ECONOMIC OVERVIEW

- BanRep, Banxico, and BCRP decisions have surprised practically all of us over the past week, impacting local assets already shaken by a huge US employment print with an additional source of uncertainty.

- Economists and markets that appeared confident in their expectations for monetary policy in the near-term were given a wake-up call, not just in Latin America, but also in developed markets. Next week’s US CPI release will call the shots for markets the world over.

- For those looking to refine their bets on central bank rates, the regional calendar is, unfortunately, somewhat bare of data that could materially shift expectations—except perhaps in Colombia, with Q4 GDP.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Colombia and Mexico.

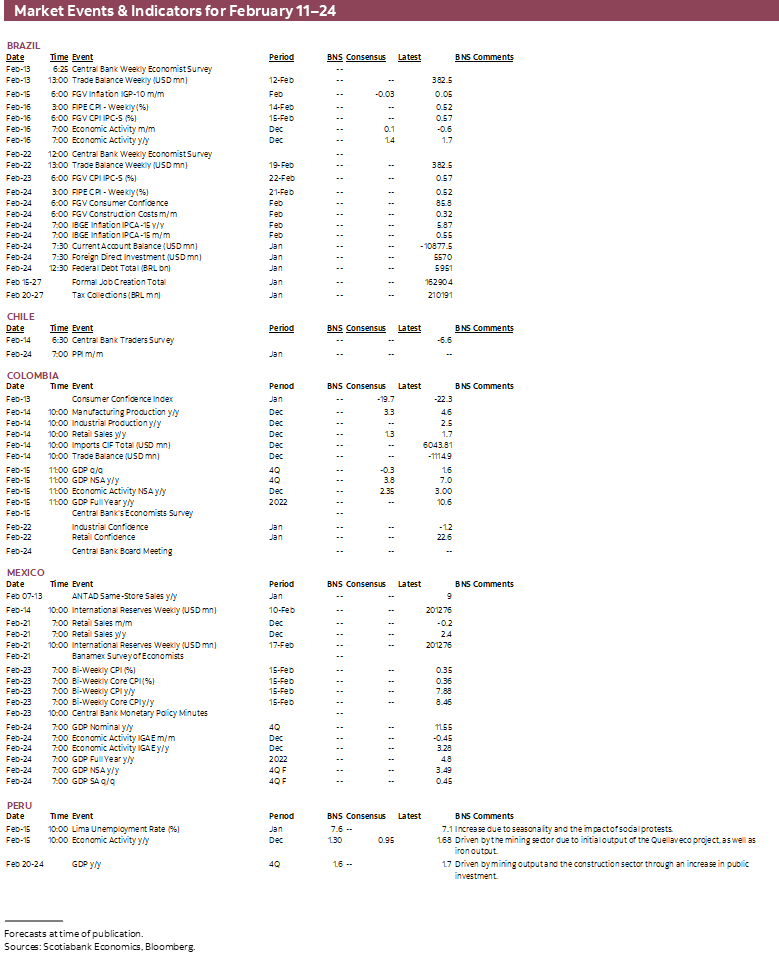

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period February 11–24 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: MARKETS REASSESS GLOBAL AND REGIONAL POLICY OUTLOOK

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- BanRep, Banxico, and BCRP decisions have surprised practically all of us over the past week, impacting local assets already shaken by a huge US employment print with an additional source of uncertainty.

- Economists and markets that appeared confident in their expectations for monetary policy in the near-term were given a wake-up call, not just in Latin America, but also in developed markets. Next week’s US CPI release will call the shots for markets the world over.

- For those looking to refine their bets on central bank rates, the regional calendar is, unfortunately, somewhat bare of data that could materially shift expectations—except perhaps in Colombia, with Q4 GDP.

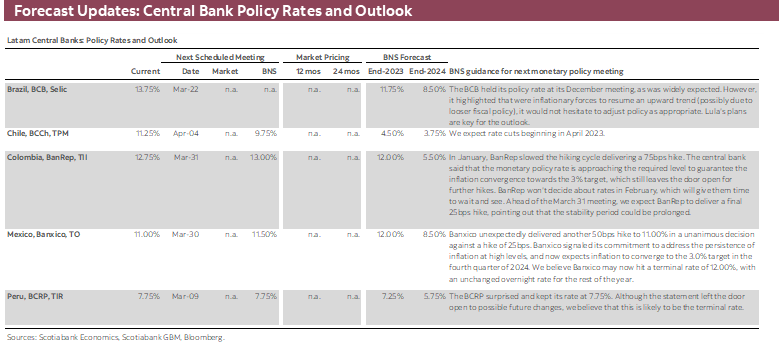

BanRep, Banxico, and BCRP decisions have surprised practically all of us over the past week, impacting local assets already shaken by a huge US employment print with an additional source of uncertainty.

At one end, Banxico lifted its overnight rate by 50bps, compared to the universal expectation of a 25bps move. At the other end, a quarter-point hike is also what economists had projected for the BCRP, which instead chose to leave its policy rate unchanged at 7.75%. Meanwhile, BanRep preferred to slow its pace of tightening to a 75bps increase against our 100bps forecast. Aside from rates policy, Chile’s statistics agency also published a stronger than expected inflation reading on Wednesday that has (at least temporarily) reduced the odds of a rate cut by the BCCh at one of its Q2 meetings.

Economists and markets that appeared confident in their expectations for monetary policy in the near-term were given a wake-up call, not just in Latin America, but also in developed markets. For instance, strong jobs data in the US have motivated traders to incorporate an additional Fed hike this year. Even in Canada, Friday’s scorching employment gain has sowed a seed of doubt into the view that a long pause from the BoC is all but certain.

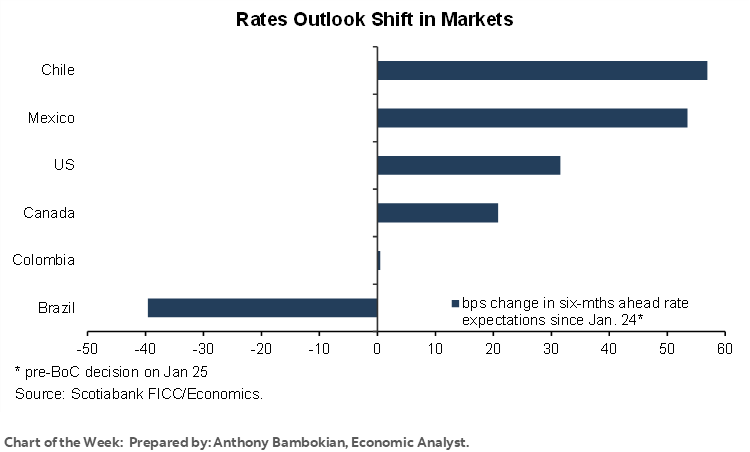

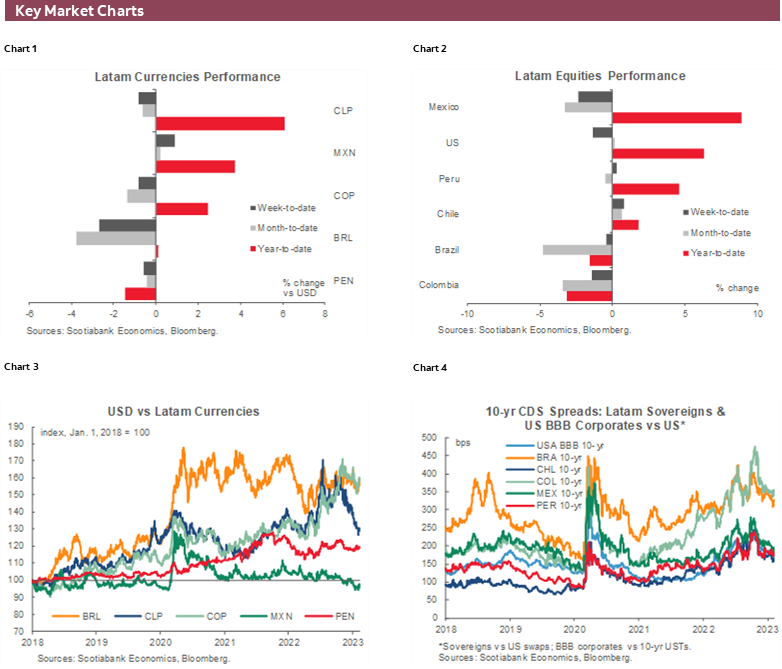

Six-months ahead market-implied rate expectations have changed across most of the Pacific Alliance, Brazil, and the US. Traders added the equivalent of ~30bps to the Fed’s peak rate (now rounded at 5.25%), with negative spillovers on the global market mood. Next week’s US CPI release on Tuesday will be the highlight of the global trading week and will likely be the dominant force of regional assets.

In the case of Banxico, markets lifted their expectation for the terminal overnight rate to practically 12% (as is our updated projection for Banxico). As for Chile, contracts did not go as far as pricing in rate hikes since the bank is clearly on hold, but three-months-out implied rates no longer show an expected 25bps cut.

At the other end of the spectrum stand Peru’s and Brazil’s central banks who blinked and now traders have positioned for relatively less hawkish outcomes; despite BanRep’s smaller hike, market-implied rates were little changed. We say ‘less hawkish’ as it will continue to be the case that policy rates will remain well into restrictive territory for months/quarters to come.

It’s difficult to get a clear sense of how much in rate hikes has been discounted in Peru, but at least Wednesday’s hold of 25bps was a shock, while we await clearer signals from local markets.

In Brazil, traders had until recently tilted towards the possibility of an extra BCB hike on the bank’s hawkish minutes and its continued claims regarding the risks of expansionary fiscal policy. This was all before reports that the BCB will reassess its inflation target to a higher level (perhaps in part to appease Lula) that has actually seen a (rough) 50bps U-turn in BCB rate pricing six months hence (at 13.50% vs 14% prior to the report).

For those looking to refine their bets on central bank rates in the months ahead, next week’s the regional calendar is, unfortunately, somewhat bare of data that could materially shift rates pricing in markets—except perhaps in the case of Colombia.

As our economists argued in last Friday’s Weekly, Q4 GDP data due for release on the 15th will be a key input into BanRep’s decision-making. This will help determine whether they complement their latest 75bps increase with a 25bps hike at the late-March rate-setting meeting. The GDP data will be preceded by retail sales and industrial/manufacturing production figures the day before and will be released alongside the results of the latest BanRep survey of economists.

Chile’s central bank also publishes the results of its traders’ survey on Tuesday, which we will monitor for whether rate cut bets have been pushed out as far as the second half of the year following the most recent BCCh decision and January’s inflation beat. The Peruvian data calendar presents unemployment rate and economic activity on Wednesday, but we’re attentive to the possibility of growing unrest in the country if the Congressional session ends today without an agreement on early elections; at writing, lawmakers had not reached an agreement. Brazil’s weekly highlight is also economic activity on Thursday (though politics will remain the focus for markets), while Mexico’s data and events calendar presents little of note.

PACIFIC ALLIANCE COUNTRY UPDATES

Colombia—FX Drivers

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

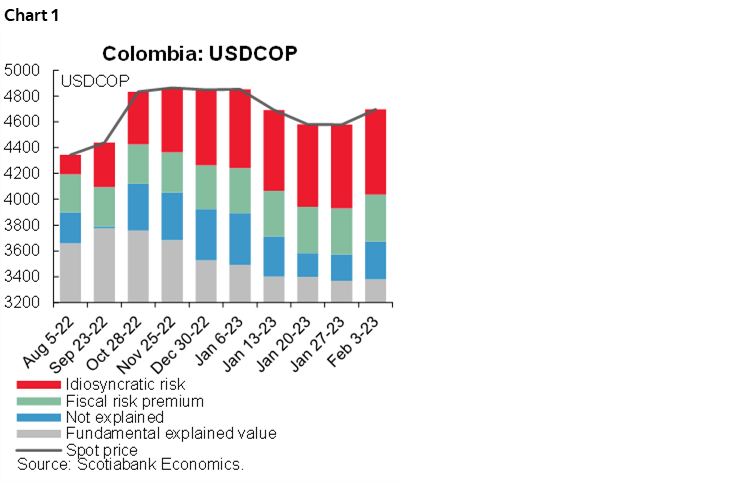

Colombia has the most flexible exchange rate framework of the PAC countries, which serves as an initial shield against external shocks to domestic economic activity. In fact, thanks in part to the FX regime, domestic economic cycles are smoother. However, the cost of this regime is that the volatility of the COP is higher and sentiment about the economic environment affects it faster and more aggressively in the short run. Therefore, it is important, in our opinion, to know what is driving current COP dynamics to see if domestic and international recent shocks are already priced in or if there is more room for sharp movements in the short run.

Our FX model allows to break down some effects that we believe can explain short-run movements. We decompose nominal COP levels among four components: the first is an explained factor which responds to conventional defined variables (i.e., terms of trade, interest rates differentials, peers common dynamics, and absolute risk perception), second is an idiosyncratic effect (political and monetary policy stands), third is the risk premium due to losing the investment grade status in 2021, and fourth is a component that accounts for liquidity and relative risk perception.

In chart 1 we show a representation of the FX fundamental value split in those four components. Between September/October 2022, the world faced a strong volatility episode in which the US dollar strengthened worldwide. Meanwhile, idiosyncratic risk started to be relevant in the strong depreciation of the COP—while the peso overreacted in relation to that seen among its peers. Additionally, the part of the model that is not directly explained—which we think it’s part of the COP that is affected by lower liquidity and higher relative risk perception versus peers—increased significantly. When liquidity returned in January and peers were affected by their own idiosyncrasies (i.e., Peru and Brazil political noise), the COP’s gains exceeded those of its peers. However, after the most recent jobs data in the US, the COP has returned to what, according to our model, is a good fit for the short run, between COP4,700 and 4,850. This level incorporates ~COP650 of idiosyncratic risk that has stabilized this year since markets got used to the communications strategy from Petro’s administration and already included the extra uncertainty around his political and economic agenda this year.

All in all, according to our short-run model the currency has so far continued ‘paying’ a premium due to idiosyncratic risks, which means that volatility around the current domestic economic and political situation is already priced in. In contrast, volatility will continue to come from international monetary policy. We think that, at the moment, external volatility affects not only international risk appetite but also liquidity in the COP market.

What may come next? Despite known risks being embedded already in the COP, there are challenges on the horizon. Idiosyncratic risk can change, a trigger for that could be the Pension Reform discussion, which is due to start in March. In this discussion there are many alternative outcomes which are crucial for the future of the currency. If the Pension Reform aims to significantly reduce flows to the Private Pension Funds, it could represent a strong negative signal for offshore players that may see the possibility of losing a relevant local counterpart. On the other side, if the Pension Reform trends towards being watered down, thus erasing part of the idiosyncratic risk, the stability in the COP would last longer.

Mexico—Banxico Decoupled, in the Opposite Direction to What it Had Hinted; What’s Next?

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Banxico’s board has been talking about the possibility of decoupling from the Fed for some time. At yesterday’s meeting, it decoupled from the Fed, but in the opposite direction as the market had anticipated. Instead of ending its tightening cycle earlier and easing its foot on the economic brake earlier than the Fed, Banxico followed the Fed’s tightening slowdown to 25bps with choosing to press both feet against the brakes with a 50bps hike on February 9th. It was also noteworthy that with dissenting dove deputy governor Esquivel now replaced by Omar Mejia, this 50bps hike was unanimous. Why did Banxico decide to decouple in the opposite direction than it had previously hinted?

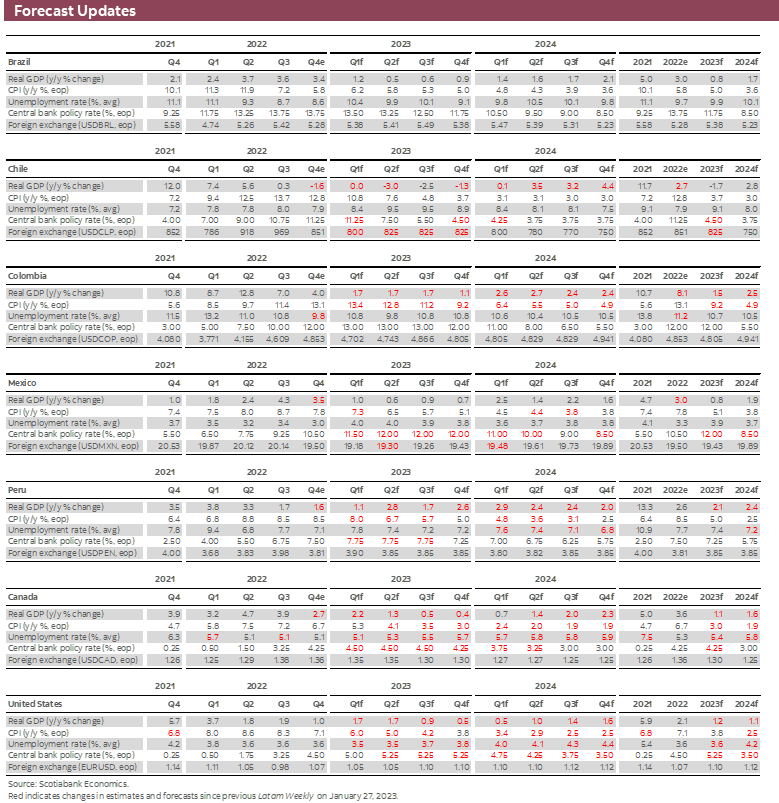

- As the statement suggested, the Mexican disinflation process has been slower than anticipated. With that, Banxico revised its expected inflation path upwards, and now does not expect inflation to converge to its target until Q4-2024, when inflation is seen at 3.1%, from 3.0% previously. Expectations for Q3-2024 were revised upwards by 0.3ppts, however, as were forecasts for essentially the whole of the projection horizon.

- Banxico is also worried about with the stubbornness of core inflation (8.45% y/y in January), which currently sits 0.5ppts above headline inflation (7.91% in January). Banxico also noted that the balance of risks to inflation remains skewed to the upside.

The implications of Banxico’s surprise are complex.

On a positive note, the board’s extreme caution on inflation, after most central banks globally (including Banxico) misdiagnosed the inflation problem, is prudent as erring on the side of caution with inflation may be the right approach to re-strengthen credibility.

On the flip side, Banxico’s 180 degree turn on the direction of its decoupling from the Fed was another misdiagnosis of inflation dynamics in the country—which is not great for credibility. We tend to agree with deputy Governor Heath’s comments last month that we’re likely at an inflection point in inflation—outside of core services inflation that we’ve been arguing for a while will likely not peak until the end of the current quartet.

We believe that Banxico continuing to track the Fed was the right decision as it would have avoided a de facto acceptance that it once again missed the mark on inflation dynamics. However, given the dent to the credibility of global central banks regarding inflation around the pandemic era, if mistakes are going to be made it is better to err on the side of caution. Hence, we don’t see too much harm in Banxico’s cautious approach.

At Scotiabank Economics, we made material adjustments to our anticipated policy rate path for Banxico and the Fed, incorporating a Fed that reinforced its message of higher rates for longer, and a Banxico that took the “dovish decoupling” off the table, at least for the time being.

We continue to anticipate that Banxico will ease earlier and more aggressively than the Fed but have delayed our anticipated start of the easing cycle, and now look for the board to support 50bps in cuts throughout its MPC meetings in 2024, but being mindful of keeping a 500–600bps spread over US policy rates. Recall that Banxico’s Governor said on February 10th that although the Fed does not dictate Banxico’s decisions and both countries have different inflation dynamics, she acknowledged Fed policy remains a relevant driver.

Next week we have a very light week in terms of data, with ANTAD’s same store sales being the main event. However, the past two weeks gave us a good indication of how the economy is evolving. The Mexican economy likely ended 2022 on a deceleration path, although manufacturing seemed to regain some momentum in December. However, looking at data north of the border, it seems the goods sectors (more closely linked to Mexican manufacturing) have been underperforming services. This seems consistent with the recent flattening in Mexican exports growth.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.