FORECAST UPDATES

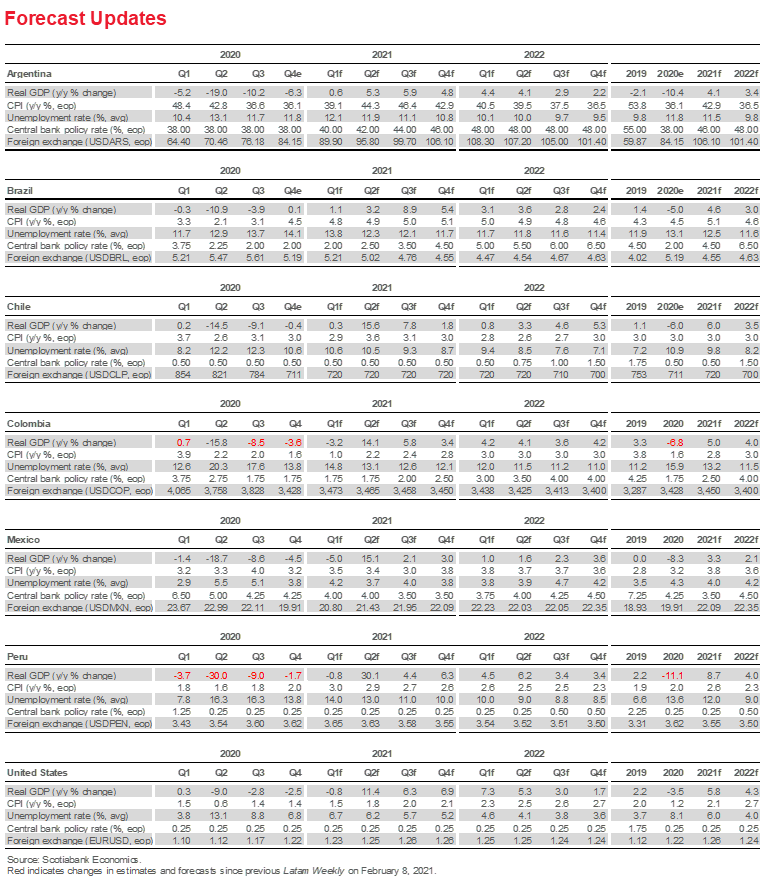

- Our forecasts are unchanged from previous publications: although new and revised numbers for actual 2020 GDP in Colombia and Peru came in a touch better than we had estimated, neither development implied the need for alterations to our outlook.

ECONOMIC OVERVIEW

- Three big questions are animating global macro discussions on emerging markets: vaccination roll-outs, prospects for inflation, and sovereign debt sustainability in the wake of exceptional COVID-19 fiscal support packages. We take stock of where the Pacific Alliance countries stand on all three fronts.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from end-2020 data and the first weeks of 2021, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

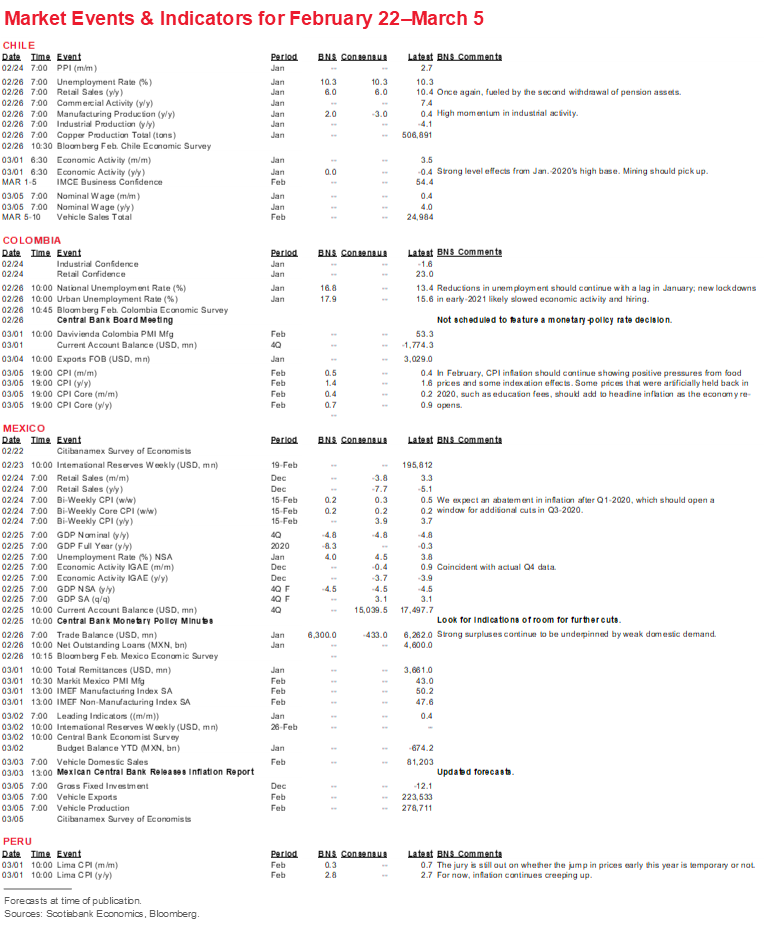

MARKET EVENTS & INDICATORS

- Risk calendar with selected highlights for the period February 22–March 5 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Vaccines, Inflation, & Debt

Brett House, VP & Deputy Chief Economist

416.863.7463

Scotiabank Economics

brett.house@scotiabank.com

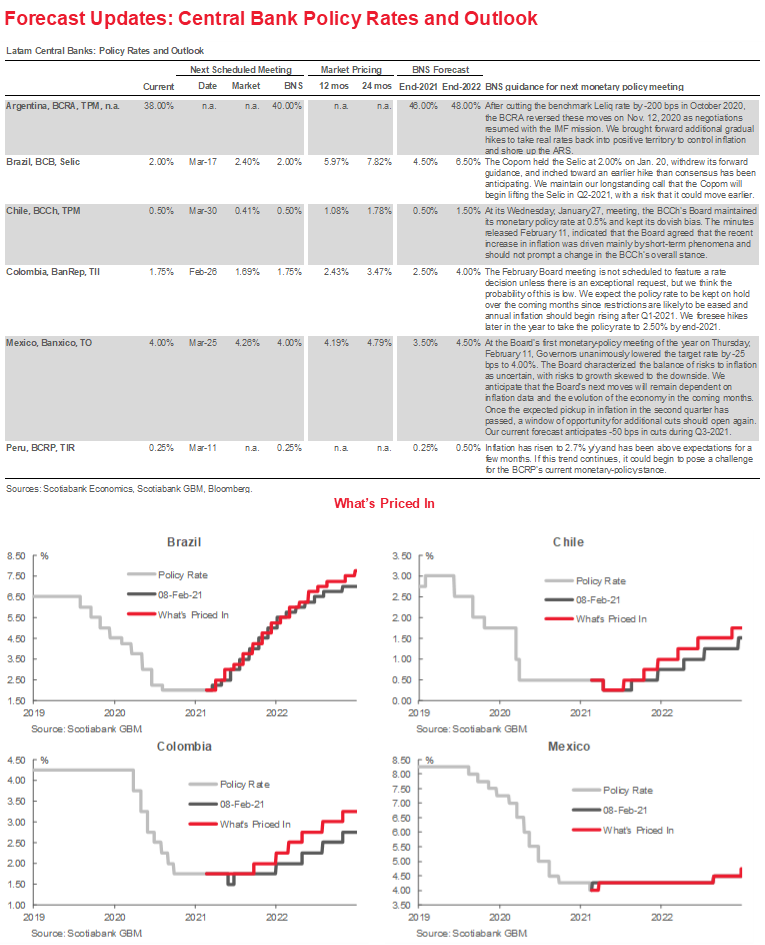

Central banks have a quiet fortnight ahead, with only minutes and a new quarterly Inflation Report coming from Mexico’s Banxico.

We look at three big questions animating global macro discussions on emerging markets: vaccination roll-outs, prospects for inflation, and sovereign debt sustainability in the wake of exceptional COVID-19 fiscal support packages. We take stock of where the Pacific Alliance countries stand on all three fronts.

FORECASTS: STEADY ON

Our forecasts have been held steady from previous publications: new and revised numbers for actual 2020 GDP in Colombia and Peru came in a bit better than we had estimated for both countries, but neither development implied the need for alterations to our forecasts. In Colombia, real GDP contracted by -6.8% y/y in 2020 compared with our estimate of -7.5% y/y; we retain our expectation of 5.0% y/y growth in 2021. Similarly, Peru’s real economic contraction in 2020 ended up at -11.1% y/y, close to our estimate of -11.4% y/y. Our team in Lima holds its forecast for 2021 growth at 8.7% y/y, well below the BCRP staff’s ambitious projection of an 11.5% y/y expansion. We believe the BCRP’s number will be revised closer to ours when its outlook is updated in the next Inflation Report, which is set to be published in March.

CENTRAL BANKS: BANXICO MINUTES CALIBRATE ROOM FOR MORE EASING

The fortnight ahead is set to see few scheduled developments on the monetary policy front, with no rate decisions in the calendar for the next two weeks (see Central Bank Policy Rates and Outlook, p. 3).

- Mexico. Banxico’s regular calendar anticipates on Thursday, February 25, the release of the minutes from its last monetary-policy rate decision on Thursday, February 11, where the Governors voted unanimously to make a -25 bps cut to the Bank’s headline policy rate, taking it down to 4.00% (chart 1)—its lowest level since May 2016. Although a solid majority of analysts expected the cut, most were surprised by the fact that all five Board members supported the move after Deputy Gov. Heath had indicated that the window for cuts may not open again until April or May.

The statement underscored that “incoming information allows for a monetary policy adjustment”. The Board saw the balance of risks as uncertain, but prospects for growth were skewed to the downside. As a result, the Board’s forward guidance was fairly neutral, noting that “monetary policy implementation will depend on the evolution of the factors that impact headline and core inflation, their expected trajectories within the forecast horizon, and their expectations.”

It’s expected that level effects will keep annual headline inflation up over the coming months (chart 2), but sequential monthly inflation is likely to remain subdued. Once the economy gets through this price hump, we see a new window of opportunity for additional cuts to support the economy through soft trade volumes, weak investment, and damp domestic demand (chart 1, again).

We will be scrutinizing the minutes for any indications from the Board’s members regarding their perceptions of Banxico’s remaining room for further easing in its policy rates. Monetary-policy decisions over the next few months will need to balance Mexico’s relatively weak domestic prospects with the implications of a strengthening global economy.

Our team in Mexico City continues to expect -50 bps in cuts during Q3-2021 (see Forecast Updates, p. 2).

Banxico’s next quarterly Inflation Report is due for publication on Wednesday, March 3. By then, Banxico’s staff will have inflation data for the first half of February (Feb. 24), detailed numbers on Q4-2020 GDP (Feb. 25), and February manufacturing results (Mar. 01).

- Colombia. The BanRep Board is due to meet on Friday, February 26, but the discussion is not scheduled to feature a policy-rate decision unless exceptional circumstances motivate a change in the agenda.

MACRO DATA: PRICES—GETTING PRICIER?

- Chile. January producer price index (PPI, Feb. 24) could give some insight on further incipient price pressures, while Feb. 26 sees the arrival of a raft of real-activity indicators. The January unemployment rate is expected to remain unchanged from December at 10.3% on rising participation, while January’s manufacturing and retail numbers are projected to reflect strong momentum and demand fuelled by pension assets. As a result, January’s economic activity index (Mar. 1) should come back to levels from a year ago—a point it hit briefly in November 2020, which means Chile would join Peru (see our February 16 Latam Daily) in reaching this monthly year-on-year watermark.

- Colombia. Although the recovery continues, January unemployment rates (Feb. 24) likely backed up a bit owing to new lockdowns at the start of the year while participation rates rose. Sequential price pressures are expected to have remained strong in February’s print (Mar. 5) even though level effects would take annual headline inflation down from 1.6% y/y in December to 1.4% y/y in January.

- Mexico. Price data for the first half of February (Feb. 24) are likely to show some decline in sequential monthly inflation, but level effects should still push up the annual headline measure from 3.7% y/y in late-January to around 3.9% y/y. Detailed GDP data for Q4 (Feb. 25) should confirm an -8.3% y/y contraction for all of 2020 and underpin a refresh of our forecasts in the following week.

- Peru. February’s likely inflation numbers (Mar. 1) are the subject of some debate over whether January’s jump to 0.7% m/m and 2.7% y/y was a temporary aberration or the beginning of a persistent drift upward. Our team in Lima expects sequential monthly inflation to cool to 0.3% m/m, but level effects imply that would still lift annual headline inflation to 2.8% y/y, taking it near the top of the 1–3% y/y target range for a time.

VACCINES AND VACCINATIONS: GETTING BETTER

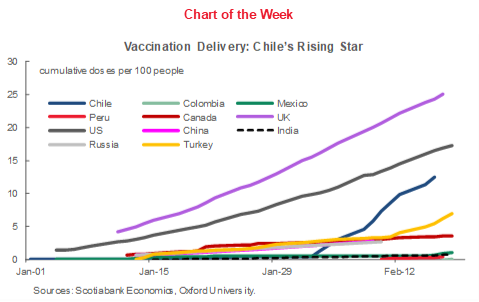

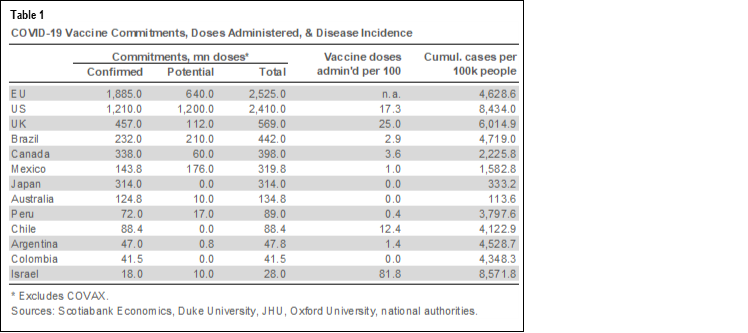

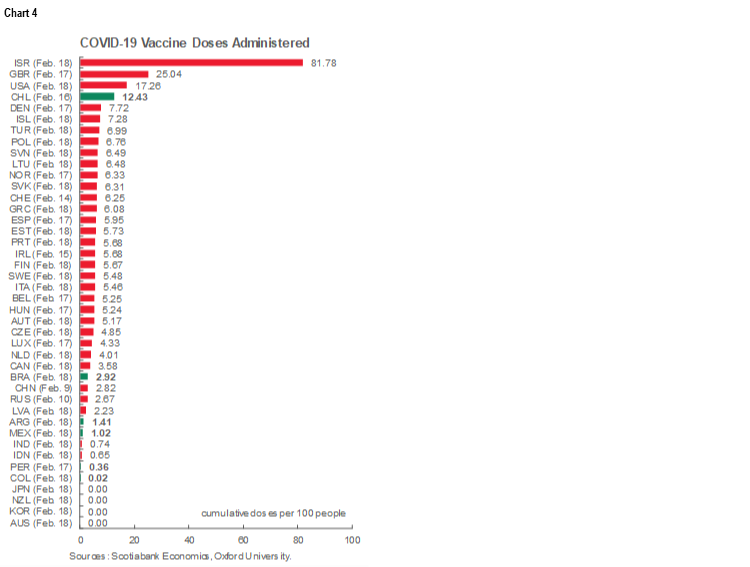

As Scotiabank Economics’ February 12 Global Week Ahead argued here, there’s a need to reset the global narrative on vaccines and vaccinations—pessimism owing to hiccups in the roll-out of shots has been overdone and reality is rapidly catching up on these sentiments. By this past weekend, mass vaccination programs had begun in all six of Latam’s major economies (table 1); existing and potential vaccine purchases commitments, even when one abstracts from procurement via COVAX, are sufficient to cover the populations in Brazil, Chile, Mexico, and Peru, with additional doses still needed in Argentina and Colombia (chart 3). In less than three weeks, Chile’s mass vaccination program has put it amongst the global leaders in per capita doses administered (chart of the week, p. 1, and chart 4). The rest of Latam is set to step up progress in the coming weeks.

Nevertheless, speeding the delivery of vaccinations across emerging markets is critical to the ongoing recovery of the global economy. A recent NBER working paper (see Useful References at the end of this section) projects that even if developed markets achieve universal coverage of their populations later this year, they will still bear nearly 49% of the economic costs of the pandemic in 2021 owing to trade links with the rest of the world. The costs of underwriting global vaccine delivery would be minuscule by comparison.

INFLATION: SET TO STAY IN RANGE

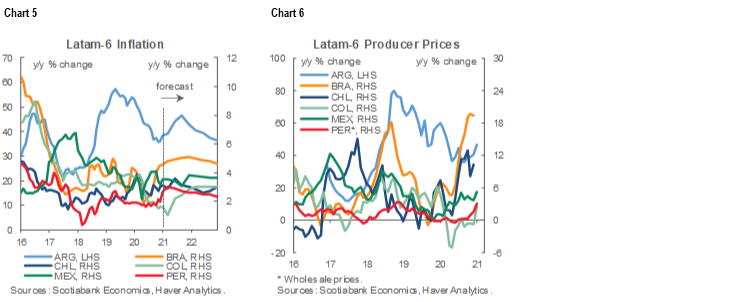

Narrowing output gaps in some developed markets, such as Canada and the US (see our February 4 Global Forecasts and a related note), are prompting concern about a possible concomitant rise in emerging-market inflation. While Brazil is seeing persistent price pressures that should prompt the region’s first rise in policy rates, and Argentina remains far from a policy mix that would bring inflation under control, price gains are set to stay within central-bank target ranges in the Pacific Alliance countries (PACs, chart 5). Recent spikes in Chile and Peru are expected to be transitory as economic support measures wane. Colombia’s soft headline inflation numbers are projected to rise later this year as level effects wear off, but they should eventually converge on the BanRep’s 3% y/y target. In contrast, level effects in Mexico should take headline inflation down at mid-year and provide space for more easing by Banxico. Across the PACs, recovering labour markets and mixed credit growth are not yet strong enough to sustain durable upward price pressures over the forecast horizon. Producer-price indices (PPIs) are on the rise across Latam (chart 6), but these gains have been anticipated in our headline inflation forecasts.

SOVEREIGN DEBT: SUSTAINABLE

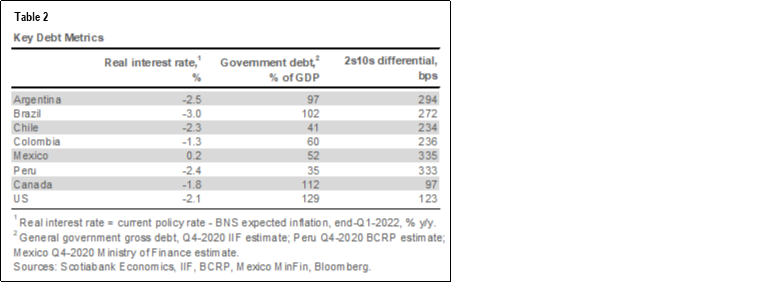

The COVID-19 pandemic prompted unprecedented policy responses by both developed-market and emerging-market governments, and now concerns are naturally turning to how these authorities will cope with the resultant boost in public debt stocks. The PAC governments’ key debt metrics continue to compare favourably with those in other major economies. As we highlighted in our February 8 Latam Weekly, on one of the most basic measures of sovereign debt sustainability—forecast real growth rates versus real interest rates—IMF projections imply that the PACs are set to be able to cover the costs of servicing existing and new debt. Real interest rates are strongly negative, with the exception of Mexico, and debt burdens are relatively low (table 2). Although long-term debt-servicing costs are set to rise with steepening yield curves, higher long-term nominal rates reflect improving growth prospects.

USEFUL REFERENCES

P. Alvelda, T. Ferguson, and J. Mallery (2020), “To Save the Economy, Save People First”, Institute for New Economic Thinking Article, November 18: https://www.ineteconomics.org/perspectives/blog/to-save-the-economy-save-people-first

C. Bown, M. de Bolle, and M. Obstfeld (2021), “The pandemic is not under control anywhere unless it is controlled everywhere”, PIIE Real Time Economic Issues Watch, February 2: https://www.piie.com/blogs/realtime-economic-issues-watch/pandemic-not-under-control-anywhere-unless-it-controlled

C. Cakmakli, S. Demiralp, S. Kalemli-Ozcan, S. Yesiltas, and M. Yildirim (2021), “The Economic Case for Global Vaccinations: An Epidemiological Model with International Production Networks”, NBER Working Paper 28395, January: https://www.nber.org/papers/w28395

C. Cookson and A. Gross (2021), “What we know about the most troublesome Covid mutations”, Financial Times, February 8: https://www.ft.com/content/71e53321-3719-4f10-9406-c614a5ddc1b8

World Bank (2021), Global Economic Prospects, January 5: https://www.worldbank.org/en/publication/global-economic-prospects

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Mass Vaccination Continues Moving Forward; Inflation Surprises to the Upside

Jorge Selaive, Chief Economist, Chile

56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Carlos Muñoz, Senior Economist

56.2.2619.6848 (Chile)

carlos.munoz@scotiabank.cl

Mass vaccination continues to be the main development in the Chilean economy. The pace at which Chile is inoculating its population is remarkable: around 200 thousand shots per day are being administered, and according to the latest estimates, the country could achieve herd immunity by mid-year, far ahead of previous expectations.

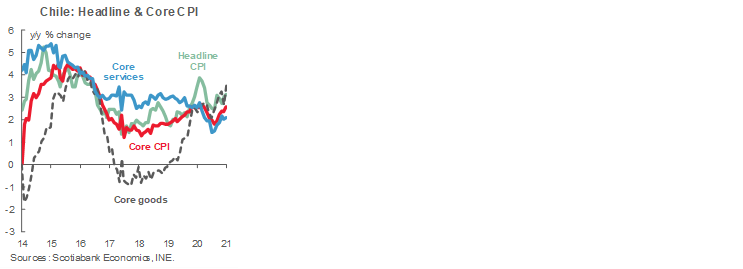

In data released Monday, February 8, January CPI stood at 0.7% m/m, influenced by notable pressures on the prices of mass consumer goods due to a strong increase in the disposable income of households and relatively limited inventories. Coupled with seasonal rises in food prices that were somewhat greater than in the previous year and a lift in international fuel prices, CPI growth reached one of the highest rates that has been seen in January. With this, annual inflation hit 3.1% y/y (first chart). However, a note of caution regarding inflation is provided by the weakness of the labour market, which continues to be the main concern for the central bank (BCCh) when evaluating the extent to which these inflation results are transitory and calibrating its monetary stimulus in response.

On Thursday, February 11, the minutes of the BCCh Board’s monetary-policy meeting on January 27 were published. The account of the Directors’ deliberations confirmed the dovish stance communicated in the meeting’s statement. The Board’s discussions showed a clear effort to complement fiscal policy and acknowledged that there are still wide output gaps to close. In the January 27 meeting, the Board voted unanimously to hold the benchmark policy rate at its “technical minimum” of 0.5%.

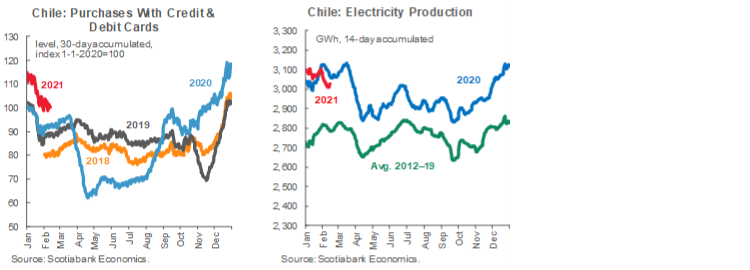

Our high-frequency indicators show that transactions growth has continued decelerating in the past weeks, closely approaching 2020’s levels (second chart). Data show that spending coming from the withdrawal of pension assets is losing momentum. By segments, supermarkets is the only category that shows high—though declining—levels of transactions, while department stores, clothing, restaurants, and tourism travel are all subdued. Electricity generation levels have also fallen in the past few weeks, with prints below 2020 records (third chart).

The next fortnight will be full of tier-1 data releases. On Friday, February 26, sectoral and employment data for the month of January will be published. We expect an increase of 6% y/y in January retail sales, as the second withdrawal of pension assets was still boosting private consumption last month. Manufacturing output should rise by 2% y/y as a certain momentum has started building around industrial activity despite mobility restrictions. We estimate that January’s unemployment rate remained at 10.3% as the widening in the active workforce matched new jobs growth while mobility restrictions were still in place. On Monday, March 1, monthly GDP data for January will come out. We estimate that the gap compared with a year ago will re-close; year-on-year growth would be higher were it not dampened by a high base for comparison from January 2020 and a tightening in COVID-19 rules. Mining activity should pick up after the subdued print in December.

Colombia—Economic Resilience and Our Inflation Forecasts Lead Us to Maintain Our Expectation of Rate Hikes from Q3-2021

Sergio Olarte, Head Economist, Colombia

57.1.745.6300 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Economist

57.1.745.6300 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

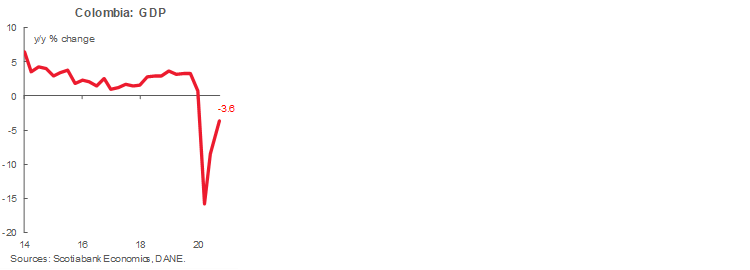

During 2020, mobility restrictions related to the COVID-19 outbreak were the driver of the global economic contraction; in Colombia, almost 40% of the economy was shut down during Q2-2020. Once people could partially return to work and adapted to new norms, the ensuing recovery in many economies surprised to the upside. With Colombia’s “new normal” re-opening scheme in place since September 2020, the relaxation of mobility and other public-health restrictions boosted Q4-2020 GDP above most estimates. In fact, Q4-2020 GDP growth was -3.6% y/y (first chart) while the market consensus expectation was -4.5% y/y.

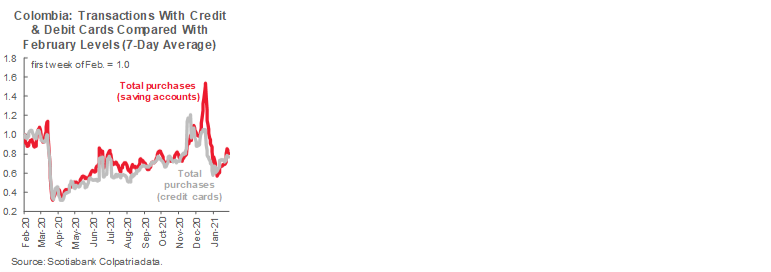

After the first round of lockdowns in 2020, economic agents began to learn how to manage mobility restrictions and mitigate their negative effects, which we saw in January this year when measures were re-imposed. In fact, despite the recent partial lockdowns in Colombia’s main cities, indicators for the first month of the year, such as energy demand and gasoline consumption, showed milder effects from the new round of restrictions (-2.4% y/y and -9% y/y, respectively) than we saw last year. As a result, we estimate that the economic recovery slowed a bit from Q4-2020 into January. But once the peak of the COVID-19 second wave passed at mid-month, restrictions were eased and economic activity picked up again. Activity by Scotiabank Colpatria’s debt- and credit-card clients showed increased consumption of more non-essential items heading into February (second chart), a sign of rising domestic demand.

Therefore, we maintain our constructive view on Colombia’s recovery in economic activity and we still expect GDP growth in 2021 of 5% y/y (see Forecast Updates, p. 2). This unchanged forecast reflects offsetting effects from Q4-2020’s strong results and the mildly negative impact of the latest round of restrictions in January 2021. With the beginning of the country’s mass vaccination program this week, 2021 should see ongoing improvements in Colombia’s economy and, consequently, more price pressures. Higher global supply costs and increased freight charges owing to some bottlenecks in international trade lines are expected to impose pass-through effects on domestic prices. As a result, the BanRep Board is likely to change its negative bias on economic activity at its next monetary-policy meeting on March 26 and keep its benchmark policy rate at 1.75%.

To test our rate forecasts, we ran a hypothetical exercise using our estimates of the BanRep’s reaction function combined with the central bank staff’s current projections for inflation, the output gap, and the neutral real policy rate. We found that even using the BanRep staff’s dovish forecasts, the model implied the need for a slightly lower nominal monetary policy rate during Q1-2021 followed by a quick reversal upward in Q2-2021 owing to a projected pick-up in headline inflation rates. We think economic activity—and price pressures—are set to be a bit stronger than the BanRep staff’s forecasts, which means that the central bank’s own reaction function implies that the BanRep Board is likely to start discussing rate hikes by June this year. It will be important to keep an eye on the Board’s voting composition: we expect unanimity to be restored (the Board’s January 29 decision to hold at 1.75% came via a 5-2 split vote) once economic activity regains some traction and monthly headline inflation begins converging again toward the 3% y/y target.

Mexico—Economic Rebound Remains Driven by Exports Sector; Power Bill in the Pipeline

Eduardo Suárez, VP, Latin America Economics

52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Mexico sees only a few major indicators coming out over the next couple weeks. We expect a slowdown in December retail sales (Feb. 24), which was foreshadowed by the big drop in ANTAD same store sales in January. This could be particularly tough on the sector following a large build in inventories going into the end-2020 holiday season. A similar pattern is likely when we get final and detailed Q4-2020 GDP numbers. Preliminary data showed a second consecutive very strong quarter for net exports owing to solid growth in exports while imports continued to lag. Similarly, investment indicators have been soft. All of this implies that domestic demand remains depressed and the strongest drivers of the recovery continue to be external demand.

On February 1, President Lopez Obrador submitted to Congress a “priority” bill to reform the country’s power sector. Priority initiatives need to be put to a vote in the Chamber of Deputies within 31 days of their unveiling; they then move from the Lower House to the Senate. The priority bill would roll back competition in the sector that had been introduced by the previous administration and establish tiered priorities for energy distribution based on the generator and the energy sourced used, along the following lines:

- Hydro power would be given top priority;

- Traditional power plants operated by the CFE (Comisión Federal de Electricidad), the public-sector power utility, would come next;

- Privately-generated wind and solar would follow; and

- Electricity produced by private-sector gas combined-cycle generators would be the last to be distributed and purchased.

The bill carries with it a range of additional possible implications that could generate some uncertainty for private investment in the sector, where most existing commitments would fall into lower-tier priority segments in the scheme outlined above. The bill would also change the guidelines for the previously established Certificates of Clean Energy (CELs): the bill would make them available to plants constructed before 2014. In addition, the Energy Regulatory Commission (CRE) would be granted discretionary powers, which could include the capacity to revise self-generation power contracts, among other changes.

There are further strategic angles to consider in assessing the possible impact of this bill and its tiered priorities:

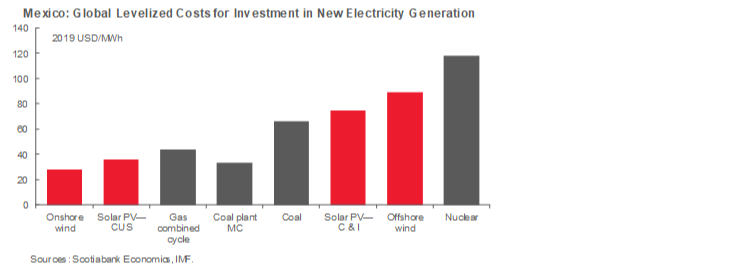

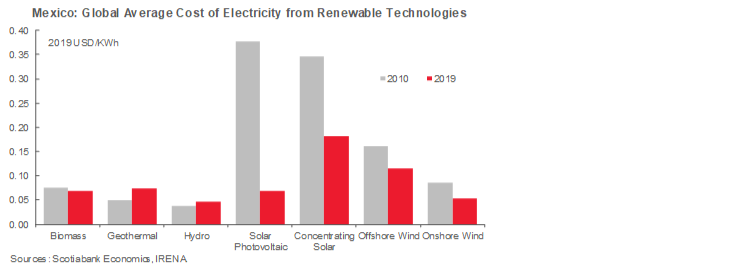

- On a comparison of current costs, renewable energy sources look increasingly attractive versus other options, especially at the scale of major utilities (first chart); and

- Amongst renewable energy sources, the bill would give the highest priority to hydro, whose costs appear to have risen recently, while lower-priority solar and wind have seen big costs reductions (second chart)

At this point, it appears that the bill has support from Morena and could be passed by Congress as soon as this week.

Peru—Politics Dominate the Scene Once Again in February

Guillermo Arbe, Head of Economic Research

51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

A new fault line has emerged at the intersection of COVID-19 with politics. A number of prominent politicians and health officials have been accused of surreptitiously obtaining Sinopharm vaccines for personal benefit. The vaccines had arrived in September, as an addition to doses for use in experimental trials. Reportedly, 487 people received vaccinations without being part of the trials, including ex-President Vizcarra, the Foreign Minister Elizabeth Astete, and the former Health Minister Pilar Mazzetti. Min. Astete resigned as a result of the ensuing scandal; Min. Mazzetti had left her post earlier in February under pressure from Congress over a separate issue. The broader concern is that this new development may provide members of Congress with an opportunity to attempt to undermine the Sagasti government. Moves in this direction, however, are unlikely to be successful given that Pres. Sagasti himself, and most of his cabinet, were not implicated in the situation.

Meanwhile, both businesses and households are awaiting with bated breath the government decision due this week on whether the mobility restrictions currently in place throughout much of the country until February 28 will be extended into March. The government is likely to make an announcement around February 25. The chance of an extension is high, although some modifications to existing rules are also likely.

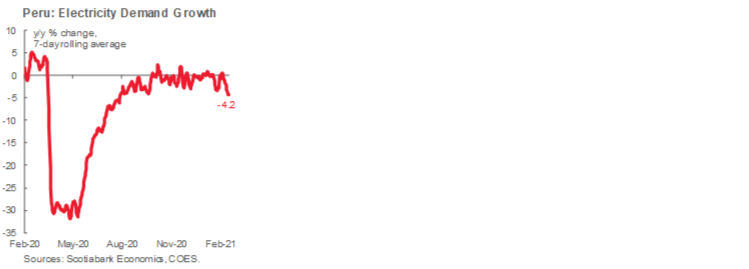

At the same time, we are waiting for the release of data that will give us insight on the magnitude of the impact of the current round of restrictions on the economy. So far, the only data we have is electricity demand, which contracted -4.2% y/y during the week ending on February 17 (chart), after having trended between -1% y/y and -2% y/y in prior weeks.

We will also be looking closely at February inflation data, due out on March 1, given the surprising jump to 2.7% y/y in January from 2.0% y/y in December. The trend so far in February implies that yearly inflation is still crawling up toward the 2.8% y/y region.

Meanwhile, the PEN continues to be under pressure, forcing the BCRP to become more active in offsetting USD demand from corporate businesses. The FX rate has been hovering in the USDPEN 3.64–3.67 region and would likely be higher if not for BCRP intervention. We had anyway been expecting a weakening of the PEN at this time of the year, as frequently occurs in the months before presidential elections. What happens to the PEN after the April vote will be telling. It is unclear whether external account fundamentals will impose themselves to strengthen the PEN or whether corporate demand for USDs will be an ongoing feature of the FX market.

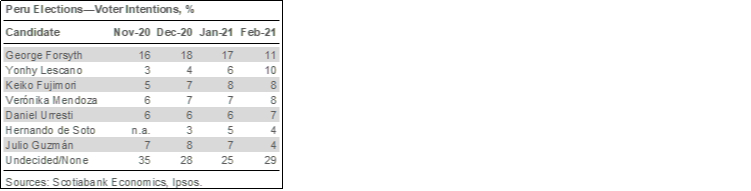

We are now only six weeks away from the April 11 presidential elections and the field continues to be quite open. There were some ripples domestically after a new Ipsos poll showed Yonhy Lescano (Acción Popular) closing the gap in voter intentions with the leading candidate, George Forsyth, thereby turning Lescano into someone to be reckoned with (table). However, this is just one poll, and, by Peruvian standards, we are still early in the game. In the past, voter intentions have frequently changed dramatically up to two weeks before previous votes. Note, also, that only seven percentage points separate the top seven candidates in the polls. Furthermore, undecided voters equal the combined share of the top three contenders’ supporters. The race can’t really get more open than this. A second-round vote in June is a certainty, but the two final candidate’s names remain up in the air.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | carlos.munoz@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.