- Colombia: Monetary policy minutes—high inflation vs economic slowdown explained the split vote in BanRep

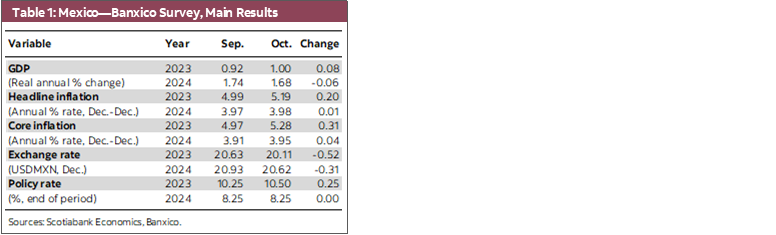

- Mexico: Banxico Survey shows higher year-end inflation expectations

- Peru: Inflation surprises lower in January, but core inflation reaches peak

COLOMBIA: MONETARY POLICY MINUTES—HIGH INFLATION VS ECONOMIC SLOWDOWN EXPLAINED THE SPLIT VOTE IN BANREP

On Tuesday, January 31, BanRep revealed the minutes for the January 27 monetary policy meeting. The minutes showed that all the board agreed that it was necessary for a new rate hike since inflation had not peaked, and given that in December, inflation increased more than expected. However, the discussion was focused on the magnitude of the hike. In fact, the decision was in a split vote, with five members voting for a 75bps hike and two members for 25bps. Interestingly enough, nobody voted for keeping the pace of the hiking cycle and increasing the policy rate by 100bps.

The reason for slowing down the pace of the hiking cycle was not very explicit, but the central bank referred to a better international context which was reflected in reductions in the risk premium in Colombia.

The minutes also highlighted that uncertainty remains high, signaling that the board maintains a data-dependent approach and that the door is still open for a new rate hike in the future. However, the minutes also emphasized that the central bank is in the latest stages of the hiking cycle since in the document it was highlighted that “the monetary policy rate is approaching to the required position to induce inflation convergence towards the 3% target.”

Our take is that the board is signaling that the hiking cycle is in its final stages. BanRep won’t have a rate decision in February, giving them room to wait-and-see the evolution of inflation and economic activity (Q4-GDP will be released on February 15). That said, we still see some space for BanRep to execute a final hike of 25bps in March, reacting to more stable inflation but still more than four times above target, while inflation expectations continue increasing for the longer run and economic activity slowing down at a moderate pace.

Key points about the board’s discussion:

- The majority group who voted for a 75bps hike highlighted that inflation risks remain high, mainly due to FX depreciation and indexation to the minimum wage and the inflation of December 2022. This group is concerned about the increase in inflation expectations, which makes it necessary to maintain a contractionary monetary policy rate.

- One board member who voted for a 75bps hike expressed that some indicators are signaling a reduction in the money demand (low confidence in the currency) which would conduct consumers to prefer international assets, durable goods, or consumption-related goods that, at the end will be reflected in high inflation.

- The dovish group, who voted for a 25bps hike, argued that economic activity is decelerating, and they consider that the central bank is achieving the goal of slowing down the economy. Additionally, the dovish group stressed that the effect of the hiking cycle on the economy will be strongly reflected in economic activity in 2023.

- Moreover, the dovish group also said that the inflation dynamic had been mainly due to a supply shock, but the upside pressures on prices had eased recently. However, they were aware that indexation effects are prolonging the effect of supply shocks in overall inflation.

—Sergio Olarte, María (Tatiana) Mejía & Jackeline Piraján

MEXICO: BANXICO SURVEY SHOWS HIGHER YEAR-END INFLATION EXPECTATIONS

Respondents in the Banxico Survey of Expectations showed higher inflation, rate, and growth forecasts for 2023 (table 1). The mean forecast for inflation moved up from 4.99% to 5.19%, as well as the core component expectation, from 4.97% to 5.28%. For 2024, responses went marginally up for the headline inflation to 3.97%, and to 3.95% in the core component, suggesting that analyst expects stickier dynamics in both headline and core inflation, converging to the Banxico target rate of 3.0% at the end of 2024. In this sense, the median of responses for the expected policy rate at the end of 2023 rose from 10.25% to 10.50%, and stood at 8.25% for the end of 2024. Looking to quarterly forecast, the mean expected rate stands at 11.00% in Q1 and Q2—implying two consecutive hikes of 25bps in the upcoming meetings in February and March—while some analysts foresee the cuts cycling to start in Q3 (10.80% mean forecast). For our part, consider the cuts would start in Q4, ending the year at 10. 50% (vs 10.50% median, 10.35 average forecast).

—Miguel Saldaña

PERU: INFLATION SURPRISES LOWER IN JANUARY, BUT CORE INFLATION REACHES PEAK

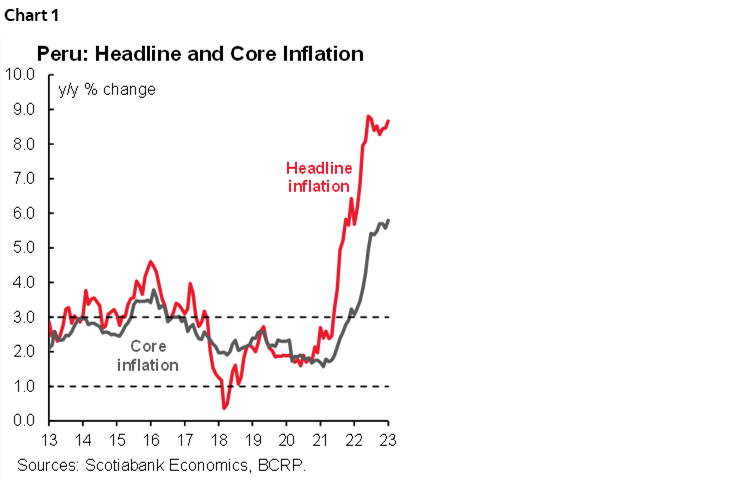

Inflation in Lima reached 0.23% m/m in January data released on Wednesday, February 1, below our forecast (0.76%) and Bloomberg consensus (0.51%). Despite this, year-on-year inflation continued to creep upwards, going from 8.46% y/y to 8.67% y/y (chart 1), a pace that was also below what was projected by the MoF (between 8.8% and 8.9%). Inflation remains well above the upper limit of 3% of the inflation target. This is the 20th consecutive month in which inflation has been above the bank’s target band, and it is highly probable that starting in February it will equal the longest period with inflation above 3%, which was 21 months (between October 2007 and June 2009), since the target band of 1–3% was established in 2007.

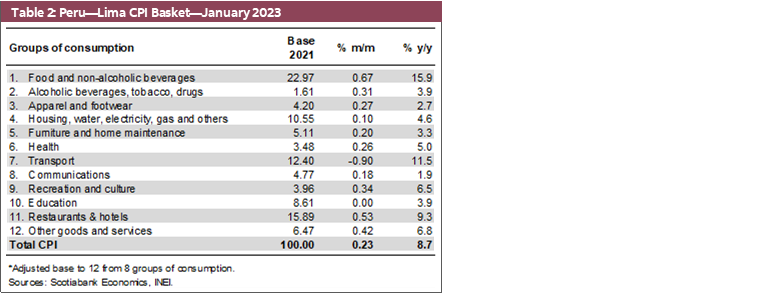

The recent social protests have had an impact on the economy, inflation and the FX rate, and their duration is still uncertain. Inflation in January reflected this impact on food prices, mainly perishable foods such as vegetables, legumes, and tubers, with a rise of 7.7% m/m (table 2), which were partially offset by lower prices for fish (-9.5%), meat (-0.9%), eggs (-2.6%) and cheese (-1.5%). In January, of the 586 products that make up the consumer basket (base 2021), 378 increased (64%), 111 decreased (19%) and 97 remained unchanged (17%), a dynamic like that posted in September 2022.

Core inflation rose from 5.57% y/y to 5.79% y/y, reaching a new peak and accumulating 14 months outside the target range. Various cost indicators, such as wholesale prices, increased from 7.0% y/y to 7.7% y/y, as did machinery and equipment prices, which rose from 0.3% y/y to 2.6% y/y, while construction material prices continued to slow down, going from 4.8% y/y to 4.7% y/y (chart 1 again).

At the city level (considering the 26 most important cities, not only Lima), year-on-year inflation readings accelerated in 19 of them (73%), mainly in the south of the country, which was the area most affected by roadblocks. The number of cities that posted annual inflation above 10% tripled, from 3 to 9.

Looking ahead, although our baseline scenario assumes that the inflation slowdown will continue, this pace is slower than expected. In our January 27 Latam Weekly, we revised our inflation forecast from 4.5% to 5.0% at end-2023. Over the past seventeen months, the central bank raised its reference rate by 750 basis points to 7.75% and raised reserve requirements three times. The real policy interest rate continues to rise and has already reached 3.45%, a level that doubles the neutral rate (1.50%), although it is low compared to other countries in the region. In its latest statement, the central bank left the door open to further increases. Although the low inflation in January suggests the possibility that the BCRP might consider the start of a pause in the rate hiking cycle, we would not be surprised by an increase of 25bps at its next meeting on February 9, since it seems to us that the factors that explained the low month inflation seem temporary and because core inflation continues to rise. Our baseline scenario is for the terminal rate to reach 8.00% in February and remain at that level for most of the year.

—Mario Guerrero

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.