- Chile: Baseline scenario for the December plebiscite: approval above 60%

- Colombia: Unemployment rate remains in single digits in July; Citi Colombia Survey: 21 out of 25 analysts expect the monetary policy rate to stabilize for the 3rd month in a row, while inflationary expectations for the end of 2023 and 2024 remain moderate

- Peru: Continuous inflation decreasing in August

CHILE: BASELINE SCENARIO FOR THE DECEMBER PLEBISCITE: APPROVAL ABOVE 60%

A new constitutional plebiscite will be held in Chile on December 17th. Negotiations within the Constitutional Council have begun, while the debate in the Plenary will take place in chapters over the next few weeks. The strategy of the Republican councillors (extreme right) is interesting and challenges the achievement of a particularly broad consensus, but the approach with the representatives of Chile Vamos (center right) seems to be moving forward. The parties’ positions regarding the plebiscite have not yet been defined, but a position of rejection by some parties can be sensed.

Some polls point to a high percentage of undecided voters while others to rejection. Soon one might even expect some parties to explicitly opt for rejection. Political analysts have pointed out that times are getting tight to achieve a single, powerful voice for approval. Everything seems to be working against the desired achievement of a broad approval vote.

Why do we believe that this plebiscite will end with an approval victory of no less than 60%? That would be the baseline scenario that seems most appropriate and likely to us at Scotiabank Economics given the current political context.

Political science literature describes with special attention the so-called fatigue vote. The voter gets tired of being called recurrently to the polls to cast his vote. It generates apathy and abstention. In Chile, since the referendum of October 2020, there will be 11 calls to the polls considering the election of parliamentarians and president in November 2025 (12 if there is a second round). Apathy, tiredness and abstention will be present with greater intensity this coming December 17th, with some attenuation in abstention given the mandatory vote. In this context, it is difficult for rational voters with a Ricardian view to choose to keep the constituent process open by voting rejection. The parties calling for rejection will raise the need for a new constituent process as allowed by law and/or the current constitution. It will be a strategy that will lose against fatigue for being too technical without appealing to emotional content.

On the other hand, the importance of a constitution to make the necessary social changes that arose during the social unrest has clearly lost relevance. Citizen concerns are on other fronts at this time (and timing, circumstance and conjuncture are always important in any vote). Moreover, for many of those who voted in favour of initiating a constituent process, it has been diagnosed that improvements in health, pensions, education and security are areas in which a new constitution does not seem essential. The government itself has pointed out that reforms have been presented, but no political consensus has been reached to approve them; at no time has it been indicated that the constitution is the reason that has prevented agreements.

The protest vote is another particularly important issue for this plebiscite and one that has been widely discussed in political science. The null or blank vote, together with the vote for the least orthodox or novel tend to characterize the protest vote. The null or blank vote, being relevant options, have never characterized or determined Chilean electoral history. If indeed the Communist Party (extreme left) explicitly reveals its preference for rejection, it will most likely fuel a vote against such option and in favour of the proposal that will be read as elaborated by the Republican Party. The latter can be read as the least orthodox party at this juncture since its history of rise has been particularly rapid at the ballot box in recent years. Also, the protest vote is already sown when a 70% disapproval of the current administration, of which the Communist Party is a part, is widely revealed. What would probably crown the strength of the “approve” option, under the prism of the protest vote, would be for government leaders or authorities to express their dissatisfaction with the constitutional proposal presented for a vote.

What is the risk of an approval of the new constitution over 60%? Errors (unforced) of the right-wing constituents that end up raising sensitive emotions for an important proportion of the population. These emotions could emerge (and be enhanced by the supporters of the rejection) in value aspects that show some kind of discriminatory reading towards minorities or progressive positions in terms of values. Silence, the absence of declarations and hidden intentions, the avoidance of public or media discussion panels seem to be allies of approval.

If the result of the upcoming plebiscite is not less than 60%, the political scenario and the banners of struggle will be adjusted. Both right and left-wing parties will have to continue searching for the adequate and differentiating political space, this time without whipping the constitution.

What reading should we make for the asset price of such a political result? Political uncertainty would have a further reduction, which is undoubtedly always appreciated by financial variables.

—Jorge Selaive, Aníbal Alarcón & Waldo Riveras

COLOMBIA: UNEMPLOYMENT RATE REMAINS IN SINGLE DIGITS IN JULY

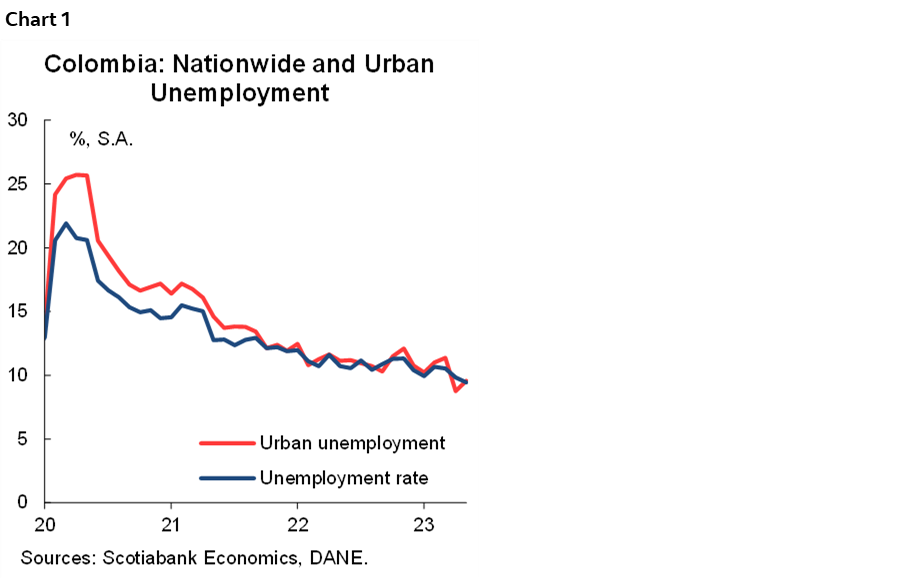

On August 31st, the National Statistics Department (DANE) released the labour market figures for the month of July. The national unemployment rate remained at 9.6%, while the urban unemployment rate stood at 9.8%. Despite labour data in general showing good results, it deteriorated slightly compared to June, both nationally and in urban areas, which were 20 basis points (bps) and 100 bps higher, respectively, than the previous month. For its part, the employment rate in July 2023 was 58.6%, an increase of 2.1 pp compared on an annual basis and becoming the highest employment rate since mid-2019.

The seasonally adjusted monthly numbers continued to trend lower, as the seasonally adjusted (S.A.) national unemployment rate reached 9.4%, the lowest since April 2017, while the S.A. urban unemployment rate was 9.6%, a deterioration of 80 bps m/m basis , but still in single digits (chart 1).

July’s labour market results continue to show a good performance, with sustained growth in job creation, along with an unemployment rate that remains at historically low levels. This will be an additional element for BanRep to consider at the next meeting in September.

Key information on employment data:

- In July, the female unemployment rate was 11.9%, which represents a slight increase compared to the rate recorded the previous month (11.6%). Similarly, the male unemployment rate went from 7.7% in June to 7.9% in July. The gender gap remained at a similar level to the previous month at 4pps.

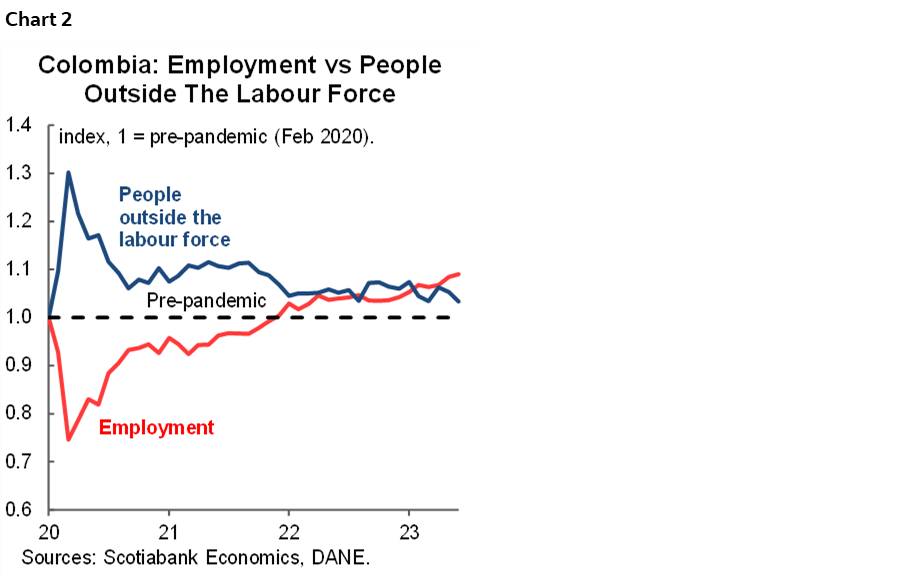

- In July 2023, the total number of employed individuals reached 23.2 million, an increase of +1.1 million year-on-year (chart 2). The employment growth continues to be driven primarily by the female population, which saw an increase of +674 thousand jobs compared to July 2022. The female population in urban areas accounted for 52.0% of the total employment growth (+365 thousand). On the other hand, for the nationwide data, the male population contributed an increase of +453,000 employed individuals in July 2023 compared to the same month of the previous year, mainly from urban areas, which contributed 44.0% of the new employment (+274,000).

- The sectors that contributed most positively to the variation in the employed population in July 2023 compared to the same month in 2022 were construction (+234,000), followed by sectors related to services and trade such as artistic, entertainment, recreational, and other service activities (+218,000); trade and vehicle repair (+176,000); accommodation and food services (+163,000); and transportation and storage (+122,000). Conversely, the only sector that showed a negative contribution in July was professional, scientific, technical, and administrative services (-60,000).

- Regarding occupational positions, the categories of self-employed workers and formal employees were the occupational positions that contributed most positively to the variation in the national total, with +604,000 and +568,000, respectively. By gender, the female population experienced a greater increase in the formal employee position (+354,000), while new jobs for the male population had a greater proportion in the self-employed worker position (+358,000).

- The proportion of informality decreased by 1.8 percentage points to 56.4%, compared to 58.2% recorded in July 2022. A total of +885 thousand formal jobs were created. Urban areas showed the greatest improvement in informality rate, decreasing from 43.9% in July 2022 to 41.6% in July 2023, and creating more than 595,000 formal jobs during this period.

The labour market results for July continue to highlight that employment growth is concentrated in the services and trade sectors. Additionally, the importance of the construction sector in generating employment stands out in economic activity in the coming months.

The strength of the labour market will remain an indicator carefully evaluated by BanRep in its upcoming monetary policy decision in September, where we estimate they will maintain the rate level stable again before beginning the easing cycle. However, the inflation data to be published next week will be crucial to reaffirm the call for rate stability for the third month.

CITI COLOMBIA SURVEY: 21 OUT OF 25 ANALYSTS EXPECT THE MONETARY POLICY RATE TO STABILIZE FOR THE 3RD MONTH IN A ROW, WHILE INFLATIONARY EXPECTATIONS FOR THE END OF 2023 AND 2024 REMAIN MODERATE

Citi’s August survey, which BanRep uses as one of its inflation expectations, monetary policy rate, GDP, and Colombian peso (COP) indicators, was released Thursday, August 31st.

Key points included:

- GDP expectations moderated for 2023 and continued to decline for 2024. For 2023, the average growth expectations decreased after having risen in the last four months. Consensus sees 2023 GDP growth at 1.24% y/y, down 9 bps compared to the previous month’s survey. On the other hand, growth expectations for 2024 continued to decline for the eighth consecutive month and now stand at 1.90% y/y, down from 1.95% y/y in July.

- Regarding inflation, analysts expect the downward trend to continue in August on an annual basis, but the monthly rate is expected to increase compared to July. On average, general inflation is expected to be 0.44% m/m in August, bringing the annual rate to 11.14% y/y. Expectations for the end of 2023 increased slightly to 8.92% y/y (up 11 bps from July’s survey), while expectations for 2024 declined to 4.80% y/y from 4.84% y/y in July. It’s also worth noting that 4 out of 25 analysts in the August survey still expect inflation to fall within the target range of 2% to 4% by the end of 2024.

- Scotiabank Economics’ projections are slightly above the analyst consensus, which calls for monthly inflation of 0.45% m/m and annual inflation of 11.16% y/y in August. It’s estimated that monthly inflation in August will remain above historical norms (pre-pandemic monthly average of 0.28%) due to pressures from non-food components, particularly gasoline and regulated prices, as well as potential risks throughout the month related to the impact of disruptions to regular operations due to road landslides.

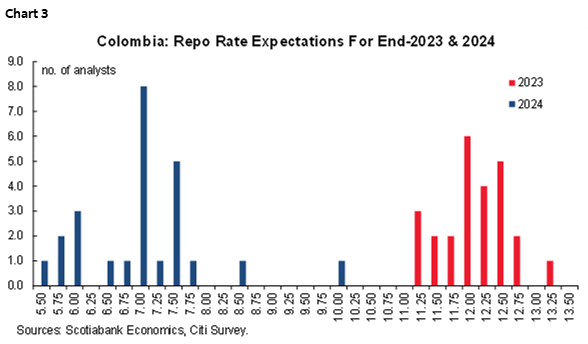

- Regarding monetary policy, most of the analysts surveyed expect interest rates to remain stable at the September meeting. 21 out of 25 analysts, expect BanRep’s board to keep the key rate at 13.25% for the third consecutive meeting, while the remaining 4 analysts expect BanRep to start a cycle of rate cuts (3 forecast a cut to 12.75% and 1 to 13%). There are still some differences in rate expectations for the end of 2023, but the range of differences continues to narrow due to a slight increase in the minimum range, which is now between 11.25% and 13.25% (compared to 11% and 13.25% in July’s survey). Among the 25 analysts, no one expects a rate hike above the current level, this month only 1 foresees BanRep to keep rates steady until the end of the year, while the remaining 24 expect the rate-cutting cycle to begin sometime between September and December 2023. For 2024, the estimated range remains fairly similar to last month’s survey, ranging from 5.5% to 10% in August, with an average of 7.01% and a median of 7% (chart 3).

Finally, the exchange rate is projected to reach USDCOP 4,146 by the end of 2023 (compared with USDCOP 4,206 in July) and USDCOP 4,135 by the end of 2024 (compared with USDCOP 4,199 in July).

—Sergio Olarte, Jackeline Piraján & Santiago Moreno

PERU: CONTINUOUS INFLATION DECREASING IN AUGUST

We expect inflation in August to be close to 0.3% m/m, close to that of July (0.39% m/m), but lower than that of August 2022 (0.67% m/m), with which the pace y/y would decline from 5.9% to 5.5%. Our forecast is close to the official figure of 5.6% (MoF) and the market consensus (5.4%), according to a Bloomberg survey. According to the monitoring of key prices that we carried out, we see a significant correction in poultry prices (-5%), partially offset by increases in the prices of perishable foods (mainly citrus fruits and vegetables), which would be reflecting the impact of the adverse climate conditions caused by the coastal El Niño. Core inflation would also be around 0.3%, remaining around 3.9% y/y.

Since August, the base effects for comparison are already marginal, so the rate of decline in inflation would be less than in the past. Perishable food prices are likely to remain under upward pressure and continue to reflect the effects of the El Niño phenomenon. Both in its latest statement and in recent monetary operations, the BCRP has given signs that it is ready to start the cycle of interest rate cuts, which we believe will happen soon.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.