Central banks & macro data: A very quiet week

Colombia: A robust end to 2020 as BanRep’s Board gets a new member

Mexico: Job creation rose slightly in January, but remained down compared with a year ago

Peru: December showed first year-on-year GDP gains since February 2020; labour market ended January on encouraging note

CENTRAL BANKS & MACRO DATA: A VERY QUIET WEEK

This is a quiet week in both central bank developments and data releases across the Pacific Alliance countries (PACs). No regular monetary-policy decisions are scheduled this week in the PACs. Similarly, the highlight of the week for new data fell yesterday, Monday, February 15, with the release of Colombia’s December and Q4 2020 GDP data, as well as Peru’s December 2020 monthly economic activity print. Peru’s Q4-2020 detailed GDP data are due on Thursday, February 18.

—Brett House

COLOMBIA: A ROBUST END TO 2020 AS BANREP’S BOARD GETS A NEW MEMBER

I. Broadly favourable manufacturing and retail data for December

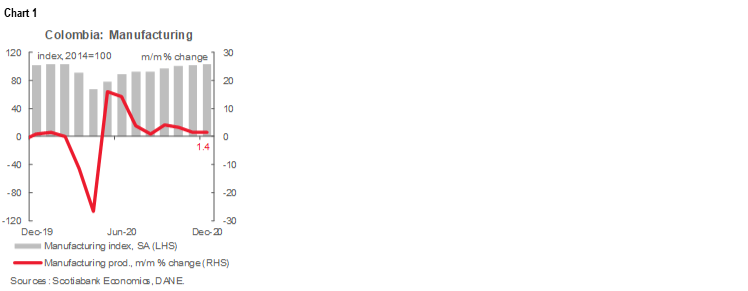

On Friday, February 12, DANE published manufacturing production and retail sales data for December that were broadly favourable. Manufacturing improved and posted year-on-year gains, while retail sales eased since the VAT holiday in November pulled purchases forward from December. However, on balance, we think the print was solid since the combined two months of November-December saw retail sales gains of 2.1% y/y. Employment remained down in both sectors—by -4.8% y/y in manufacturing and -7.2% y/y in retail—with the annual shortfalls concentrated mainly in clothing-related sub-sectors.

Manufacturing. December manufacturing posted the first year-on-year gain since the pandemic began, but the sector’s employment numbers remained below pre-pandemic levels. Annual growth in manufacturing production grew by 1.5% y/y in December, better than expected by the Bloomberg consensus of 0.8% y/y, and the first positive print since March, when the pandemic started. Manufacturing production significantly improved with the economic re-opening: in December, we saw sequential 1.4% m/m sa growth, similar to November’s figure (chart 1). Manufacturing production surprised us since we expected a weaker year-on-year expansion in December, which keeps us constructive on the sector’s prospects for 2021.

Over the whole of 2020, manufacturing production contracted by -8% y/y, while employment fell -5.8% y/y. Over the last year, output in 22 out of 39 sectors contracted in year-on-year terms; in December the balance was 26/39, but this was a reasonably good result compared with the worst of the pandemic. Throughout 2020, six sectors accounted for 62.5% of the year’s total contraction in manufacturing: beverages (-9.7% y/y), oil refining (-13.9% y/y), clothing (-25.3% y/y), construction-related mining industries (-12.8% y/y), iron and steel products (-21.2% y/y), and vehicles (-38% y/y). Activity in these sectors has been strongly affected by mobility restrictions and weaker demand. On the positive side, essential food-related industries grew at rates above 3% y/y. Manufacturing’s 2020 contractions were regionally concentrated in Bogota and Antioquia, which accounted for almost half of the sector’s annual downturn.

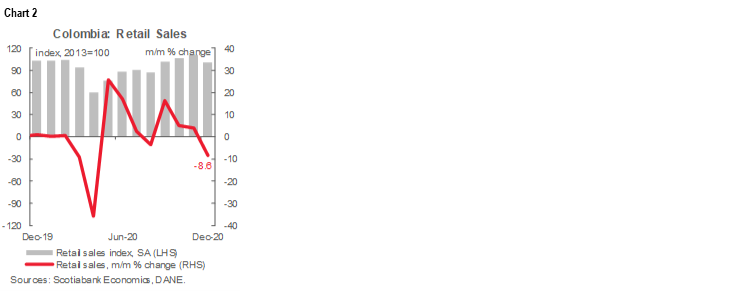

Retail. Retail sales were down -2.8% y/y in December, which reflected the hangover from November’s VAT holiday, and were well below the Bloomberg consensus expectation of an expansion of 2.1% y/y. In seasonally-adjusted terms, total retail sales, ex-other vehicles, fell by -8.6% m/m in December (chart 2).

For 2020 as a whole, retail sales fell by -7.8% y/y, although the composition was more of a mixed bag since subsectors’ performances varied strongly in reaction to mobility restrictions. The largest gains were registered in retail sales of food (6.5% y/y), computer equipment (28.5% y/y), cleaning products (21.2% y/y), and home appliances (9.4% y/y), while annual sales losses hit hardest in gasoline (down -14.5% y/y), vehicles for household use (off -21.3% y/y), other vehicles (down -23.5%y/y) and clothing (-28% y/y). By region, Bogota accounted for half of 2020’s retail contraction since the capital saw the toughest restrictions.

To sum up, December’s coincident manufacturing and retail indicators posted positive activity levels, which confirmed that the economic recovery is remaining on track with the re-opening. Still, the labour market remains a big concern since employment was down compared with 2019 even though year-on-year production levels were up.

The relative strength in manufacturing and retail at end-2020 keeps our view intact that the BanRep will eschew further rate cuts.

II. Jaime Jaramillo Vallejo is the new BanRep Board member

On Friday, February 12, President Duque named Jaime Jaramillo Vallejo to BanRep’s Board to replace Arturo Galindo, who has resigned due to personal issues.

Jaime Jaramillo has a Ph.D. in economics from Boston University and more than 40 years of experience in institutions such as the International Monetary Fund (IMF), the World Bank, the Asian Development Bank, and locally, the National Planning Department (DNP). Jaramillo’s work has been focused in macroeconomic policy, monetary policy, and financial stability. He will undoubtedly contribute his strong technical background to the Board’s deliberations and help maintain BanRep’s independence. Although the recent appointments of Bibiana Taboada and Mauricio Villamizar could skew the Board a bit to the dovish side, we think Jaramillo’s arrival will provide some balance with a focus on technical, orthodox perspectives.

Mr Jaramillo’s CV is posted on the BanRep site here.

III. Real GDP in Q4-2020 posted a robust response to re-opening to end 2020

Q4-2020. In data out on Monday, February 15, Colombian real GDP fell by -3.6% y/y in Q4, better than both the consensus expectation of -4.5% y/y, and our forecast of -6.2% y/y (chart 3). On a sequential basis, the economy gained 6.0% q/q sa; although this represented a moderation from the 9.4% q/q sa growth we saw in Q3, it was still a healthy expansion. The Q4 numbers confirmed that the economy reacted more strongly than expected to re-opening measures, especially in industry and some services-related sectors.

During Q4, the Colombian economy consolidated the effects of the "new normal" re-opening scheme that started in September. The plan has broadly allowed more than 95% of economic activity to resume and it has been boosted by special measures, such as the VAT holiday in November. End-2020 activity data imply a solid hand-off to 2021, with the economy increasingly able to cope better with new lockdowns and adapt quickly to changing conditions.

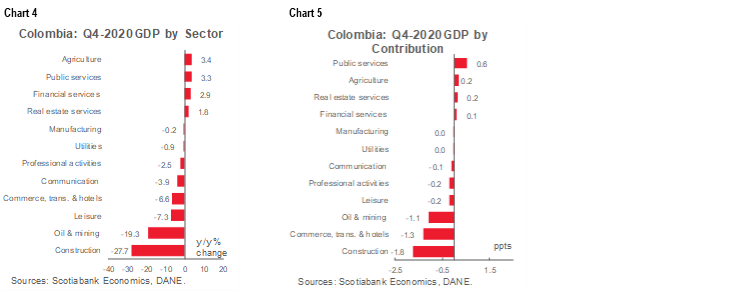

From the supply-side, some of the worst performing sectors in Q4-2020 were construction (-27.7% y/y); mining (-19.3% y/y); and commerce, transport, and hotels (-6.6% y/y)—which together subtracted -4.2 ppts from the quarter’s topline GDP growth rate (charts 4 and 5). On the positive side, agriculture (3.4% y/y), public services (3.3% y/y), and real estate activities (1.8% y/y) dominated, contributing 1 ppt to the overall year-on-year growth rate for the quarter. One thing to highlight is that, according to the monthly economic activity index (ISE), by December, 5 out of 12 sectors showed annual gains, the best balance since the pandemic began. Some other sectors continued closing their gaps from a year before, which altogether puts the economy on a solid recovery path.

It is worth noting that some previous quarters saw revisions: (1) Q1 growth was shaved from 1.2% y/y to 0.7% y/y; and (2) Q3 growth was lifted a touch from -9.0% y/y to -8.5% y/y. The changes were driven by weaker construction estimates and better numbers in leisure-related sectors.

On the demand side, domestic demand fell by -3.5% y/y in Q4 (chart 6) on the back of a 6.0% q/q sa sequential gain. Private spending contracted by -0.8% y/y, but grew by 8.0% q/q sa (close to the Q3 figure of 8.2% q/q sa) on better durable goods consumption growth (up 12.8% q/q sa and 8.6% y/y) amid November’s VAT holiday; services consumption remained weak compared with a year ago (-4.9% y/y), but it expanded by 11% q/q sa from Q3, indicating that progress on the re-opening allowed more significant social interactions in Q4.

Government spending was up 4.0% y/y in Q4, the best expansion in the year, while in q/q sa terms it grew by 0.5%. Investment was down in a similar way to Q3 (-17% y/y) owing to a modest 1.2% q/q sa gain in Q4. Investment remained at the weakest levels since Q1-2013, particularly reflecting soft construction activity. On the positive side, machinery spending grew by 0.5% y/y.

Net exports contributed only marginally to Q4-2020 growth (0.3 ppts, chart 7) because imports expanded (6.6% q/q sa), while exports contracted (-1.5% q/q sa), compared with Q3. Global demand for mining production weighed on exports, while recoveries in domestic consumption and investment activities drove demand for imports up from Q3 to Q4. Having said this, we continue to estimate a current account deficit of -3.2% of GDP in 2020, while in 2021, it would widen to -3.8% of GDP as a result of the domestic demand recovery.

2020. All in all, the Q4 data closed 2020 with real GDP down -6.8% y/y for the year as a whole, which was better than consensus (-7.2% y/y), BanRep’s forecast range (-6.8% y/y to -7.4% y/y), and our own forecast of -7.5% y/y (see the February 8 Latam Weekly). These results should moderate somewhat the central bank staff’s inclination toward additional cuts in the BanRep’s key policy rates.

Commerce, transportation & hotels (-15.1% y/y), construction (-27.7% y/y—coincidentally the same as the Q4 y/y figure) and mining (-15.7% y/y) accounted for 85% of the full-year economy-wide contraction in 2020. The first two sectors were driven by weaker domestic demand, while the mining dynamic reflected anaemic global demand. On the positive side, agriculture was the best performing sector (up 2.8% y/y), showing that essential consumption prevailed during the pandemic. That said, by the end of 2020, GDP quarterly production stood only at levels similar to those observed in Q4-2018 (chart 8)—with an even longer road still to go to get back to full-year 2019 levels.

For 2020, private consumption was a particular drag on economic growth, since the recession hit households hard. Consumption was focused on staples, with a little help on durables from VAT holidays in June, July, and November—but at -7.5% y/y it came in a touch better than the BanRep staff’s expectation of -7.7% y/y. Investment’s pullback (-17.1% y/y) was also smaller than expected by the central bank (-18.1% y/y), especially in view of the weakness in the construction sector (both civil works and building construction); machinery and equipment drove the upside surprise. These data have important implications for calculations of the economy’s overall output gap and lend further support to our view that the BanRep is unlikely to cut again in this cycle.

The fourth quarter data implied that further re-opening led to improvements in economic activity and we expect the economy to continue notching up gains in 2021. The Q4-2020 real GDP numbers confirmed that Colombia has overcome the worst of the current crisis and rebounded faster than we previously expected. Still, challenges remain as the country’s main cities imposed new lockdowns in early 2021. As a result, despite 2020’s solid hand-off, we are maintaining our 5.0% y/y forecast for growth in 2021. We continue to expect BanRep to keep its monetary policy rate at 1.75% in the coming months as it waits for further information on the inflation rebound before deciding to take any action.

—Sergio Olarte & Jackeline Piraján

MEXICO: JOB CREATION ROSE SLIGHTLY IN JANUARY, BUT REMAINED DOWN COMPARED WITH A YEAR AGO

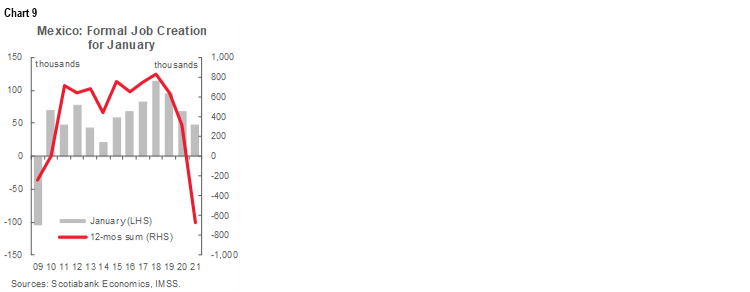

According to data released on Friday, February 12 by IMSS (the Mexican Institute of Social Security), formal jobs totaled 19.822 mn in January. This was below the 20 mn mark for a second consecutive time. Formal job numbers surpassed that watermark in November after a seven-month trend below the 20 mn threshold, but the labour market hasn’t been able to sustain those gains. January’s monthly increase of 42.9k jobs followed the usual drop in December and represented the weakest January job gains in seven years (chart 9). This marginally widened the labour market’s gap compared with a year ago from -3.2% y/y to -3.3% y/y, for a total of 10 consecutive months of year-on-year declines—a run that hasn’t been seen since 2008–09.

By sector, the annual decline in formal employment was centred in business services (-9.9% y/y), construction (-6.0% y/y), extractive industries (-5.4% y/y), commerce (-2.4% y/y), electricity (-0.5% y/y), and transportation & communication (-0.1% y/y). Gains registered in the agricultural (0.7% y/y), social services (0.3% y/y), and processing (0.1% y/y) sectors were insufficient to offset those other year-on-year losses.

The number of formal employers affiliated to the Institute (999,042) decreased for the second consecutive month (by -1,372 businesses). In an annual comparison, the number of IMSS-affiliated employers edged back for a fourth consecutive month, going from -0.1% y/y to -0.2% y/y.

Finally, the average salary of formal workers was MXN 428.8 (USD 21.4) per day as of January 31, equivalent to a nominal annual increase of 8.2% y/y. IMSS noted that this was the steepest gain in any January during the past decade, surpassing the 6.0% y/y gain recorded in January 2019.

—Miguel Saldaña

PERU: DECEMBER SHOWED FIRST YEAR-ON-YEAR GDP GAINS SINCE FEBRUARY 2020; LABOUR MARKET ENDED JANUARY ON ENCOURAGING NOTE

I. Out of the red! Annual GDP growth was positive in December at 0.5% y/y—the first time since COVID-19 struck

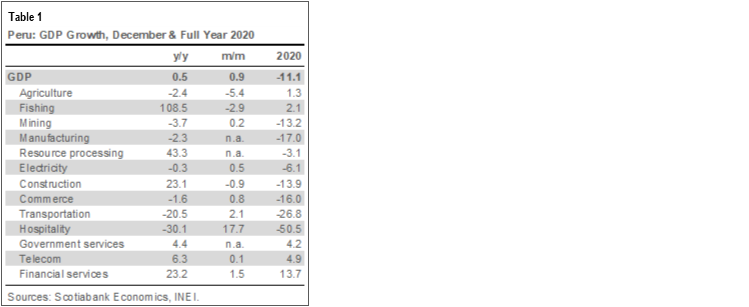

December real GDP growth came in at 0.5% y/y, according to official figures published on Monday, February 15 by the National Statistics Institute (INEI, chart 10). The result for December was not as surprising as one might think, considering that the consensus and ourselves expected a contraction in the vicinity of -1% y/y. The range of uncertainty surrounding monthly results in these unusual times is more than wide enough to encompass a mild shift from negative to positive. The result was encouraging, though, as it was further evidence of the strength of the recovery prior to the second, current, wave of COVID-19.

Real GDP growth for the full-year 2020 was -11.1% y/y (table 1). This was mildly better than our forecast of -11.5% y/y. To put this in perspective, as recently as last October the consensus forecast for 2020 GDP was at -12.8% y/y (LatinFocus Consensus Forecast). During much of the year, it seemed possible that 2020’s contraction in real GDP would be the deepest since the Great Depression. As it turns out, it came in narrower than the -12.3% y/y decline during the hyperinflation year of 1989.

Only agriculture, fishing, government services, telecom, and financial services grew for full-year 2020 (table 1 again). These were all sectors that were never locked down, and at the same time were either not linked to domestic demand, or supported by special circumstances (e.g., telecom-distance working/learning; financial services-Reactiva, etc.).

In December, six major sectors showed positive year-on-year growth, and an equal six contracted. In month-on-month terms, all but three major sectors grew.

Fishing pushed year-on-year growth into positive territory in December. Although fishing only represented 0.74% of GDP, its 108% y/y growth was strong enough to add 0.8 percentage points to the month’s headline expansion. November was the beginning of the fishing season, which ended in January. Agriculture was the biggest surprise to the downside, falling -2.4% y/y and -5.4% m/m. December was the first month of the rainy season, but this does not seem to be the cause of the pullback: agriculture growth has been erratic all year. Uncertainty relating to demand and distribution logistics may be the greater issue.

Although manufacturing (-2.3% y/y) and commerce (-1.6% y/y) both declined in annual terms during December, the contractions were small, and commerce recorded sequential growth of 0.8% m/m. The annual gains in construction were fully anticipated by leading indicators, but the persistence of growth in financial services is more of a surprise given that the Reactiva program is pretty much over.

II. Labour market ended January on encouraging note

The National Statistics Institute also released on Monday, February 15, fairly encouraging employment information for the moving quarter Nov. 2020–Jan. 2021. Once again, the unemployment rate has improved more than expected, coming in at 13.0% for this three-month period. This was better than our forecast of 13.8%, and represented a sharp decline from unemployment rates north of 16% just a few months ago. This still represented an -11.9% y/y decline in jobs in the moving quarter. It was interesting that employment actually rose in commerce, up 1.7% y/y, which is, perhaps, a reflection of the demand for delivery services and out-of-work Peruvians reinventing themselves as salespeople. This would be in line with a reported -12.4% y/y decline in average monthly salaries, as new jobs that are being created are paying less than those lost.

—Guillermo Arbe

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.