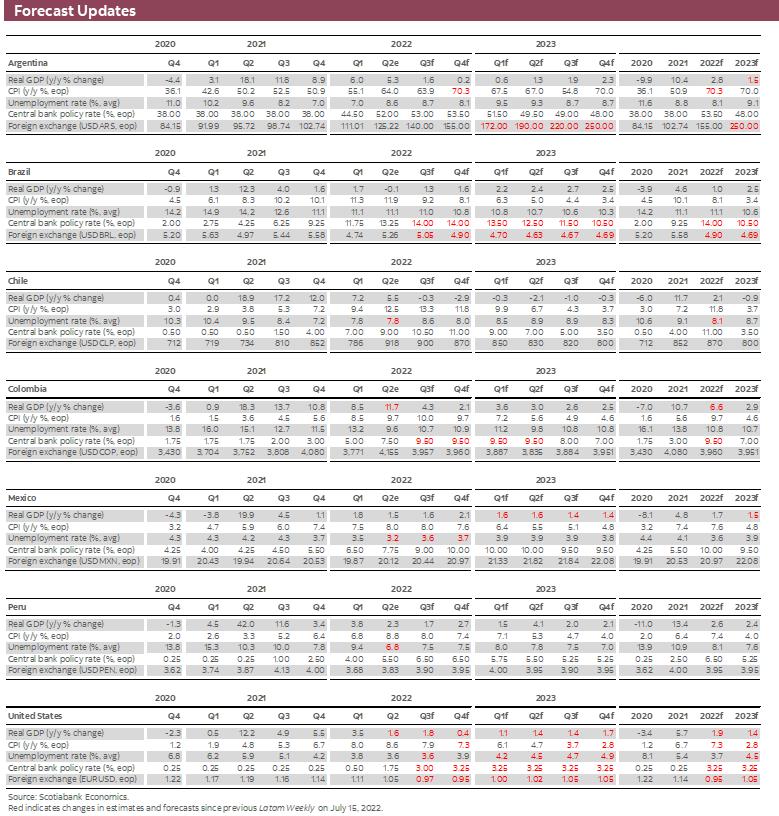

FORECAST UPDATES

- Two quarters of negative growth in the US on top of another 75 bps interest rate hike by the Fed and an earlier rate increase by the ECB represent big changes to external inputs for local forecasts. See the latest revisions that Scotiabank’s teams in the region have made to their projections in the forecast tables below.

ECONOMIC OVERVIEW

- Fears of global recession are on the rise following release of US GDP numbers showing two quarters of negative growth and the second successive 75 bps hike by the Fed.

- There is little indication of recession in the Latam region, however, where, if anything, growth has surprised on the upside. Growth is coming down from post-pandemic rebound highs, but that reflects a transition to more sustainable medium-term rates.

- In contrast, Argentina appears to be in the throes of another bout of severe financial instability. Expected inflation is shooting higher, widening the gap between official and black-market exchange rates.

- Yet, apart from its immediate neighbours, instability in Argentina likely does not pose a serious contagion risk to the rest of the region. This is because sound policy frameworks and strong institutions provide resilience to external shocks.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru.

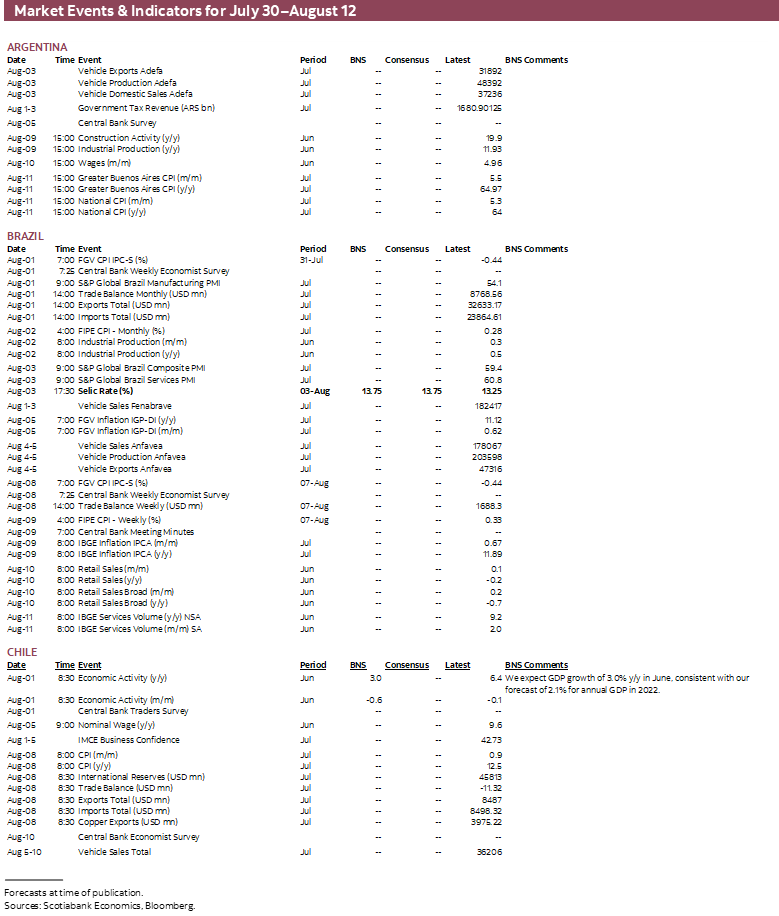

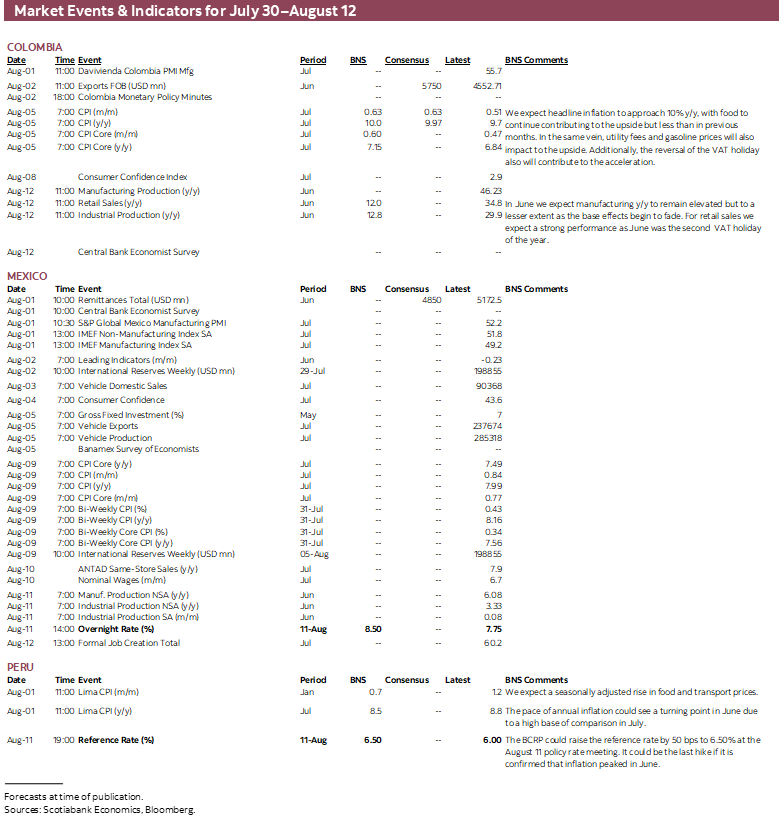

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period July 30–August 12 across the Pacific Alliance countries, plus their regional neighbours Argentina and Brazil.

Economic Overview: Nothing to Fear but Fear Itself

James Haley, Special Advisor

416.607.0058

Scotiabank Economics

jim.haley@scotiabank.com

- Growing fears of financial instability in Argentina, measured by the widening gap between the official and black-market exchange rates, reflect a deterioration in the expected path of key economic fundamentals.

- These fears were stoked by the resignation of the former Economy Minister, Martin Guzman, over policy differences within the government, likely regarding the terms of the government’s program with the IMF. In these circumstances, short-term projections of Argentina’s financial outlook are subject to enormous uncertainty.

- One thing is certain: The loss of the fiscal and financial discipline provided by the IMF program would likely unleash an expectations-led financial crisis as ordinary citizens scramble to preserve the purchasing power of salaries and savings. And while this scenario is not inevitable, the longer that uncertainty remains, the bigger the challenge to financial stability.

- But, in contrast to the past, Latam countries with sound policy frameworks and strong economic and political institutions are unlikely to suffer severe adverse contagion effects. In this respect, they have nothing to fear but fear itself.

Fears of a global recession are on the rise, fueled by Q2 US GDP numbers, released July 28th. With two quarters of negative growth and the Fed aggressively raising interest rates, including another 75 bps hike on July 27th, those fears may be justified. As Scotiabank’s Derek Holt points out, however, financial markets reacted to the Fed’s announcement with considerable aplomb, possibly misconstruing the meaning in the message. That said, while the case remains to be proven, global recession fears could well be realized if central banks inadvertently tighten too much, as each individually puts a bias on restraint in order to get ahead of expectations and preserve credibility, without regard to the collective effect that may have on global financial conditions and thus growth.

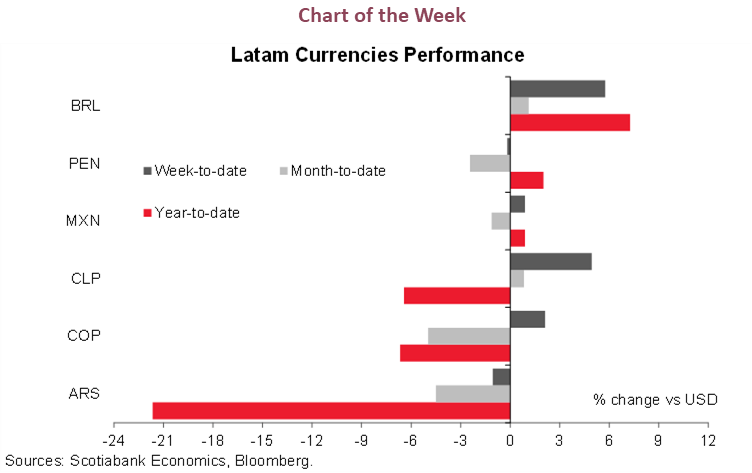

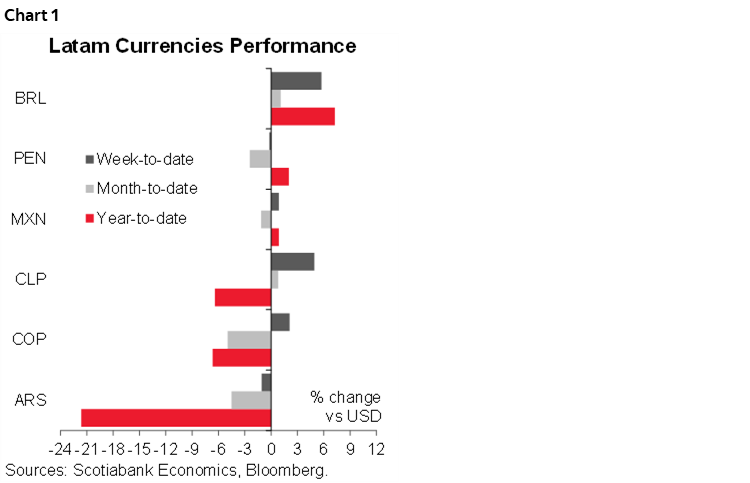

To this point at least, there is no evidence of recession in the Latam region. Growth there is generally holding up—if anything, exceeding expectations, as in the case of Colombia—even as it eases from post-pandemic rebound highs. Financial markets have been buffeted by the surge of the US dollar, which has resulted in increased volatility, as our team in Bogota observes in the Country Notes below, and steep currency depreciations as in the case of the Chilean peso (chart 1). But there is little cause for alarm. That can’t be said with respect to Argentina.

MIND THE GAPS

The Latam Weekly does not typically devote much editorial space to Argentina. In some respects, this inattention is incongruous with the fact that the country is richly endowed with natural resources and has enormous economic potential; Argentina should loom large in terms of economic importance to the region and the global economy writ large. That it does not is largely because of endemic policy missteps that have created a huge gap between this potential and the actual economic outcomes. Those missteps have had the effect of reducing the economic and financial linkages between Argentina and its Pacific Alliance peers, which have generally fallen over time.

From the perspective of its regional neighbours, this disengagement may not be wholly unwelcome. Particularly now. In recent days, the economic outlook in Argentina has darkened. The most telling statistic of this change is another gap—the one between the official exchange rate and the black-market exchange rate. This gap has widened considerably, reflecting a growing fear that the modicum of fiscal and financial discipline prevailing under the auspices of the IMF program may now be at risk. In this event, watch for a sudden deterioration in financial conditions as inflation expectations, which have already spiked higher, become unmoored.

Sadly, Argentines have ample experience with financial crises and IMF programs that are derailed by external shocks or inadequate execution on the part of the government. Holding wealth—even if it is a weekly pay cheque—in a currency whose purchasing power is rapidly being eroded by inflation is not a winning strategy. The sensible thing to do in such circumstances is to convert domestic currency into a more stable store of purchasing power. And for many, this stable store of value is the US dollar. The gap between the official exchange rate and the exchange rate at which ordinary citizens are prepared to exchange currency thus mirrors the rise in inflation expectations and the decline in the credibility of the government’s financial stabilization plan.

Another bout of financial instability is not inevitable, however. While external price shocks propagated by Russia’s invasion of Ukraine have pushed inflation up, as they have around the globe, the First Review of the IMF program, completed in late June, recognized these effects, and adjusted the program’s targets accordingly. Steadfast adherence to the quantitative performance targets—which are intended to provide financial discipline—could yet prevent instability.

But the proximate cause of the latest wave of fear undermines the case for optimism. Expectations of inflation rose sharply in recent weeks following the resignation of the former Economy Minister, Martin Guzman, reportedly over fundamental policy differences within the government on the need to exercise fiscal and financial restraint to meet the conditions of the IMF program. While his latest successor, the second in less than a month, Sergio Massa, may successfully navigate between the domestic shoals of internecine political disputes and the reefs of external price shocks, that felicitous outcome is by no means assured. There is little doubt, however, that he has a difficult challenge ahead.

One thing is certain: the longer that corrective measures are deferred, the bigger the challenge. With inflation expectations already ratcheting up, the risk of extrapolative behaviour becoming entrenched is rising. Workers, observing price increases, extrapolate future price increases upwards. Fearing the erosion of real wages and purchasing power this entails, they demand higher wages based on these future inflation rates. Shopkeepers, likewise, increase prices in anticipation of extrapolated future inflation to preserve the value of working capital. And in the absence of fiscal and financial discipline, there is no nominal anchor to arrest this process.

PROJECTING UNCERTAINTY

In these circumstances, short-term economic projections are fraught with uncertainty and error. The problem is that short-term forecasts of inflation, interest rates and the exchange rate hinge critically on a discrete policy decision—whether to stick with the IMF program, and its orthodoxy of fiscal and financial discipline, or embrace a heterodox policy program of expansion. The former has the overarching advantage that it has proven to work, albeit with the disadvantage that it requires painful adjustments. The latter, with its Panglossian promise of painless expansion, is the triumph of hope over experience; it is little wonder therefore that it is the politically expedient option. Unfortunately, it has rarely, if ever, been proven effective.

Adoption of either of the two policy choices facing the government would have stark implications for short-term projections. This is because analytically consistent forecasts would likely entail big changes from the status quo. Adherence to the government’s IMF program, for example, would require large interest rate hikes to facilitate the positive real interest rates that are a key condition of the program. These higher rates would, however, contain inflation and stabilize the exchange rate, which would otherwise be subject to severe downward pressures. But higher interest rates would also take a toll on short-term growth and employment. In contrast, should the government’s implementation of the IMF program flag or fail, fear of rampant inflation would likely overtake financial markets, resulting in both higher inflation (as any pretence of financial discipline is given up) and a deeply depreciated currency. Moreover, while growth and employment might get a short-term bump from more expansionary policies, any gain would prove ephemeral as the costs of yet another financial crisis mount.

A third “muddling-through” scenario is possible in the near term, one that entails partial observance and serial renegotiation of IMF program targets. Such an outcome would result in inflation that is higher than currently programmed, with commensurate interest rate increases—but which lag inflation—and currency depreciation that reflects higher inflation. But even that unsatisfactory scenario may only be possible with increasingly draconian measures to contain inflationary pressures and exchange rate depreciation, measures that would further reduce Argentina’s economic and financial links to the region and the rest of the world. Nevertheless, with pervasive uncertainty in respect of the government’s intentions, it probably is the scenario that most analysts implicitly assume.

For the purposes of the Latam Weekly forecast tables, we report the market consensus, recognizing that this is likely to yield results that are likely to be off the mark.

THE REWARDS OF VIRTUE

There was a time—not that long ago—when financial instability in Argentina would raise serious concerns of contagion to the rest of the region. No longer. While financial instability in Argentina can be expected to adversely affect its immediate neighbours, with whom it is more-highly connected through trade and financial channels, this is not the case with respect to the Pacific Alliance.

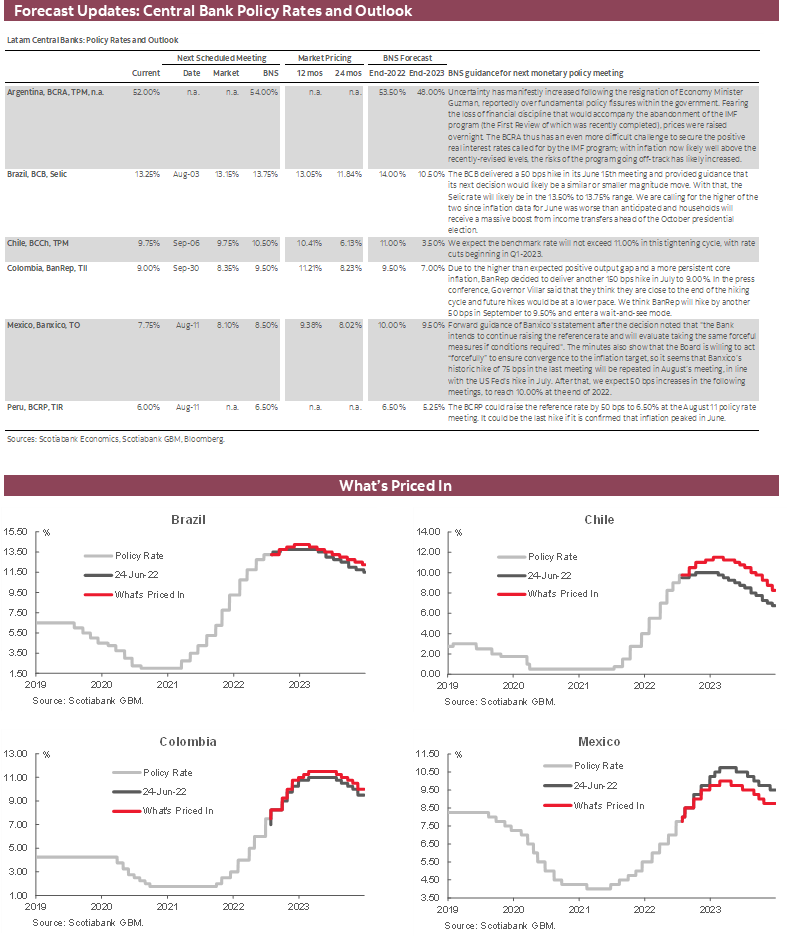

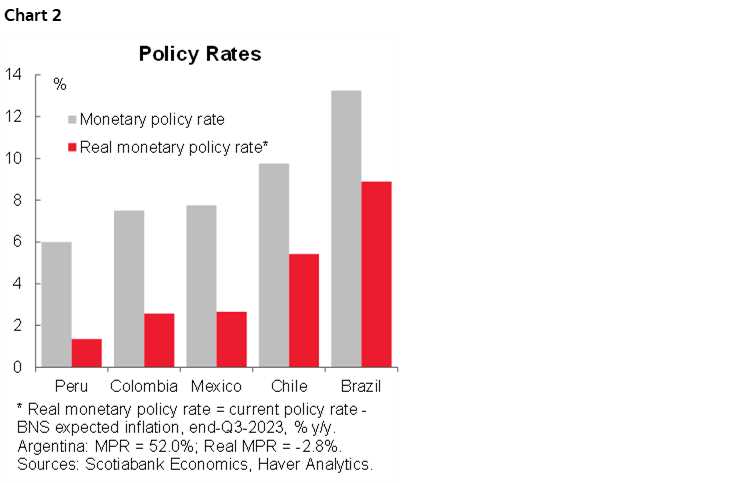

Over the past two decades, Pacific Alliance countries along with others in the region have established sound policy frameworks and strong economic and political institutions. Together, these frameworks and institutions anchor policies and expectations, helping to reduce risk premia and allowing governments in the region to break the curse of pro-cyclical policy responses. And the virtue of the tough choices made in the past to safeguard fiscal frameworks and preserve central bank independence is rewarded with increased resilience to external shocks. In the current conjuncture, those tough choices include raising interest rates above the rate of inflation (chart 2).

But that virtue is not assured; political uncertainty, slippages of fiscal and monetary policy anchors, and the erosion of democratic norms could reduce that resilience. In an environment of “risk-off” such factors could increase the possibility of contagion. Countries in the region must remain vigilant to these threats to long-term prosperity.

NOTHING TO FEAR

In the darkest days of the Great Depression, US President, Franklin D. Roosevelt soothed the nerves of an anxious nation by counselling that “the only thing we have to fear is fear itself”. Roosevelt was warning against a self-fulfilling, expectations-led collapse in activity in which the fear of an economic collapse incites people to defer purchases and businesses to postpone investment, generating the very outcome they fear. For global investors, the fear of a self-fulfilling prophecy is unwarranted in the case of the Pacific Alliance and elsewhere where sound policy frameworks and strong institutions provide resilience to external shocks.

But that can’t be said with respect to Argentina. This is because the deterioration in the short-term outlook there mirrors a corresponding self-inflicted deterioration in the path of expected fundamentals, as fiscal and financial discipline is eroded. Efforts to address the current funk with more spending and looser monetary policies would only create more instability. And while that scenario would entail severe hardships for Argentina’s poor, the effect on most Latam countries would likely be muted.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Current CLP Level Should Ensure External Sustainability

Jorge Selaive, Head Economist, Chile

+56.2.2619.5435 (Chile)

jorge.selaive@scotiabank.cl

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

Waldo Riveras, Senior Economist

+56.2.2619.5465 (Chile)

waldo.riveras@scotiabank.cl

COVID-19 SITUATION IN CHILE

The daily number of confirmed COVID-19 cases has continued to increase in recent days, though the test positivity rate is stable around 15%. For now, however, occupancy rates of ICU beds and COVID-19-related death rates are stable at low levels. Meanwhile, the vaccination campaign has reached 92.9% of the eligible population. The rollout of booster (third) doses continues—reaching 15.4 million people—and the new booster dose (fourth) is in progress—with 10.5 million people covered.

AS ANTICIPATED, THE CENTRAL BANK HAS BEGUN EXCHANGE RATE INTERVENTION

On Thursday, July 14, the central bank (BCCh) announced a USD 25 bn foreign exchange intervention to support the CLP after it plummeted to a record low, reaching CLP 1,049. The program includes spot dollar sales of up to USD 10 bn; foreign exchange hedge sales to the same amount, and a foreign exchange swap program to provide liquidity of up to USD 5 bn. In general, the program is consistent with what we expected. The CLP is currently around 12% below the maximum level reached before the intervention. However, in our view, it remains above the level explained by its fundamentals.

CLP DEPRECIATION SHOULD BE SUFFICIENT TO GUARANTEE EXTERNAL SUSTAINABILITY

Recent assessments of Chile’s current account deficit by international observers suffer from a vision of temporary adjustment. In particular, their focus on the high current account deficit as a percentage of GDP with respect to a broad group of countries does not represent a good basis for the depreciation of the Chilean peso (CLP).

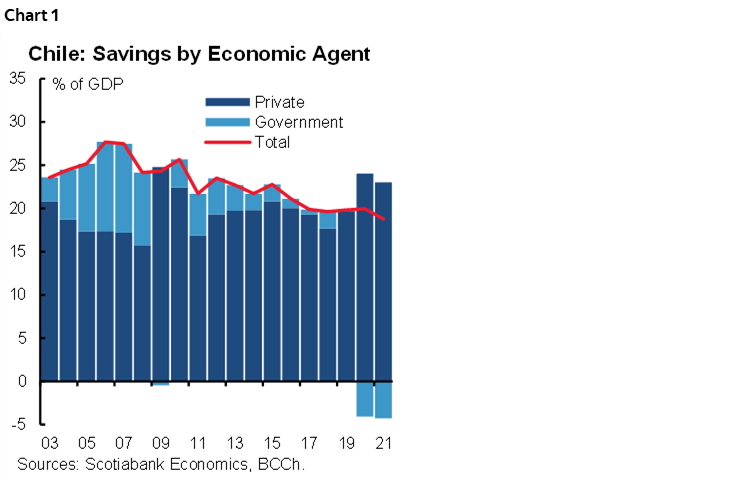

Why do we have such high current account deficit? In our view, the main driver of large current account deficits is the government. Large deficits which prevailed prior to 2019 began to narrow at the start of the pandemic. But deficits quickly started to increase again as a result of a stable private investment and a decline in public savings (chart 1).

Who has financed the current account deficit? Prior to 2019, foreign direct investment (FDI) was the largest source of current account financing (albeit focused on mining and the energy sector). That fact alleviated concerns about financial vulnerability. However, since the beginning of the pandemic Portfolio Investment (PF withdrawals) and, to a lesser extent, the increase in sovereign debt that has financed deficits.

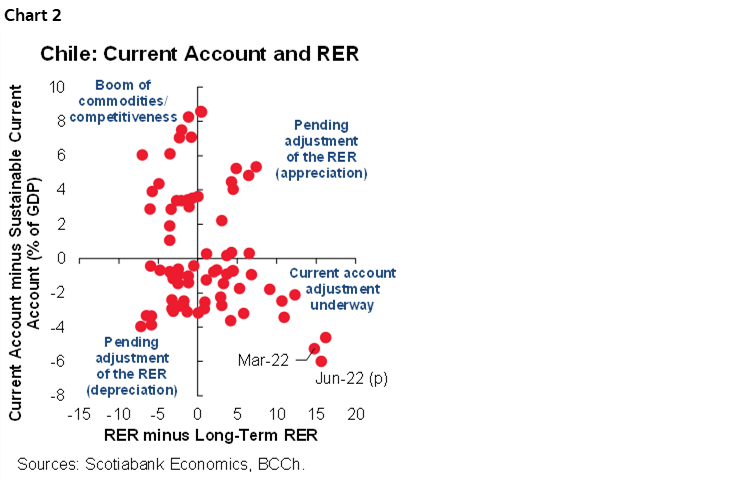

Is the economy making the necessary adjustments? In our view, the answer to this question is in the affirmative; moreover, the adjustment process is already well advanced. As of Q2-2022, a virtuous combination between current account deficits and the real depreciation of the CLP already exists (chart 2). Taking in account the above, our analysis suggests that the adjustment is already underway, assuming no new PF withdrawals, fiscal transfers that jeopardize fiscal convergence and/or levels of public debt higher than the included in the latest Public Finance Report (38.0% of GDP in 2022). We have seen positive signs in these dimensions.

Is further depreciation of the CLP necessary? According to our analysis, we do not expect a further real depreciation of the CLP in our baseline scenario in which the economy expands 2.1% in 2022 and falls into recession with a contraction of 0.9% in 2023. In our view, the current depreciated level of the CLP, if sustained, would be enough to ensure external sustainability.

A LOOK AHEAD

In the next fortnight, the central bank will release the monthly GDP growth for June, on Monday August 1, while the statistical agency (INE) will publish the July’s CPI on Monday, August 8.

Colombia—The Explained and Unexplained Drivers of the Exchange Rate

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

Maria Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

The world is in a unique moment. Markets are unusually volatile owing to the possibility of stagflation for the first time in more than forty years. This risk is making central banks more hawkish than expected, while supply pressures make it more difficult than usual to normalize inflation, forcing monetary policy to become pro-cyclical and stoking recession fears across the world.

In this environment, investors’ preferences are tilted to maintaining a light positioning and seeking refuge in the US dollar, which has strengthened beyond expectations. Given this context, the Colombian peso (COP) has been hit along with other Latam currencies. Having said that, as in the rest of the region, the Colombian economy has its idiosyncrasies that can affect expectations formation.

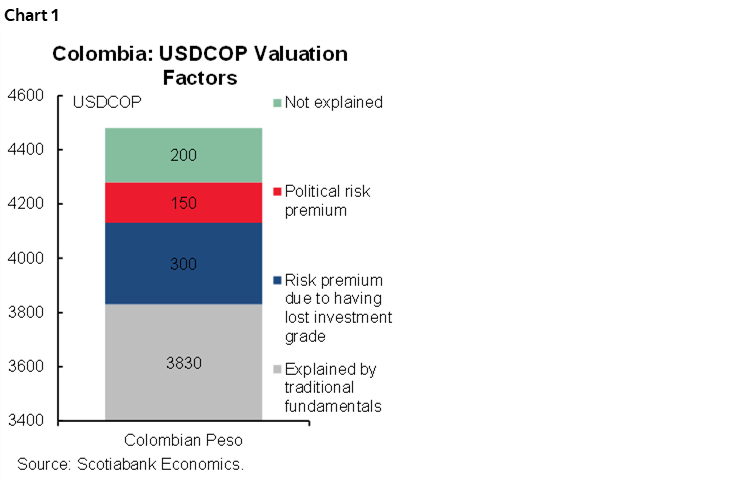

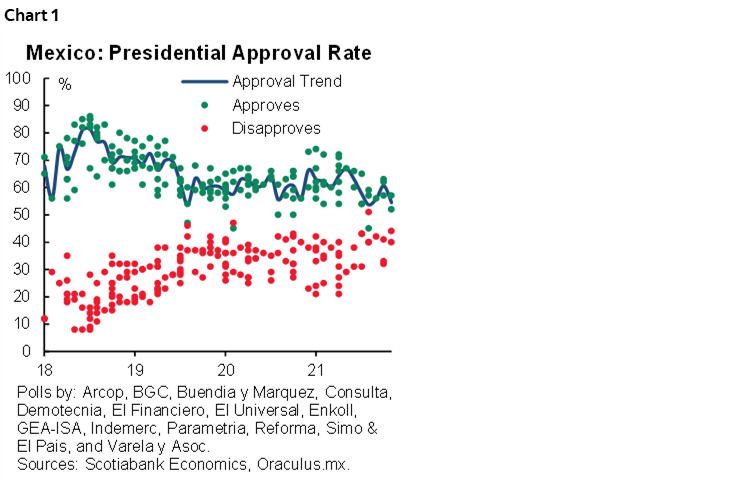

Initially, our FX model showed that the uncertain international situation has increased the USDCOP fit by around 350 pesos (10%), to 3,850 pesos in a long-run perspective (chart 1). As long as volatility continues and markets adjust to lower international liquidity with higher interest rates, we think this effect will continue to exert pressure on the COP.

Starting from its fundamental value, we identify some premiums on the FX. The first is the loss of investment grade status last year, which led the COP to weaken structurally by an additional COP300, as a result of the deterioration in the country’s risk perception. This effect takes the fundamental exchange rate to USDCOP 4,150. Moreover, as we think this represents a structural deterioration for the COP, we expect these +300 pesos premium to remain in the COP over the medium term, since we do not expect Colombia to recover its investment-grade for at least the next two years.

The model also shows that political uncertainty has affected COP dynamics; specifically, a +COP150 penalization attributable to the presidential elections season. The strong movements after the first round of presidential elections (an appreciation of 125 pesos) and the almost exact opposite reaction after the second round confirmed that the COP currently has a roughly COP 150 risk premium priced-in.

Summing up all the effects, our models say that the COP should be hovering around USDCOP 4,300, but with the possibility of high volatility remaining. The recent more centrist tone of President-Elect Petro with respect to making structural reforms under the ruling institutional framework in Colombia and cooperating with Congress and the Courts will, in our opinion, diminish the electoral effect once President-Elect Petro takes office. However, volatility will continue on the back of international uncertainty and Congressional discussion of the tax reform proposal that we expect the government will present to Congress in the second week of August.

All in all, our models point to a period of unusually high volatility in the COP owing to the external environment and the beginning of Gustavo Petro’s presidential term. However, levels significantly above 4,300 pesos are not explained by any structural or temporary shock (chart 2). In fact, we think recent historical high levels above 4,500 pesos were overreactions to an illiquid market and should vanish fairly quickly. In addition, BanRep explicit communication of non-FX intervention could keep volatility high while preventing speculative extrapolative expectations, and eliminate levels significantly above our fit level of about USDCOP 4,300. For now, we keep our forecast of COP returning to levels close to USDCOP 4,000 by the end of the year as the effect of the presidential season declines and reflecting a partial reversion after the external environment eases once developed countries’ central banks approach the end of their hiking cycles.

Mexico—AMLO’s Presidential Approval and Voter Intentions Ahead of the 2024 Presidential Election

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

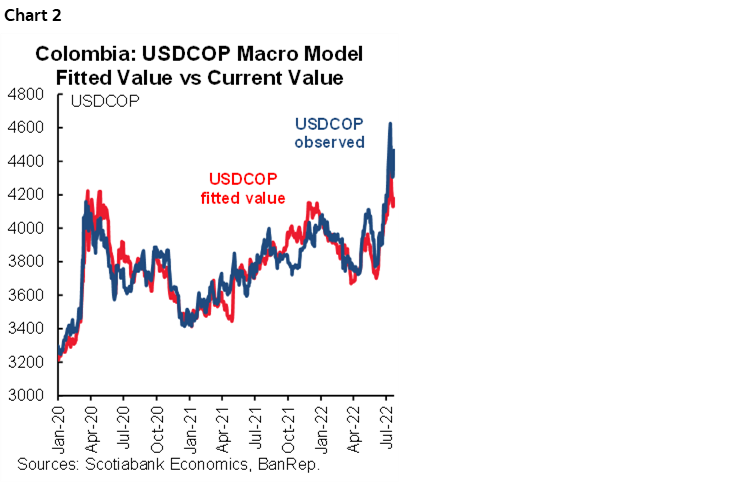

With a 75% approval rating, President Lopez Obrador started off his mandate with the strongest approval rate of any president since at least 1994. And with two-thirds of his presidential term behind him, Lopez Obrador continues to enjoy high ratings from Mexican voters (the Oraculus.mx poll-of polls puts AMLO’s approval rate at 62%) (chart 1). In fact, at this stage of a presidential term, AMLO’s approval rate is the highest among the last five presidents, stretching back almost 30 years. The highest “terminal approval rate” (at the end of a 6-year mandate) since 1994 was achieved by Ernesto Zedillo, who closed his presidency with a 67% approval rate, after kicking off his time as president with the lowest approval rating of any president in the same period.

These political factoids raise an interesting question: Does history suggest that a 60% approval rating guarantee that a president’s party will remain in power? The answer is a resounding “No”. President Felipe Calderon (PAN party) closed his mandate with a 58% approval rate, yet his party lost the presidency in 2012 to the PRI’s Enrique Peña Nieto (who ended his mandate with an approval rate of less than half, with the second lowest among presidents in the last 30 years—at 23%).

Note, however, that the approval rating of AMLO’s Morena party is also materially higher than that of any opposition party in the country, with voter intentions for the 2024 presidential election currently at 43%, more than twice as high as the two strongest opposition parties (PRI and PAN), both of which stand around 17% (chart 2). This suggests that if the opposition wants to present a credible candidate who could challenge the government in the 2024 presidential election, it would have to continue with its recent strategy of forming a coalition, and likely broaden it, in order to have a chance of winning in 2024.

The PRI-PAN-PRD coalition has been able to secure a few victories working together. But it is noteworthy that in the last election (June 2022), Morena still won four out of six Gobernatorial elections, all of which were previously held by the opposition (Quintana Roo, Oaxaca, Hidalgo, and Tamaulipas), while the opposition held onto Durango and Aguascalientes. All six states were previously held by the opposition. The two states retained by the opposition saw the opposition compete as a block, whereas in Hidalgo the opposition lost as a PRI-PAN-PRD block. In Oaxaca, the PAN competed on its own, and the PRI-PRD formed an alliance. In Quintana Roo, the PAN-PRD formed an alliance, while the PRI competed on its own. And in Tamaulipas, the opposition lost despite forming a PRI-PAN-PRD coalition.

The most recent polls suggest that for the 2024 election, the PRI-PAN-PRD block would still lose against the Morena coalition by about 10 percentage points, with the gap widening recently (chart 3). Even if the MC party, which has so far been reluctant to form a coalition, Morena and its allies are still ahead in voter intention polls, although in that scenario, the gap is close to the poll’s margin of error (chart 4).

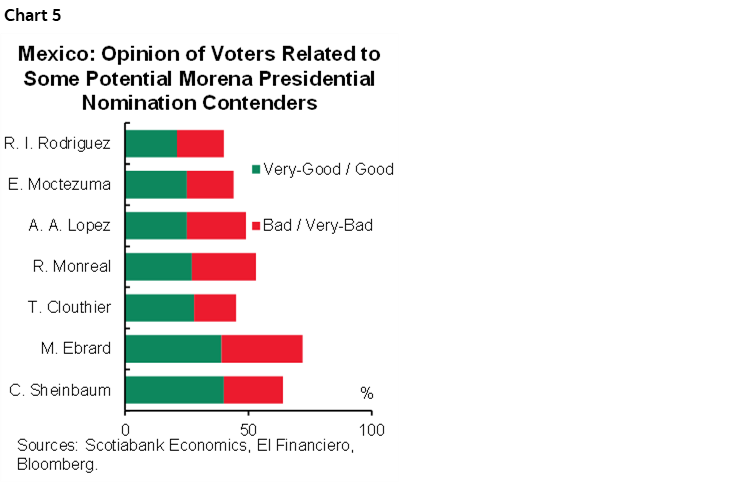

Another element to consider is the candidates both for Morena and the opposition. In Morena, the front-runners include Claudia Sheinbaum, the Mayor of Mexico City, who many consider to be AMLO’s personal choice (chart 5). She is seen as providing continuity with AMLO’s administration. Another Morena front-runner is Secretary of Foreign Affairs Marcelo Ebrard, who is viewed as a pragmatic politician (he was formerly in the PRI and PRD), but who has a much higher rejection rate in polls than Sheinbaum, and is not believed to be AMLO’s top choice as his successor—even if he was AMLO’s successor as mayor of Mexico City. Others potential candidates for Morena include Ricardo Monreal (another pragmatic politician formerly of the PRI), who is perceived to have fairly independent views. A more recent entry into Morena’s potential candidate pool is Interior Minister Adan Augusto Lopez, whose first foray into Federal politics came when AMLO brought him into the role of interior minister halfway through his mandate, and who is an AMLO loyalist, also representing continuity with AMLO’s policies.

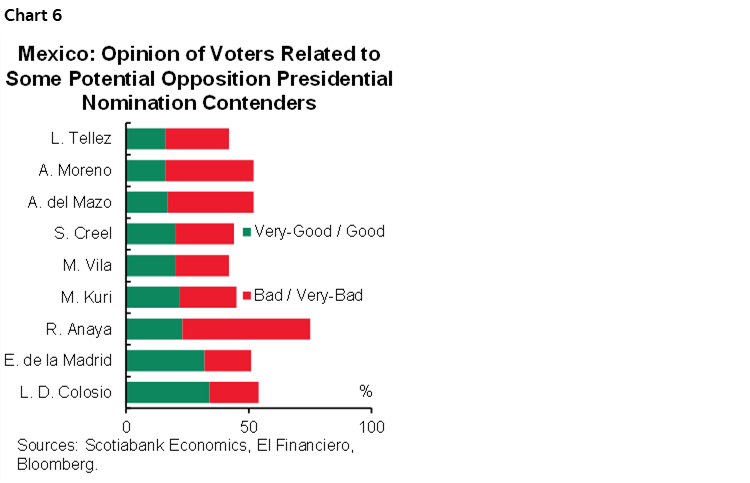

For the opposition, polls suggest that the strongest contender is Monterrey Mayor Luis Donaldo Colosio (chart 6). A young (37-year-old) politician whose father was assassinated campaigning for the presidency in the 1994 presidential contest. He is seen as a charismatic contender, who has a reputation for strong ethics and pragmatism. He is currently an activist in the MC party, which has a relatively low party voter intention at the Federal level (under 10%), even if it currently controls the governorships of 2 of the most strategic states in the country—Nuevo Leon and Jalisco. Enrique de la Madrid, a Harvard educated career civil servant who has also worked in the private financial sector, is also seen as one of the top contenders. His father was president of Mexico 1982–88, and was tasked with rebuilding the economy after the 1982 crisis. Enrique de la Madrid’s voter intention numbers are similar to Colosio’s, but he is currently pitching himself as a “citizen candidate”, independent from any of the major political parties. Other potential contenders for the opposition include PRI party president Alejandro Moreno, who has recently come under fire, and former PAN presidential contender Ricardo Anaya who enjoys a high national recognition, but a higher than 50% rejection rate in some polls.

The presidential elections are still two years away, but at this stage Morena appears to be the party to beat. Polls suggest that, for it to have a strong chance to unseat Morena from government, the opposition will likely need to form a broad coalition, including the MC party, which has so far been reluctant to be part of a coalition. We anticipate that the electoral process will start coming into focus at some point over the next 12 months, with the synchronization of the US and Mexican 2024 presidential elections adding another angle to watch.

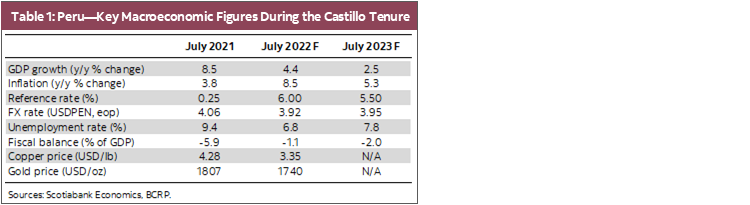

Peru—The Government Begins Its Second Year in Survival Mode

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

By the time you read this, President Castillo will have delivered his mandatory July 28 State of the Nation address. We will produce an analysis on the address on August 2, with emphasis on policy guidelines, economic in particular. However, politics in general is likely to be at centre stage in President Castillo’s mind at the moment. Indeed, the most challenging issue that the Castillo Regime will need to deal with as his second year in office begins is frankly, political survival.

President Castillo has already tried to safeguard the survival of his administration with the removal just over a week ago of the Minister of the Interior, Mariano Gonzalez, who was bent on pursuing a number of individuals close to the president, and who are in hiding from prosecution for corruption. The new Minister of the Interior, Willy Huerta, has already been accused by prosecuting attorneys of obstruction of justice for not providing police support to their actions.

And, yet, the survival of the Castillo Presidency was again put in jeopardy this week when one of the fugitives, Bruno Pacheco, who was Secretary General to the Presidency during the early months of the Castillo Regime, turned himself in. According to press reports, Pacheco has already admitted that: 1. a number of high-ranking police officials had paid bribes for their appointments, and that these payments were managed by President Castillo’s nephews; 2. the current Secretary General of the presidency, by order of President Castillo himself, assisted Pacheco in hiding; 3. twelve members of Congress received special “benefits”, presumably in exchange for their votes against the impeachment of President Castillo. This would represent an increase from the six members of Congress already under investigation.

The Castillo Government thus begins its second year besieged by corruption allegations, with ties involving family members. His presidency is weakening and he himself is increasingly isolated. Corruption issues are pretty much putting all other matters of discussion on the back burner, including the economy—despite concerns over inflation and decelerating growth.

Meanwhile, the Cabinet is, in practice, quietly holding its own, albeit operating at a relatively low gear. A small cohort of three or four members dedicated to shielding and defending President Castillo, with the remainder evading politics and mainly involved in managing their individual ministerial responsibilities. The Minister of Finance, Oscar Graham, is among the latter. This is just enough to allow the State to perform.

With five corruption investigations focused on President Castillo himself, and likely more coming following the testimonies by Bruno Pacheco, impeachment continues to be part of the political discussion. But impeachment depends on Congress, and it remains unclear whether there will ever be enough votes in favour. Pacheco himself may have provided the key as to why sufficient votes are not forthcoming when he suggested that at least a dozen members of Congress may have been swayed by “benefits”. The past impeachment garnered 78 votes of the 87 votes needed. Twelve votes would be enough to swing the results.

The newly elected congressional leadership, with Lady Camones (Lady is her name, not a title, in case you were wondering) as spokesperson, appears divided on the issue of impeachment. While Ms. Camones has suggested the possibility of seeking an impeachment, another member of the four-member Board has stated that this is not part of their mandate.

Meanwhile, President Castillo begins his second year with yearly inflation (to June) at 8.8%. Luckily, inflation is not significantly dependent on government management. Furthermore, there are signs that inflation is starting to turn, and we expect the yearly rate to come in at 8.5% in July (table 1). If so, this would validate the BCRP’s belief that inflation peaked in June. Even so, we continue to expect the BCRP to raise its reference in August from 6.0% to 6.5%, mainly to reinforce the anti-inflation message. However, if inflation declines again in August, as we expect, then the BCRP would conceivably no longer see the need for any further rate increase. This would also provide the Castillo Regime with some relief, as a rising cost of living is politically bad for any government. Inflation was 3.8% at the beginning of the Castillo Administration (July 2021), will hopefully have peaked in June, and then decline towards around 5% a year from now.

Growth was not so bad during the first year of the Castillo Regime. Based on official figures to May, and our estimate for June, GDP growth would have been 4.4% in the last 12 months. This continued to reflect a rebound from past COVID-19 mobility restrictions, which will carry very little weight going forward. We expect a significant slowdown to 2.5% for his second year in office. The Quellaveco copper mine, which has just begun, will help by adding nearly half a percentage point to growth once it is in full swing. The strength and professionalism at the ministry of finance notwithstanding, we do not see overall State management amending sufficiently for fiscal policy to drive growth significantly, nor do we se politics improving enough for business confidence and investment to return to normal. Unless there is a regime change, in which case anything could happen.

The fact that metal prices are lower today then a year ago, also does not bode well. While inflation may have peaked in June, the fiscal deficit has peaked to the downside at around 1% of GDP currently. The trade balance, at USD 15.4 bn over the 12 months to May, has also likely topped out. Macro accounts will continue robust, given such strong starting points, good economic management, and also simply because metal prices are still quite acceptable. Thankfully, just as politics did not interfere with Peru’s strong macro accounts in the first year of the Castillo Government, there appears little reason to believe it will interfere in the second.

The unusual, and distressing, thing about Peru today is that there seems to be more uncertainty concerning whether President Castillo will still be in office a year from now, than there is regarding our economic forecasts over this time frame.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Forthcoming |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

| COSTA RICA | |

| Website: | Click here to be redirected |

| Subscribe: | estudios.economicos@scotiabank.com |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.