ECONOMIC OVERVIEW

- Banxico and BCRP officials will decide on their respective policy rates next week, with 25bps hikes expected from both, while regional inflation prints help us refine our expectations for monetary policy in the months ahead.

- Colombia’s CPI data for January is expected to show the smallest acceleration in inflation in many months, while Chile’s inflation is seen falling to 12%. Meanwhile, in Brazil, the disinflationary process seems to have stalled.

- In this Latam Weekly, our economists in the region discuss Pemex-related fiscal risks in Mexico, the impact of protests on Peru’s output, Colombia’s political risks ahead, the Chilean peso’s ‘too-fast’ appreciation, and Lula’s spat with Brazil’s central bank.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico, and Peru as well as Brazil.

MARKET EVENTS & INDICATORS

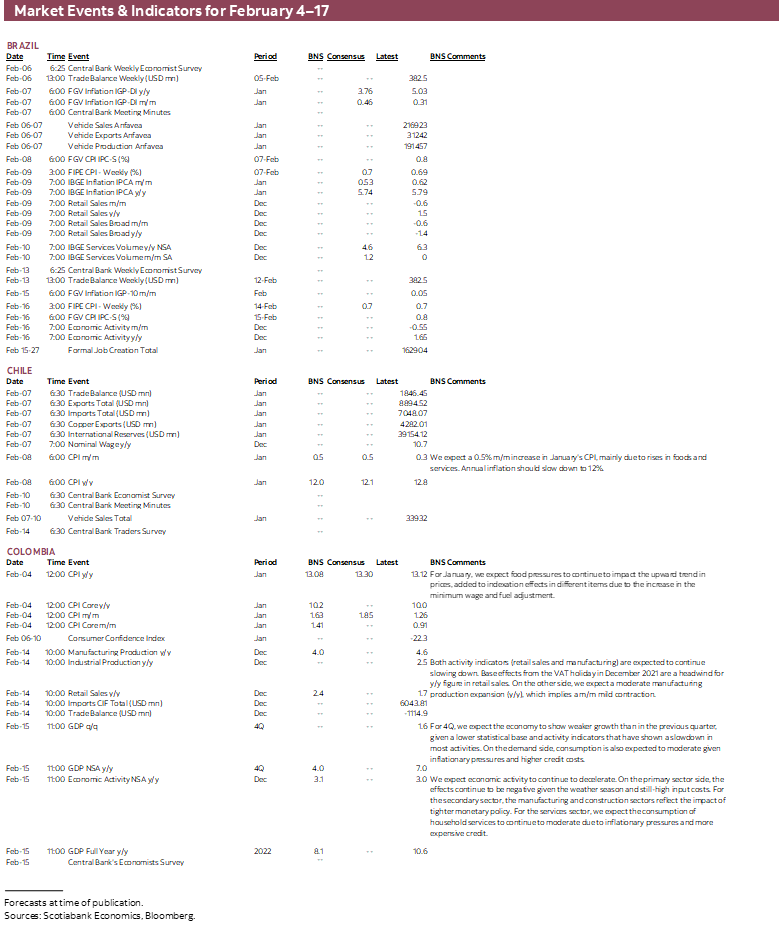

- A comprehensive risk calendar with selected highlights for the period February 4–17 across the Pacific Alliance countries and Brazil.

ECONOMIC OVERVIEW: BANXICO AND BCRP ALONGSIDE REGIONAL CPI DATA

Juan Manuel Herrera, Senior Economist/Strategist

Scotiabank GBM

+44.207.826.5654

juanmanuel.herrera@scotiabank.com

- Banxico and BCRP officials will decide on their respective policy rates next week, with 25bps hikes expected from both, while regional inflation prints help us refine our expectations for monetary policy in the months ahead.

- Colombia’s CPI data for January is expected to show the smallest acceleration in inflation in many months, while Chile’s inflation is seen falling to 12%. Meanwhile, in Brazil, the disinflationary process seems to have stalled.

- In this Latam Weekly, our economists in the region discuss Pemex-related fiscal risks in Mexico, the impact of protests on Peru’s output, Colombia’s political risks ahead, the Chilean peso’s ‘too-fast’ appreciation, and Lula’s spat with Brazil’s central bank.

With the Fed in the rear-view mirror, delivering an as expected but lukewarm 25bps hike, Banxico and BCRP officials will decide on their respective policy rates next week, while regional inflation prints (Mexico’s included) help us refine our expectations for monetary policy in the months ahead.

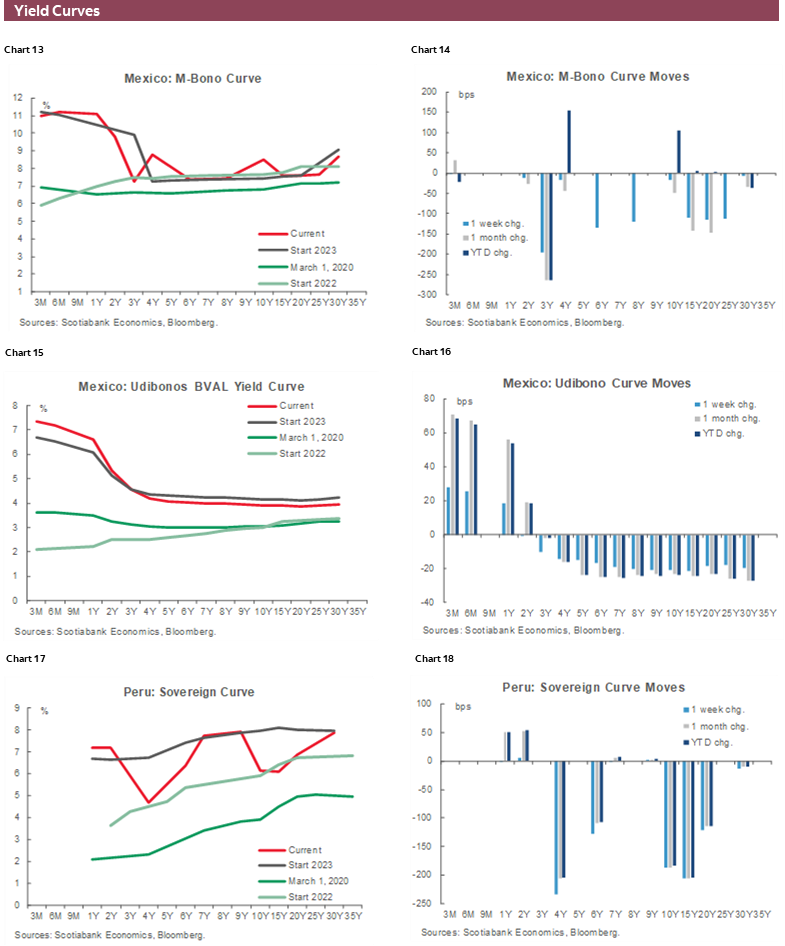

In Mexico, Fed decoupling talk had gained traction in late-2022/early-2023 before the H1-Jan CPI print released last week poured cold water on those calls. In particular, the uptick in core inflation (goods) is a point of concern for policymakers. Recent comments from Heath and Mejia suggest Banxico is not yet at a divergence point and a 25bps hike is the most likely scenario next week. Inflation data for the whole of January will be released the morning of the Thursday announcement, though Banxico will already have this information at hand when it makes its decision on Wednesday evening.

Setting Banxico aside, it is also important to highlight the ongoing discussion regarding the Federal Government’s financial support of PEMEX. In today’s weekly, the team puts the state-owned maturing debt into context, noting that saddling the government’s accounts with it would hurt, but it would not be calamitous. What may be a bigger issue is that weak growth (owing to depressed investment, in part) and high interest rates does not bode well for the country’s fiscal picture.

Peru’s BCRP will likely roll out another quarter-point increase given stubbornly-high inflation which has failed to decelerate as fast as had been anticipated by the central bank. Core prices growth posted a new cycle high in data published earlier this week, although the overall headline CPI increase was significantly lower than expected.

As our Peru economists noted in yesterday’s Latam Daily “although the low inflation in January suggests the possibility that the BCRP might consider the start of a pause in the rate hike cycle, we would not be surprised by an increase of 25bps at its next meeting on February 9, since it seems to us that the factors that explained the low month inflation seem temporary and because core inflation continues to rise.”

Over the weekend, Colombia’s DANE will release CPI data for January that our economists expect will show the smallest acceleration in inflation in many months. Signs of steadying inflation is a positive for BanRep, who is set to deliver a final 25bps hike next month, in the view of our Bogota team. To firm up that view, the team is also looking ahead to the mid-month Q4 GDP release. However, they argue in today’s report that political developments regarding the budget ’top-up’ and the health reform are key risks for markets to monitor between now and the next BanRep decision.

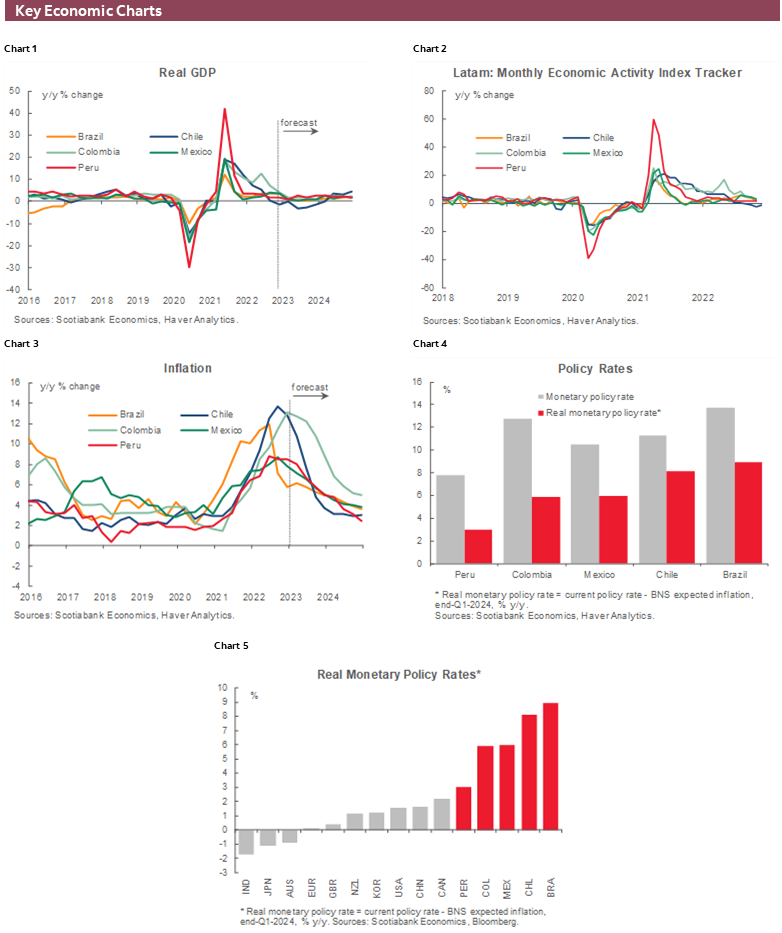

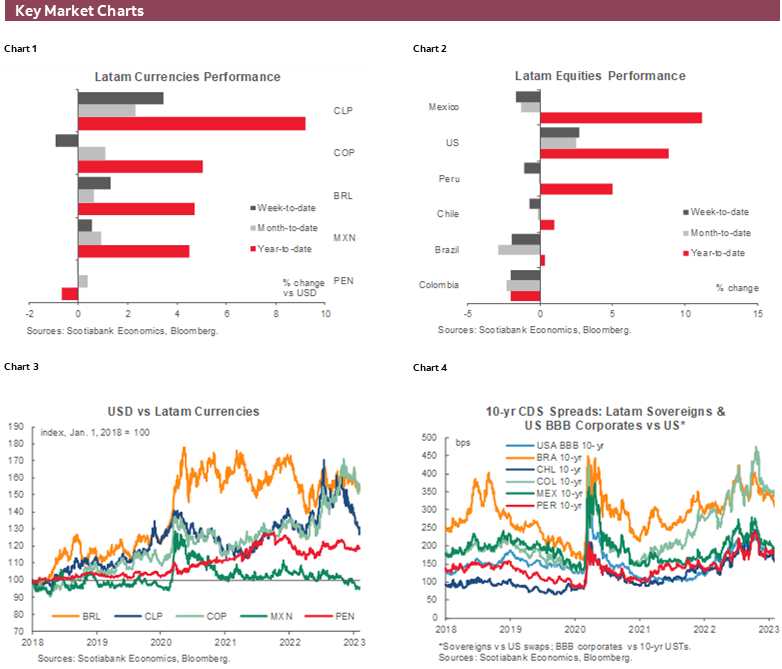

Chile’s INE will also publish prices data next week, where we project a decline to 12% y/y in headline inflation. In Santiago, our economists believe that the recent CLP appreciation has gone beyond that which would be explained by macroeconomic fundamentals. With “more risks of negative than positive surprises” on the prices front, they believe that a faster turn lower in inflation would pull the BCCh away from the path intimated in its baseline scenario—thus shifting faster to a less restrictive stance that could partly undo recent gains in the CLP that resulted from short-term capital inflows.

Finally, Brazilian inflation data out on Thursday is expected to show only a minor decline in its year-on-year pace from December. Macro releases in retail sales and services activity for December will help us refine our forecast for Q4 GDP growth in the country. It’s difficult to see the data pulling the market’s attention away from Lula too much, however, as our economists note “it may still be too early to tell what version of Lula we are getting in his second mandate.” Still, the stalling in inflation points to the BCB being in no rush to think about lowering rates, keeping its Selic rate steady at 13.75% for a few quarters.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—CLP Appreciation: Too Much, Too Soon

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

The Chilean peso has strongly appreciated in recent days, explained by better external financial conditions, resilient domestic activity, and an improvement in terms of trade. Although, it is also driven by short-term capital inflows, the selling of USD to accelerate fiscal spending, forward dollar sales by the BCCh, and perhaps a misjudging of political and economic risks that lie ahead.

In inflation-adjusted terms, the real exchange rate is around its historical average and the USDCLP is overvalued with respect to its fundamental value. But is Chile the same country it was 20 years ago? Obviously not. Chile is the only country negotiating two structural reforms and in the middle of a constitutional process.

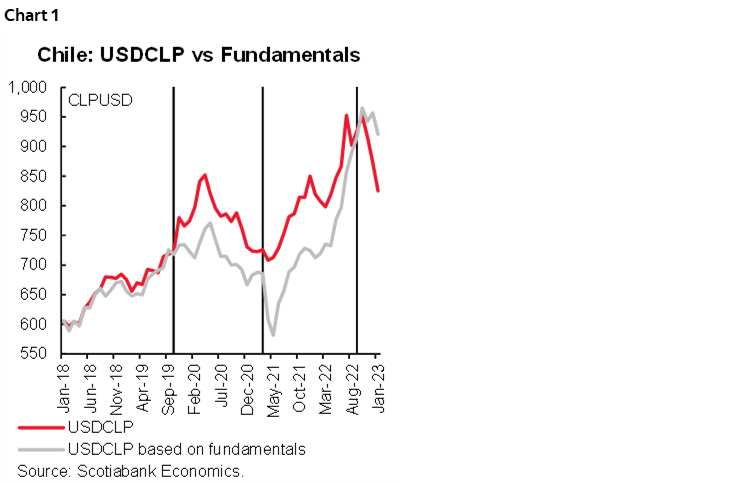

Macroeconomic fundamentals cannot fully explain the strong appreciation of the CLP (chart 1). Political moderation and preliminary signs of fiscal consolidation have allowed for reduced misalignment. Though we observe a better political environment after Sep 4, the tax and pension reforms can be a source of domestic financial volatility and the risk of a non-market-friendly constitutional assembly is not insignificant.

Taking all the above into account, we have adjusted downwards our forecast for USDCLP from 850 to 825 at Dec-2023. However, we do not rule out lower levels in the short-run.

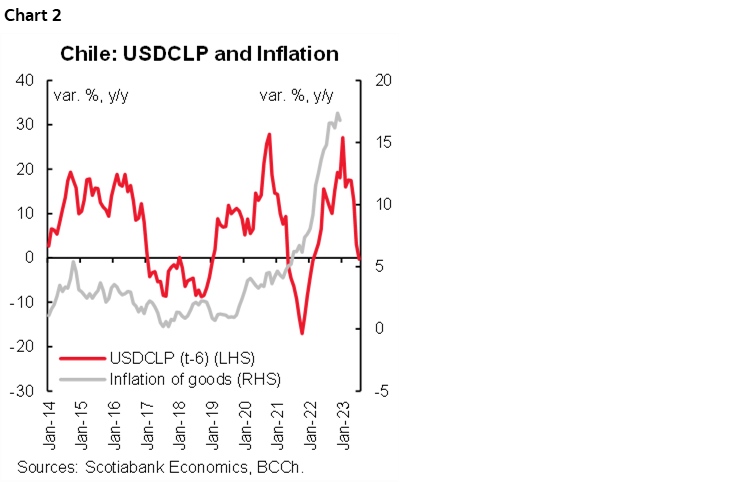

In terms of inflation, we see more risks of negative than positive surprises over the next few months despite one-off and second-round effects. High inventory levels, a negative output gap, a weak labour market, and the multilateral appreciation of the Chilean peso will impact goods inflation (chart 2), food prices, and some volatile items.

We expect a 0.5% m/m increase in CPI in January, in data due for release by the INE on February 8, which would reduce y/y inflation to 12% from 12.8% in December.

All in all, a faster inflationary break will lead the BCCh to modify its monetary policy stance earlier than anticipated in its baseline scenario which should unwind part of the short-term capital inflows behind the CLP appreciation.

Colombia—Relevant Remarks Regarding Monetary Policy Before the Start of the Congress Legislature

Sergio Olarte, Head Economist, Colombia

+57.1.745.6300 Ext. 9166 (Colombia)

sergio.olarte@scotiabankcolpatria.com

María Mejía, Economist

+57.1.745.6300 (Colombia)

maria1.mejia@scotiabankcolpatria.com

Jackeline Piraján, Senior Economist

+57.1.745.6300 Ext. 9400 (Colombia)

jackeline.pirajan@scotiabankcolpatria.com

This week was filled with information related to monetary policy. In Colombia, the central bank staff released the Monetary Policy Report (MPR) showing a new set of economic forecasts for the policy horizon. The central bank revised to the upside its inflation projection and now believes that inflation will stabilize in Q1-2023, closing the year at 8.7%, to then sit within the 2–4% target band at 3.5% in Q4-2024. However, this scenario assumes a strong economic activity deceleration going from an 8.0% GDP expansion in 2022 to only 0.2% growth in 2023 and 1% in 2024. In this scenario, the unemployment rate is expected to rise, and the current account balance will shrink from 6.3% of GDP to 3.9%. BanRep’s staff projects a monetary policy rate path that is on average above the economist consensus, which points to 13% as a terminal rate and a rate of ~10.5% by the end of 2023.

As was the case in the October MPR, we believe that the central bank staff is probably signaling a more hawkish stance than BanRep’s board of directors. It makes us think that the unexpected slowdown in the hiking cycle reflects fears from the board about facing a stronger economic deceleration.

The most relevant publication in the days ahead will be January CPI figures published over the weekend. Recent surveys put the economist consensus at 1.78% m/m and 13.27% y/y, which is higher than our estimates of 1.63% and 13.08%, respectively. That said, despite inflation having a chance to increase further, the acceleration is expected to be the lowest in many months, which is a signal of stabilization in headline inflation. At Scotiabank Economics, we still see a significant probability of inflation peaking in Q1-2023, which may be confirmed by the February reading and which would allow the central bank to consider a final hike of 25bps at the March meeting.

GDP data on February 15 is also key to our view regarding future monetary policy moves. Our estimate for 2022 GDP growth is 8.1%, but we expect a deceleration towards a 1.5% expansion next year (below our previous estimate of 2%). This negative revision reflects an expectation of more muted private consumption and a slower recovery in investment. An economic deceleration is compatible with our forecast for the monetary policy rate reaching 13% and staying at that level until headline inflation drops to single digits.

Ahead of the next monetary policy meeting, the attention will turn to the political agenda. Next week brings the starts of extraordinary sessions of Congress with the first bill up for discussion regarding the budget top-up, which will preliminarily include COP20tn from expected higher revenues due to the tax reform and COP5tn due to greater tax revenue in 2022 thanks to above-expectations growth and oil prices.

The health reform will be presented in mid-February. However, this week, the leader of the Liberal Party, Cesar Gaviria, said that his party will not allow the destruction of the current health system. Instead, he favours strengthening the system. From our perspective, this clearly signals that political negotiations won’t be easy.

Mexico—Pemex’s Support, Fiscal Impact, and Some Perspective

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Over the last couple of weeks, the Federal Government’s support for Pemex has been a big topic of discussion, in the president’s “mañanera” (his daily morning address), in local media, and among investors.

Our sense is that nothing has really changed. There has been some discussion of providing the company with tax relief, as has been the case in the past, but as Undersecretary of Finance Yorio suggested tax relief will likely remain limited—and unlikely to change federal tax dynamics materially.

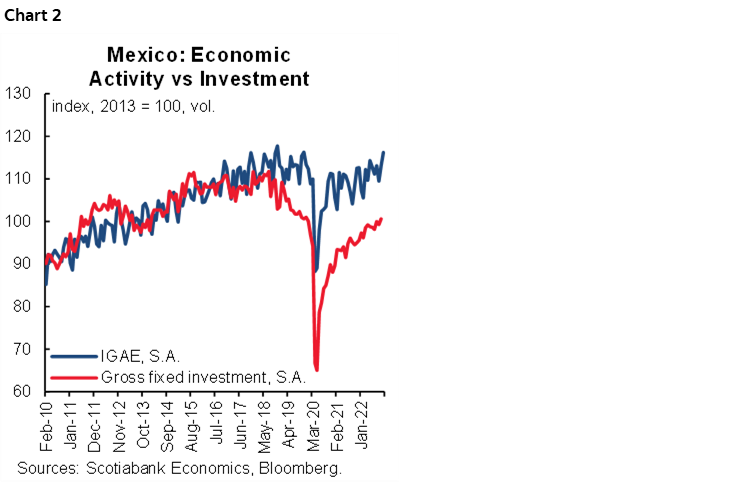

More meaningfully is that we expect that Pemex will continue to see some of its maturing debt (chart 1) being covered by the Federal Government, again, as has been the case in recent years. How relevant are these from the FinMin’s perspective?

If Hacienda were to cover 100% of the company’s debt maturities for 2023 it would likely lead to a fiscal impact of around 0.5ppts of GDP. Material, but nowhere near crippling, and we estimate this would likely be materially smaller than what we perceive to be overly optimistic assumptions about growth and interest rates in the 2023 budget.

- If in 2024 Hacienda decided to again absorb 100% of Pemex’s debt maturities, the fiscal impact would be about 0.6ppts of GDP—again, material, but not crippling.

- Overall, we believe the more important impact of the government’s energy policy (both in oil and power) is more related to the benefits of allocating limited resources to projects that crowd in private investment, rather than those that crowd it out.

- Mexico’s biggest challenge at the moment is very low investment, which will likely undermine future growth. Using the “g – i” methodology (g=growth, i=interest rates) for looking at long term public finance dynamics, the long term issue is that with US yields likely to be around 200bps higher in coming years relative to the past 12, and with growth likely to be lower in Mexico due to weak investment, we will likely have a higher “i”, and a lower “g”. This means a long term fiscal deterioration of around 150–250bps of GDP per year—which will need to be covered by either a public debt ‘drift’, a higher primary surplus, or taxes.

Since 2018, investment rates / levels in the Mexican economy have become abnormally low. As chart 2 shows, investment has considerably lagged the growth of the economy suggesting that not only is future productive capacity not being prepared, but we could even be seeing the maintenance of productive capacity suffering. The gap between gross fixed investment and GDP has become so large, that it may take a period of above trend investment to catch up to the investment lag of recent years. This underperformance in gross fixed investment is particularly remarkable if we consider the international context and the opportunities presented by nearshoring, with China already losing close to 5 percentage points in the share of US imports of goods—but where Mexico has so far only marginally benefited at the aggregate level.

Peru—Growth Amid Protests

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

The protests are showing signs of waning, but their impact and aftermath remain. This impact has been material on both growth and inflation. We should get a better idea of the magnitude of the impact on growth when the December 2022 GDP figure is released on February 15. Meanwhile, the Minister of Finance stated that lost growth for the December 2022 to January 2023 period amounted to over USD500mn, or between 1 and 1.6 percentage points lower growth than otherwise for each month. We consider that the impact in January was likely to have been greater than in December. Overall, due mainly to the impact of protests, we are lowering our 2023 GDP growth forecast from 2.4% to 2.1%. We see further downside to this forecast if protests flare up again.

We recently reduced our 2022 GDP forecast from 2.8% to 2.6%. This forecast had a downside bias even before the December protests. Having said that, it is interesting to note that the early figures that were released on February 1 regarding partial growth in December were not all that bad. Mining and oil & gas GDP reportedly rose 9.3% y/y in December. Copper output was particularly strong, up 19% y/y. Although this reflects in great measure the new Quellaveco mine, it also implies healthy levels of production at other copper mines, and appears to rebuff the notion that protests had impacted mining output during the month. We’ll have a clearer view on this once the production figures by company are released next week.

Public investment rose 9.9% y/y in December, according to the Ministry of Finance. This is lower by half compared to preceding months, but is still not a bad showing.

Where the impact of protests may be more evident is in construction. Domestic cement demand fell a significant 6.7% y/y in December, and this is likely to be enough to drag construction GDP into nil-to-negative territory for the month.

Overall, the balance for December is turning out to be a bit more positive than anticipated. But one should not conclude from this that the economic impact of the political turbulence in the country is negligible. The impact in January should be more evident. While electricity demand was robust in December, the data for January is showing definite signs of weakness, especially demand coming from certain mining operations.

The other manner in which the protests are affecting the economy is in inflation, which rose to 8.7% yearly, in January. We provided an in-depth look at inflation in the February 2 Latam Daily. The bottom line is that inflation should have begun falling in December, and continued declining in January, and yet the opposite is happening. The price components that are most contributing to inflation currently are agricultural produce for domestic markets, which are products that are most vulnerable to roadblocks. Still, with inflation still trending upwards, and inflation expectations having risen from 4.3% to 4.6%, we expect the BCRP to raise its reference rate by 25bps to 8.0% next week. The difference is that this time the chances are that this will be the last time. Of course, we’ve said that before.

At the time of writing, Congress had still not decided on a date for early elections. The initial proposal was to call for elections in April 2024. This proposal, which had already received one of the two ratification votes it needed, was scrapped in order to introduce another proposal with an even earlier date for elections in December 2023. However, this proposal did not obtain the two-thirds of votes it needed. The main issue of disagreement between the congressional parties appears to be regarding whether or not to include a Constitutional Assembly in the early elections format. Meanwhile, the Constitutional date of April 2026 is the only date officially on the calendar.

Brazil—The Puzzle of Brazil’s High Interest Rates … Goes 3D

Eduardo Suárez, VP, Latin America Economics

+52.55.9179.5174 (Mexico)

esuarezm@scotiabank.com.mx

Is he the pragmatist that governed back at the turn of the century, or are we getting a more polarized government? One area which is starting to cause concern is Lula’s relationship with the BCB, and its leader Roberto Campos.

On Thursday, the dispute between the two was aired on full display in Brazilian TV (Rede TV), when Lula said “I will wait for that citizen to finish his mandate to make an assessment to find out what the independent central bank meant”. This follows comments that Lula made when he took office, when he said “It’s silly to think that an independent central bank governor is going to do more than when the president appointed him”.

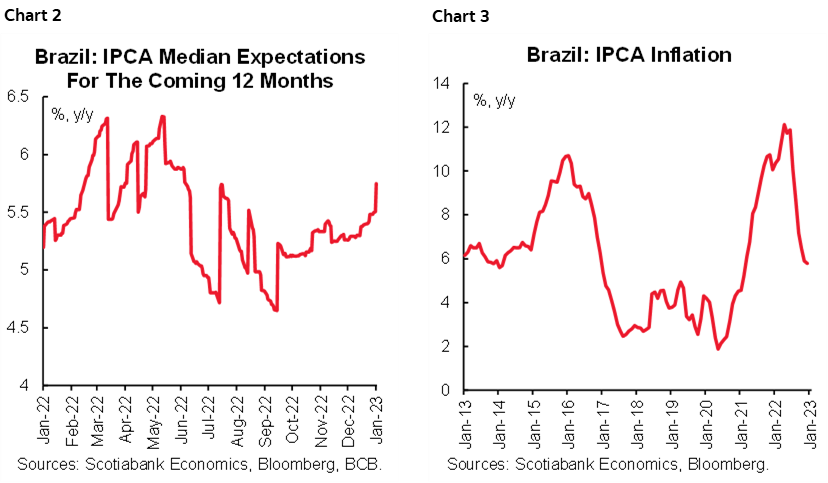

The BCB has for some time struggled to compensate against very loose fiscal policy, which is seen as one of the drivers of Brazil’s high interest rates (as discussed in this classic IMF paper), and it has intermittently highlighted fiscal considerations as part of its rate hike decisions in recent years. In the current spat, Lula is upset over the BCB’s reluctance to cut its policy rate, and the bank’s concerns about looser fiscal discipline (chart 1)—that prevent it from kicking off an easing cycle, despite the country’s inflation having clearly peaked. However, even Lula’s former BCB head and ally Henrique Meirelles noted that Lula’s comments on inflation and BCB policy may have “squandered” the opportunity to kick off the rate easing cycle, by contributing to a reversal of what were anchored and declining inflation expectations back in January.

The median expectation for IPCA inflation from the BCB’s Focus Survey is once again starting to drift higher (chart 2), even when actual IPCA prints have been steadily on a downtrend since last summer (chart 3). The consensus expectation for January’s IPCA inflation also suggests a stalled disinflationary process. The consensus median sits at +0.45% m/m for January’s IPCA, following a +0.62% m/m print in December which represents a turnaround from the negative m/m prints observed during most of the second half of 2022. This dynamic, alongside once again rising longer term inflation expectations will likely keep the BCB’s hand steady regarding the Selic rate.

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.