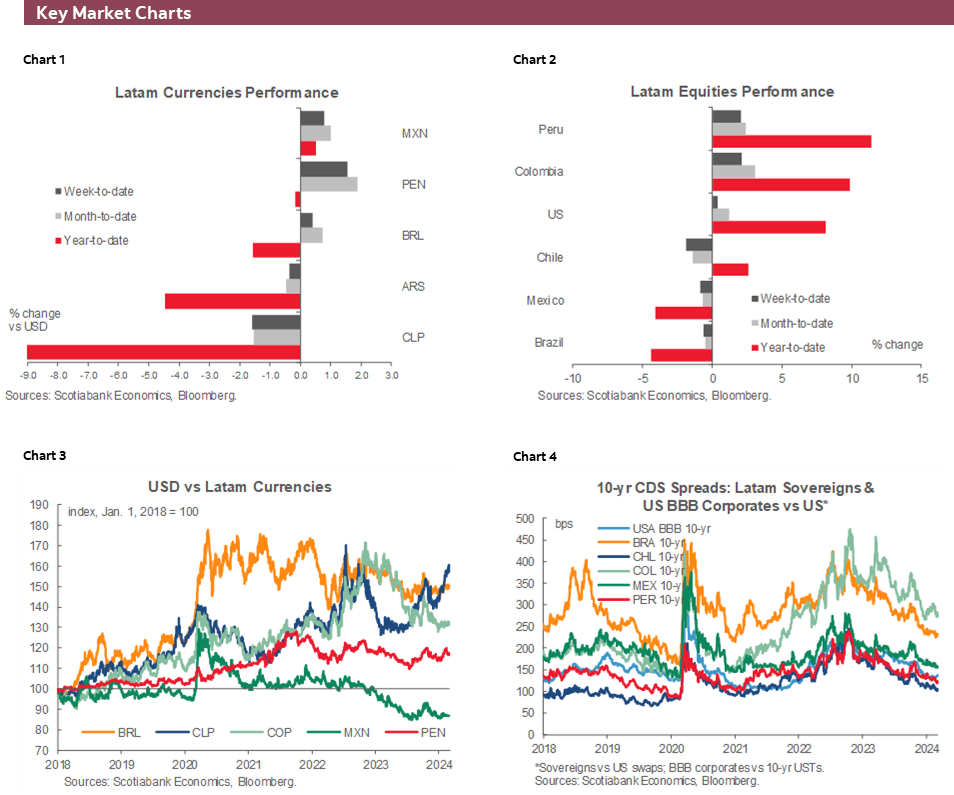

ECONOMIC OVERVIEW

- The key Latam week did not disappoint. Thursday and Friday CPI beats in Colombia and Chile, and a surprising rate hold by the BCRP caught local markets off-guard.

- After a packed week in the Pacific Alliance, we now have a relatively quiet few days where comments by regional central bankers (and global data) may be an important risk for local traders unsure about upcoming policy announcements.

- Peru GDP and Colombian macro figures for January are the Pacific Alliance data highlight. In Brazil, we get the last of the key regional inflation figures for February.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia and Peru.

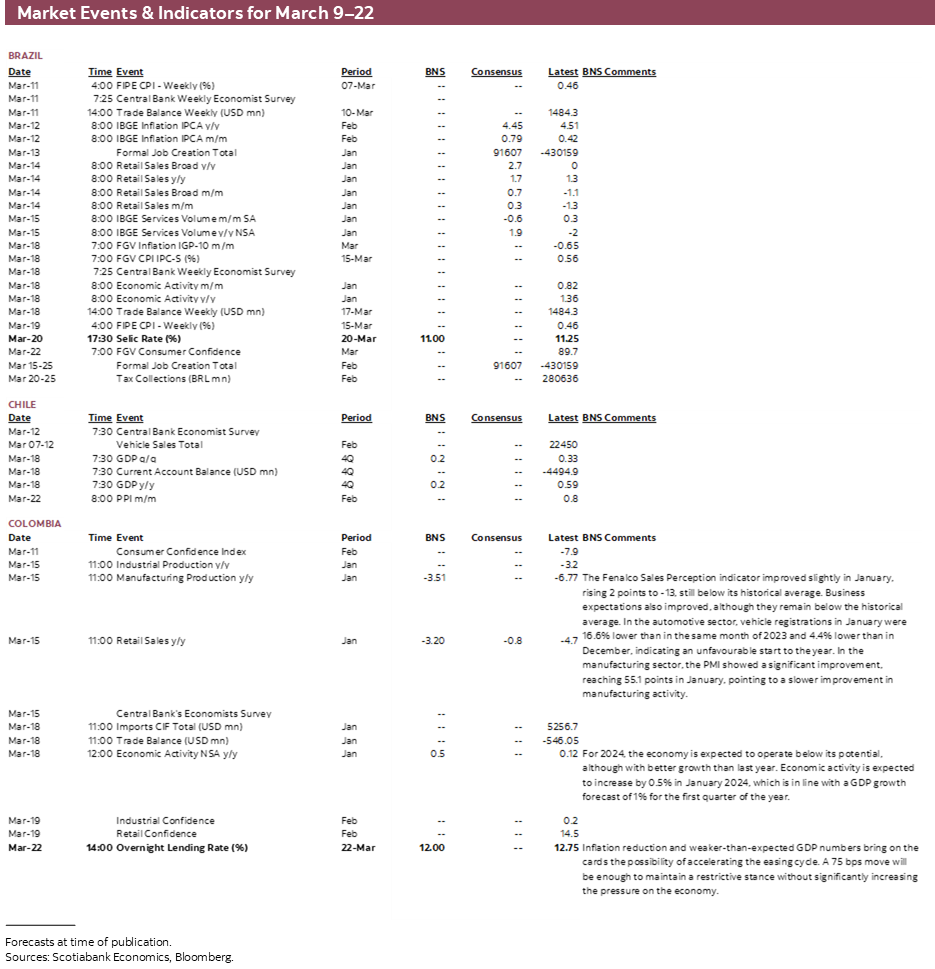

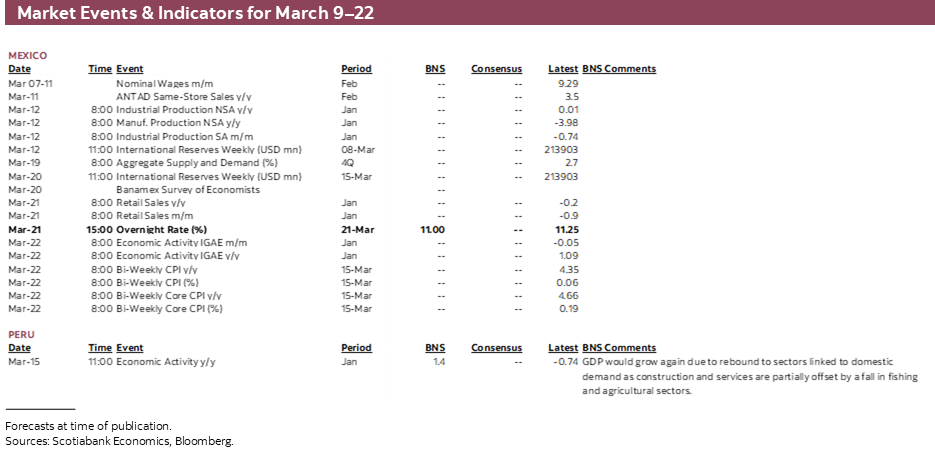

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period March 9–22 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: PERU GDP, COLOMBIA MACRO, AND BUSY EX-LATAM WEEK

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- The key Latam week did not disappoint. Thursday and Friday CPI beats in Colombia and Chile, and a surprising rate hold by the BCRP caught local markets off-guard.

- After a packed week in the Pacific Alliance, we now have a relatively quiet few days where comments by regional central bankers (and global data) may be an important risk for local traders unsure about upcoming policy announcements.

- Peru GDP and Colombian macro figures for January are the Pacific Alliance data highlight. In Brazil, we get the last of the key regional inflation figures for February.

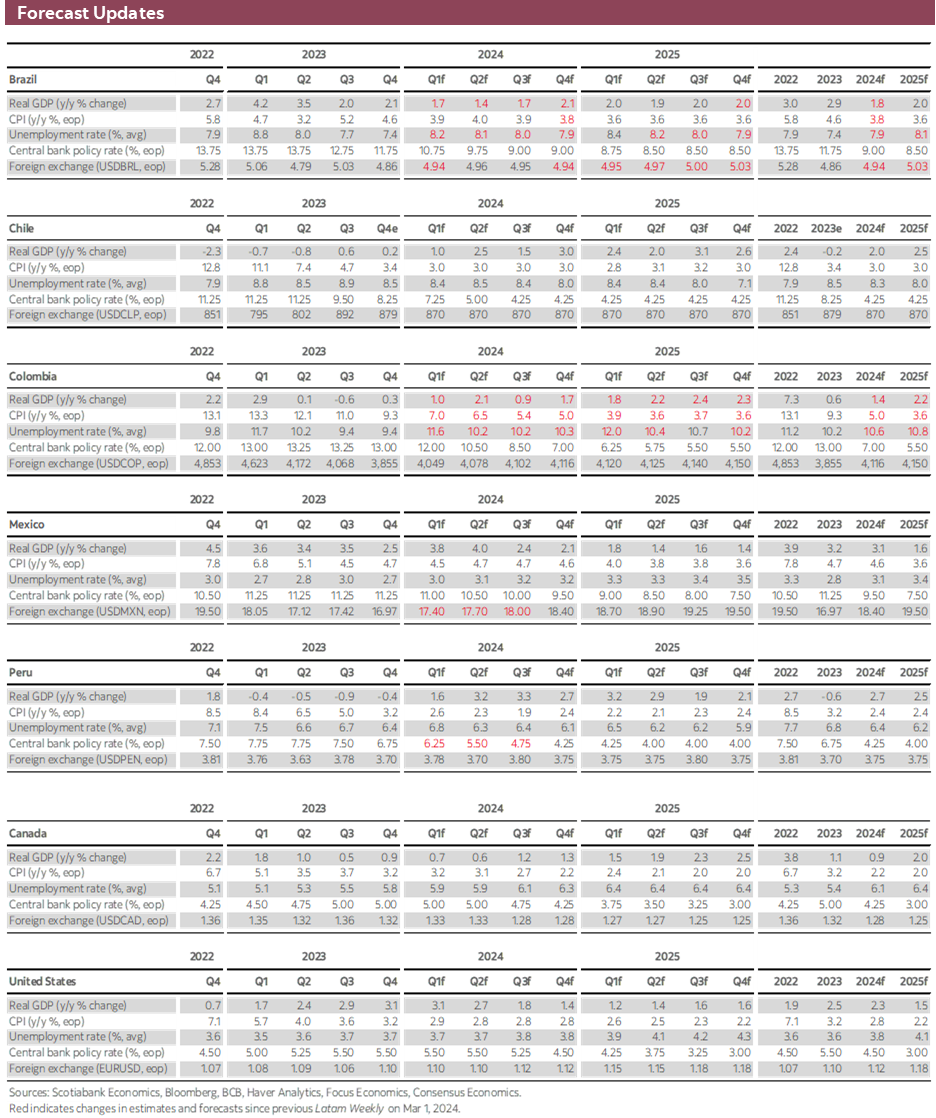

The key Latam week did not disappoint. Although things started out quietly with no major data of note, Thursday and Friday CPI beats in Colombia and Chile, and a surprising rate hold by the BCRP caught local markets off-guard and heightened uncertainty around the path for monetary policy in the region. In contrast, Mexican inflation readings were aligned with bi-weekly data released two weeks prior, with limited takeaways for rate expectations.

Outside of the region, there weren’t many surprises from the ECB nor the BoC, and US data prior to Friday’s jobs report generally came in line with expectations. Powell noting the Fed is not far from the required confidence for cuts had been the highlight for global rates markets this morning before the (weak under the hood) US labour report triggered a chunky rally. Next week, the ex-Latam calendar has US CPI, UK jobs/wages/GDP, Chinese CPI, and the PBoC’s decision as the main things to watch between today and Friday.

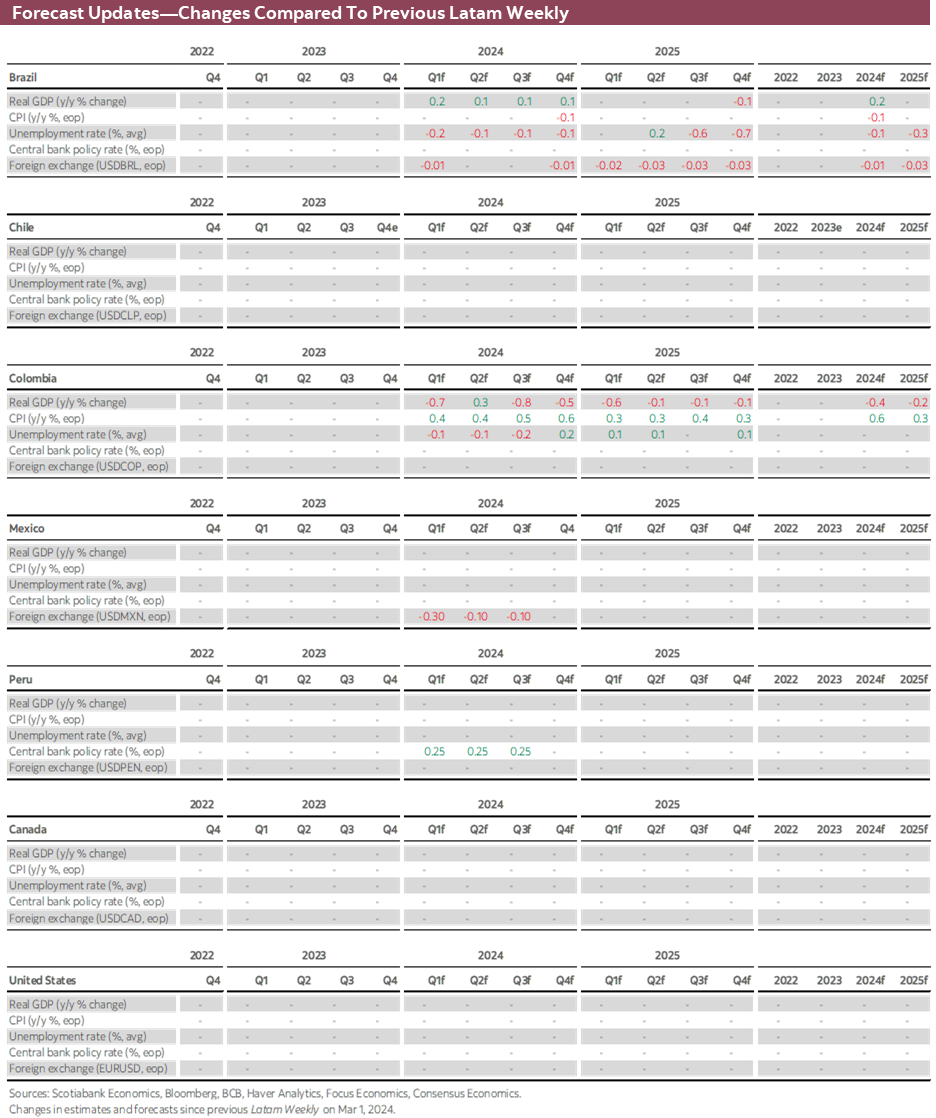

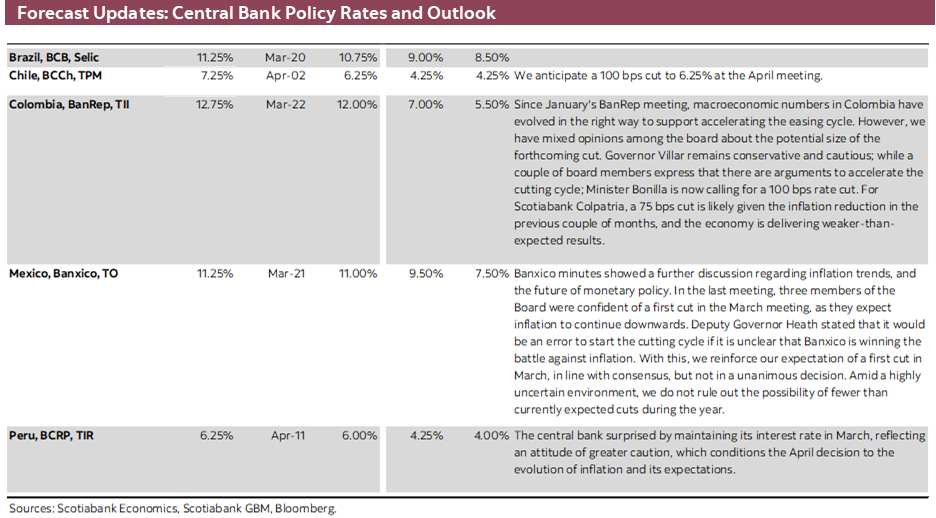

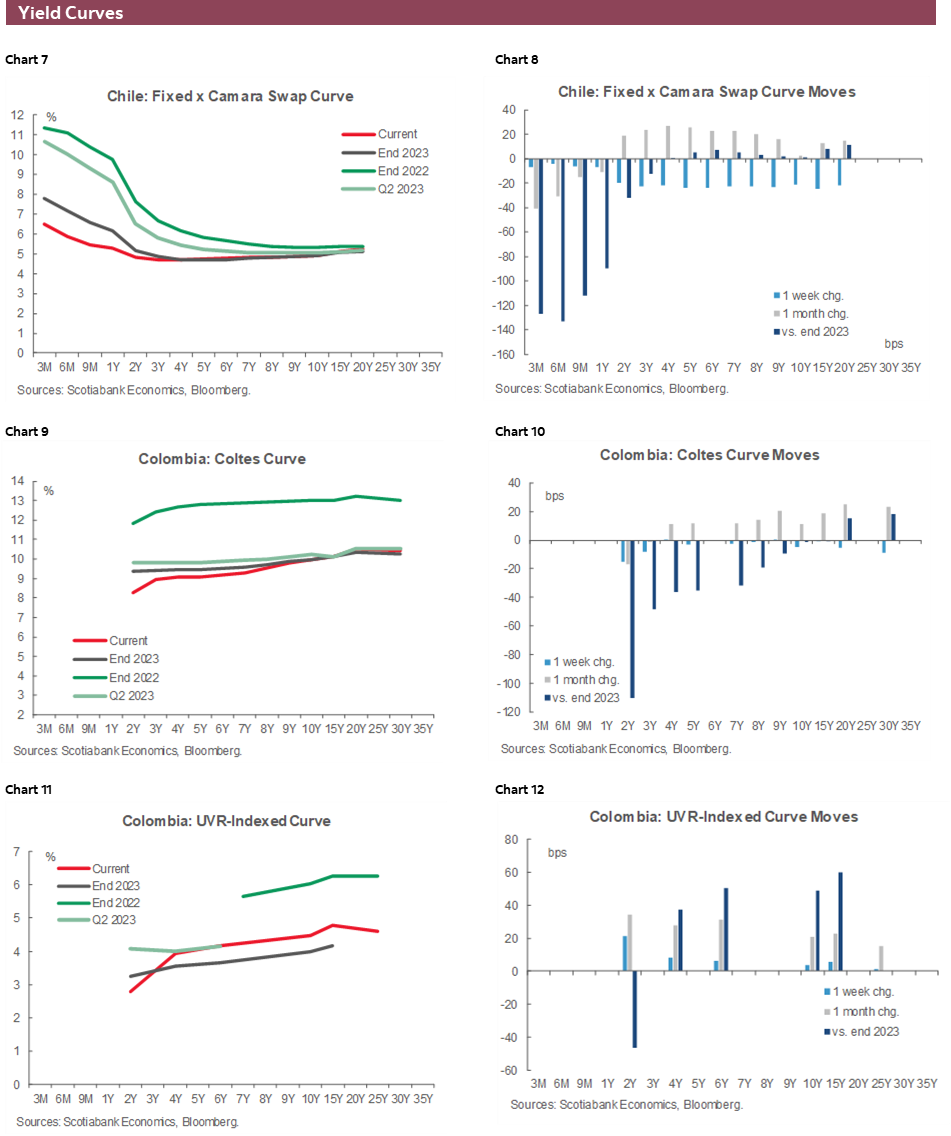

After a packed week in the Pacific Alliance, we now have a relatively quiet few days where comments by regional central bankers may be an important risk for local traders unsure about upcoming policy announcements. Our economists’ calls of respective 75bps and 100bs cuts by BanRep and the BCCh at their upcoming decisions were challenged by above consensus inflation data that raise the odds of smaller moves—and, accordingly, our Chile colleagues now see ‘only’ a 75bps move next month.

Colombia’s economy has also looked better than we expected, so in today’s report our economists in Bogota discuss their upward revision to their growth projections on a better outlook for private consumption. Still, their 75bps call is left unchanged. Friday’s January industrial/manufacturing production and retail sales data will help us refine forecasts for economic activity figures that come out on the 18th. With these, we may have more clarity on what BanRep will do on the 22nd as the next prices release is not until early-April.

There’s also no more CPI data on the calendar prior to the BCCh’s April 2nd meeting, and there are limited on-calendar triggers for cuts repricing in coming days. The only figures that may make a difference, January sectoral output and economic activity data, do not come out until late-March/early-April. So, as far as BCCh expectations go, it will be up to local officials to give their take next week on the latest prices readings and whether these change their view on the return to on-target inflation.

Peru’s central bank surprised everyone with its rate hold decision, but then gave us no clear reason for why it chose to do this. Hopefully we get some colour from them next week. Though it did not cut the reference rate, the bank lowered reserve requirements (RR)—a rare policy adjustment—which suggests the BCRP is still keen on providing support for the economy.

Maybe stronger than expected inflation in February prompted a more cautious rates approach from a bank that has policy meetings every month. Maybe the firming up of expectations that the Fed will not cut earlier than June means the BCRP has to be more mindful of the US-Peru rate differential and so can’t cut every month. Now, it is important to note that the RR reduction results in an immediate liquidity injection, and its 50bps.

December GDP data showed that Peruvian economic activity surprisingly contracted by 0.7% y/y in the final month of 2023, for an annual contraction of 0.6%. Next Friday’s release of January GDP should show a solid start to the year for Peru’s economy. In today’s report, the team outline their projection of 1.8% y/y growth as well as their expectation that inflation will fall below the 3% ceiling in March. They also discuss the latest political developments in the country and possible implications.

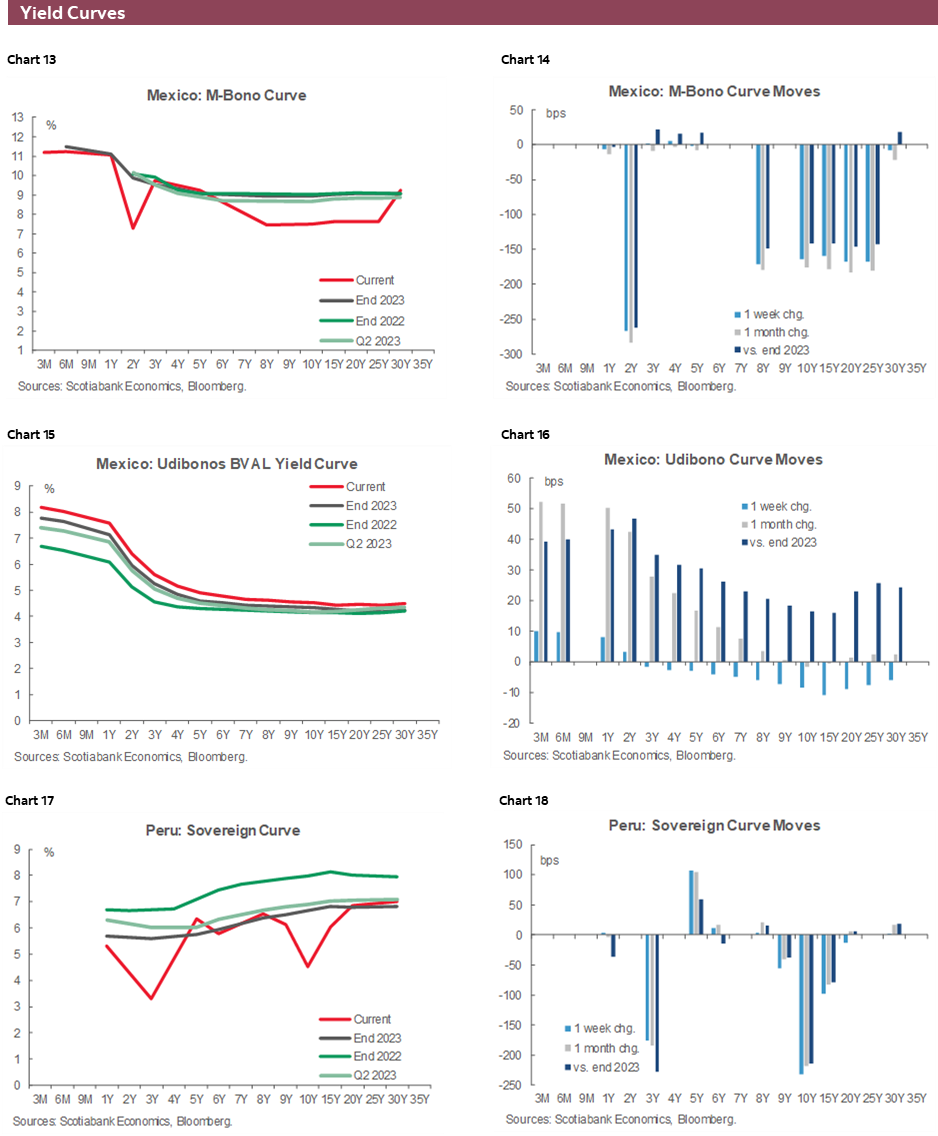

Mexican inflation data were certainly not as exciting as those from Colombia and Chile so most determinants still point to Banxico kicking off the easing cycle on the 21st. There’s still some anxiety around this and whether the central bank will start out slowly with rate cuts, perhaps skipping some meetings; it may also be sensitive to rate differential vis-à-vis the Fed. There’s not much in Mexico’s calendar next week to change our and the market’s opinion, but we’ll keep an eye on Tuesday’s industrial and manufacturing production data as a forecasting input for January economic activity figures out the day after Banxico’s meeting.

Brazil’s IBGE is the last of the key countries in the region to release CPI data for February, on Tuesday, with economists expecting a modest deceleration in headline inflation in year-on-year terms, but with monthly headline and core inflation picking up which may add to the idea that the BCB will soon shift to a lower pace of cuts—at one of its May or June decisions. Retail sales and services volumes data are also on tap.

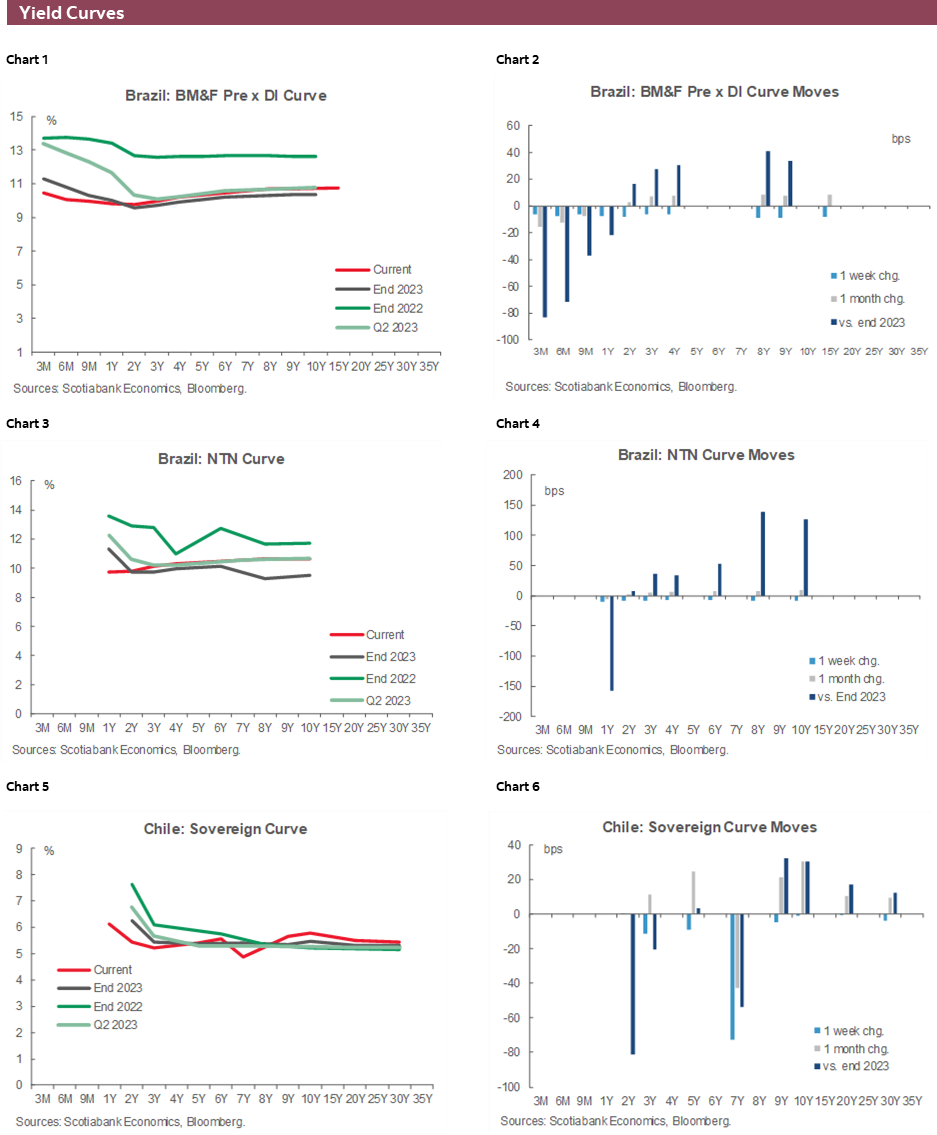

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—Macro Dilemmas that Motivate the Caution Before the Action

Sergio Olarte, Head Economist, Colombia

+57.601.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.601.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

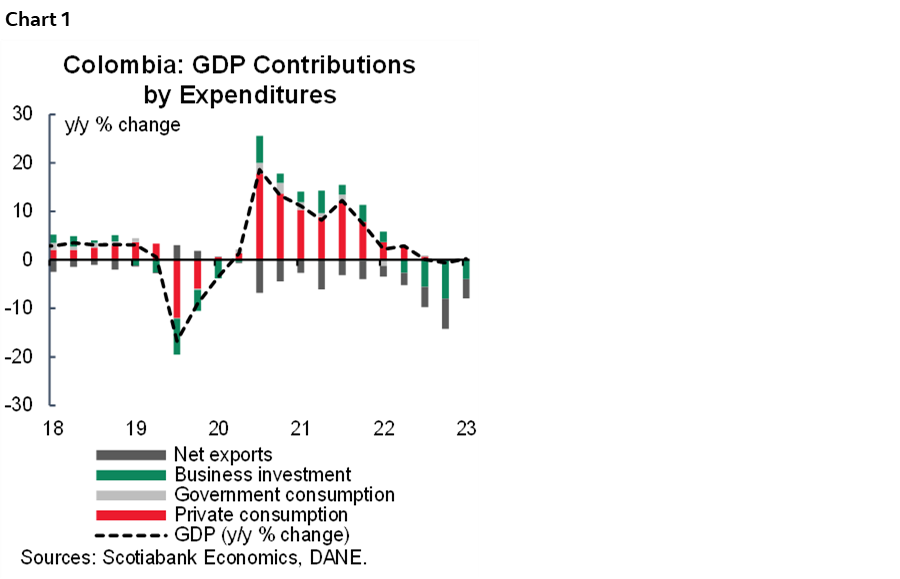

Colombia’s macro picture is far from being simple; economic activity delivered a negative surprise in 2023, posting a weaker-than-expected GDP growth of 0.6% that reflected a significant moderation in the domestic demand (chart 1), going from an expansion of 7.6% in 2022 to a moderate 2.3% growth in 2023, especially amid a deceleration in private consumption, passing from an expansion of 9.4% in 2022 to 1.2% in 2023, and a significant contraction on investments (-26.0% in total investments including inventories changes), all in a context in which the public sector wasn’t effective in implementing the fiscal budget. The previous picture was revealed on February 15th, and since then, many relevant actors in the economic scenario have highlighted the need of better and sharper action from policymakers, emphasizing that the main target currently should be to make the Colombian economy achieve a recovery and high quality path for economic growth to make it sustainable. In fact, this is also a medium-term concern for the credit rating agency S&P. That said, amid recent economic data at Scotiabank Colpatria Economics, we revised the GDP growth forecast for 2024 to 1.4% as private consumption is expected to recover in the second half of the year, while the recovery in investment is expected to start due to an increase in inventories in the H1-2024, while in the H2-2024, we expect a better contribution from private projects.

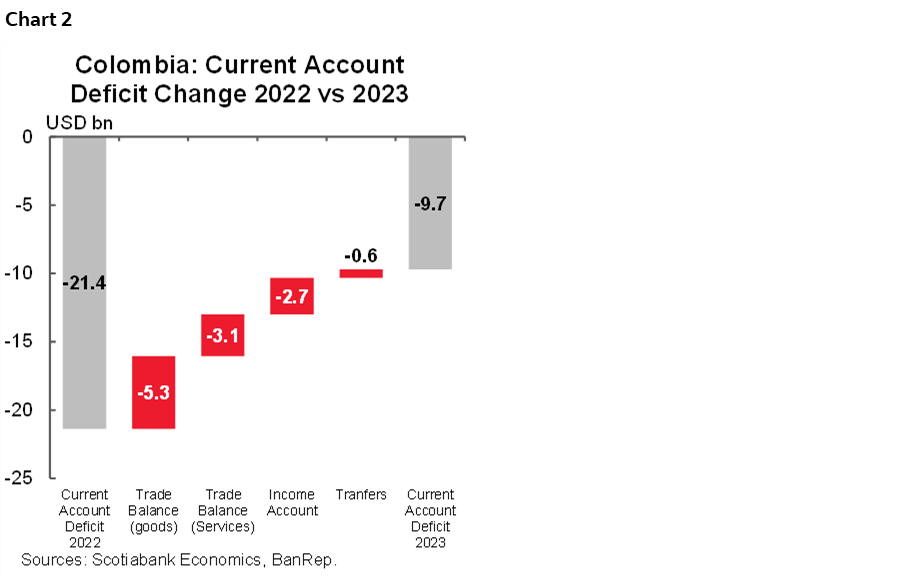

Economic activity deceleration drove an important reduction in the current account deficit, which fell from USD 21.4 bn in 2022 to USD 9.72 bn in 2023 (~-55% y/y), which as a proportion of GDP represents a reduction from 6.2% deficit to a deficit of 2.67% of GDP, the main driver in the deficit reduction was the lower trade deficit of goods (chart 2), in which the contraction in imports (-17.1% y/y) outpaced the contraction in exports (-11.7% y/y). That said, the external deficit mirrored the weakening of domestic demand and contributed to moderate FX upside pressures observed during 2022 when the economy exhibited a strong activity that was also reflected in historically high imports. Ahead of 2024, the current account deficit is projected at 3.5% of GDP (~USD 13 bn), which will be compatible with a mild recovery in domestic demand and the increase in international purchases to rebuild inventories.

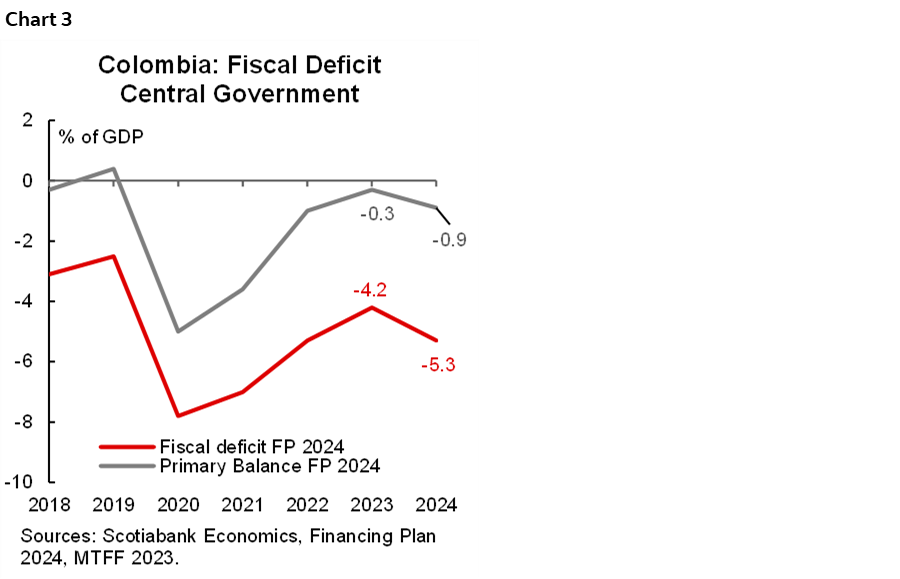

In the case of fiscal accounts, the almost straightforward overcompliance of the fiscal rule could face challenges. In 2023, the fiscal deficit was reported at 4.2% of GDP (primary deficit of 0.3% of GDP), while the target for 2024 is to widen the deficit towards 5.3% of GDP (primary deficit of 0.9% of GDP, chart 3). The context of a negative output gap poses a challenge for tax revenues but also allows the government to manage a higher deficit. In any case, we think that there is confidence in the compliance of the fiscal rule; however, what concerns us the most is the implementation of the budget and the quality of the fiscal spending, especially when the economic activity is still weak and a boost from the public sector is more than needed.

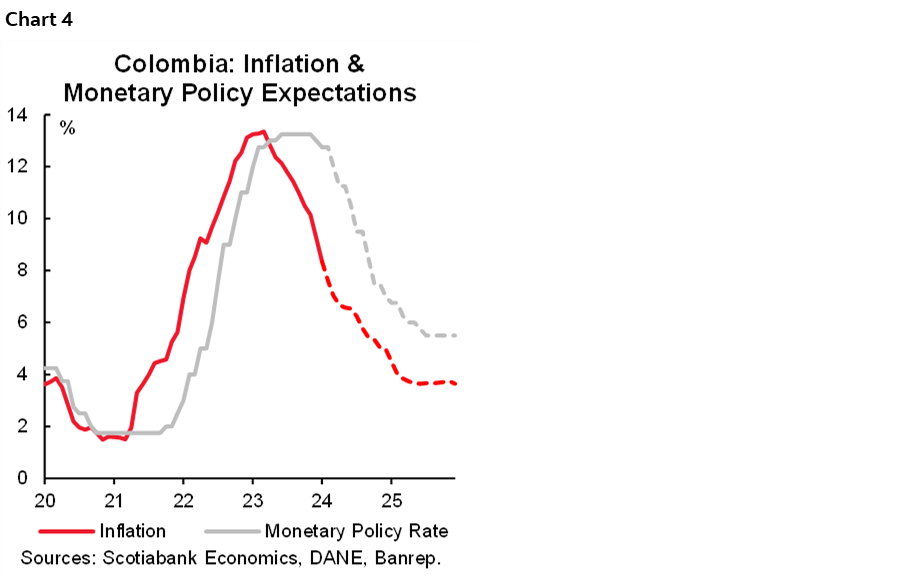

On the prices side, recent results demonstrate that the strongest disinflation phase has started. Statistical base effects and lower indexation are the two key components for the inflation reduction. January and February’s inflation cumulated more than a 150bps correction vs the inflation at the end of 2023, and we project inflation could hover around 7% to 6.5% by mid-2024, which is encouraging but still points to a significant deviation from BanRep’s inflation target range defined between 2% and 4%, and an expectation that the achievement of the inflation target won’t take place before mid-2025. Either way, we expect inflation to continue making progress to close the year around 5%, which will continue encouraging the discussion for rate cuts.

In the previous context, the favourite word for BanRep is ‘caution’. Inflation is still well above the target while the economic activity reflects in part a desired deceleration but also a concern about investments. A couple of BanRep’s board members said they are considering accelerating the easing cycle, while Governor Villar continues to lean to the conservative side. The Finance Minister has mentioned that he will vote for a 100bps rate cut to avoid a significant spike in the real rate. At Scotiabank Colpatria, we project a 75bps rate cut, which will maintain the monetary policy rate at a restrictive territory but avoid putting more pressure on the economy than necessary. If our scenario materializes, the rate-cutting cycle will stimulate a gradual economic recovery during H2-2024 (chart 4).

Last but not least, the legislative period in Congress started in mid-February. However, discussions of social reforms are facing significant challenges. The government has struggled to find enough quorum for the Pension Reform discussion and is running out of time before the bill is archived (the deadline to continue the debate is June 20th), while in the case of Health Reform, uncertainty about the fiscal cost is delaying the discussion. At Scotiabank Colpatria we think the challenging environment for reforms will continue. However, inaction from the policy makers is also a concern. We don’t expect domestic assets to build risk premiums around political uncertainty. Having said that, the issue around public sector inaction could derive in a challenging context in the medium term for economic growth, which could continue preventing Colombia from going back to the investment grade privilege sometime soon.

All in all, Colombia’s macro is not simple. However, macroeconomic fundamentals are evolving gradually to a condition that could allow the central bank to continue taking lower interest rates. If that happens, we expect economic growth to start to recover. However, the headwind will continue on the public sector’s side. Market volatility is diminishing on the FX side, however, we think markets are waiting for more signals from monetary policy to act and decide on a direction, while on the fixed income side, volatility is driven by the Federal Reserve but mostly waiting for the moment to materialize the total return behind the easing cycle.

Peru—The Government Needs Growth

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The Dina Boluarte regime is facing numerous political fronts and opponents, and high inflation and negative growth throughout much of 2023 did not help. Inflation has now come down. What the government needs now is to show growth, and January GDP, to be released on March 15th, may well comply. Finally!

The preliminary growth figures for January that have been released so far are encouraging: cement sales +9% y/y; electricity +4%; mining +4%. This adds to a sharp increase, reportedly of 137% y/y, in public spending. This latter figure mostly translates to higher construction GDP, but not in this magnitude. On the downside, agriculture declined 2.8%, due to the lagging effect from 2023 productivity lapses, and fishing fell 27%, as the recent government-mandated fishing season started early (fishing GDP was +52% in October and +61% in November, but ended in December, whereas the previous year the season had run from November to January). These numbers overall suggest GDP growth mildly below our initial 1.8% y/y growth estimate for January, mainly because mining growth came in lower, possibly because of the impact of seasonal rains.

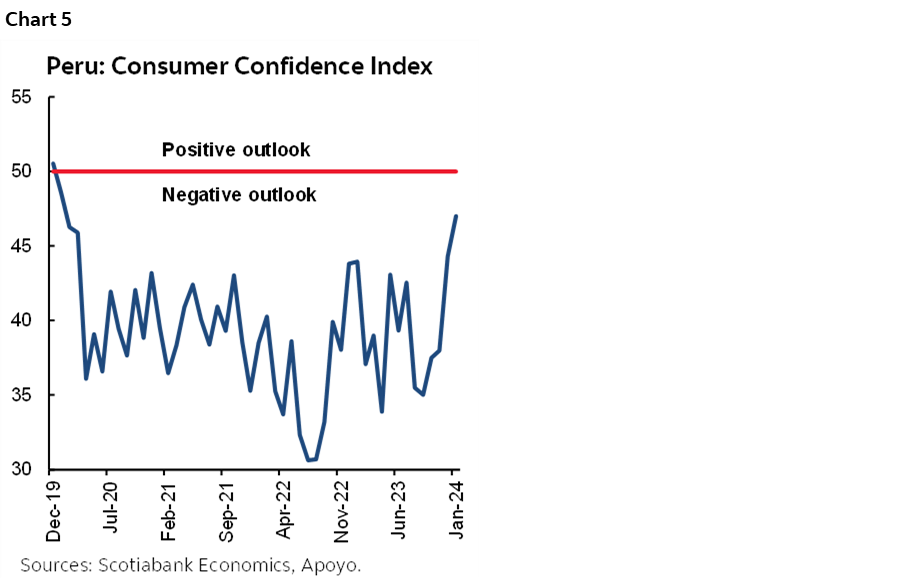

Where there may be some upside to our GDP growth estimate is if the impact of public investment on construction is greater than we are expecting, or if the celerity of the rebound in domestic demand occurs faster. On this score, it’s interesting to note that the consumer confidence index improved to a four-year high in January–February. It’s still negative, but it’s the least negative it has ever been since the Covid pandemic started. You can probably thank low inflation for that (chart 5).

Talking about inflation, we do expect it to finally pierce the 3% ceiling to enter the target range in March. Monthly inflation in March 2023 was 1.29%, much higher than the historical average of 0.75%. Although it’s early in the game, as long as monthly inflation this year is closer to the historic trend than it is to last year’s figure, yearly inflation should decline from the 3.3% figure registered in February, to comfortably under 3.0%, say around 2.8%. This would be on-trend for our 2.4% by year-end and gives the BCRP all the room in the world to continue lowering its reference rate by 25bps per month, until it reaches our year-end target of 4.25%.

The government has a new head of cabinet as of yesterday, and a new finance minister since early January. Having these key new members of the cabinet begin their terms with positive growth and inflation under control may hopefully bolster political stability. The sideshow of purported sex scandals and conspiracies has lost expediency with the change in the head of the cabinet but has left wreckage in its wake which can continue to cause instability. Meanwhile, the 2026 elections are looming closer, and Congress is moving faster to implement change. On March 6th Congress approved, with a 91 to 31 vote, a change in the Constitution to institute a two-Chamber Congress. There will now be a 60-member Senate to accompany the 130-member House. This will not necessarily resolve Peru’s problem with the quality of congressional representation, as the additional chamber does nothing to alter the country’s dysfunctional political party system, but it will hopefully help prevent measures emerging from Congress that are questionable or that affect the country’s institutionality.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.