ECONOMIC OVERVIEW

- September CPI releases from Chile, Colombia, Mexico, and Brazil, and Peru’s central bank decision are next week’s headline acts in Latam, joined by Banxico meeting minutes, against a relatively quiet global backdrop where U.S. government shutdown developments are the main item to watch.

- In today’s report, the team in Chile go over their estimates for a pick-up in inflation in September, with the BCCh seen holding at its October decision a few weeks before general elections.

- Our economists in Mexico discuss the results of the latest BIS FX and OTC survey that reaffirm the importance of the MXN in international financial markets.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile and Mexico.

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period October 4–17 across the Pacific Alliance countries and Brazil.

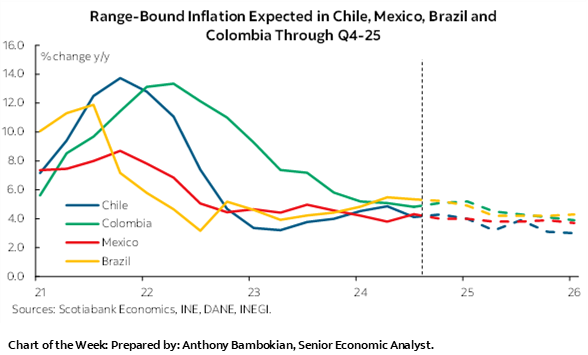

Chart of the Week

ECONOMIC OVERVIEW: CPI WEEK, BCRP HOLD

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- September CPI releases from Chile, Colombia, Mexico, and Brazil, and Peru’s central bank decision are next week’s headline acts in Latam, joined by Banxico meeting minutes, against a relatively quiet global backdrop where U.S. government shutdown developments are the main item to watch.

- In today’s report, the team in Chile go over their estimates for a pick-up in inflation in September, with the BCCh seen holding at its October decision a few weeks before general elections.

- Our economists in Mexico discuss the results of the latest BIS FX and OTC survey that reaffirm the importance of the MXN in international financial markets.

September CPI releases from Chile, Colombia, Mexico, and Brazil, and Peru’s central bank decision are next week’s headline acts in Latam, joined by Banxico meeting minutes, against a relatively quiet global backdrop where U.S. government shutdown developments and the aftermath of the weekend’s OPEC+ decision and Japan’s LDP (and thus PM) vote are the main things to watch. Were the U.S. government to resume operations, we could also finally get September payroll figures that were scheduled for release this morning.

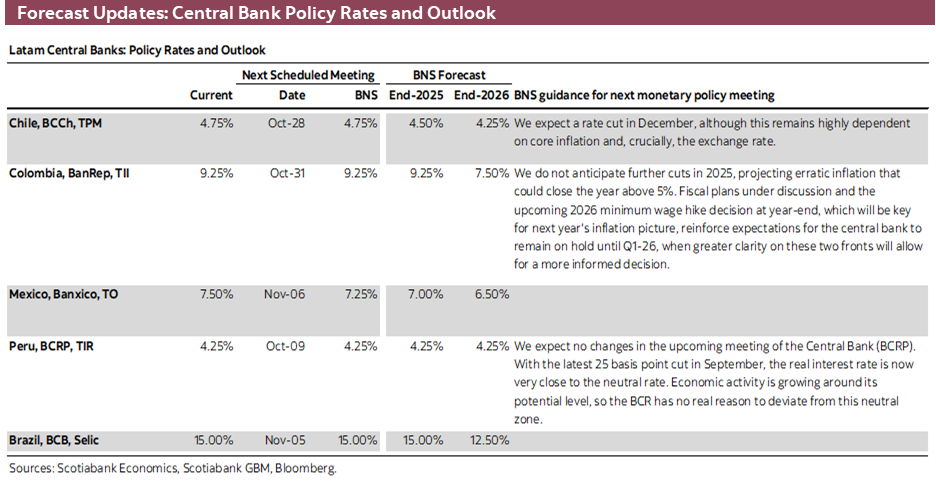

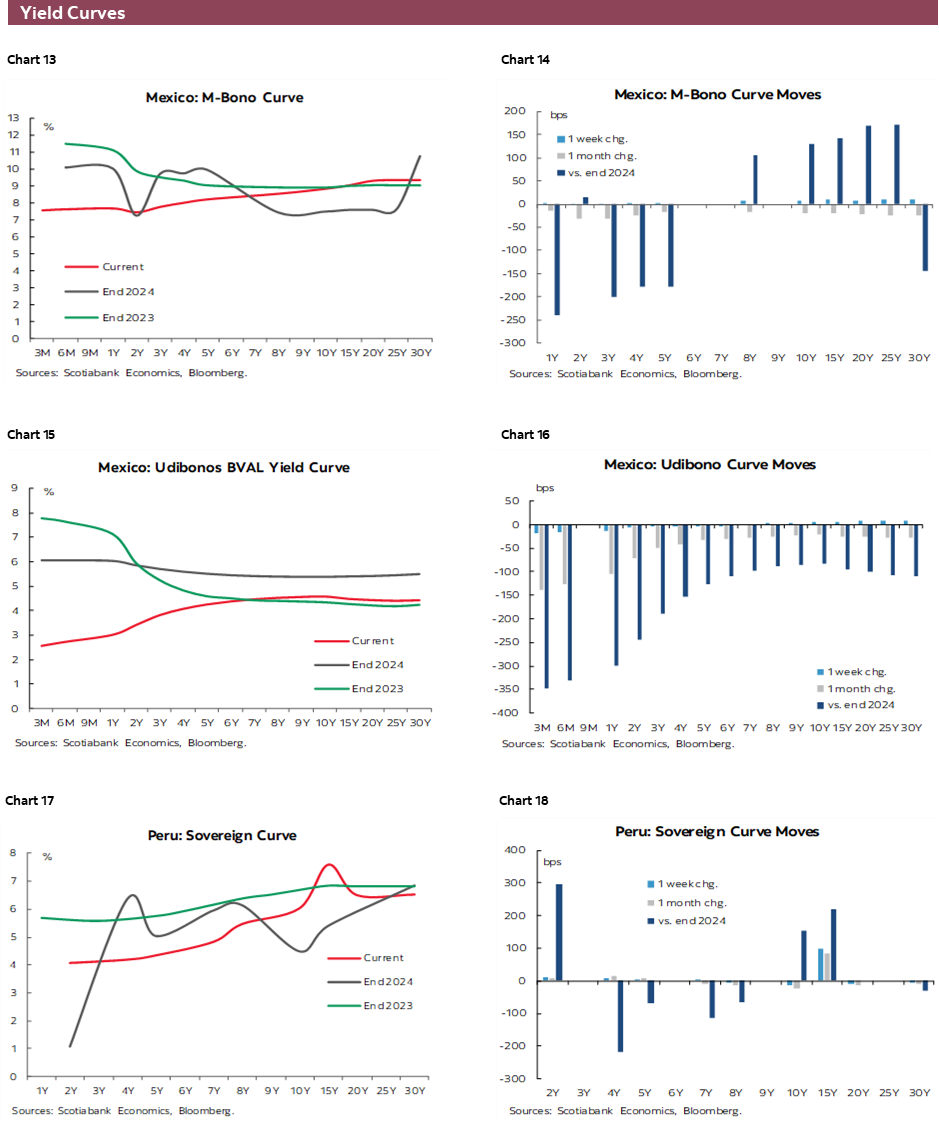

Earlier this week, Peru released September CPI data that showed an as-expected acceleration in inflation to 1.4% from 1.1% y/y thanks to a low base of comparison. We expect that this accelerating trend will continue over the balance of the year towards our end-2025 forecast of 1.9%, thus eyeing the mid-point of the BCRP’s 2–4% target band. This week’s inflation rise, while unsurprising, narrows the odds that the central bank considers another reference rate cut soon, as accelerating inflation could put an end to declining inflation expectations. In January, the median economist polled by the BCRP expected inflation to end 2026 at 2.50%, falling to 2.25% as of the September survey.

Given healthy GDP growth and the BCRP’s closeness to the neutral rate, we think the bank will hold next week and for the foreseeable future. The possible inflationary impact of the latest approval of pension withdrawals may also warrant some caution among policy makers. Note that Peruvian markets are closed on Wednesday for holidays.

Colombia kicks off the CPI week on Tuesday, with headline inflation seen holding around 5.1% y/y and likewise for core inflation remaining in the 4.8–4.9% zone. Our team anticipates moderate contributions from food price increases as well as a rebound in regulated prices. The latter have fallen month-on-month (MoM) for three consecutive months, their longest losing streak since 2020. The 0.3% MoM rise that our team (and the median) expects in next week’s release will also owe to the seasonal rise in education inflation.

Regardless of next week’s CPI reading, even if it were to miss, the bar for BanRep rate cuts in 2025 remains high due to inflationary risks coming from next year’s minimum wage hike and ongoing stickiness from indexation practices. At its Tuesday decision, BanRep continued to point to rising inflation expectations, firm economic conditions, and ongoing global uncertainty, with four members sticking to rates caution and unlikely to vote for cuts until 1Q26—in contrast to the three doves that voted for easing this week (see our team’s recap here).

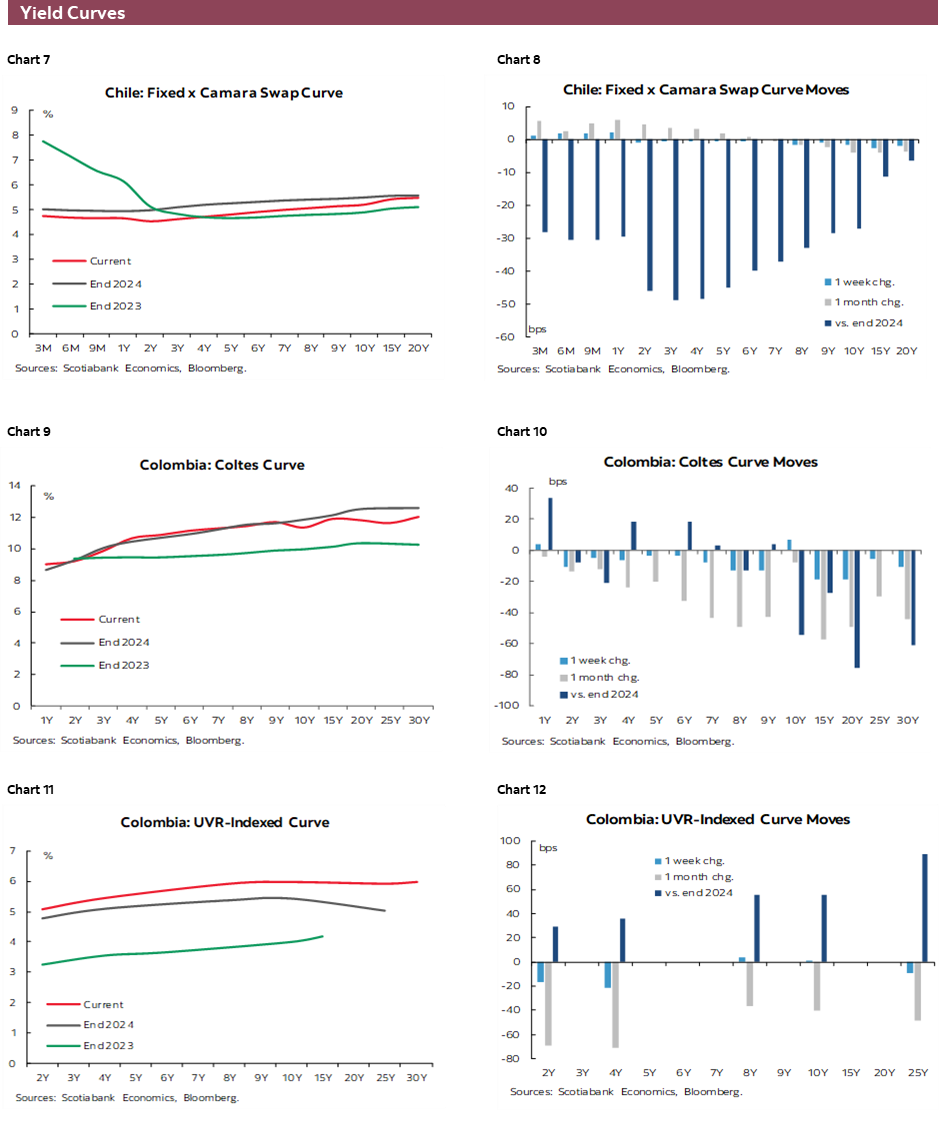

Wednesday brings Chilean prices figures that our economists estimate will show a 0.4% MoM rise that translates into a 4.3% year-over-year (YoY) gain, compared to no MoM change and a 4.0% YoY reading in August. In today’s weekly, the team goes over their estimates, with inflation excluding volatile items seen at 0.3% MoM and 3.9% YoY—unchanged from August’s gain—with upside price pressures emanating from utility bill and minimum wage hikes. Chile also releases September international trade data on Tuesday that should show a decline due to suspended copper production at the El Teniente mine in August (spilling over into September export figures due to lags).

We think the BCCh will choose to sit out at its October 28th meeting, keeping its overnight rate unchanged at 4.75% with general elections about three weeks later, on November 16th when Chileans will vote on a new Congress as well as the presidential candidates that will go on to a likely second round vote on December 14th. The market reaction to the result of the November and December elections may play into the BCCh’s thinking ahead of their December 16th decision, when we expect them to announce a rate cut to 4.25%, as they also look ahead to an expected deceleration in inflation to 4.0% by year-end and 3.0% at end-2026 according to our economists’ forecasts.

On Friday, the BCCh publishes the results to its survey of economists, where the median expected the bank to hold at 4.50% until year-end. Meanwhile, markets are currently assigning about toss-up odds of a 25bps cut at the final meeting of the year, with a cut fully priced in for one of the January or March meetings. The timing of the BCCh’s next cut is a tricky one to call, but it should ultimately be one more 25bps reduction at some point between December and March that, broadly speaking, should not have a massive impact on the country’s economic outlook—that should be more sensitive to the November/December election results.

Mexico is out with inflation data on Thursday, followed by Banxico’s meeting minutes later that day. We project that full-month inflation will roughly align with H1-Sep figures to show 3.8% and 4.3% YoY headline and core readings, respectively, up from 3.6% and 4.2% in August. With that, headline and core inflation would average 3.6% and 4.2% in the third quarter, matching Banxico’s estimates at the time of their September 25th rate cut decision.

Banxico expects that headline inflation will average the same 3.6% rate in 4Q25, but expects that core inflation will cool to 4.0%. These estimates may not be farfetched, but we are skeptical of Banxico’s call for headline and core inflation to decelerate to the low 3s, and thus virtually on target, as of the second quarter of next year. We project that headline inflation will sit around 3.7–3.9% through 2026, a view that is shared by most economists and should be confirmed by next week’s Citi Survey results due on Tuesday.

Thursday’s Banxico meeting minutes may provide some colour on how board members perceive the upside risks to these forecasts, but so far only Dep Gov Heath remains the only policymaker concerned enough to vote for a rate hold. This will likely be the case for the bank’s two remaining meetings this year, when we expect 25bps cuts at each, with another two in 1Q and then rate stability at 6.50%. Fed decisions may play a key role in the path for Banxico’s policy over the next few months, so next week’s Fed meeting minutes out on Wednesday may also have important implications for Banxico expectations.

In today’s report, our economists in Mexico highlight the results of the latest central bank survey of FX and OTC derivates markets, carried out by the BIS and published by Banxico earlier this week. MXN trading rose two spots to 14th as the most traded currency globally, with 86% of peso transactions occurring outside of Mexico, pointing to the MXN’s high liquidity and its 24hr trading window. Overall, the MXN sits as a key currency in international financial markets as a key instrument for investment, hedging, and speculation.

Finally, Brazilian inflation is seen ticking slightly higher, to 5.2% from 5.1% YoY, on the back of a 0.5% MoM rise in prices to follow a 0.1% decline in August due to one-time power bill credits. There should be limited change in market and economist expectations for BCB policy, with inflation well above the bank’s 1.5–4.5% (3% +/-1.5ppts) target band keeping policymakers on hold for the time being.

Headline inflation is nevertheless expected to fall into the low-4s in early-2026 and throughout the year. This should allow the BCB to ease its degree of high policy restrictiveness over the course of the year but the 250bps expected in rate cuts by end-2026 would still leave the Selic rate at 12.50%, a full two percentage points above the mid-2024 low of 10.50% and almost double the pre-pandemic level of 6.50%.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—We Project CPI for September at 0.4% m/m (4.3% y/y)

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

- Main upward contributions expected from clothing and food

We project CPI for September at 0.4% m/m (4.3% y/y), in line with market surveys and inflation forwards, but below the central bank’s forecast in the September IPoM (0.55%). Our estimate includes a core CPI (ex-volatile items) of 0.3% m/m (3.9% y/y) and volatile inflation of 0.5% m/m (5.1% y/y). Within the core CPI, we expect goods inflation of 0.5% m/m and services inflation of 0.2% m/m, reflecting persistent cost shocks (electricity tariffs, minimum wage adjustments, among others).

The main positive contributions would come from clothing and footwear (+0.11 ppts) and food and non-alcoholic beverages (+0.09 ppts) (table 1). In the former, we anticipate price increases above seasonal patterns for men’s clothing and footwear, following unusually muted (or even negative) price changes in August. Similarly, the monthly contribution from the food division would be mainly driven by higher prices in meat and vegetable products. The transport division is also expected to contribute positively (+0.05 ppts), mainly due to increases in gasoline prices, interurban transport fares, and new car prices.

Inflation diffusion for the overall CPI would remain slightly above historical averages. Although recent diffusion has shown volatility, we assume a higher level of core diffusion than in August, mainly explained by the services component. For volatile items, we assume a similar diffusion level to the previous month, broadly in line with historical averages.

Mexico—Banxico Reports Increased Peso Trading Volumes in BIS Global Survey

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Earlier this week, Banco de México released the results of the Triennial Central Bank Survey on Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets, conducted in April 2025 by the Bank for International Settlements (BIS). This survey, the most comprehensive source of information on global FX and derivatives market activity, provides a detailed overview of recent trends, structural changes, and the evolving participation of various currencies, including the Mexican peso. The findings of this edition reflect a context of heightened volatility and reconfiguration of international financial flows, driven by significant trade policy announcements and geopolitical tensions.

Among the most notable findings, global FX trading volumes increased by 28% compared to the 2022 survey, reaching a daily average of USD 9.6 trillion. This surge occurred in an environment of elevated exchange rate volatility, spurred by trade policy announcements made by the United States in early April 2025. It is worth noting that the 2022 survey also coincided with a period of high uncertainty following the onset of the Russia-Ukraine conflict.

Regarding the Mexican peso, it ranked as the 14th most traded currency globally, improving two positions from its 2022 ranking. It also became the third most traded currency among emerging market economies, behind only the Chinese renminbi and the Indian rupee. The global trading volume of the peso rose by 35% compared to the previous survey, increasing from USD 114 billion per day in 2022 to USD 153 billion in 2025, representing 1.6% of global FX turnover. Notably, 82% of peso transactions occurred outside of Mexico, reflecting the currency’s high liquidity and operability in international markets, where it trades 24 hours a day.

Domestically, the average daily trading volume of the peso reached approximately USD 28 billion, marking a 34% increase compared to 2022. This growth was observed across all instruments: spot transactions, forwards, FX swaps, cross-currency interest rate swaps, and options. As in previous surveys, 98% of trades were conducted against the U.S. dollar. Additionally, electronic trading platforms continued to gain prominence, accounting for 89% of transactions—nearly 8 percentage points higher than in 2022. Meanwhile, the daily volume of other currencies traded against the dollar in the local market amounted to USD 2.1 billion.

In terms of locally traded interest rate derivatives, the daily volume declined by 41% compared to 2022, totaling USD 3.9 billion. Despite this decrease, interest rate swaps remained the dominant instrument, representing 97% of the total volume, slightly below the 99% reported in the previous survey. Globally, interest rate derivatives trading volumes rose significantly, from USD 5.0 trillion to USD 7.9 trillion per day. In this context, the volume of instruments denominated in Mexican pesos also increased, from USD 22.5 billion to USD 29.1 billion.

The results of the BIS 2025 Triennial Survey reaffirm the growing importance of the Mexican peso in international financial markets. Its rise in the global ranking and its consolidation as one of the leading emerging market currencies reflect market participants’ confidence in its liquidity, depth, and continuous tradability. Despite the decline in local interest rate derivatives trading, the strong performance of FX markets—both globally and domestically—underscores the peso’s role as a key instrument for investment, hedging, and speculation. These findings also highlight the need to continue strengthening the domestic financial market infrastructure to maintain competitiveness and adaptability in an increasingly complex and volatile global environment.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.