ECONOMIC OVERVIEW

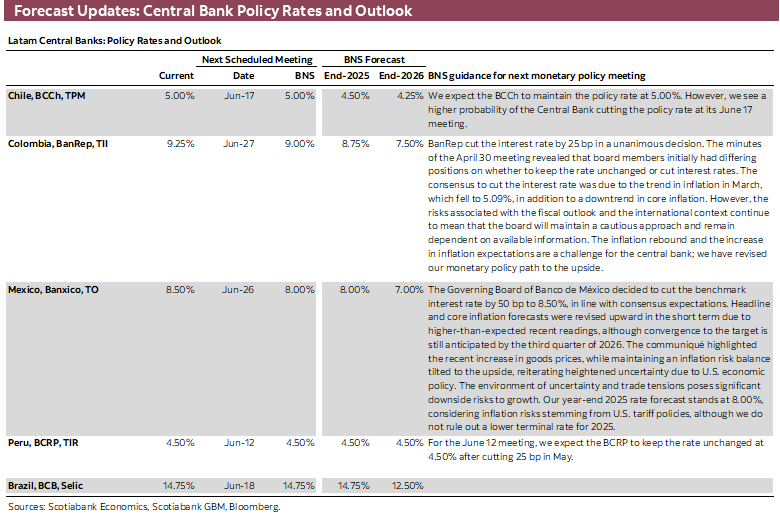

- Key CPI releases await in the Americas, with readings out of Colombia, Mexico, Brazil, and the U.S. all on tap. The BCRP kicks off the June cycle of Latam central bank decisions with a likely hold at its Thursday announcement.

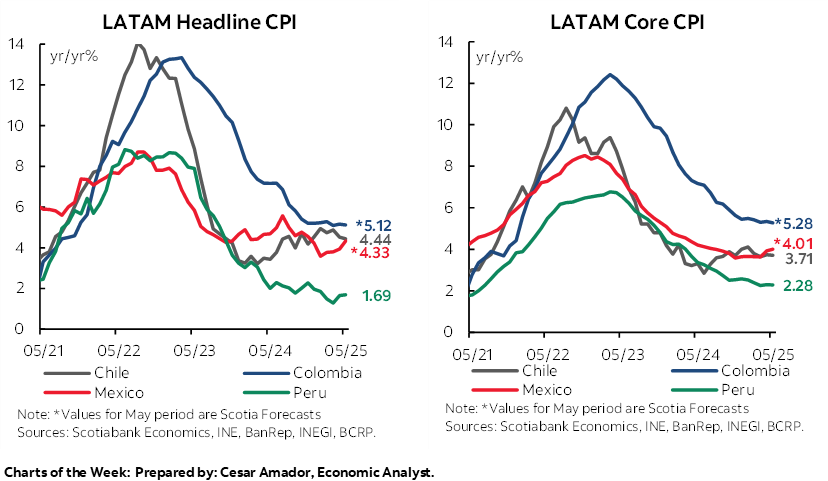

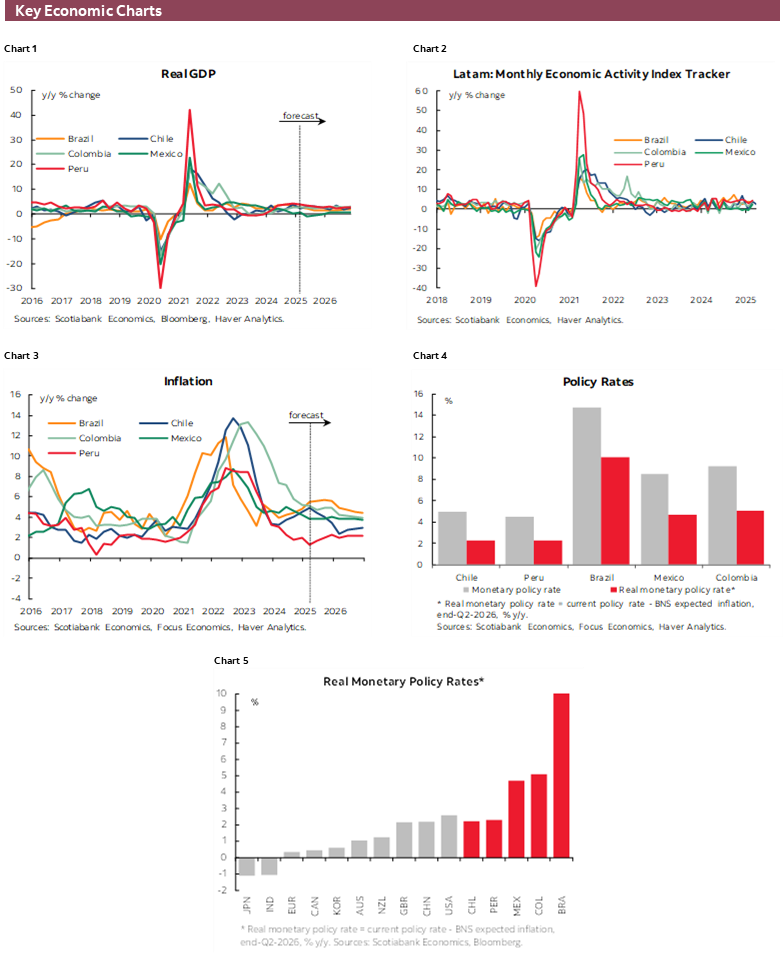

- Inflation is seen little changed above 5% in Colombia, accelerating in Mexico above 4% for the month after hot mid-May readings, and marginally slowing in Brazil while remaining in the mid-5s zone.

- In today’s report, we focus on Colombia’s external account balances, Mexico’s inflation trends and a slight retreat in economic pessimism, the case for a rate cut on the 17th in Chile, and recent macro figures and fiscal developments in Peru.

PACIFIC ALLIANCE COUNTRY UPDATES

- We assess key insights from the last week, with highlights on the main issues to watch over the coming fortnight in the Pacific Alliance countries: Chile, Colombia, Mexico and Peru.

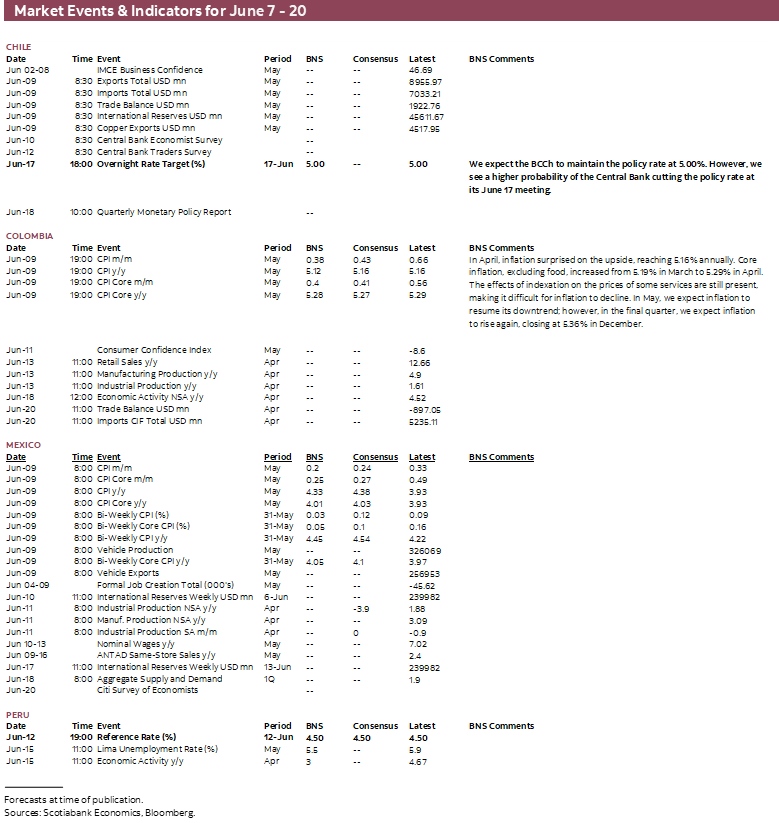

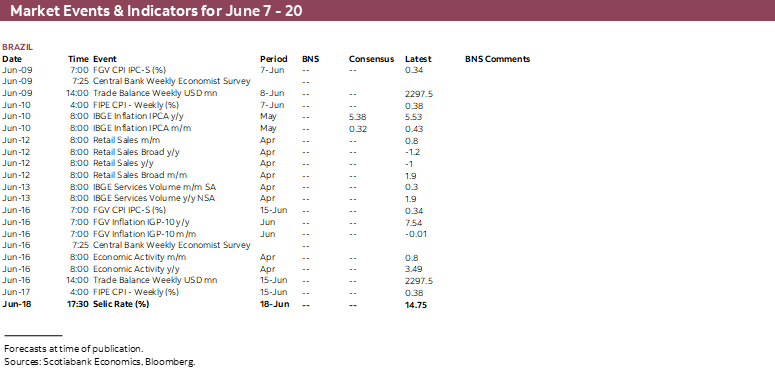

MARKET EVENTS & INDICATORS

- A comprehensive risk calendar with selected highlights for the period June 7–20 across the Pacific Alliance countries and Brazil.

Chart of the Week

ECONOMIC OVERVIEW: CPI WEEK, BCRP DECISION

Juan Manuel Herrera, Senior Economist

+52.55.2299.6675

juanmanuel.herrera@scotiabank.com

- Key CPI releases await in the Americas, with readings out of Colombia, Mexico, Brazil, and the U.S. all on tap. The BCRP kicks off the June cycle of Latam central bank decisions with a likely hold at its Thursday announcement.

- Inflation is seen little changed above 5% in Colombia, accelerating in Mexico above 4% for the month after hot mid-May readings, and marginally slowing in Brazil while remaining in the mid-5s zone.

- In today’s report, we focus on Colombia’s external account balances, Mexico’s inflation trends and a slight retreat in economic pessimism, the case for a rate cut on the 17th in Chile, and recent macro figures and fiscal developments in Peru.

Key CPI releases await in the Americas, with readings out of Colombia, Mexico, Brazil, and the U.S. all on tap, with China also joining in on the fun at the start of the week, while Peru’s central bank decides on policy. China will also publish international trade data for May that will give us a first ‘official’ look into how the U.S.-China tariffs détente may have supported trade between the two nations. Of course, the rollercoaster of trade headlines and developments will likely continue to take markets for a ride, as a one-month countdown to the end of the reciprocal tariffs pause begins at the start of the week.

Starting with Colombia, inflation in both headline and core terms is expected to remain relatively unchanged, around 5.1%–5.2% and 5.3% respectively in May. Headline prices growth in the country has held in a fairly narrow range since last November, sitting between 5.1% and 5.3%, as indexation price rises at the start of the calendar year keep inflation ‘sticky’. Core inflation has shown a bit more progress, falling from 5.9% in November to as low as 5.1% in March. But, the rise to 5.3% in April and likely only a small decline in May has pumped the brakes on its deceleration, as indexation factors also play a role. Strengthening consumption may also be applying some pressure, as domestic demand seems to be on an improving trajectory, reflected in current account data that our local team highlights in today’s report which shows strength in consumer goods imports.

Beyond Monday’s CPI release, local markets will be paying very close attention to fiscal developments, with one week to go until the government releases its medium-term fiscal plan (MFMP) on June 13th—and the outlook is not favourable. From our team in Colombia: from a 5.1% of GDP deficit estimate presented in the financial plan, the MFMP is expected to outline a higher projection. The government is reportedly seeking a strategy to have a larger fiscal deficit this year without severe consequences. Colombia’s fiscal rule has a mechanism to justify noncompliance in unforeseen circumstances, and these are the famous escape clauses (used during the pandemic). If the activation of the escape clause is approved, the government must justify whether there are extraordinary events that compromise the country’s macroeconomic stability and justify the suspension of the fiscal rule mechanism, something we see as impractical, as we are not in a scenario that warrants it. We estimate a total fiscal deficit of between 6.0% and 7.4% of GDP in 2025, with increases in additional borrowing needs of between COP 20 trillion and 48 trillion.

In Mexico, H1-May CPI data had already shown a hefty acceleration in inflation from 3.9% to 4.2%, and economists now expect that H2-May inflation will rise to about 4.5% . However, while the rise in headline inflation in H1-May was primarily driven by non-core items, H2-May price growth will also include upward pressures in core inflation which is seen climbing above 4% in the bi-weekly and monthly readings. As the team in Mexico discusses in today’s Weekly, the minutes to Banxico’s latest meeting showed that some officials are concerned about goods inflation—and next week’s data are likely to add to their worries. On the flip side, and as discussed today also, pessimism around Mexico’s economy is slightly in retreat (although the outlook remains poor) thanks to a cooling of trade risks, but there remain a lot of unknowns. However, a visit by President Sheinbaum to the G7 meeting in Canada (an invite which she has yet to accept) in a couple of weeks could lessen risks if USMCA leaders agree to additional tariff reductions. Mexico retaliating against the latest U.S. metals tariff hikes would, of course, pull in the other direction.

Turning to Brazil, economists project a slight cooling of inflation, from 5.53% to 5.4% in May, right in line with the IPCA-15 (mid-month) inflation reading thanks to decelerating food and transportation price gains. With inflation picking up speed from last year’s low of 3.7% in April 2024 to the mid-5s zone more recently, an upside surprise in next week’s release may further tilt the balance in favour of a final BCB 25bps hike at its June 20th decision; with markets pricing such a move at about 80% odds. Local markets will also monitor fiscal news in the country, with Finance Minister Haddad possibly unveiling a fiscal package to replace a proposed tax hike on financial transactions that drew heavy resistance from private and public players. Also of note, former president Bolsonaro faces questioning by the country’s Supreme Court starting on Monday on accusations of plotting a coup following the 2022 elections. Although Bolsonaro is banned from running in Brazil’s 2026 election, polls that list him as a potential candidate (which he claims he is) show him tied in a head-to-head matchup against incumbent Lula, with 41% of those surveyed supporting each candidate. The evolution of the trial may inject some intrigue into expectations and polls for next year’s vote.

Our economists in Lima briefly discuss their expectations for next week’s BCRP decision in today’s Weekly. Peru’s central bank has surprised us and markets on multiple occasions during their current easing cycle, cutting when expected to hold or holding when expected to cut. Thursday’s announcement looks easier to call than in the past, with our team penciling in a rate hold at 4.50% as do all but one economist (expecting a 25bps cut) among those polled by Bloomberg. The focus will squarely fall on what guidance the Velarde-led central bank may offer given a very narrow bandwidth for additional cuts. In today’s publication, we also provide an update on recent macroeconomic figures in Peru which point to a sizeable slowing of GDP growth in April, albeit with a strong calendar drag behind that month’s readings that means we may have to wait until May data to get a better feel of baseline growth dynamics. Finally, as for many in the region, fiscal accounts are getting a lot of attention, and so the team discusses the latest developments on this front with Peru’s newly-appointed Fin Min recently lifting the country’s fiscal ceiling for 2025.

Chile’s calendar will probably not turn many heads next week, with only the release of the BCCh’s economists and traders surveys results and international trade data for May on tap. Still, it’ll be interesting to track a possible shift in rate cut expectations among economists and those in markets with only about ten days to go until the next BCCh decision. While markets are only pricing in less than 20% chance of a rate cut, there is a chance that officials opt for a cut. In the May BCCh survey, only about one-in-six economists expected that the BCCh would cut at the June 17th decision (odds are that more will pencil in a cut). Our economists in Santiago outline the possible reasons for the central bank to choose to ease policy for the first time since December 2024, when it last cut by 25bps to the current rate of 5.00%.

PACIFIC ALLIANCE COUNTRY UPDATES

Chile—Why Would the BCCh Cut Rates on the 17th Alongside Upside Revisions to Growth Forecasts?

Anibal Alarcón, Senior Economist

+56.2.2619.5465 (Chile)

anibal.alarcon@scotiabank.cl

The minutes of the April 29th meeting revealed that the options the Board considered at that time were to maintain the policy rate at 5.00% or reduce it by 25 bps, following two meetings (in January and March) where it considered maintaining the rate at 5% to be the only plausible option. In fact, since the January 28th meeting, the Central Bank had maintained a neutral bias for the path of the monetary policy rate, stating that it would “evaluate the next steps in the monetary policy rate”.

So, what would be the options at the June 17th meeting? The first would be to maintain the rate at 5.00%, as has been the case for several months, while the second would again be to reduce the policy rate by 25 bps. In our view, the cut gained more probability within the Board given the new information and would be the consensus option at this meeting for tactical and risk management reasons. The arguments are summarized below:

- The Central Bank would revise upward its GDP forecast for 2025, driven by upward surprises in the external sector and likely upward adjustments in domestic demand due to improved investment prospects. The recovery is highly heterogeneous across sectors. On the supply side, the external and primary sectors, along with mining, are recovering, while the sectors most sensitive to the monetary policy rate remain weak. In terms of spending, consumption would see a seasonally adjusted contraction in Q2-25.

- Indeed, in Q2, goods consumption is expected to be marginally negative on a seasonally adjusted basis, given the reversal in purchases by foreigners and residents, whose consumption has not yet accelerated.

- April labour market data showed significant job losses, especially among salaried workers, widespread across sectors. This makes the overall activity cycle less compatible with the diagnosis of labour market weakness at the margin.

- Core inflation (ex-volatiles) has surprised to the downside since last March’s IPoM. A negative surprise of 0.2% has accumulated in core CPI from March to May. This would allow the Central Bank, in its new baseline scenario, to reduce projected core inflation from 3.5% in the March Monetary Policy Report (IPoM) to around 3.2% in the June IPoM (by incorporating CLP appreciation and weaker consumption in Q2-25). Regarding headline inflation, we anticipate a marginal cut in the bank’s 3.8% inflation projection for 2025, given that the negative surprise to date must be incorporated, as well as the impact of the electricity rate hike, which we expect to occur in the July CPI release. At Scotiabank, we maintain our inflation projection of 3.5% y/y through December 2025.

- The Real Exchange Rate is around 103 (base index 100 = 1986), similar to February of this year, while the multilateral exchange rate is at levels similar to March. Inflationary pressures on tradable goods are not particularly significant.

- The external scenario remains highly uncertain, a factor sufficient to justify, for risk management purposes, a gradual, phased approach to a neutral policy rate by Q1-26.

- Before the Fed? Yes, this time. As a sign of independence from external monetary policy, the Central Bank would demonstrate its ability to take significant (albeit limited) steps before the Fed, absorbing the shock (depreciation of the CLP) that we hope will be limited.

- This will be a limited surprise for market rates, given that we do not expect a particularly dovish statement or rate corridor, but rather a tactical cut decision justified by the widening external risks and the medium-term global slowdown.

- Finally, cutting the policy rate and having a negative CPI in June will give greater validity to the early decision in the face of the Central Bank’s communication.

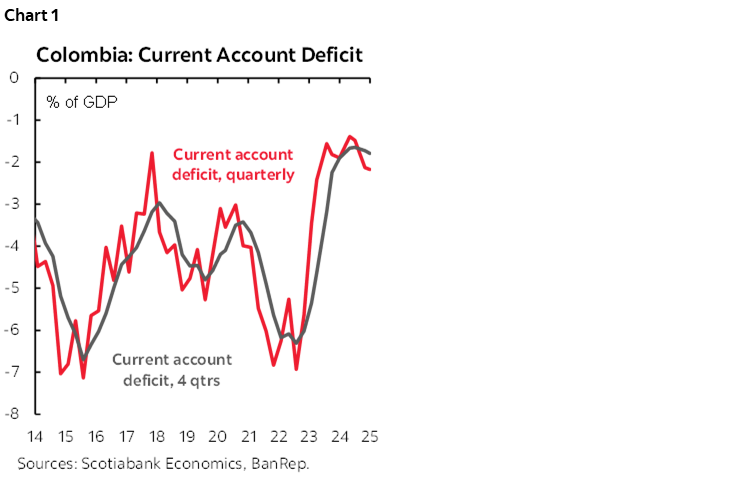

Colombia—The Current Account Deficit is Widening, Reflecting Improved Domestic Demand

Daniela Silva, Economist

+57.601.745.6300 (Colombia)

daniela1.silva@scotiabankcolpatria.com

On Tuesday, June 3rd, the central bank (BanRep) released the Q1-2025 Balance of Payments (BoP) report. The current account deficit stood at USD 2.29 billion, equivalent to 2.2% of GDP, the highest since Q2-2024 (chart 1). Compared to Q4-2024, the current account deficit widened by US$32 million (0.04% of GDP). The increase in the current account deficit is part of a recovery in domestic demand explained by a higher trade deficit but offset by a lower net outflow in the income account, and the continued favourable inflows of remittances.

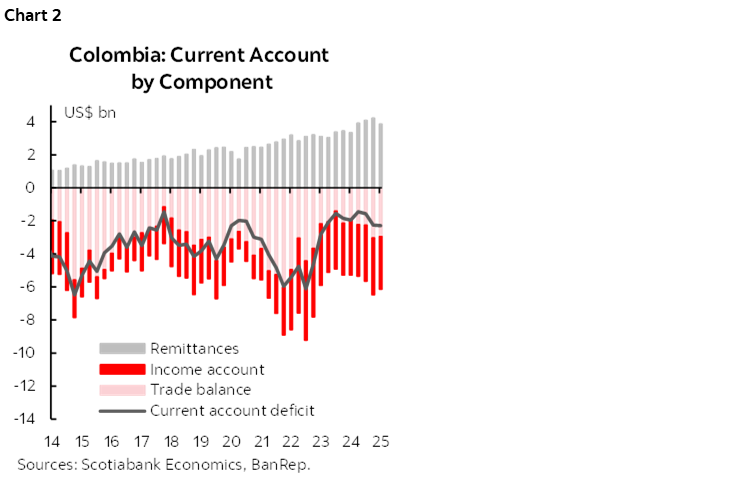

The current account deficit is a sign that economic activity continues to recover. The trade deficit widened by 52% compared to the first quarter of 2024, reaching US$2.94 billion, with 10% annual growth in imports and 5% in exports. What has been evident in foreign trade figures is that imports of consumer goods have increased, suggesting improved dynamics in domestic demand.

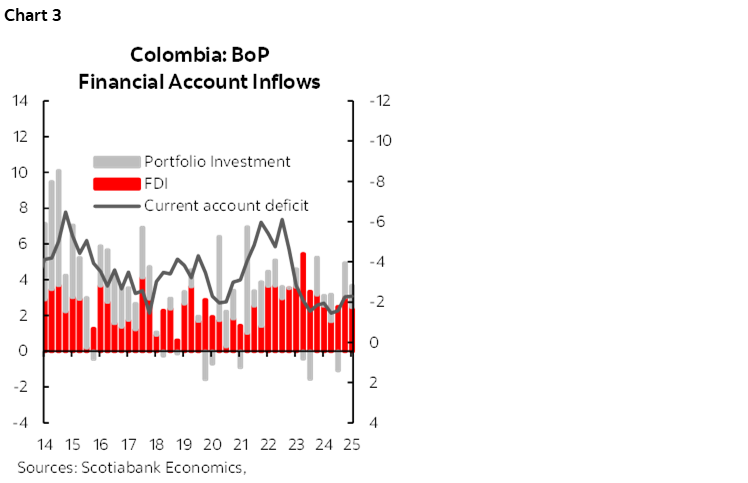

In terms of financing, net FDI inflows decreased compared to the previous quarter, reaching US$3.14 billion (-29% q/q). FDI was concentrated in the mining and oil sectors with 36% of total inflows, followed by the financial services sector with 22%. Meanwhile, in the case of portfolio investments, US$1.2 billion was received, representing a decrease compared to the previous quarter but an increase of 107% compared to the first quarter of 2024, reflecting greater appetite for local currency debt.

On the FX side, the structure of the balance of payments suggests that no fundamental behavior explains the currency’s current resilience. The exchange rate remains below the level suggested by fundamentals, primarily due to the inflow of carry trade operations due to the expectation of a higher BanRep rate and lower transaction flows from local agents. In the medium term, our expectation of a widening current account deficit, the low price of oil, and complex local fiscal outlook, would support a further depreciation of around 4.350 pesos by the end of 2025.

Current account:

In Q1-2025, the current account deficit stood at USD 2.29 bn (2.2% of GDP), increasing by 1.4 q/q and 17.8% y/y. In annual terms, the trade deficit widened significantly, with slightly higher revenue accounts and increased transfers.

- Trade balance: In the first quarter of 2025, the trade deficit was USD 2.94 billion, a 52% y/y increase (chart 2). Exports increased by 5% y/y, with non-traditional exports growing by 16% y/y in Q1 and coffee exports growing by over 100%. However, on the downside, oil exports have been affected by low international prices. On the other hand, imports increased by 10%, reflecting the improved dynamics of domestic demand, with a 6.6% annual increase in the import of consumer goods. Additionally, a surplus in services of USD 145 million related to good tourism dynamics.

- Income account: Outflows stood at USD 3.19 billion, remaining relatively stable compared to the previous quarter. Compared to a year earlier, the income account deficit was USD 150 million lower, mainly explained by lower interest payments on external loans and an increase in income from Colombia’s investments abroad. On the other hand, profits for companies with FDI in Colombia increased, especially in financial and business companies and the commerce and hotel sectors.

- Transfers: Inflows of USD 3.8 billion were received in the first quarter, 15.5% (US$518 million) higher than in Q1-2024. Remittance inflows stood at US$3.1 billion, equivalent to 2.9% of GDP and 13.2% of current balance of payments revenue. Remittance inflows increased by 15.1% y/y.

Financial account:

The financial account recorded net inflows of US$1.83 billion (1.7% of GDP), US$234 million higher than in Q1-2024. The economy is struggling to find traditional sources of financing, which contributes to the expectation of more pressure on the depreciation of the FX than appreciation.

- Foreign Direct Investment: In Q1-2025, FDI inflows stood at US$3.14 billion (3.0% of GDP), decreasing by 14.7% y/y (chart 3). The main sectors receiving FDI were oil and mining (36%), financial services (22%), and manufacturing (13%). Approximately 44% of FDI was due to new capital investments, while 41.4% was due to reinvestment of profits.

- Portfolio investments: In the first quarter of 2024, Colombia recorded capital inflows of USD 1.21 billion (1.1% of GDP), a higher inflow than in the same period of the previous year. Debt issuances in the local market (USD 1.03 billion) were the main drivers of this growth.

Mexico—Scaling Back Pessimism; Inflation Jump in May

Rodolfo Mitchell, Director of Economic and Sectoral Analysis

+52.55.3977.4556 (Mexico)

mitchell.cervera@scotiabank.com.mx

Brian Pérez, Quant Analyst

+52.55.5123.1221 (Mexico)

bperezgu@scotiabank.com.mx

Miguel Saldaña, Economist

+52.55.5123.1718 (Mexico)

msaldanab@scotiabank.com.mx

This week, investment and consumption indicators offered some relief, despite an overall weak outlook. Gross fixed investment in March softened its annual decline (-0.2% y/y), while consumption rebounded in the same month (1.2%). However, on a sequential basis, investment rose month-over-month (0.3% m/m), while consumption continued to drop (-0.2% m/m). However, formal employment in May decreased on a sequential basis (-47 k), showing its weakest may since 2009—excluding the 2020 lockdown—(0.1% y/y), but also the total number of employers was down, showing a declining annual trend (-2.8%).

Also, this week, the OECD revised Mexico’s growth forecast upward, from -1.3% to 0.4% for 2025. The revision did not generate much optimism among analysts, mainly because the change is based on assumptions about trade tensions. In contrast, the results of the Citi Survey remain unchanged, with a 0.1% GDP consensus for 2025. Additionally, a week earlier, the Bank of Mexico revised its forecast downward to 0.1% from 0.6%, with a range between -0.5% and 0.7%. Overall, we believe the wide range of forecasts is mainly due to trade uncertainty, as model outcomes depend on the assumptions they are based on. Initially, the OECD anticipated greater trade tensions in the region, along with tariff measures due to unilateral changes in U.S. policy. However, since then, several tariff pauses have been achieved, and Mexico’s response has been measured.

Nevertheless, the imposition of an additional 25% tariff (50% total) on steel and aluminum by the U.S. this week reminded us that risks and uncertainty remains. According to estimates from our Toronto team, this would imply an effective tax rate of 12% on total imports. The rate would rise by 5.9% on Mexican imports and 5.7% on Canadian imports (see Daily Points).

Trade has been the main external factor injecting uncertainty this year, but tariff negotiations will soon also include partners’ interests in reviewing the USMCA. In this regard, the invitation from Canadian Prime Minister Carney to President Sheinbaum to attend the G7 summit from June 15th to 17th becomes relevant. Canada’s stance on the treaty review remains unclear, as does whether it will seek to join forces with Mexico to negotiate trade relations with the U.S. jointly. So far, there doesn’t appear to be a unified bloc, but the invitation is certainly seen as a gesture of openness to various possibilities.

Regarding domestic factors, the judicial election has also been a source of uncertainty, although the market largely overlooked the initial results. For now, rate movements seem driven by international conditions, though domestic risks remain significant. While the initial election results appear to have had no immediate impact on valuations, we believe their economic impact will be more long-term, beginning once the new officials take office in September. Meanwhile, investors continue to question fiscal sustainability and the feasibility of meeting the deficit target set by the Ministry of Finance for this year. In this regard, rumours of a new Pemex restructuring have brought some optimism to investors, and it will undoubtedly be a key topic in the coming months, along with fiscal performance and potential changes in credit rating agency outlooks.

Next week, the most relevant indicator will be May’s inflation reading, which analysts expect to rise annually to 4.37% (3.93% previous), along with the core component at 4.02%, mainly due to an acceleration in goods prices. This reading will be particularly important for gauging future monetary policy moves. Although the Bank of Mexico’s Governing Board roughly signaled in its last policy decision that it would implement another 50 basis point cut in June, the meeting minutes revealed some members’ concerns about the rebound in goods prices and the potential rise in inflation expectations. Therefore, while decisions may no longer be unanimous, we don’t believe June’s cut will be the last of the year. A reading above consensus would likely prompt upward revisions to year-end inflation expectations and complicate the central bank’s decisions in the second half of the year. We expect a year-end rate at 7.50%, in line with consensus. Other indicators to be released include May’s automotive production and export data, where we expect continued annual declines, affected by U.S. trade tensions and changes in automakers’ production strategies.

Peru—Macro Data and Events is a Mixed Bag, but Overall Good

Guillermo Arbe, Head Economist, Peru

+51.1.211.6052 (Peru)

guillermo.arbe@scotiabank.com.pe

We expect the BCRP to maintain its reference rate at 4.50% at its meeting next Thursday, June 12th. However, we are interested in seeing what the BCRP might signal in its statement with regard to future action. For now, 4.50% continues to be our terminal rate. Past statements have been somewhat ambiguous as to the BCRP’s willingness to go lower. Its statement next Thursday could shed more light on this. There is little margin for further cuts, however, as the real reference rate is very near neutral, so the downside risk seems limited to a possible additional 25bps cut.

Information regarding April GDP has been trickling in and it has been decidedly mixed. While metals mining GDP rose a robust 8.5%, y/y, in April, fishing GDP fell 20%, and oil & gas was down 4.4%. Other leading indicators were generally positive, but weaker than previous months. All in all, we see GDP growth of around 2.7%, y/y, for April. This, of course, is much lower than the 3.9% growth that took place in Q1. This is not, however, a sign of a slowing economy, but, rather, reflects the impact of two less working days due to calendar shifts for Easter in 2025 (April) versus 2024 (March). By the same standard, GDP growth for Q1-25 near 4% overstated the strength of the economy. Growth in May should be a better indicator of the health of GDP growth.

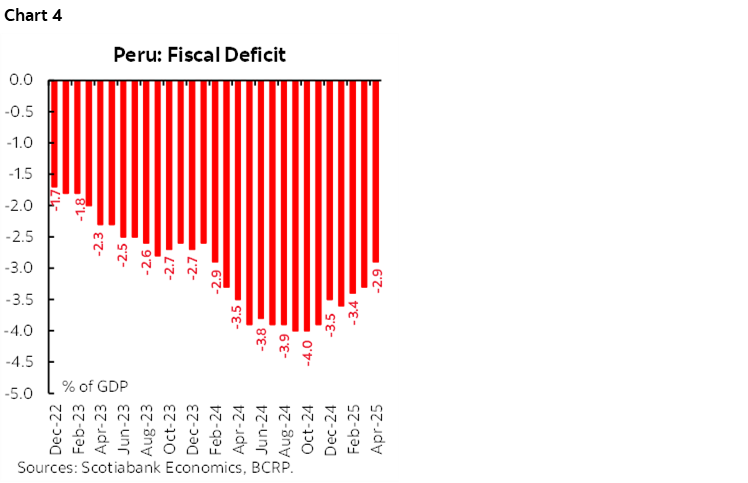

On another note, there has been a lot of noise domestically surrounding Peru’s fiscal situation. Although Peru’s fiscal deficit fell significantly, to 2.9% of GDP in March 2025 (chart 4), from a high of 4.0% in October 2024, news emanating both from Congress and the Ministry of Finance has given the local market analysts something to think about. Congress approved a law that would double the portion of the 18% sales tax that goes to municipal governments from 2% to 4%, leaving the central government with that much less spending power. This in itself could be viewed as simply a transfer of revenue from one government hand to another. However, since there is no concurrent transfer of responsibilities, one can argue that municipal governments will spend the additional resources because they can, but the central government will not be able to spend less at the same time, thereby inflating the government deficit.

Nearly coincident with this, the new finance minister, Raúl Pérez Reyes, said that the legal 2.2% of GDP debt ceiling for 2025 would be raised to 2.8% of GDP. This has rubbed a lot of local economists the wrong way, for what it implies regarding fiscal control. Our view is that Peru’s fiscal situation continues to be manageable despite these changes. In fact, the new fiscal ceiling of 2.8% (which may not be reached, given poor state spending capacity) is still lower than our 3.3% GDP growth forecast, so does not really threaten fiscal accounts per se. The underlying issue is that municipal governments have a poor history of resource management and execution capabilities. Peru’s overall state budget management and execution is not a well-oiled machine, and to take resources from one government format that works better, to another that works less well risks generating greater fiscal concerns over time.

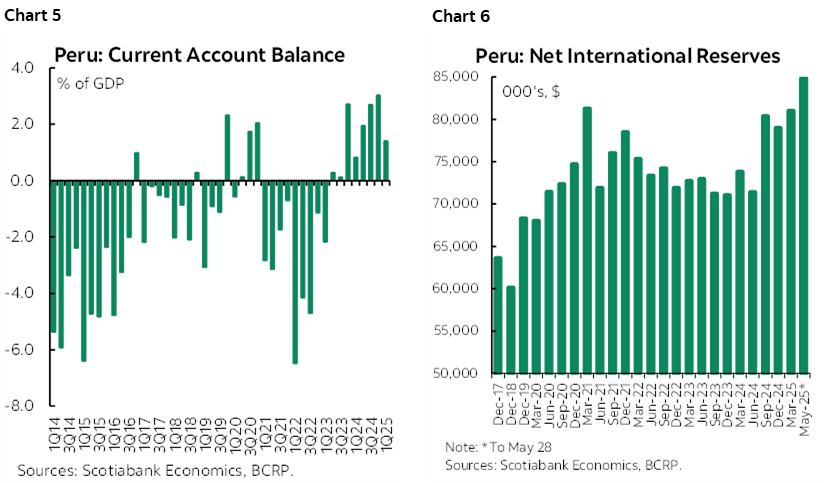

To end on a positive note, Peru’s external account balances are soaring. The current account surplus was 2.2% of GDP in Q1 (chart 5), and, significantly, has been positive for eight quarters running. Note that a positive current account is not automatic when copper prices are strong, as high metals exports can be considerably countered in balance of payments accounts by profit outflows from foreign mining companies. What is happening suggests that the trade balance is so strong that it is offsetting accounting outflows of profits. This situation has continued in Q2, judging from the continual strong rise in net international reserves in recent months (chart 6).

| LOCAL MARKET COVERAGE | |

| CHILE | |

| Website: | Click here to be redirected |

| Subscribe: | anibal.alarcon@scotiabank.cl |

| Coverage: | Spanish and English |

| COLOMBIA | |

| Website: | Click here to be redirected |

| Subscribe: | jackeline.pirajan@scotiabankcolptria.com |

| Coverage: | Spanish and English |

| MEXICO | |

| Website: | Click here to be redirected |

| Subscribe: | estudeco@scotiacb.com.mx |

| Coverage: | Spanish |

| PERU | |

| Website: | Click here to be redirected |

| Subscribe: | siee@scotiabank.com.pe |

| Coverage: | Spanish |

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.