FORECAST UPDATES

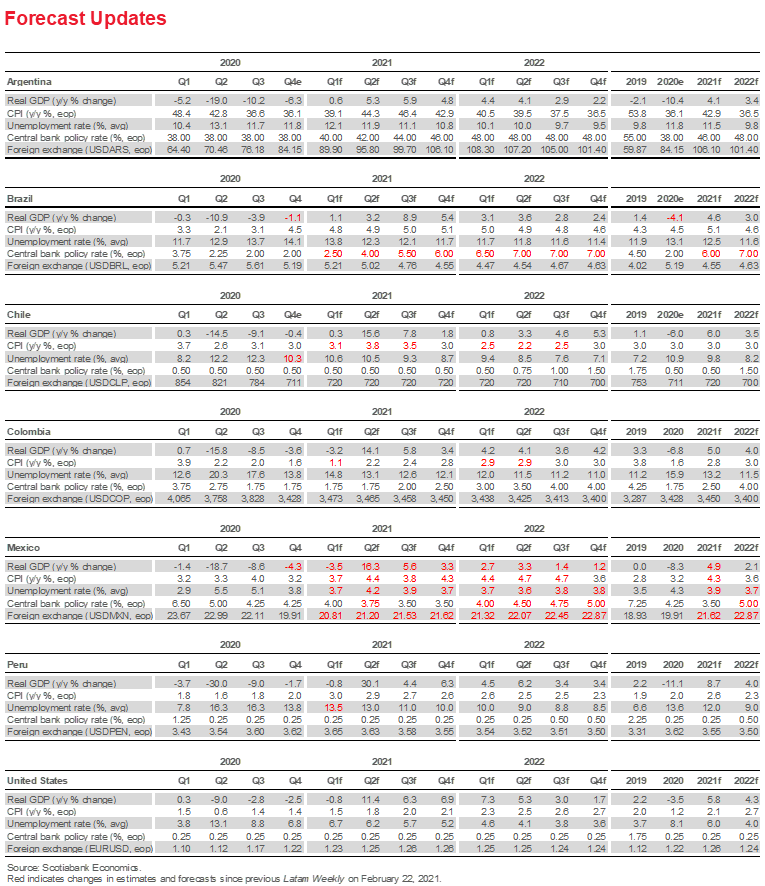

- In Brazil, we made our longstanding, front-loaded rate path for the BCB’s hiking cycle even more pro-active, with a first rate increase brought forward from Q2-2021 to the upcoming March 17 Copom meeting. In Mexico, the receipt of detailed sectoral Q4-2020 GDP data and indications of a stronger than expected hand-off to 2021 prompted a refresh of our outlook. While our forecast for real GDP growth in 2021 has been upgraded from 3.3% y/y to a 4.9% y/y, we continue to expect two more -25 bps cuts from Banxico before the end of Q3-2021.

ECONOMIC OVERVIEW

- COVID-19 second waves prompted new public health restrictions in late-2020 and early-2021, but their impact on economic activity has been less pronounced than measures imposed last year. As these contagion controls begin to be relaxed once again, we look at the corners of the Pacific Alliance countries' economies that are still working to re-open fully.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from end-2020 data and the first months of 2021, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period March 8–19 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Lift-Off and Re-Opening

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

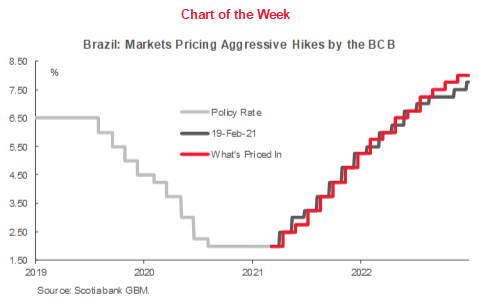

Brazil’s BCB is now expected to begin its hiking cycle at the Copom’s March 17 meeting.

Mexico’s growth outlook for 2021 has been upgraded substantially.

Pacific Alliance governments have begun lifting second-wave contagion controls, but as in most economies, service-sectors have the furthest still to go to re-open fully.

FORECAST UPDATES: BRAZIL AND MEXICO IN FOCUS

Our forecast updates (see table on p. 2) are focused on Brazil and Mexico, where some meaningful changes have been introduced.

In Brazil, we made our longstanding, front-loaded rate path for the BCB’s hiking cycle even more pro-active, with a first rate increase brought forward from Q2-2021 to the upcoming March 17 Copom meeting. Consensus has now broadly aligned around this view. The DI market is currently pricing almost 700 bps of Selic raises over the next three years in response to annual inflation around 5% y/y, more fiscal stimulus, and debt-sustainability concerns.

In Mexico, the receipt of detailed sectoral Q4-2020 GDP data and indications of a stronger-than-expected hand-off to 2021 prompted a refresh of our entire outlook. While our forecast for real GDP growth in 2021 has been upgraded from 3.3% y/y to 4.9% y/y, we continue to expect two more -25 bps cuts from Banxico before the end of Q3-2021 owing to persistent softness in both investment and consumption. While level effects are set to keep headline annual inflation at the 4% y/y ceiling of Banxico’s target range into Q2-2021, our team in Mexico City now foresees one -25 bps cut in Q2 and a second in Q3 (previously both were pencilled in for Q3), with policy rates heading upward again in early-2022.

CENTRAL BANKS: THE FIRST LIFT-OFF

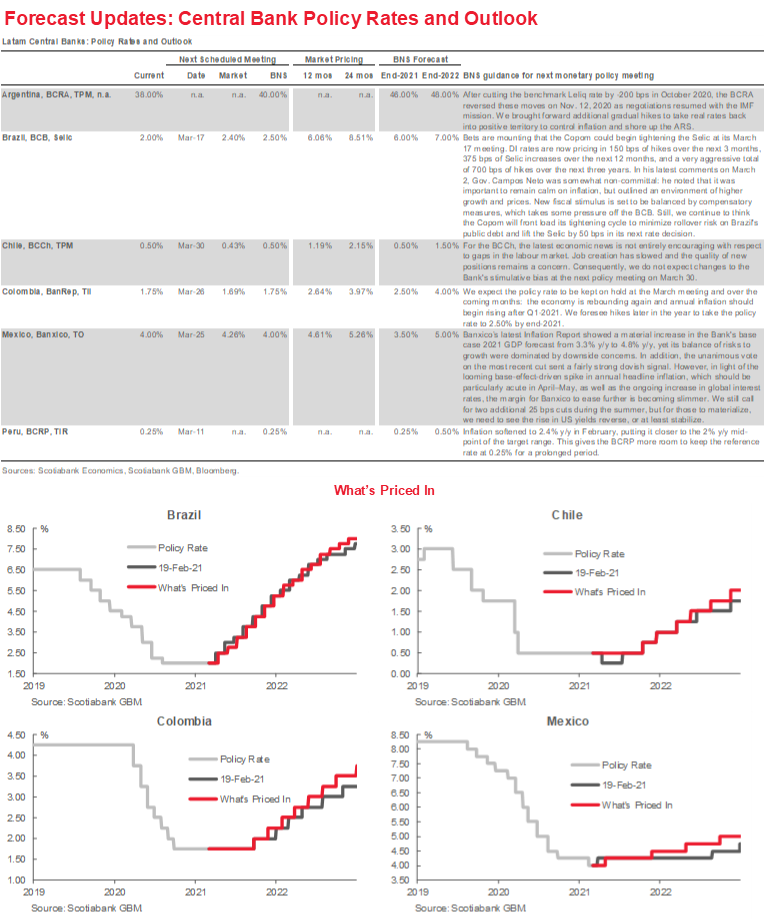

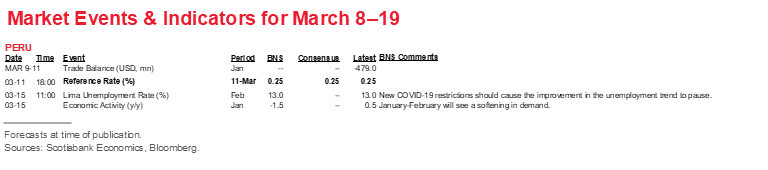

March features a busy central bank calendar (see table, p. 3), with Brazil’s BCB and Peru’s BCRP leading the way.

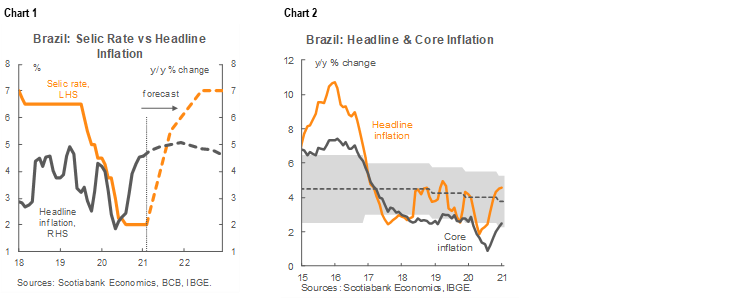

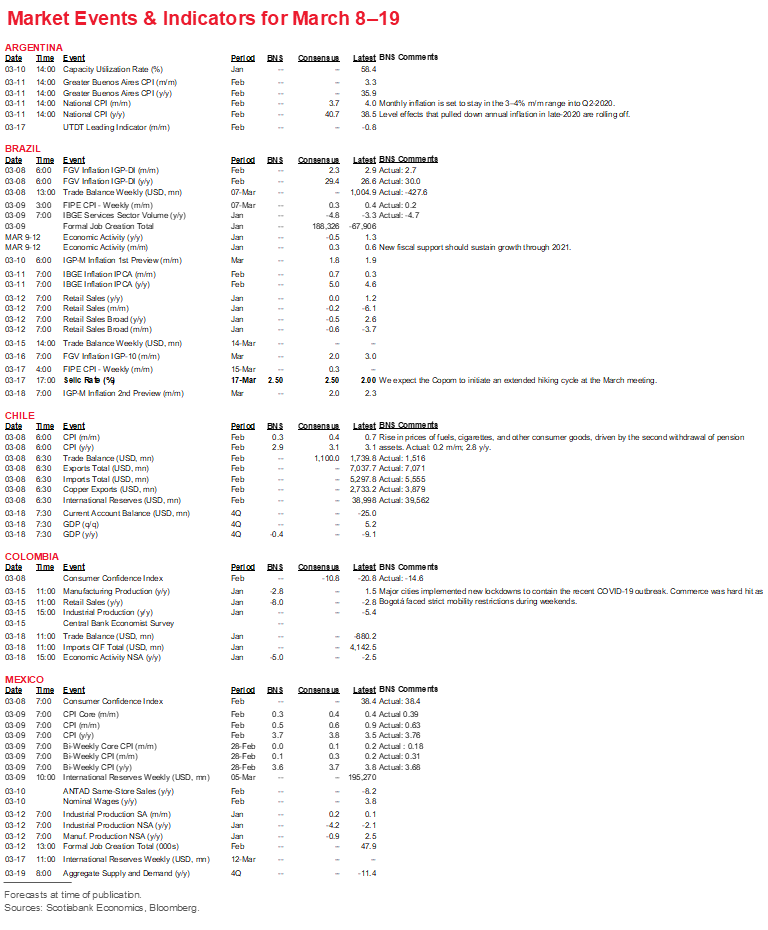

- Brazil. The Copom’s next rate decision is scheduled for Wednesday, March 17, and we, along with the consensus of analysts, expect a 50 bps increase in the Selic to kick off the first major hiking cycle amongst major Latam central banks (chart 1). Persistently high inflation in the midst of a gradually falling BCB target (chart 2), roll-over concerns with respect to Brazil’s large stock of public debt, and a fresh, if modest, round of fiscal stimulus prompted us to bring forward this first rate increase from our previous forecast that it would happen in Q2. Over the course of 2021, our Brazil economist expects the Copom to lift the Selic from 2.00% to 6.00%, and onward to 7.00% by end-2022. Our projected rate path is slightly more front-loaded than expected by the DI market, which is pricing 150 bps in hikes over the next three months and 375 bps in increases over the next year. Our calculus is that more pro-active moves by the Copom could limit this cycle’s terminal rate below the nearly 9.00% priced into DIs three years out (chart of the week, p. 1). Markets have opened a door for the Copom to move and we believe they’ll take this opportunity—and then some.

Both our view—and the market’s—is based on macro fundamentals rather than strictly a reflection of recent BCB communications. In his latest comments on Tuesday, March 2, Governor Campos Neto was somewhat equivocal: he stated that it’s important to remain calm on inflation, but he also noted that we’re in an environment of higher growth, with inflation becoming a new reality.

The BCB’s job has been made somewhat easier by recent developments on the fiscal front. The new USD 7.8bn stimulus package is likely to start flowing soon, and its Renda Brasil program, which replaces the Bolsa Familia system, should help sustain demand. Additionally, compensatory measures to maintain fiscal sustainability that were introduced by Minister Guedes managed to survive the legislative process without being undermined—which dampens some conflicting concerns for the BCB.

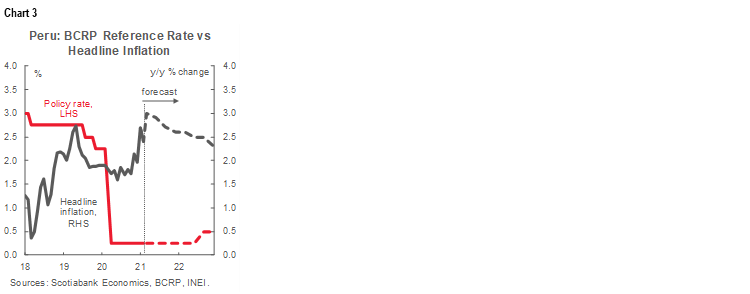

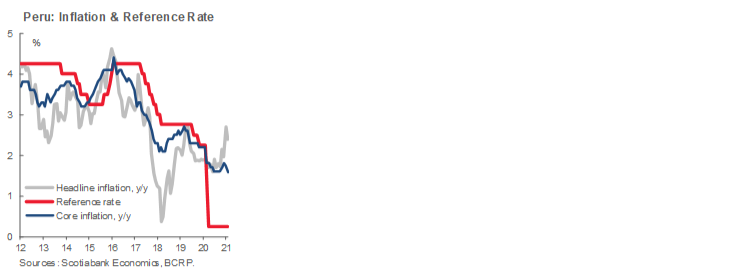

- Peru. The BCRP’s Board is scheduled to meet on Thursday, March 11, and we don’t anticipate any major developments at this meeting: the policy rate is expected to be held at the current record low of 0.25% with no meaningful change in the Board’s communications (chart 3). At its previous rate decision on Thursday, February 11, the Board similarly kept its key policy rate on hold at 0.25% and held its forward guidance unchanged in its statement. Board members advised that it would be “appropriate to keep the Bank’s expansive monetary policy stance for an extended period, so long as the negative effects from the pandemic on inflation and its determinants continue to persist.” The Board also repeated its promise that any further stimulus, if needed, would be provided through other instruments.

Following the pull back in annual inflation from 2.7% y/y in January to 2.4% y/y in February (chart 4), our team in Lima re-affirmed its expectation that the central bank will keep policy rates on hold through mid-2022. Although level effects could still drive headline annual inflation back toward the top of the BCRP’s 1–3% y/y target range at some point in the coming months, sequential monthly inflation looks set to remain well contained.

GAPS IN THE RE-OPENING RADAR

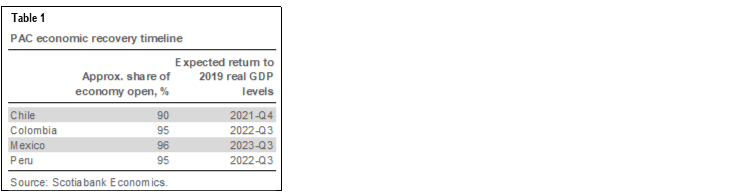

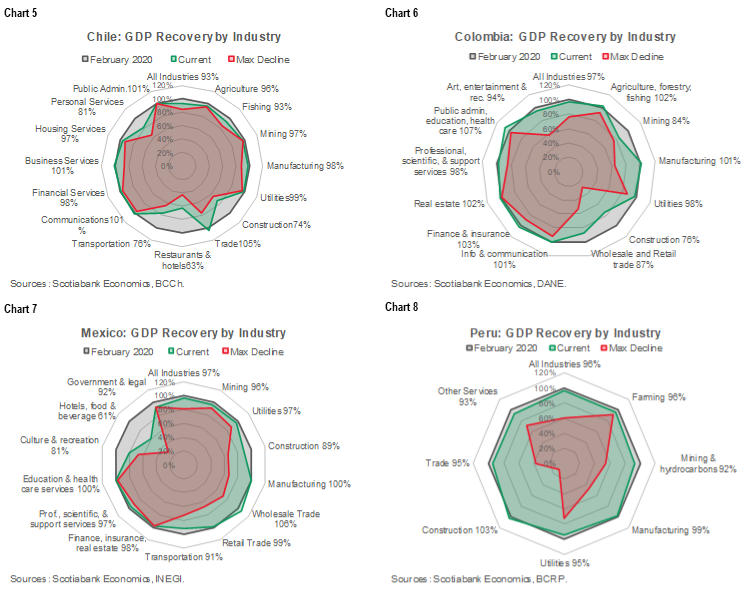

Despite the imposition of new controls to head off rising second waves of COVID-19 through the turn of the year, the Pacific Alliance economies continue to be nearly fully re-opened (table 1). But as in most countries, significant reactivation challenges remain in sectors and business models where physical distancing is difficult. As charts 5 through 8 underscore, most of the major sectors in Chile, Colombia, Mexico, and Peru have returned to pre-pandemic levels of monthly economic activity. Notable exceptions remain in tourism, hospitality, culture, and entertainment across all four economies, where levels of economic activity are up to -20% below pre-COVID-19 numbers. Transportation remains similarly impaired across all four countries owing to mobility restrictions.

Construction is the other major sector where activity remains broadly impaired, but with substantial variation across the Pacific Alliance. Building activity is down between about 10% in Mexico and nearly 25% in Colombia compared with February 2020, but construction has recovered to 103% of pre-pandemic levels in Peru. Peru’s outperformance reflects a relatively hot housing market in Lima and a recovery in public investment after a few quarters in which government capital spending had been a drag on growth.

In contrast, it’s notable that manufacturing, retail trade, utilities, and extractive industries are more or less fully re-opened across all four economies. At this stage, even if a third wave should emerge and elicit new controls, it’s unlikely that activity in these sectors would retrench again—we would instead simply see a delay in further gains.

USEFUL REFERENCES

H. Bastian (2021), “The Differences Between the Vaccines Matter”, The Atlantic, March 7: https://www.theatlantic.com/health/archive/2021/03/pfizer-moderna-and-johnson-johnson-vaccines-compared/618226/

R. Cherif and F. Hasanov (2021), “When it Comes to Services vs Manufacturing, Words Matter”, IMF Global Economy Blog, February 16: https://blogs.imf.org/2021/02/16/when-it-comes-to-services-vs-manufacturing-words-matter/

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Mass Vaccination Continues at a Formidable Pace; Employment Growth Slowed in January

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

Mass vaccination continues advancing at a formidable pace in Chile. As of the beginning of March, the national government had received 7,865,476 Sinovac vaccine doses and 505,050 Pfizer/BioNTech doses, which has allowed the vaccination of more than 19% of the population with at least a first dose.

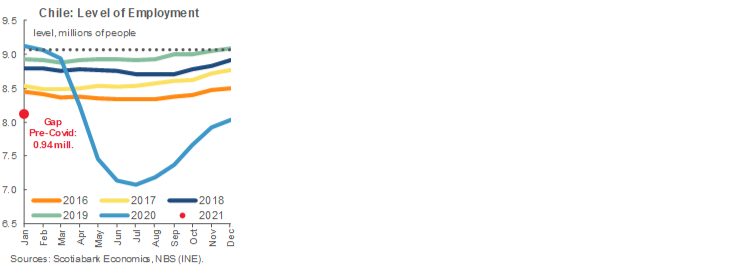

In data released Friday, February 26, the unemployment rate decreased to 10.2% in the rolling quarter November 2020 to January 2021, but the workforce is starting to grow more rapidly than employment (first chart), as is to be expected given that mobility restrictions have been lifted and more active searches for employment have begun. This will curb the fall in the unemployment rate in the coming months, and we do not rule out that it may even rise as the number of people entering the labour force could run ahead of job creation. As we have mentioned before, as vaccinations advance and mobility returns, so will the desire to seek employment. Sectoral data for January was also released on February 26. Manufacturing production fell -4.4% y/y, a print that was below expectations, explained by a sharp decrease in the production of chemical substances due to lower external demand. Positive news came from retail sales, which expanded 10.2% y/y (excluding new cars), fueled by the second set of withdrawals of pension assets.

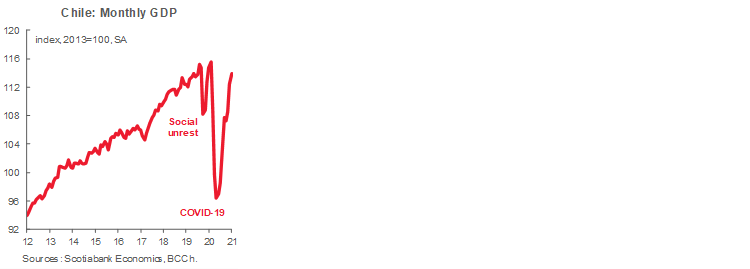

Data released on March 1 showed that January monthly GDP contracted -3.1% y/y (versus Bloomberg: -1.3% y/y and EEE: -1% y/y), owing to fewer working days relative to January 2020. On a seasonally adjusted basis, activity expanded 1.3% m/m, as services continue to rebound. The main disappointment came from construction, which fell relative to the previous month and in year-over-year terms, affected by COVID-19-control measures that have prevented a complete resumption of large construction activities. It should be noted that minor construction and architecture activities remain dynamic,as indicated in the central bank’s February Business Perceptions Report.

Given that February 2021 had the same number of business days as February 2020 and considering that seasonally adjusted growth that has been observed most months since June (interrupted only in October 2020, see second chart), we anticipate a decline between -1 y/y and 0% y/y in February GDP. So far, these results are fully consistent with an expansion of GDP in 2021 of no less than 6.0% y/y as the recovery gathers steam in the months ahead.

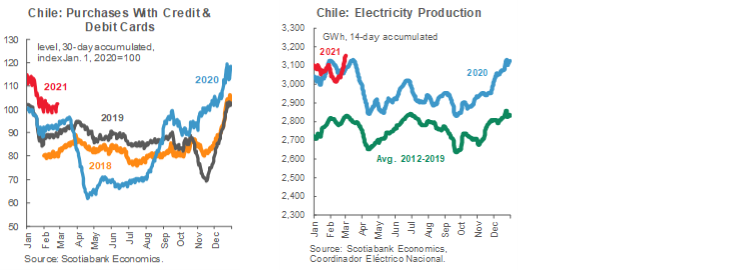

Our high-frequency indicators show that growth in the volume of Scotiabank Chile debit and credit card transactions has flattened at the margin, but remains above levels from a year ago (third chart). These data show that spending coming from the withdrawal of pension assets continues to lose momentum. But, in contrast, electricity generation levels have picked up in recent weeks, surpassing 2020 levels for the same period (fourth chart).

February inflation data was released on Monday, March 8. We anticipated a print of 0.3% m/m, explained by the rise in fuels, cigarettes, and upward pressure on mass consumption goods, fueled by the second withdrawal of pension assets. In the event, inflation came in at 0.2% m/m, and with this, annual inflation was 2.8% y/y last month, which followed 3.1% y/y in January. For year-end, we maintain our inflation forecast of 3.0% y/y, which is below market expectations. Our view is that the still-significant gap in the labour market should translate into lower pressures on prices throughout the year. This would offset the transitory upward shocks seen in the past few months, which were explained mainly by the withdrawal of pension assets and the liquidity measures to support household incomes.

Detailed national accounts data for Q4-2020 will be released on March 18. As often happens, we might see a slight revision in GDP figures, but that should not change the effective growth rate of 2020, which was -6.0% y/y. For 2021, on the other hand, we expect an increase of 6.0% y/y.

Colombia—Recovery Implies Wider Current Account Deficit, but It Should Be Covered by FDI

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

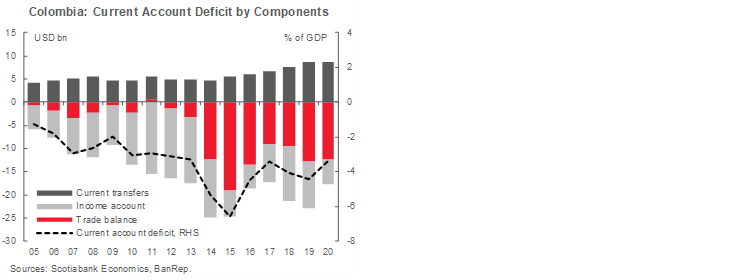

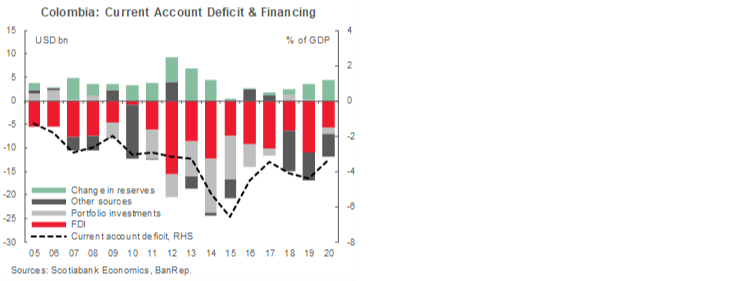

On March 1, BanRep published balance of payments (BoP) results for Q4-2020 and for 2020 as a whole, completing the picture in terms of macro variables for 2020. Not surprisingly, the current account deficit narrowed significantly in 2020 to -3.3% of GDP from -4.4% of GDP in 2019. A substantial decline in domestic demand led imports to fall by -21.7% y/y (goods and services) and reduced net outflows from the income account (also expected). These developments coincided with better-than-anticipated results for remittances—especially during the last quarter of 2020, which saw an expansion of 9.5% y/y—which confirmed that in 2020 the automatic stabilizers in Colombia’s external accounts worked perfectly: indeed, the net effects between exports, imports, income, transfers, and remittances are themselves the automatic stabilizers (first chart).

Additionally, in 2020 higher government indebtedness provided substantial new external financing (“other sources”, second chart) that was required to fill the shortfall in revenues resulting from the recession (COP 15.5 tn or 1.5% of GDP) and pandemic-related higher countercyclical spending equivalent to around 4% of GDP.

In Q4-2020, the current account deficit widened by -1.5% q/q to reach -4.1% of GDP, despite support to exports from better oil prices. Although a higher current account deficit is considered a vulnerability, it also showed that domestic demand recovered as mobility restrictions were eased. In fact, from September 2020 imports started a recovery path and, by December 2020, consumption and raw materials imports had turned positive compared with a year before. In contrast, capital goods imports were flat—very much in line with the quarter’s major GDP components, where private consumption was up by 8% q/q but investment rose by only 1.5% q/q. All this good news of rising domestic economic activity comes with a cost: the ample current account deficit had to be financed, and fortunately, the arrangement under the IMF’s Flexible Credit Line (FCL) saved the day.

For this year (as we stressed in the February 22 Latam Weekly), we expect economic activity to consolidate its recovery and GDP to grow 5% y/y on the back of improved investment along with a normalization in consumption; therefore, we expect the trade balance to deteriorate further owing to much higher capital imports, especially those related to transport and civil works. However, we do not anticipate the same speed of recovery for exports since coal (12% of total exports) has an endemic problem and we do not foresee higher exports from the sector this year. Additionally, as oil exports (in dollars) recover due price gains, outflows from the income account will also increase as a result of higher remittances of revenues from foreign oil companies back to their headquarters.

Finally, as the fiscal package passes in the United States, we believe remittances will benefit due to their high positive correlation with US economic activity. All in, the current account deficit in Colombia will likely deteriorate in 2021 to -3.8% of GDP or slightly more if economic activity accelerates further.

As discussed above, higher current account deficits must be financed; however, in 2021 Colombia will not have the extraordinary assistance from multilaterals it had in 2020 and government external debt issuance is unlikely to increase at the same pace as last year. Financing, therefore, must come from another source. The last couple of recovery cycles showed that higher current account deficits have been financed primarily by FDI. For instance, in 2011, Colombian GDP grew 7% y/y and the current account deficit deteriorated by USD 1 bn—but FDI grew 128% y/y to finance this greater external deficit. This trend continued for the next three years, especially since investment grew by 8.5% y/y, on average, during that time. Higher capital imports for investment were accompanied by their own financing via FDI. For 2021, we expect investment to rise by 7.7% y/y, financed by 48% y/y growth in FDI that would complete financing of the current account deficit.

Colombia’s current account deficit is likely to put a limit on the extent to which the COP may appreciate in the near term. As vaccinations roll out, global economic activity grows, international trade recovers, and risk sentiment improves, EM currencies should receive some support, but Colombia’s balance of payments could dampen the extent to which the peso sees gains compared with its peers.

Mexico—Revisions to Our Forecasts

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

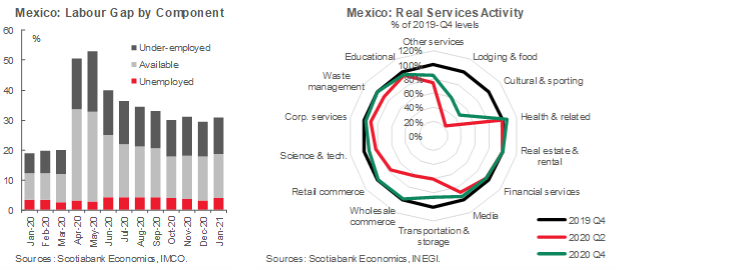

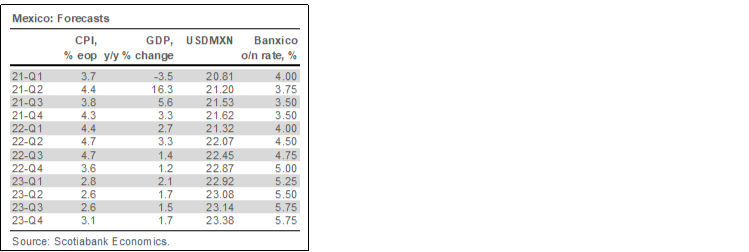

Mexico remains stuck in a “K-shaped” recovery where domestic demand and the services sector have lagged other major components of GDP. However, vaccination efforts in the US (which accounts for 65–77% of tourism into Mexico) as well as an eventual normalization in domestic activity imply that, during the second half of the year, we could see a stronger-than-anticipated recovery in tourism & entertainment, the weakest sub-sectors within services. The rebound in services should provide a significant boost to both GDP and employment. Mexico’s employment gap remains over 10 percentage points wider than its pre-COVID-19 level (first chart), with an important part of the recovery to date coming from secondary activities. We expect the recovery in the tourism & entertainment sector, which accounts for around 10% of employment, to support jobs gains and to provide an impulse to broader domestic demand. Accordingly, despite still seeing an economy in contraction on a y/y basis in Q1-2021, we are revising our 2021 growth forecast upwards, based on our expectation of much more dynamic services-sector activity in H2-2021 that begins closing existing gaps (second chart). Our revised 2021 real GDP growth forecast of 4.9% y/y, on the back of a stronger quarterly profile (table), is 10 bps higher than the base case Banxico just released in its Quarterly Inflation Report.

The next couple of weeks are relatively light for the data pipeline, with the first major release being February CPI on March 9. In the event, the print came in tight to consensus at 0.63% m/m and 3.76% y/y, just above our projections. Although this brought sequential inflation down from 0.86% m/m in January, level effects pushed annual inflation up from 3.54% y/y. Looking ahead, we get ANTAD same store sales for February (March 10), which should improve after a dismal January; and industrial production for the first month of the year (March 12), which we expect to show a loss in momentum. On March 19 we will also get aggregate demand data, where we expect domestic activity to remain broadly subdued, with investment still the weakest link in the recovery.

The next Banxico rate decision is scheduled for March 25, and we expect the Board to stay on hold at that time. Monetary-policy decisions will remain finely balanced through the middle of the year as policy makers and markets look to see how headline inflation fares through Q2-2021, but we expect -50 bps of additional cuts during Q2–Q3.

Peru—Double Uncertainty in Q1: COVID-19 and Elections

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

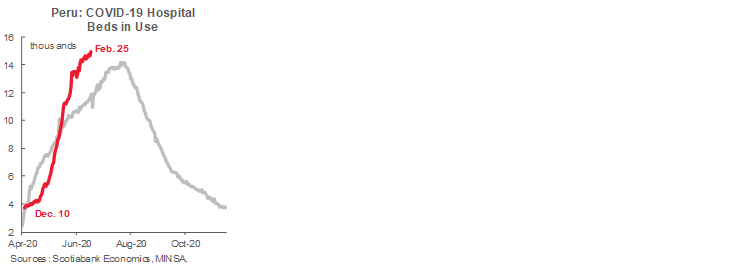

COVID-19 concerns continue to dominate the government agenda. Although there are incipient signs that the second wave of new cases is passing its peak (first chart), the country is still far from being out of the woods. However, most of the restrictions that were put in place in February have been lifted, and the government seems to be inclined to continue to ease controls. Vaccinations have started, with about 1% of the population having received shots.

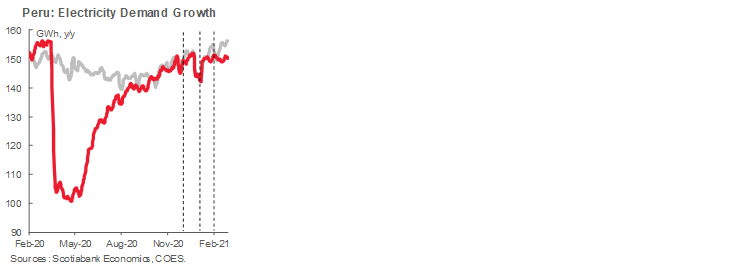

The economy appears to have gotten off to a slower start in 2021, as COVID-19 measures, as limited as they have been, put a pause on the impressive recovery with which 2020 ended. We now expect a mild -1.5% y/y contraction in GDP in January. February is more difficult to gauge. The restrictions were broader, but they affected mobility—and therefore demand—rather than production. Electricity output declined a rather benign -1.8% y/y in February (second chart) and government officials reported a strong 18.7% y/y increase in public investment in February. However, what we’re really looking forward to seeing is March, which will be the first month to compare with last year’s lockdown, so GDP growth should be very high. Just how high will tell us how much of the growth is simply a rebound off a low base, and how much is more than that. Construction, real estate, agroindustry, and government spending are sectors and sources of demand that are currently clearly above pre-COVID-19 levels.

Politics will dominate economics until the April 11 elections. The elections continue to be very open, with the leading candidates for the presidency garnering no more than 10% to 11% of support in polls. Only seven percentage points separate the leading candidates from those in 6th to 7th place. Undecided and blank poll results garnered three times the responses of the leaders in the polls. In short, there are only so many ways to say that the race is as open as can be. As elections near, votes typically start concentrating around candidates who are more likely to get into the second round.

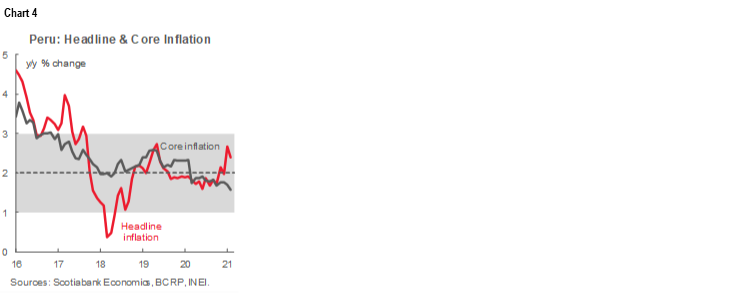

In recent economic news, inflation subsided to 2.4% y/y in February from 2.7% y/y in January and, with this print, our concerns over inflation’s trend have also eased. This is a level of inflation at which the BCRP can be comfortable leaving its reference rate at 0.25% for a prolonged period of time (third chart).

Copper has been the talk of the town ever since it surpassed USD 4/lb, a price nearly beyond belief just six months ago. The FX market has yet to acknowledge high metal prices, however, and the PEN has continued to weaken. A correction and realignment with metal price fundamentals later in the year may depend on how much confidence the soon-to-be elected authorities instill in markets. In the short term, corporate USD demand has continued to be firm, but at a reduced pace, while offshore USD demand has come off the sidelines to put additional downward pressure on the PEN. In response, the BCRP has become more active in containing the PEN’s losses. The end result is a moderate softening of the USDPEN to the 3.66–3.68 level. We had been expecting this range, as the PEN typically weakens prior to elections.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.