ECONOMIC OVERVIEW

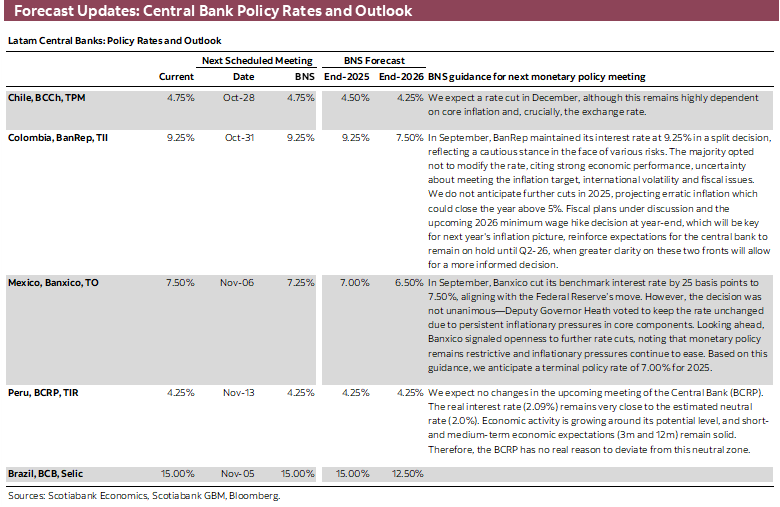

- There should be no surprises from all key Latam and G10 central bank decisions next week, with rate cuts from the Fed and BoC and rate holds from the BCCh, BanRep, ECB, and BoJ widely expected. The focus will be on forward guidance, which may be limited in Chile ahead of elections while Colombian officials may express worries about next year’s minimum wage hike.

- Mexican 3Q GDP is next week’s Latam data highlight, with the data expected to show a contraction in economic activity from year-ago and quarter-ago levels, reflecting weak domestic demand conditions and external challenges. In today’s report, the team goes over the recently approved tax increases for 2026 which may only act as a small support for public finances.

- A possible meeting between Trump and Xi in Asia will be in focus for markets, with the trading mood also driven by earnings releases by U.S. tech giants.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight Mexico.

MARKET EVENTS & INDICATORS

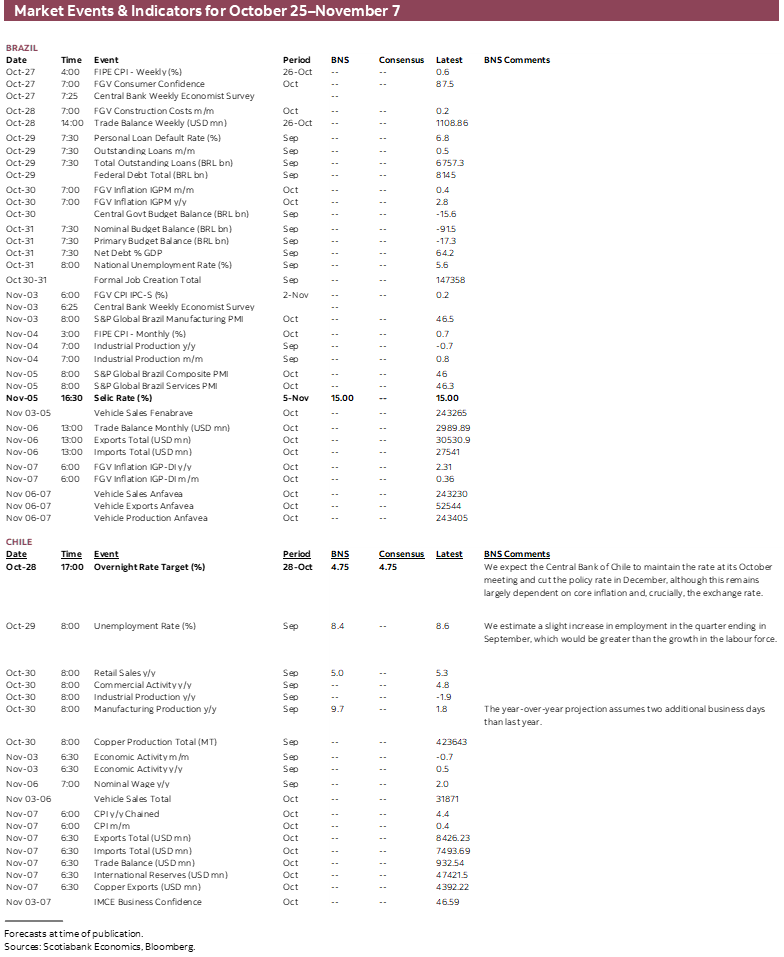

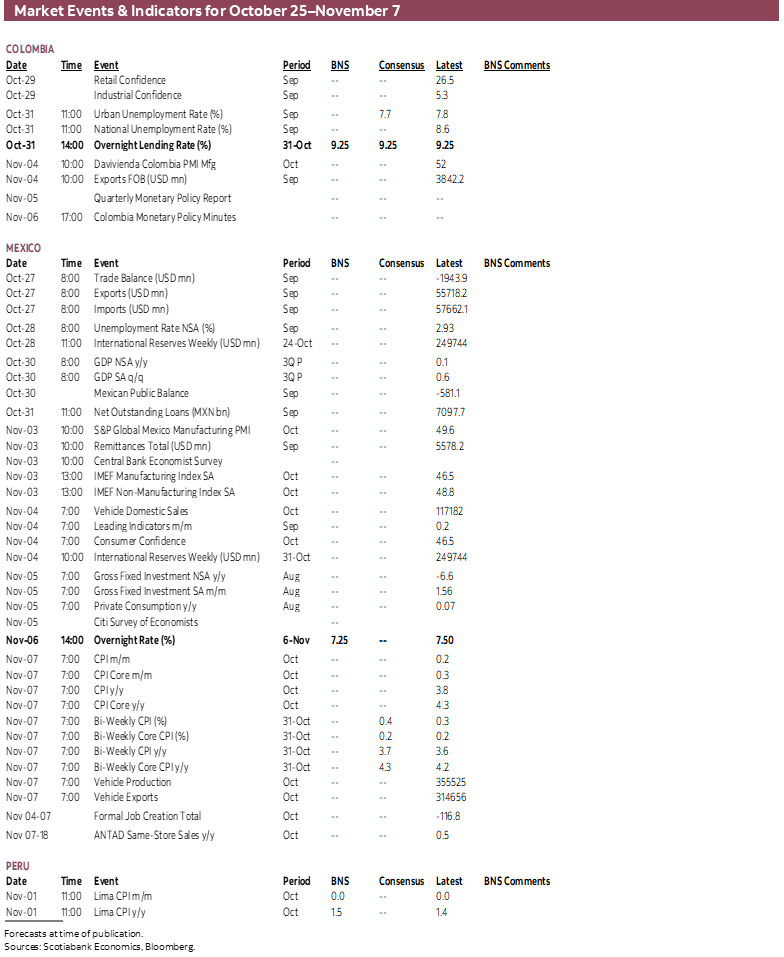

- A comprehensive risk calendar with selected highlights for the period October 25–November 7 across the Pacific Alliance countries and Brazil.

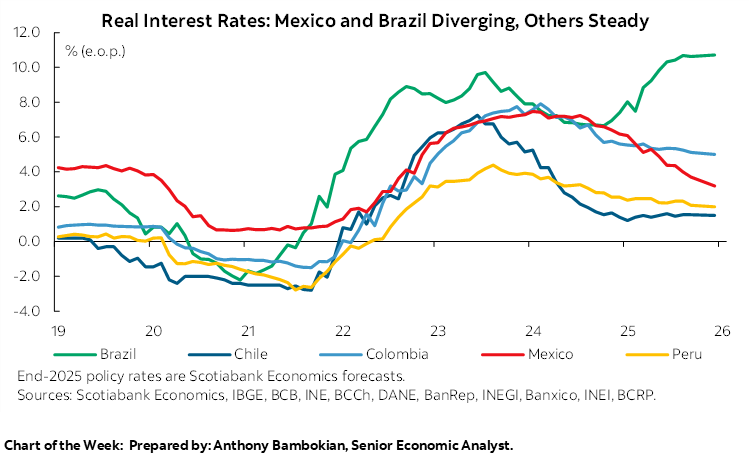

Chart of the Week

ECONOMIC OVERVIEW: DECIDED DECISIONS, MACRO UPDATES, AND TRADE NEGOTIATIONS

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- There should be no surprises from all key Latam and G10 central bank decisions next week, with rate cuts from the Fed and BoC and rate holds from the BCCh, BanRep, ECB, and BoJ widely expected. The focus will be on forward guidance, which may be limited in Chile ahead of elections while Colombian officials may express worries about next year’s minimum wage hike.

- Mexican 3Q GDP is next week’s Latam data highlight, with the data expected to show a contraction in economic activity from year-ago and quarter-ago levels, reflecting weak domestic demand conditions and external challenges. In today’s report, the team goes over the recently approved tax increases for 2026 which may only act as a small support for public finances.

- A possible meeting between Trump and Xi in Asia will be in focus for markets, with the trading mood also driven by earnings releases by U.S. tech giants.

The final week of the month will bring something for everyone, with Latam and G10 central bank policy announcements and GDP releases, unemployment data in the Pacific Alliance, and a highly awaited possible meeting between Presidents Trump and Xi following weeks of building U.S.-China trade tensions. Peru and Brazil are the exceptions, with relatively quiet calendars. On top of economic and political developments, global markets will move to the beat of earnings releases by Apple, Meta, Amazon, and Alphabet among other major names.

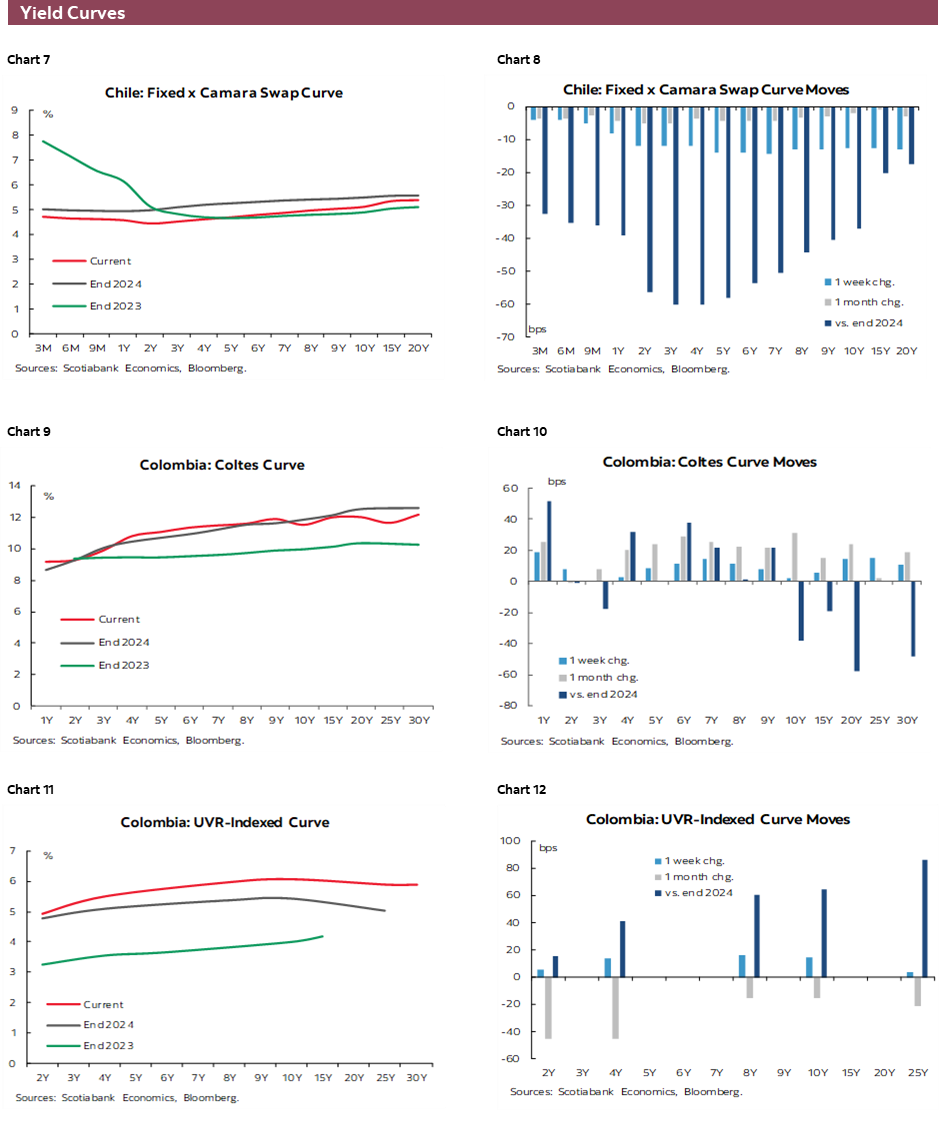

Chile’s central bank is first up, with a monetary policy announcement on Tuesday that is universally expected to leave the benchmark rate unchanged at 4.75%. With elections around the corner (November 16th), robust economic activity, and some recent heat in inflation prints, there’s no real reason for the BCCh to loosen policy further next week. Unemployment rate data due on Wednesday, followed by retail sales and industrial/manufacturing/copper production figures out on Thursday may help us refine expectations for the December meeting.

However, markets are relatively unconvinced that we will see rate cuts again this year, with less than 10bps priced in by year-end. On the flip side, results to the BCCh’s economists survey published earlier this week showed respondents are still very much biased in favour of a cut, with about 75% of them forecasting a 4.50% rate at year-end—with this share even increasing from 65% at the September survey. Speaking of surveys, CADEM presidential poll results published last Sunday show the left’s Jara at 29% compared to the right’s Kast at 24% in the first-round vote, but the latter’s would-be second round lead has widened to 49–33 compared to 47–36 a week prior.

At the opposite end, BanRep closes the week with an expected rate hold at 9.25%—which we expect will remain the case until 2Q26. August economic activity data released on Monday was somewhat disappointing, with a slowdown to 2.0% from 4.4% in July falling short of forecasts of around 3%. But, seasonal or base effect factors may have played an outsized role in driving a soft print while the economy is still tracking an expansion of about 2.5% this year on the back of strong household spending (see here); we’ll also see what Friday unemployment figures have to say. The bank’s guidance will be the main thing to watch next week, with a focus on their views regarding the government’s possible double-digit minimum wage increase for 2026 and the upside inflation risks it would generate.

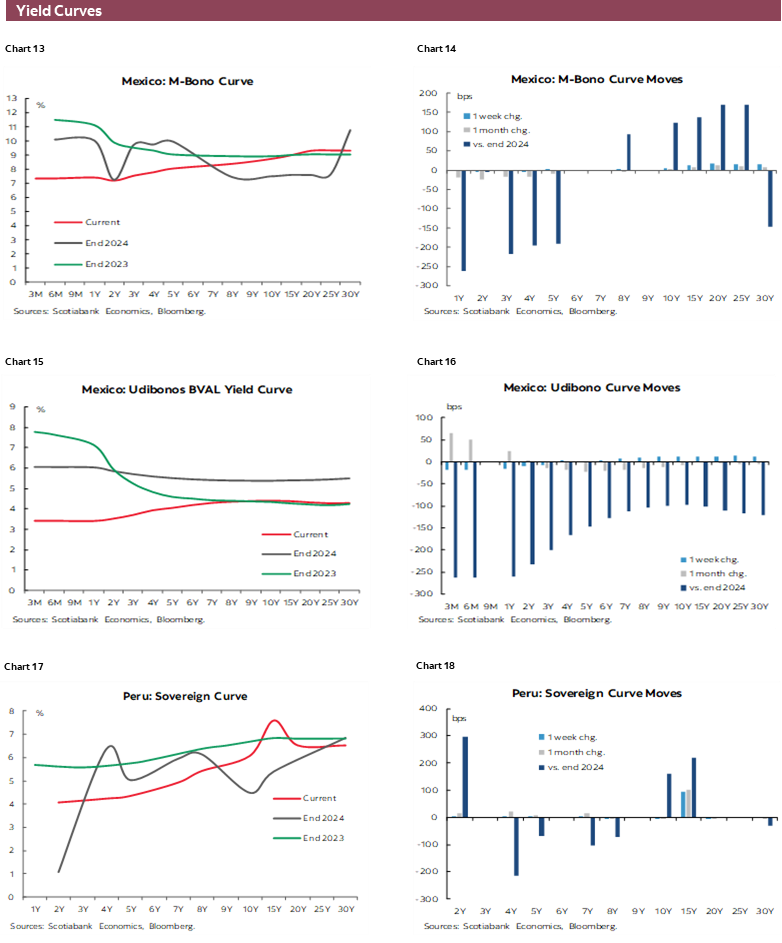

Mexican 3Q GDP data on Thursday is the region’s main economic release next week, and it’s not expected to be a good one. After registering no year-on-year growth in 2Q, following a 0.9% expansion in 1Q, Mexico’s economy is seen contracting by around 0.5% y/y in the third quarter. Monthly economic activity data showed that GDP fell by 1.1% and 0.9% y/y in July and August, respectively, due to a pronounced contraction in manufacturing (-1.9% and -3.1%) joining ongoing construction weakness, but also a weak showing for the services sector.

On 3m/3m basis with seasonally-adjusted data, Mexico’s economy contracted by 0.2% in the quarter to August, compared to the 0.6% expansion it tracked in the quarter to May or 0.5% to June, which lined up with the 3Q reading of 0.6% q/q. Put another way, Mexico’s economy likely contracted in y/y and q/q terms during the third quarter, reflecting a challenging domestic backdrop of weak hiring, weak investment, and soft confidence compounded by external risks in U.S. trade policy.

On the political front, our team in Mexico discusses in today’s report the recent approval of special taxes for the 2026 fiscal year. The law has established a huge 87% tax hike on sugary drinks, with a 100% levy on tobacco products like vapes and pouches, as well as a 50% tax hike on online gambling, and 8% on violent video games, among others. The tax law is expected to lift public revenues by around MXN 75bn in 2026 but not materially alter the worrying path of Mexican government finances.

Outside of the region, the Fed and the BoC are widely expected to announce 25bps cuts on Wednesday, while the ECB and BoJ are seen keeping policy rates steady on Thursday with the latter perhaps offering more exciting forward guidance colour. U.S. GDP scheduled for Thursday is unlikely to arrive due to the now second-longest U.S. government shutdown, but we will get 3Q GDP data from a handful of Eurozone countries, and the bloc as whole, over Thursday and Friday, alongside inflation readings from the region. Canada also releases monthly GDP data to end the week.

PACIFIC ALLIANCE COUNTRY UPDATES

Mexico—2026 Tax Hikes Approved

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

Martha Cordova, Economic Research Specialist

+52.55.5435.4824 (Mexico)

martha.cordovamendez@scotiabank.com.mx

Last week, Mexico’s House of Representatives approved the Special Tax on Production and Services (IEPS) Law for the 2026 fiscal year. One of the most significant changes is the increase in the tax on sugary drinks, which will rise from $1.64 to $3.08 per litre—an 87% hike. Héctor Saúl Téllez, Deputy Coordinator for Economic Affairs of the PAN party, estimates that this adjustment will generate revenues of $75.29 billion pesos in 2026, a 73.8% increase compared to the current year.

Additionally, for the first time, a tax of $1.50 per litre will be applied to beverages sweetened with non-caloric sweeteners, which were previously not included in this legislation.

Regarding nicotine and tobacco products, a 100% tax will be imposed on all items containing nicotine, such as pouches and vapes, along with a 200% ad valorem tax on cigars. Moreover, the specific tax per cigarette will increase from $0.64 to $0.85 in 2026, leading to a 32.8% rise in cigarette prices, with further gradual increases expected through 2030.

Other consumer products affected by this reform include violent video games: 8% increase, online betting platforms: 50% increase, games of chance and lotteries: tax rate will rise from 30% to 50%, among others.

The most immediate adverse effect of this reform will be its impact on consumer prices. It is estimated that the tax increase on soft drinks alone could contribute 5 basis points to inflation in 2026.

The central argument behind this reform is the promotion of public health and well-being. This is supported by alarming data: 70% of Mexico’s adult population is overweight or obese, and 90% of type II diabetes cases are directly linked to excess weight. However, for the effects of this fiscal policy to be sustainable and long-lasting, it must be accompanied by concrete actions in the healthcare sector.

Currently, public health spending has decreased by 11%, representing just 2.6% of GDP—well below the minimum recommended by the World Health Organization, which suggests investing at least 6% of GDP.

The IEPS reform for the 2026 fiscal year reflects an effort by the Mexican government to discourage the consumption of harmful products and boost tax revenue. While these adjustments will have short-term inflationary effects, their success will depend on a comprehensive strategy that includes increased investment in the healthcare system. Without a parallel strengthening of public health spending, the expected benefits in terms of social well-being may be limited, turning this reform into a revenue-generating measure rather than an effective public health policy.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.