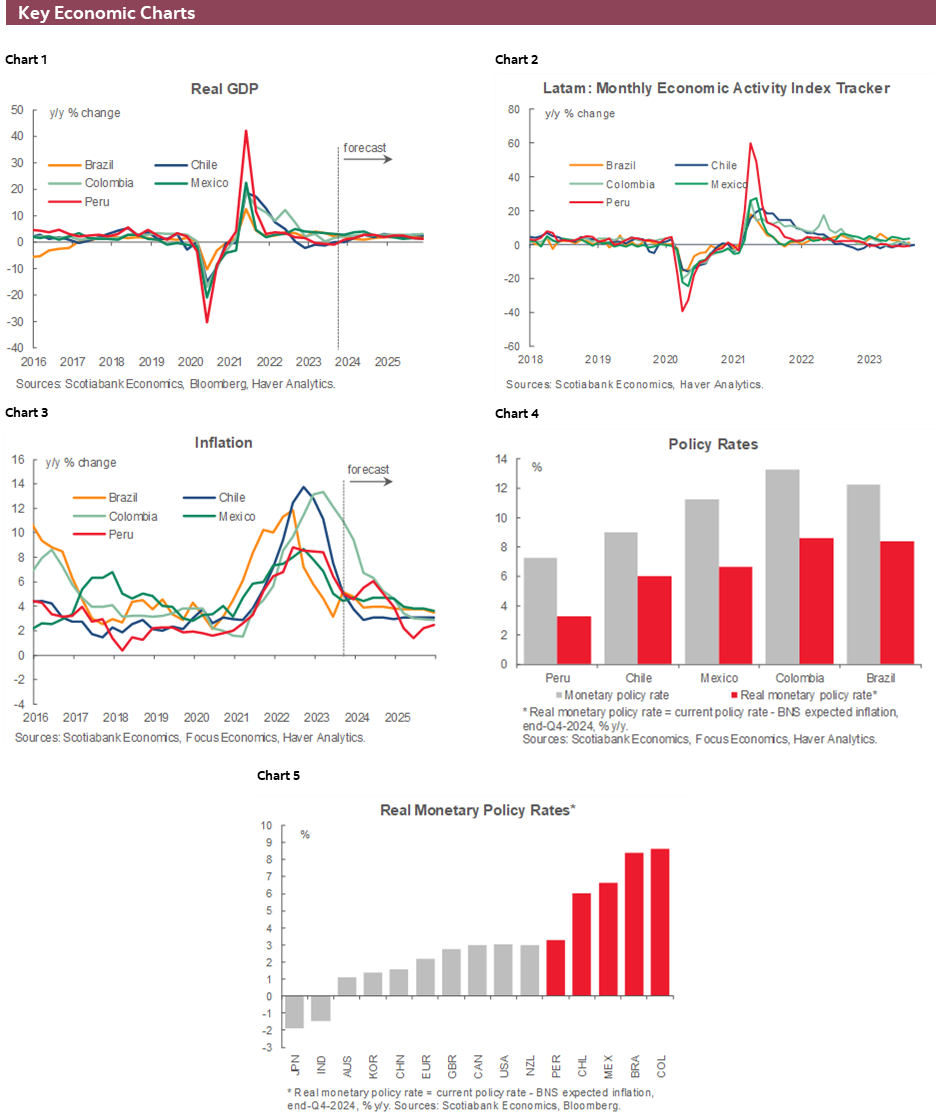

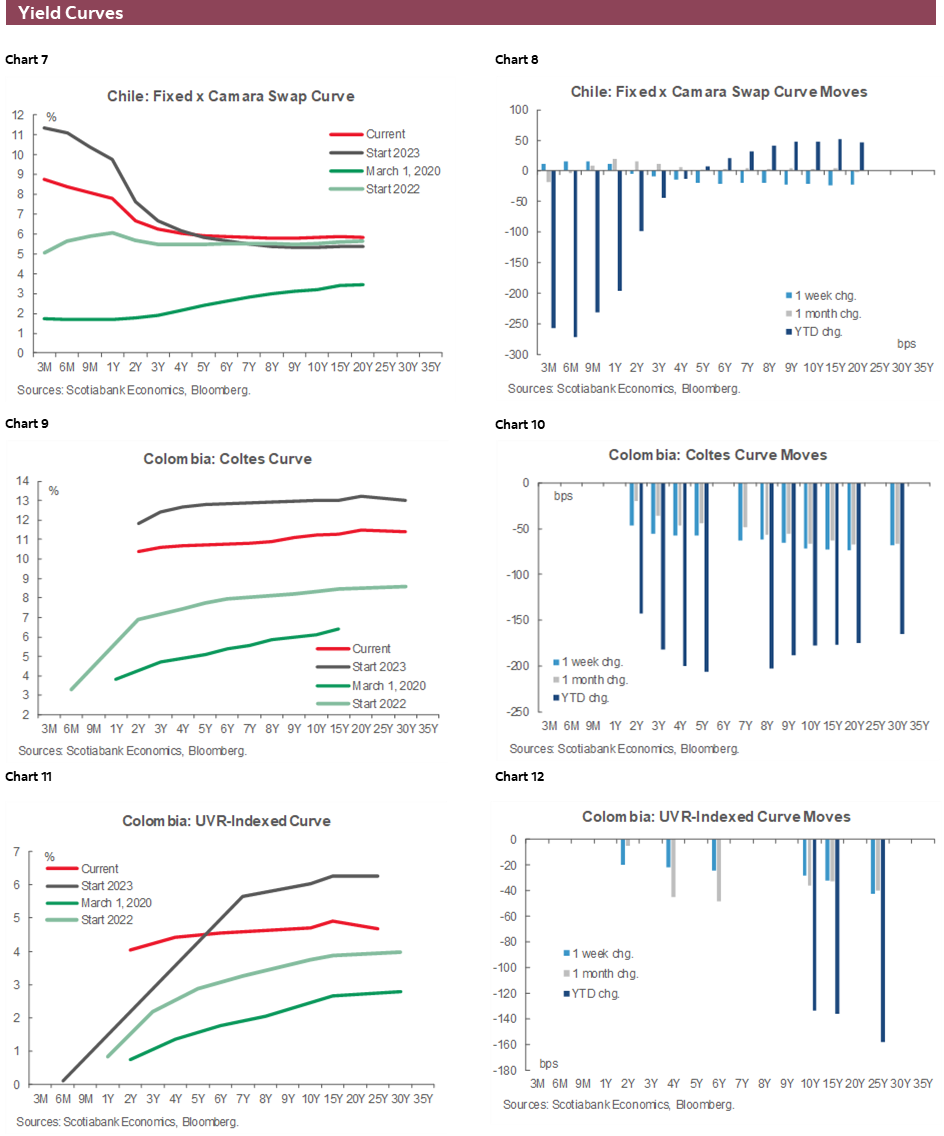

Beyond politics, the other relevant fundamental for Colombia is monetary policy. October’s meeting maintained a similar wording observed in September; the main concern is still inflation, while the assessment of the economic activity is of a weaker growth but a still-positive output gap. In that sense, the call for rate cuts is a close call between December and Q1-2024; we still favour a rate cut in December if core inflation continues decreasing and if the negotiations of the minimum wage point to a reasonable adjustment. For December 2024, the rate is expected at 6.75%, which means an average real rate (ex-ante or ex-post) of 2.9%, contractive vs. BanRep estimation of a neutral rate of 2.5%, however, international context remains a relevant issue for BanRep, since going against the tide could have huge side cost, for example in the FX.

Mexico—A Look Ahead to Mexico’s 2024 Election

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Mexico’s 2024 Elections could strongly shift the balance of power in the Mexican political system, due to how many officials will be elected, but it’s still too soon to know how the vote will turn out. The election will include the presidency, all the Senate (128 seats including direct and indirect representation) and the Lower House (500 seats including direct and indirect representation), as well as local legislatives, and 9 governors (out of 32). 1580 municipal governments as well as Mexico City’s 16th districts will also be up for election, alongside 31 local legislatives. The vote will be held on the first Sunday of June (June 2nd), and the new president will take office on October 1st, 2024.

At this stage, it appears that the main contenders for the presidency will be Clauda Sheinbaum (who was the Governor of Mexico City, and AMLO’s protégée) representing Morena’s coalition of parties, Xochitl Galvez, who is somewhat of an independent candidate (although she did hold posts with the PAN) representing the Frente Amplio coalition (which includes the center right PAN, the centrist PRI and the center left PRD), and whoever the MC party appoints as its standard bearer. The head of the MC has suggested his party’s potential candidates could be AMLO’s former Foreign Affairs Minister Marcelo Ebrard or the MCs governor of Nuevo Leon Samuel Garcia.

In terms of key dates in the process, the actual vote is the first Sunday of June 2024, while the new legislative and president will take over at different dates, as is usually the case (see below). In addition, there are also set dates for the starts of the selection and campaign process outlined below:

- October 5th, 2023 was the last date for parties to announce the process for Candidate selection

- Pre-Campaigning is scheduled for November 20th–26th to January 3rd.

- Candidate selection for the different direct representation positions is set for January 24th at the latest, and for indirect representation positions by January 31st.

- Electoral platforms must be registered in the first 15 days of January (we can get a clearer picture of policy priorities here).

- The formal campaign process will stretch from March 1st to May 29th, followed by the electoral blackout from May 30th to June 1st.

- The 2014 Political Reform had left open the possibility of 2 Legislatives operating simultaneously in August 2024 due to an error, which has now been corrected. The new Legislative will now convene on September 1st 2024.

- The new President of Mexico will now take over on October 1st (previously new presidents took over on December 1st), meaning AMLO will still have 1 month as president with the new Congress before the new one takes over.

From investors’ perspective, we believe 2 of the key issues that will be looked at are:

- What plans does each team have for the power sector?

- How the fiscal situation will be handled.

It’s possible that these two questions will not be fully answered until a new government takes over, but hints on the different plans could start emerging on some key dates. We believe the electoral platform proposals, and the formal campaign period will be relevant to garner some information on these fronts. In addition, once we start seeing the electoral teams and key experts that surround each candidate could shed some light on these issues.

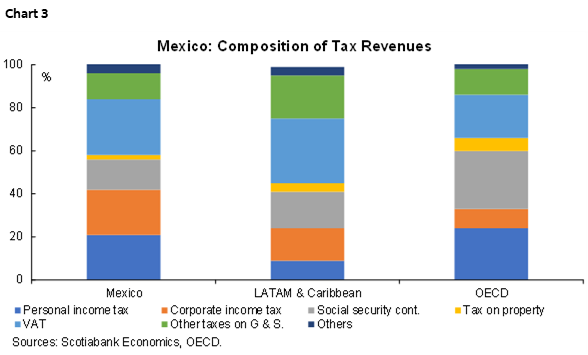

The 2024 budget shows a material widening of the PSBR (the wide definition of the fiscal deficit), to 5.4% of GDP, with fixed investment as a share of GDP falling, which implies that the increase in spending will be difficult to cut as the bulk of the spending increase is allocated to social programs. Mexico will have some space funding this larger deficit, as the increased inertial deficit is almost identical in size to the increase in the AUMs of the domestic pension fund system, and we don’t perceive that a relaxation of foreign investment limits to the pension funds regulation is in the cards. However, even though this change would give Mexico some additional room to fund itself for longer, allowing public debt to balloon would put Mexico’s investment grade at risk down the line, in turn putting Mexico’s weighting and inclusion in some benchmarks at risk—which would put debt funding ability back at risk. Hence, the better scenario is for the incoming administration to address the fiscal situation either with a tax or broader fiscal (spending + tax) reform. Looking at Mexico’s tax structure relative to the rest of LATAM and the OECD, taxes on corporate income in Mexico are high (one of the factors we believe weighs on investment), while social security contributions and property taxes are low (chart 3).

On the power front, there are growing concerns over increasingly tight power supply, in a country where the economy’s engine (the manufacturing sector), consumes about 55% of installed capacity. Spare power capacity (as % of total potential production) is almost at its lowest level since 1980, and with investment in the sector limited, and new plants typically taking 4-7 years to complete, the issue needs to be urgently addressed. With the fiscal situation tight already, some form of private participation will likely be needed. In addition, with a global trend to greener energy sources, and some DMs starting to restrict imports from dirtier energy manufacturers, a long-term plan for addressing the many elements of Mexico’s power sustainability strategy is necessary. AMLO was not able to amend the 2013 reform that allowed private participation at the Constitutional level, so the threshold to go back to that reform is not as high. However, going back to the 2013 reform could not be the only alternative. An update of Mexico’s old Pidieregas (a form of PPP structure that was used in the 1990s and early 2000s) could be an alternative, even if some adaptations are likely necessary. Some potential necessary adaptations could include: 1) adapting the financial structure to turn them into “on-balance sheet” debt, to comply with global regulatory changes, 2) the legal recourse to protect investors could be adapted to go directly to international arbitration under Mexico’s various trade treaties to make the projects more attractive to private investors. In addition, there is still the possibility of the pending arbitration under USMCA between Mexico vs Canada & the US over the power sector, which could force Mexico to go back to the 2013 reform, or potentially face fairly steep countervailing duties under USMCA.

Peru—We Expect Two More Reference Rate Reductions This Year… Despite El Niño

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

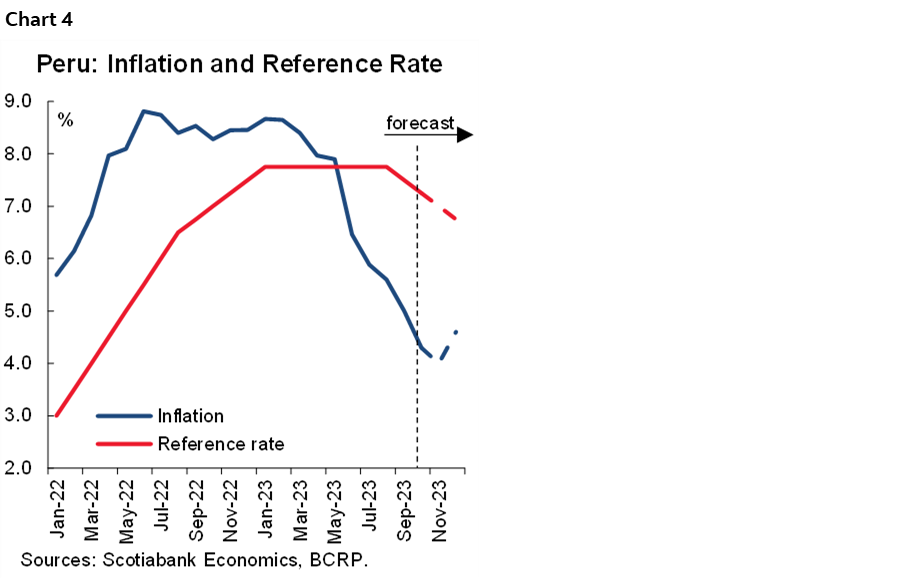

There is really little doubt that the BCRP will lower its reference rate on November 9th. We expect a 25bps decrease, to 7.0% (chart 4). What has changed is that we now expect an additional 25bps decline in December, to end the year at 6.75%. The brief pause we were expecting in December, we have pushed forward to January. The backdrop to our outlook of mildly faster easing is the sharp decrease in yearly inflation from 5.0% in September to 4.3% in October, plus our expectation that GDP growth will quite definitely be negative in 3Q. This combo tilts the balance towards another 25pbs decline in the reference rate in December, to 6.75%, with a prudence-pause put off until January. It’s tempting to up the ante even more and suggest that the BCRP will lower the rate by 50bps. The possibility is not off the table. However…, El Niño is coming, and the BCRP knows this.

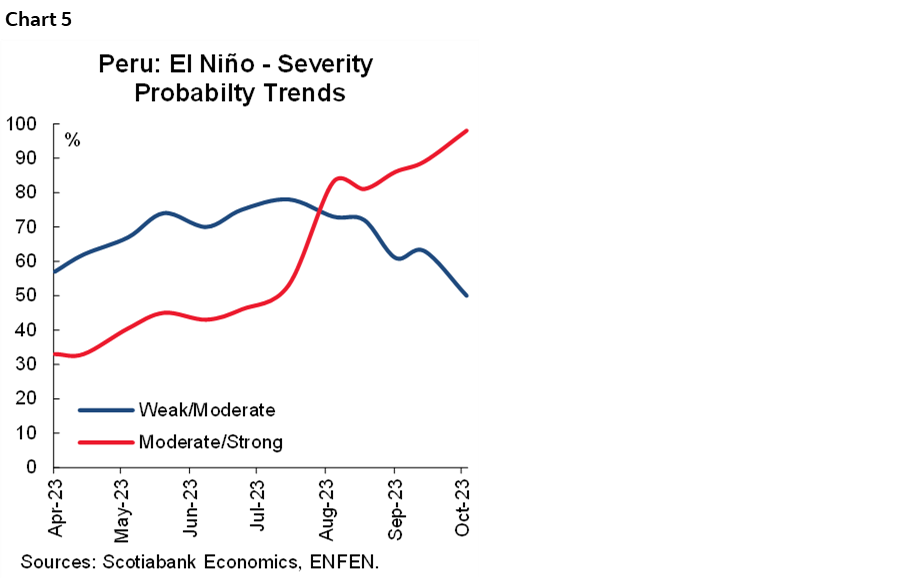

In early 2024 the BCRP must tread carefully. The local weather bureau that follows El Niño, Enfen (Estudio Nacional del Fenómeno de El Niño) now gives a 98% probability that the coming Niño will be moderate-to-severe (chart 5). In the past, similar Niños typically led to an inflationary blip. To lower the reference rate before El Niño is a fairly easy decision, but to do so in early 2024, with El Niño shaking its rattles and wetting the crib, will be less easy. The BCRP will need to balance the current state of GDP growth and inflation, which is crying out for a more aggressive reference rate downtrend, with the inflation risk that the upcoming El Niño poses. If the BCRP is too aggressive in reducing its reference rate, it risks having its currently still contractionary monetary policy turn suddenly expansionary at the height of the 2024 Niño inflation blip. Then again, the BCRP knows that the situation would only be temporary. Which is why we hesitate in changing our expectations regarding the pace with which the BCRP will lower its rate in 2024. We currently expect reference rate will be lowered to 5.0% by the end of 2024.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.